Pork Wrap December 24

The hog and pork complex experienced another steady week. The

negotiated markets were essentially unchanged from the week before

and the cutout averaged $0.65 lower than the week before. In the

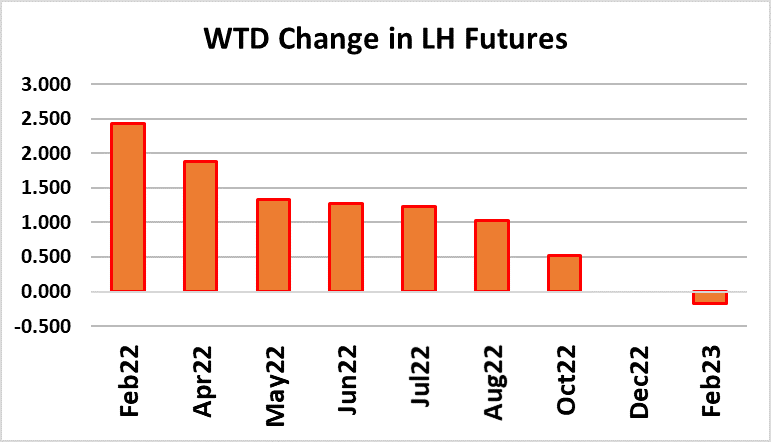

midst of this uneventful week in the cash markets, the Feb futures

saw fit to rally almost $2.50 and is now trading close to $12 over the

current LHI. That seems excessively wide. Are traders trying to tell

us something? The surge of bullishness in the futures could very well

be related to the escalating risk posed by the omicron variant and

traders may be saying that they would rather be long than short if

packing plants have to reduce production due to absenteeism

spawned by COVID infections. Hog futures react differently than

cattle futures to production restrictions because the cutout plays a big

role in hog pricing.

Production slowdowns will raise cutout values and thus also likely

raise the LHI. Any such slowdowns would certainly cause the hog

production pipeline to back up and reduce the price of negotiated

cash hogs, but the positive influence from the cutout on hog pricing

often overwhelms the negative effect from cash hog markets. There

also seems to be a general sense that pork demand is about to enter

into another upcycle and take prices higher. That is what the

combined margin has been pointing to, however this week it ticked a

little lower. It is definitely in the zone where it normally turns higher,

so it is natural to assume that the next move in pork will be up.

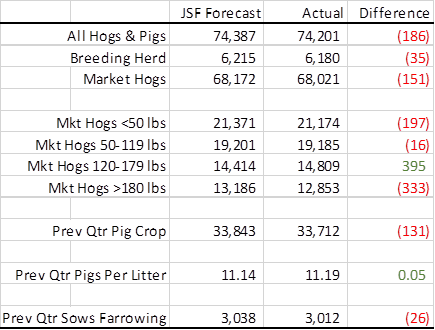

Futures traders will spend the holiday weekend digesting Thursday’s

Hogs and Pigs report. That report didn’t contain a lot of surprises, so

the market impact may be minimal. USDA reported the total swine

herd about 0.6% lower than what analysts were looking for, so that

might be considered mildly bullish. However, the breeding herd was

dead-on with the average trade guess and the breeding herd is the

engine that powers future hog supplies. The Sep/Nov pig crop was

estimated down 2.6% before USDA revised last year’s Sep/Nov pig

crop estimate upward. After that change, the pig crop was down

3.6%.

The revision to past numbers makes absolutely no difference to how

many pigs are on the ground right now. It only affects people’s

perception when they view the percentage change. The average

trade guess was for the Sep/Nov pig crop to be down 2.8%, so the

reported number was actually 0.2% larger than what analysts were

expecting. That should be mostly neutral to the market. The number

of pigs saved per litter bounced back up in the most recent quarter

and if producers can maintain the growth in that important productivity

measure, it would allow them to get more market hogs out of the

same sow base than what we’ve seen in the past few quarters. In all,

I think the H&P report shouldn’t be a big market mover on Monday.

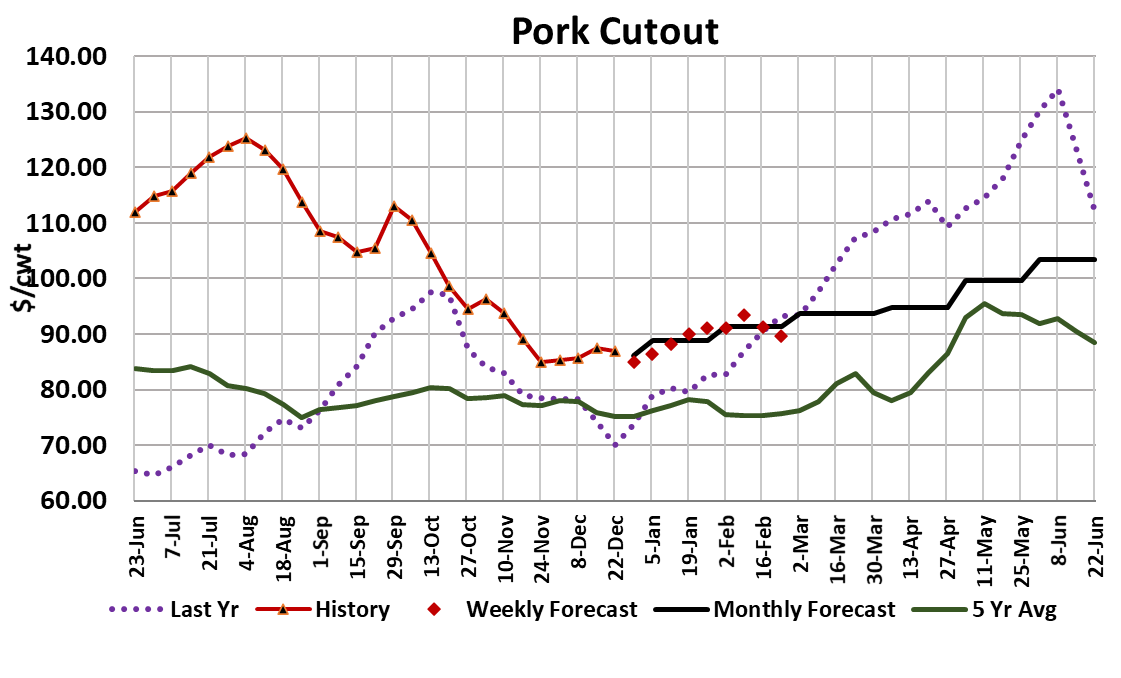

The numbers were a little smaller than what I had dialed in, so

when I included the new data it raised my 2022 price forecasts

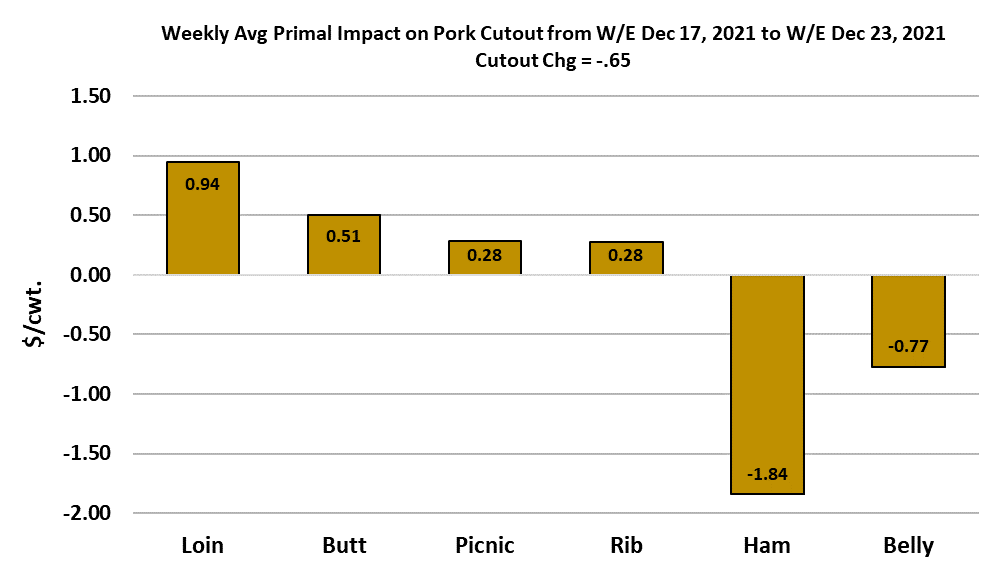

slightly. This week, it was gains in the retail items that supported

the cutout while the hams and bellies exerted downward pressure

on the cutout. In the end, it was almost a wash and the cutout

remains stuck in the mid $80s. If packers experience increased

absenteeism as COVID cases increase, then we might well expect

to see more day-to-day volatility in the pork cutout. It already

gyrates wildly depending upon what proportion of the ham volume

was boneless on any given day.

Further labor tightening will increase boneless product pricing

relative to the bone-in and thus make the swings even bigger on

days when the boneless buyers are active. The forecast over the

next few weeks has all of the retail items working higher and some

modest increases in belly pricing. Hams will likely be the laggard,

but by the middle of January they could be strengthening as well.

Trim markets also appear to be poised for increases in January.

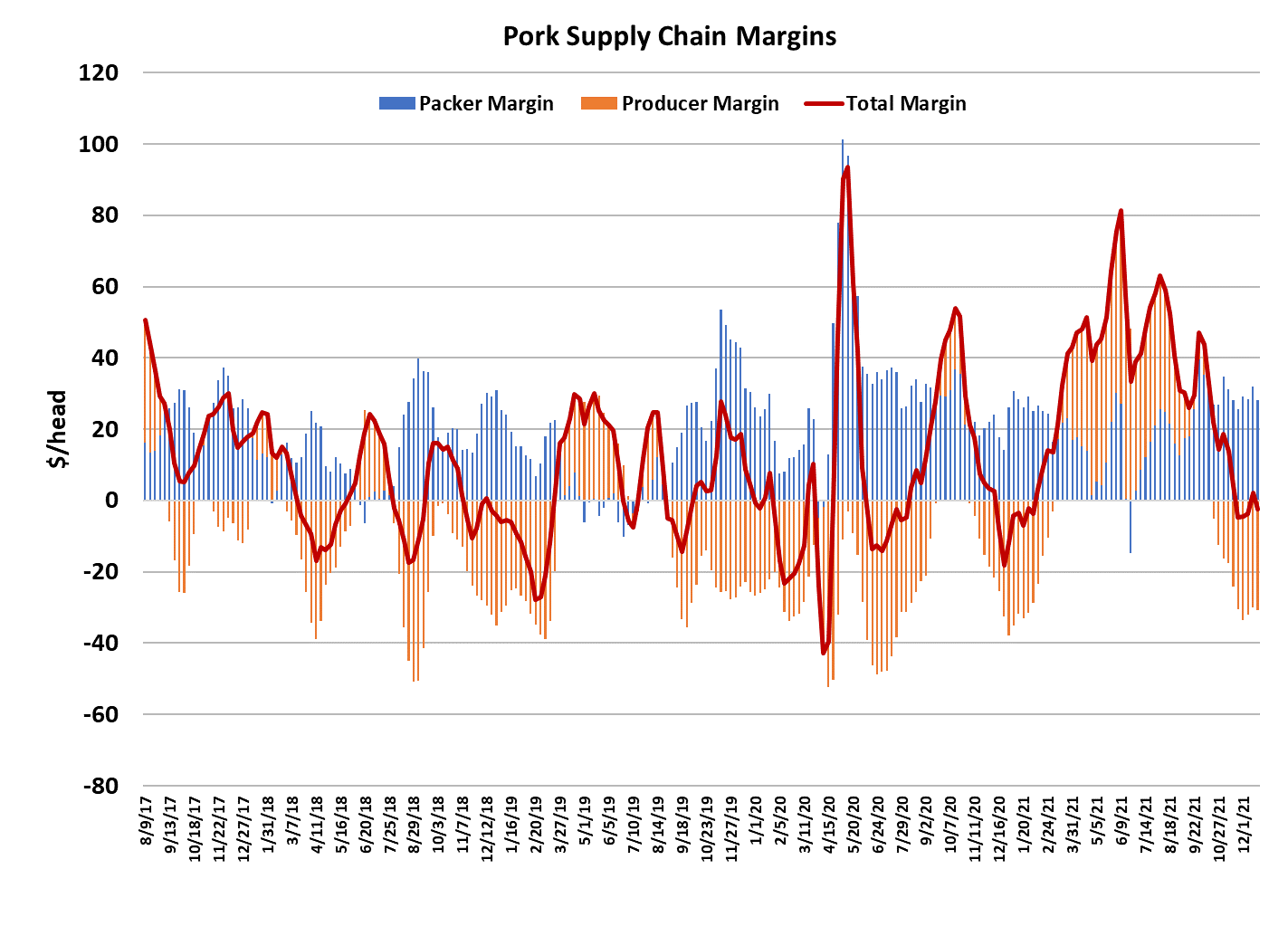

This week packer margins averaged about $28/head, down $4 from

the week before. I see margins stabilizing in the high $20s/low

$30s over the next month or so before they start to move below $20

in February. I’m expecting packers to only do a modest kill on

Christmas Eve and zero on Saturday to put the weekly total

somewhere close to 2.05 million head. Next week, 2.2 million is

expected and when we return to full production in the first week of

January, kills should be around 2.5 million head or slightly higher.

So far, the industry has over-killed USDA’s estimate of the summer

pig crop and that trend should continue in January unless covidrelated slowdowns disrupt harvest facilities. Hog carcass weights

are at their seasonal high point now, but pretty close to what was

expected.

It looks like the hog pipeline is filled, but not backed up. Export

demand still looks pretty weak compared to last year as China is

only buying a fraction of what they did last year at this time. I think

that is one of the things that has hog producers cautious about

expanding. The prospect of persistently high corn prices is

another. Futures corn traded over $6/bushel this week and we

haven’t even entered the season where traders normally start to

build in a risk premium for concerns about the next crop. With all

of the volatile weather around the globe, there will almost certainly

be floods, droughts, wind storms or some other phenomenon this

spring that will cause traders to bid up corn futures further. Next

week watch the news on COVID infections and the public’s reaction

to soaring case counts. That is the most important feature in this

market right now

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}