Pork Wrap December 23

The hog and pork complex was affected by the same holiday and

weather disruptions that plagued the cattle and beef complex this

week. Nasty winter weather doesn’t have as big of an impact on

hogs as cattle because the hogs are raised indoors in heated

facilities, but it does affect transportation of the animals, workers,

and packing plant operations also. As a result, the hog kill

plunged to a level way below what was anticipated simply due to

the holiday weekend. Coming into this week, I was expecting

slaughter to be in the 2.2-2.3 million head range and instead it

ended up at a paltry 1.77 million head, mostly due to sharp

weather-related kill reductions on Thursday and Friday. With

Saturday being Christmas Eve, that left packers no opportunity to

make up for the lost weekday kills. Instead, they will probably try

to pile more hogs into next Saturday’s kill. Even though all plants

will be dark on Monday, I see next week’s kill close to 2.15 million

head. In the meantime, pork production is way down and pork

buyers are likely to find pork availability fairly tight early next

week. The sharp reduction in pork production is already having

an impact on the cutout, as it printed just over $92/cwt. on Friday

afternoon. That was about $7 higher than where it was at the

beginning of the week. However, the cutout had been softening

early in the week before the weather hit, so the weekly average

was about $0.72 below last week’s average. Negotiated hog

markets also moved lower with the WCB cash market dropping

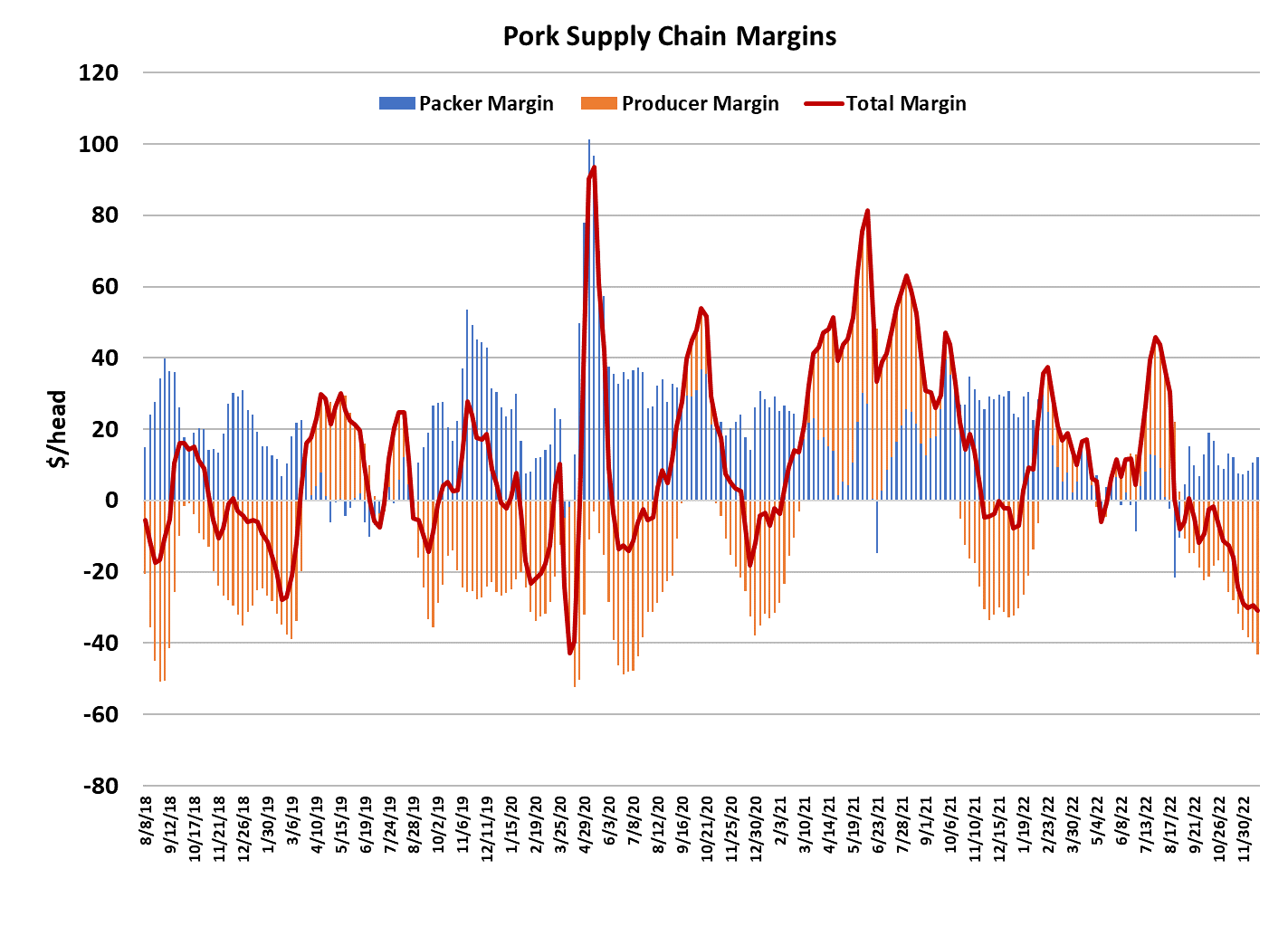

$1.68/cwt. on a weekly average basis. Packer margins improved

to a little over $12/head and that was their best margin since the

middle of October. The very small kill this week will likely help

packers regain some margin, but maybe only temporarily. It

should certainly take some pressure off of the negotiated market

and that has been a sore spot for packers for many months now.

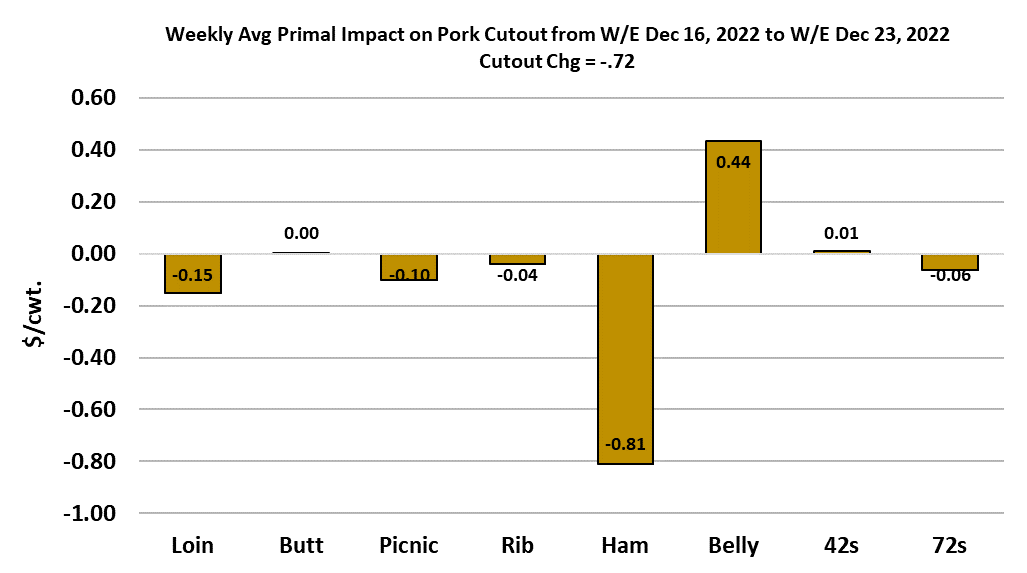

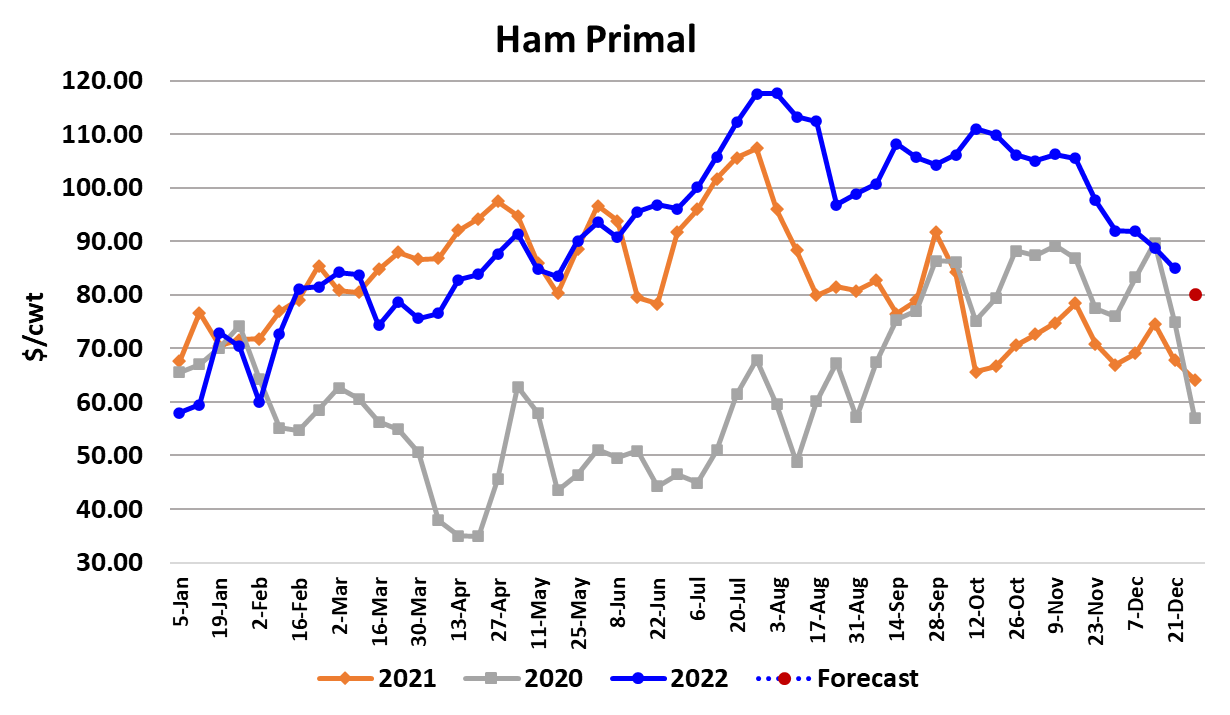

Even with all of the disruption, the cutout parts performed in line

with expectations. Hams moved lower, bellies a little higher and

the rest of the carcass was mostly sideways. The combined

margin was a little lower also, so we will probably have to wait

another week or two before a bottom appears. It is long overdue

and this downcycle has been particularly severe. I expect a new

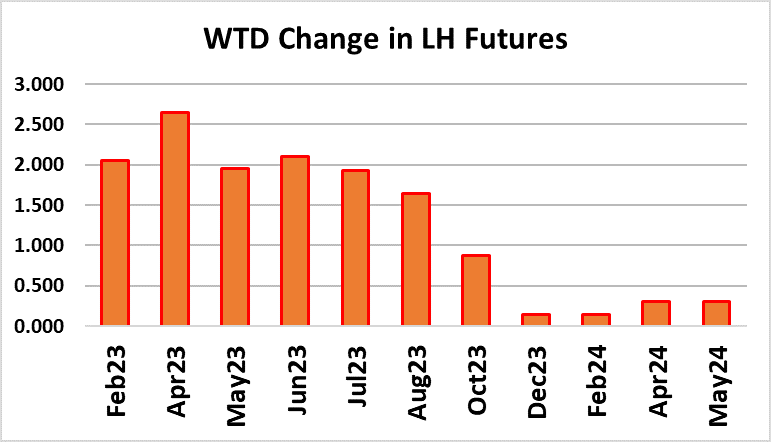

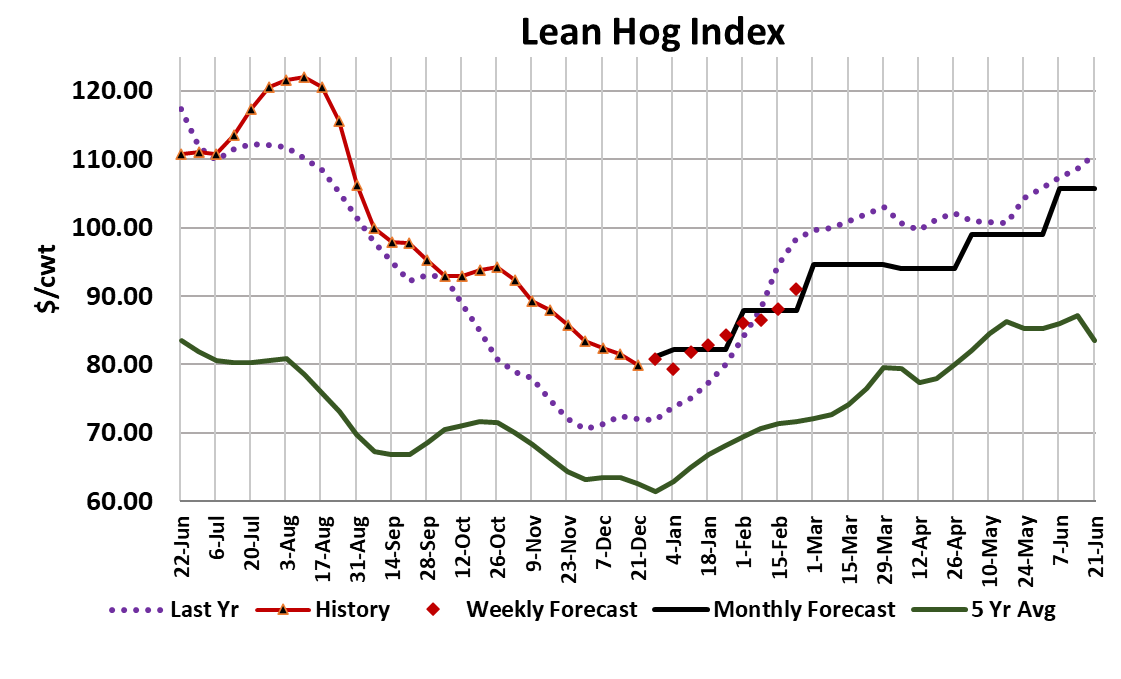

upcycle to take hold in early January. Futures traders tried to get

a jump on that this week when they rallied the Feb contract over

$4/cwt. on Wednesday and then added another $0.65/cwt. to that

on Thursday. The contract finished the week at $87.82, which is

a about $9 higher than the current level of the LHI near $78.50.

That big gain in the Feb priced it a couple of dollars higher than

what the fundamentals justify, in my opinion, but I can’t really

blame traders for getting excited about what might happen to

price levels as a result of a much smaller than expected kill this week.

A lot will depend on how pork buyers respond next week. Will they rush in

and bid up prices out of fears about availability? That is one possible

scenario. If the short kill fails to bring much lift to prices next week, then

that is probably a very bad sign. The weekly export data revealed a big

purchase by Mexico and if that goes through it will probably be very

supportive to the ham market in the near term. Even Mexican buyers

know that the best time to buy hams is in late December. Bellies haven’t

shown much life so far and that may be partly due to large freezer stocks.

USDA’s cold storage report showed belly stocks as of Nov 30 up 115%

YOY and at an identical level to the same period in 2019. For reference,

belly prices remained very low through the first couple of months of 2020

as a result. Thus, we might be wise to expect bellies to under-perform in

early 2023. Strong hams, weak bellies seems to be an ongoing theme in

this market. I suspect that if we ever do get a sharply higher belly quote

on solid volume then the futures will rally hard, no matter what level they

start from. USDA’s quarterly Hogs and Pigs report was released today

and it showed the US hog herd still contracting and very close to the level

that analysts were expecting. One exception was the breeding herd,

which had been projected to be down about 0.5% YOY and was actually

found to be 0.5% higher. That should portend hog supplies in the second

half of 2023 a little larger than what we thought heading into the report.

The Sep/Nov pig crop was reported down 1.3%, same as the Jun/Aug pig

crop was. Those are the hogs that will be slaughtered from March

through May and so we should expect kills to remain below last year until

at least summer. Productivity as measured by pigs per litter and sows

farrowing, was a little stronger than analysts expected. There was

certainly no suggestion of serious disease problems in those numbers. In

all, it was a pretty benign H&P report. Next week, watch for tight pork

supplies to lift the cutout, at least temporarily. If it doesn’t, that would be a

pretty serious concern.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}