Pork Wrap December 22

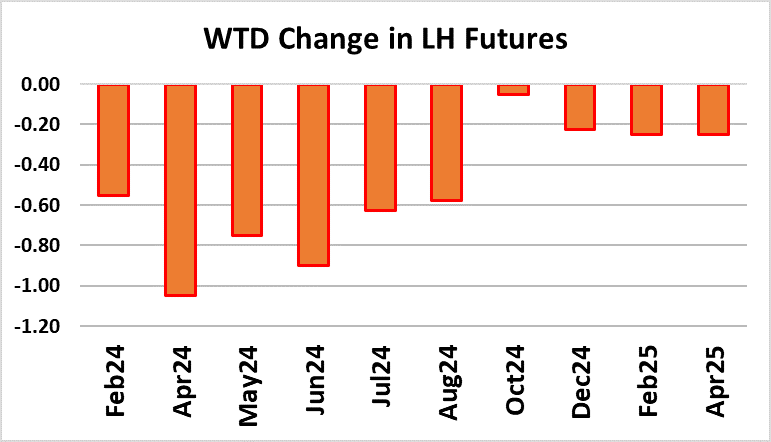

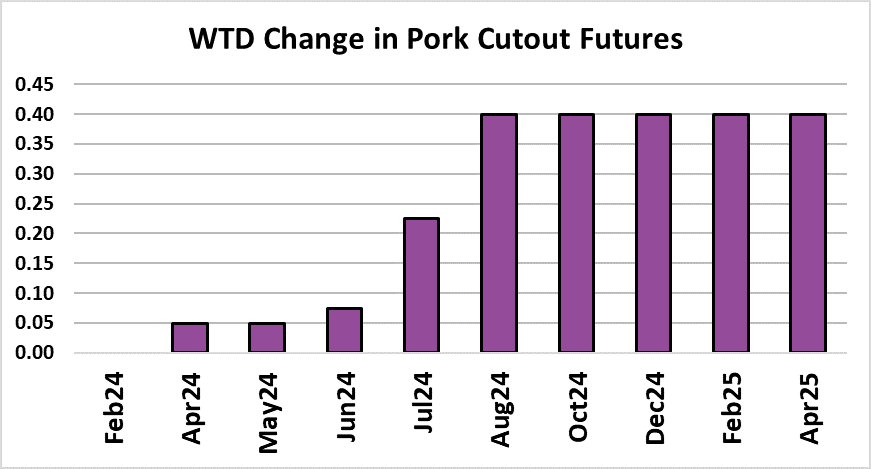

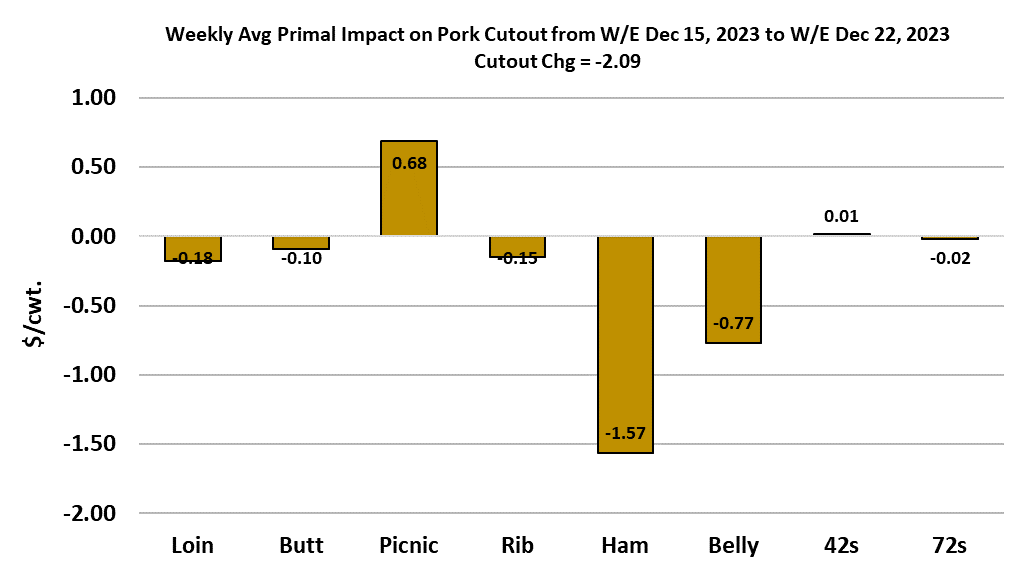

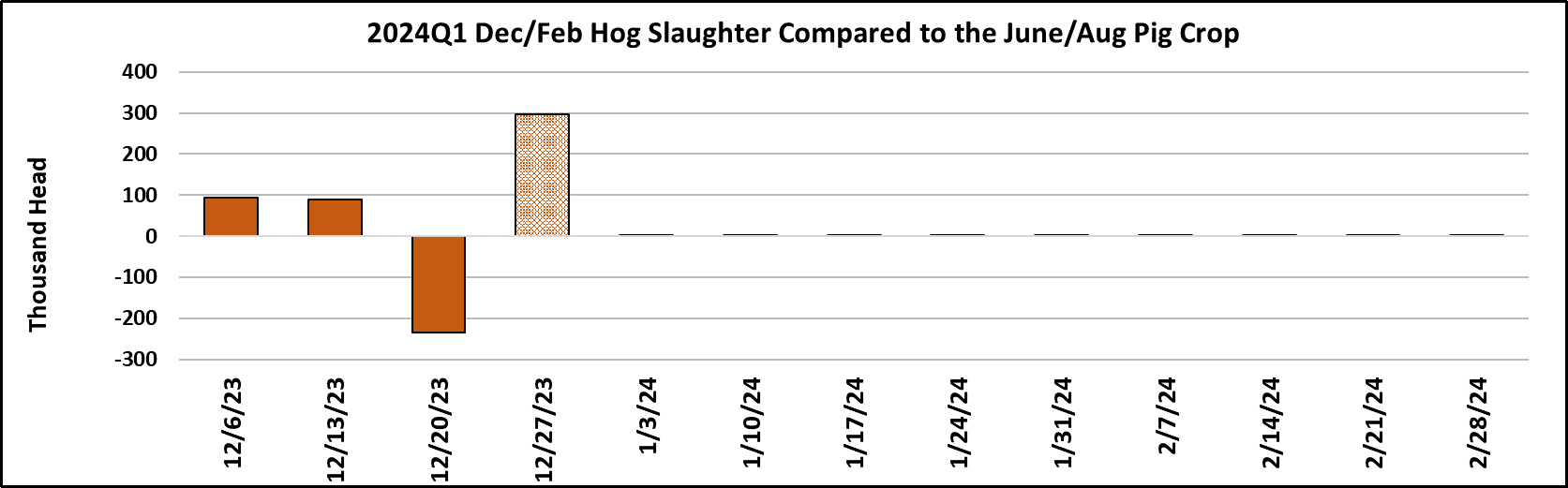

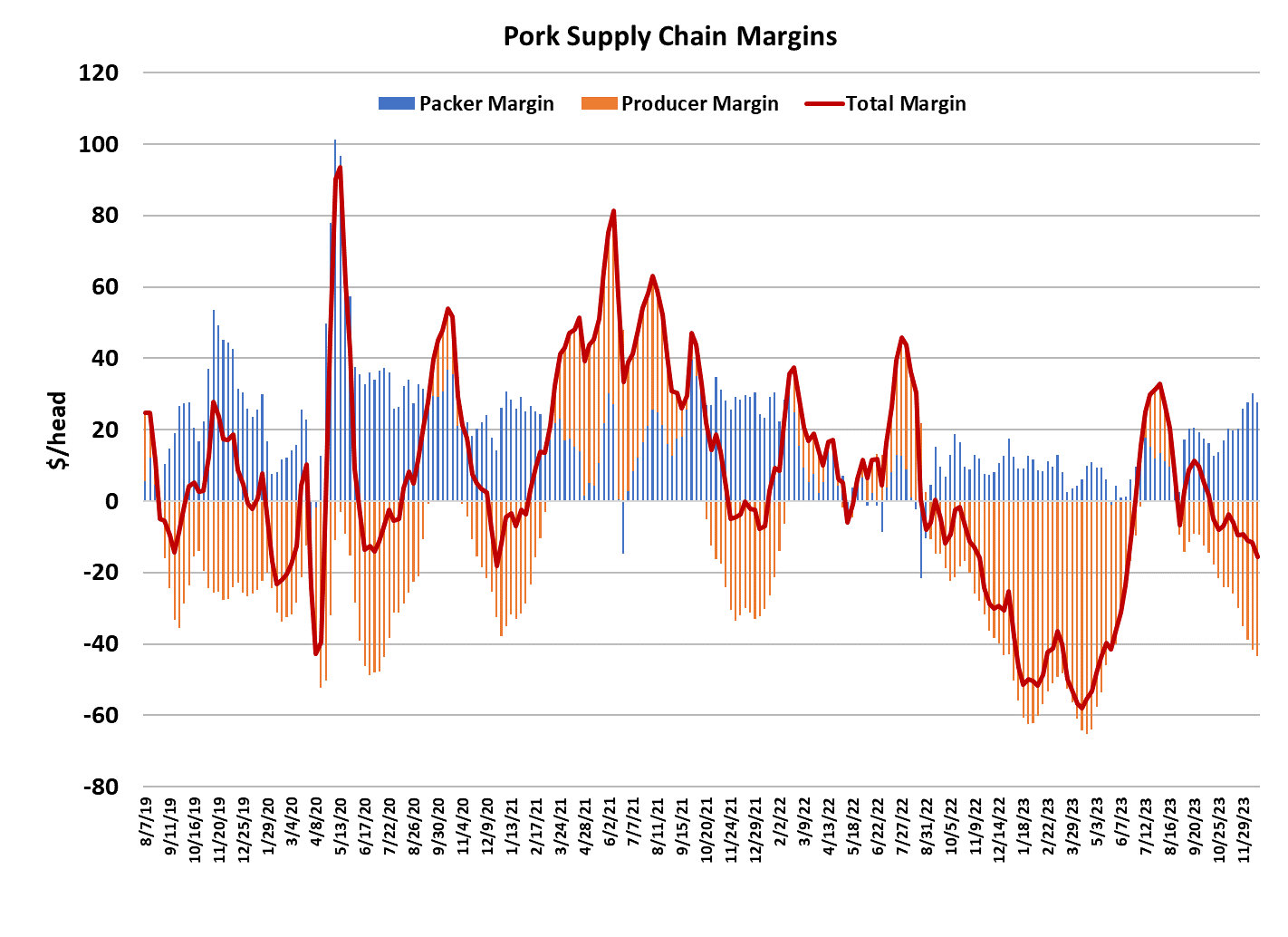

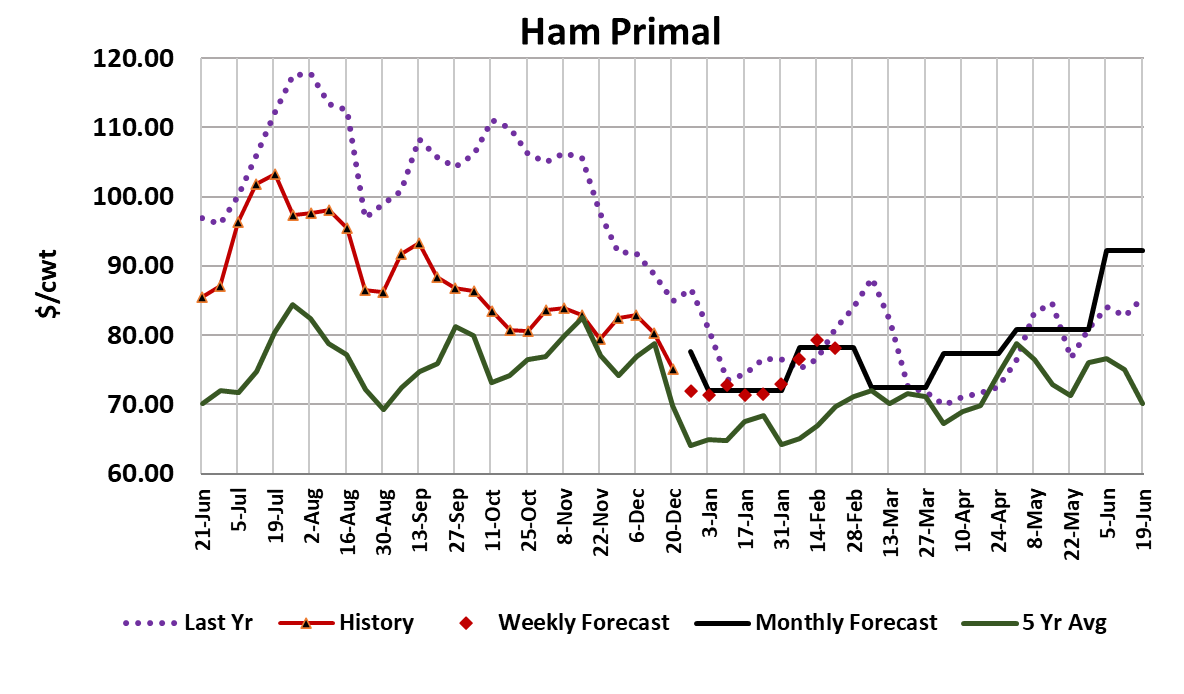

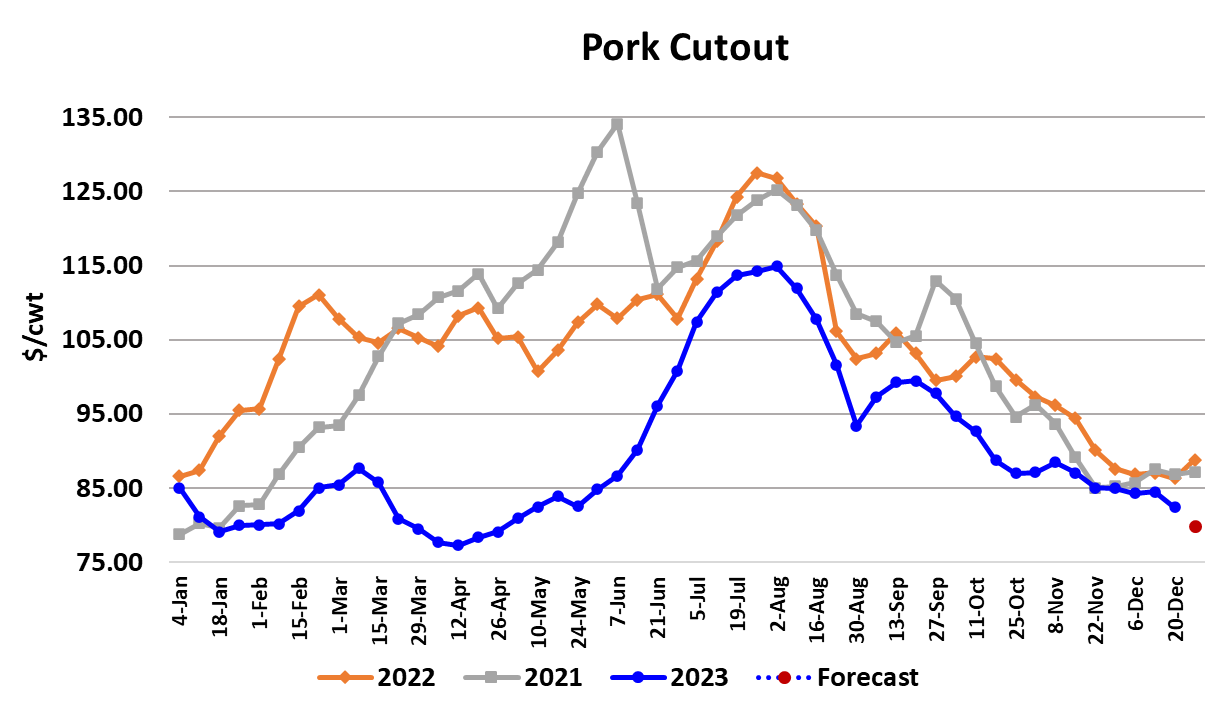

Prices in the hog and pork complex continued their orderly march lower this week, as the cutout averaged $82.30, down $2.09/cwt. from last week. Negotiated hogs fared a little better and the NDD negotiated base price was down $1.28 to average $47.78. With the cutout coming down faster than cash hogs, packer margins compressed slightly this week, now calculated at about $28/head. Packers ran a relatively light Friday and Saturday kill ahead of the Christmas holiday and that dropped the weekly slaughter total to 2.43 million head. Next week, there will be no production on Monday, but packers will likely do a very heavy Saturday kill and that should help the weekly total to come in around 2.25 million head. As we move through these short kill weeks, there is always a risk that the cutout will bump higher due to lighter production, but often it seems that both buyers and sellers prepare in advance for holiday disruptions and thus the price impact is smaller than one might think. The short kills will not be friendly to the cash hog market however, as those animals will keep on eating and gaining weight as they await their date with destiny. Packers will need less hogs and producers will be motivated to move whatever hogs the packer will take and thus it is likely that some further deterioration in the cash hog markets will occur. At present, it looks like overall pork demand is continuing to ease lower. That is evident in the combined margin chart. This week, both the belly and ham primals saw prices ease a bit and that was more than the small gains in retail items could make up for. Seasonally, hams still have considerable downside risk and there isn’t much reason to get excited about bellies at this time of year either. With those primals both on the defensive, it will be hard to get much lasting improvement in the cutout. Every so often we will see a light volume day in the belly market and prices bounce higher, but just as soon as more normal volumes get transacted, the price comes right back down. There was further bad news for the bellies contained in this afternoon’s Cold Storage report. The volume of bellies in cold storage grew by 19 million pounds when the normal seasonal build would have been closer to 10 million pounds. As a result, bellies in cold storage are now down only 14% YOY, compared to the 30% YOY decline that was reported for October. There is a very real risk that when we get the next report, it will show belly stocks near or above last year. Recall that in the first half of 2023 large frozen belly stocks were a huge drag on the cutout. It’s possible that the industry may be forced to replay that again in early 2024. Hams in cold storage declined as is typical for this time of year, but the decline was only 55 million pounds when 75 million pounds would be more typical. Thus, there are now 5% more hams in cold storage than last year, which is a departure from the YOY declines that were posted in every month from June through October. Its not that ham stocks are burdensome, but maybe just a little less supportive than they were back in the late summer and early fall. Cold storage levels are important for the pork market, but the big news of the week came in the form of USDA’s latest Hogs and Pigs report that was released Friday afternoon. That report showed total swine inventories up 0.2% YOY, when most analysts had been expecting something closer to a 1% decline. The breeding herd on Dec 1 was reported down 1.7% YOY, but that won’t have much of an impact on hog supplies because productivity surged once again. The number of pigs saved per litter was up 3.9% YOY and that comes on the heels of a 4.3% increase in the previous quarter. Apparently, producers are culling out the least productive sows so that even though the breeding herd is down, the number of piglets born comes close to even with the previous year. In this case, the Sep/Nov pig crop was only down 0.2% and those are the hogs that will be slaughtered in the upcoming March/May quarter. There were a ton of revisions in this report also, most of them upward. USDA revised the Sep 1 swine inventory up over one million head. That’s a huge adjustment and helps to explain why kills this fall have been far larger than expected. There were non-trivial upward revisions in the inventory numbers going all the way back to March, 2022. It is good that they made those revisions so that the numbers better align with what was seen in the slaughter data, but it would be even better if they could figure out what it is about their surveying methods that is causing them to consistently undercount hogs. Anyway, futures traders probably won’t be too happy with the data in this report and thus some selling pressure is expected in the market on Tuesday. This week, the futures were only modestly lower, despite the darkening outlook. They may make up some ground on that front next week. With pork demand nearly as bad as it was last spring and now there is news that we are going to see more hogs this spring than expected, there is little reason to be bullish on price levels in Q1. As a result, the price forecasts keep getting adjusted lower. The only thing good that I can think of to say about this hog market is that at least the long slide prices has been slow and orderly. Unfortunately for producers, often markets that are slow going down are also slow to rise when that time comes. Next week, look for more of the same: lower everything.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}