Pork Wrap December 2

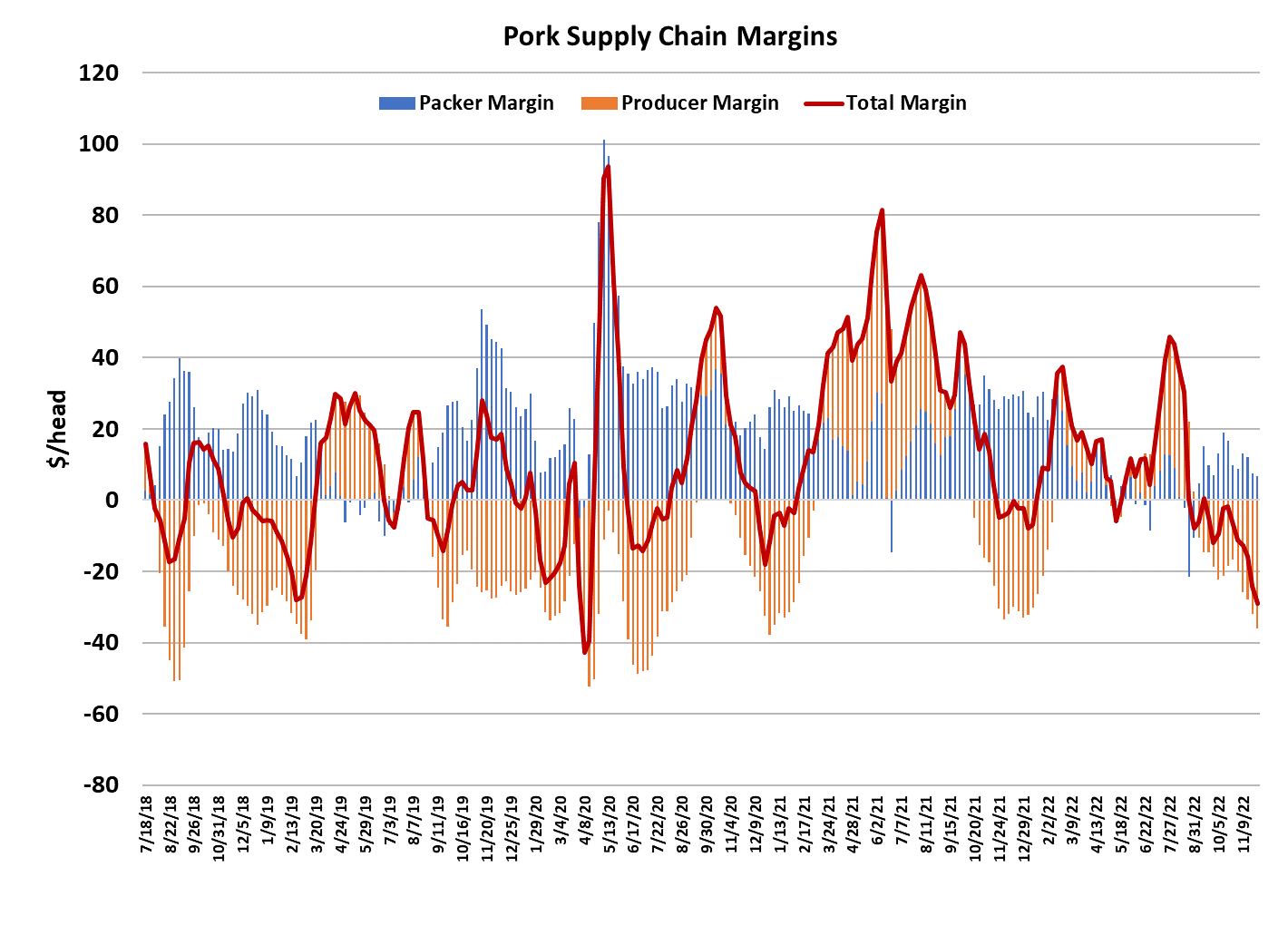

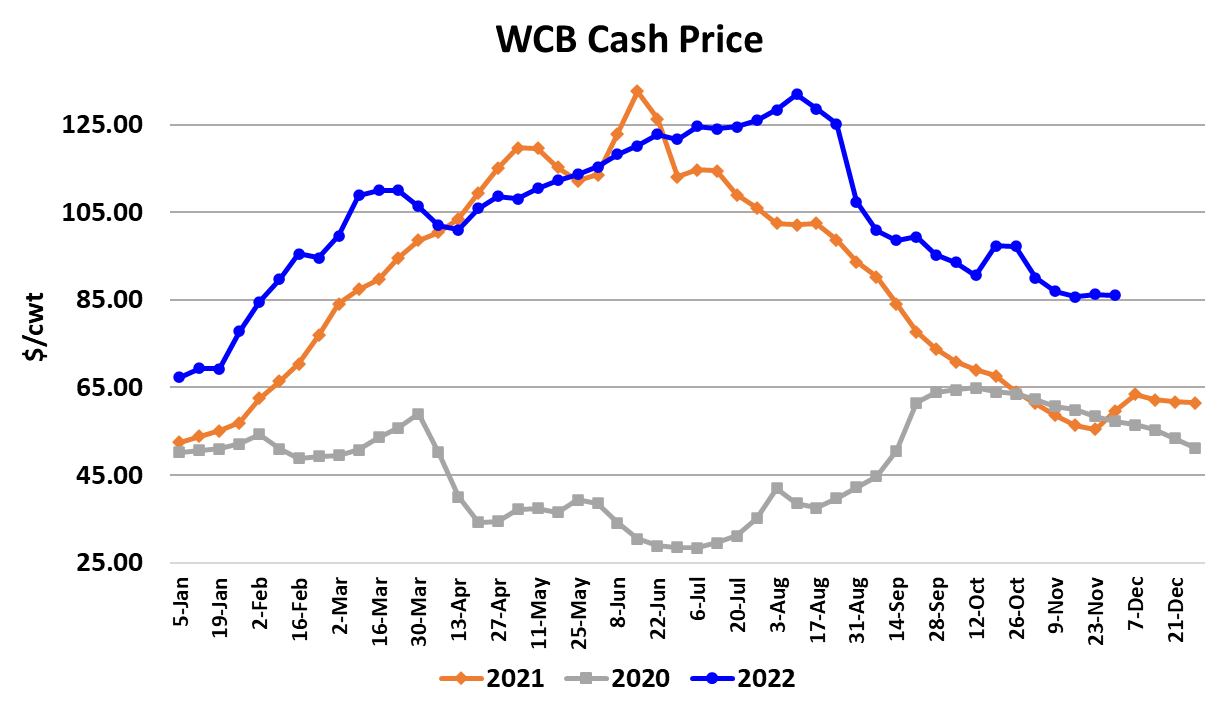

Negotiated hog prices held rather steady this week as the NDD

was up $0.34 on a weekly average basis and the WCB was down

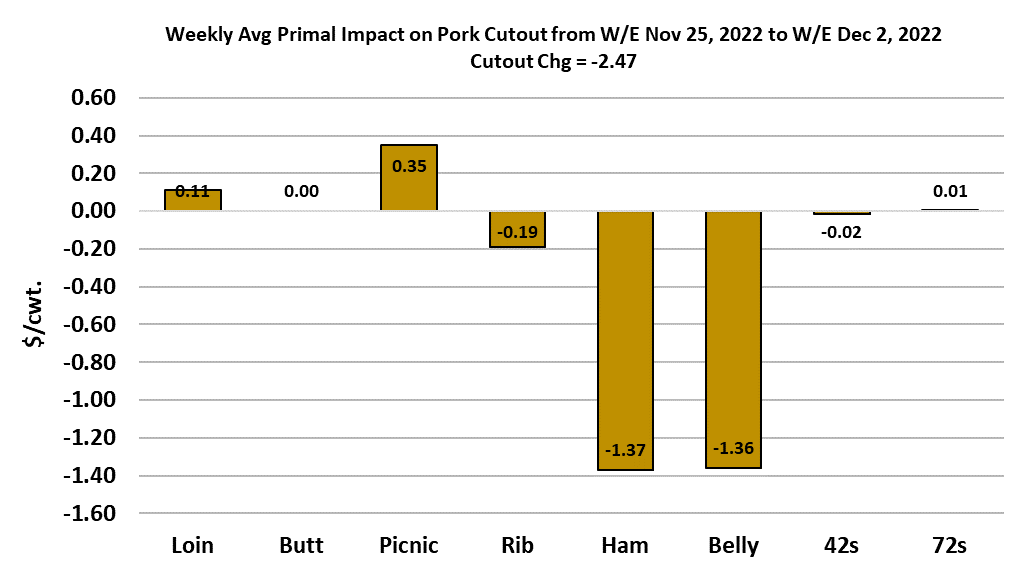

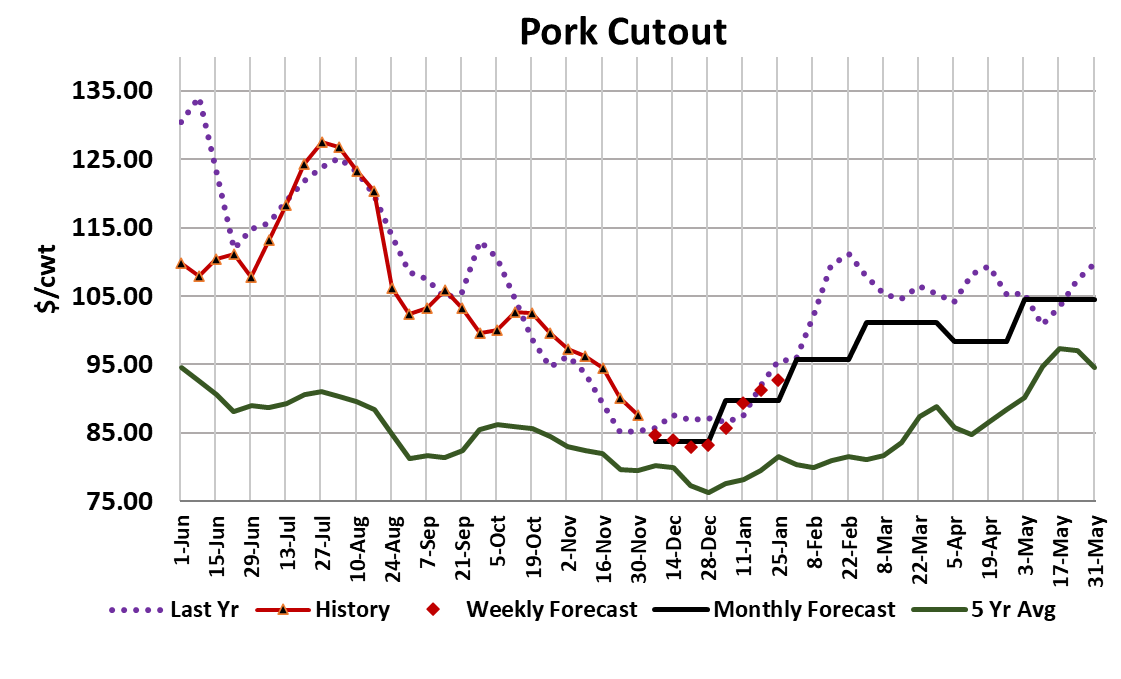

$0.14. The problem for packers was that the cutout dropped

$2.47/cwt. That shrank their margin once again and I calculate it

to be currently just under $7/head. Who would have guessed

that the week after Thanksgiving pork packing margins would be

only $7/head? The last time that happened was in 2011 and that

was a different era where $7 was a big margin. In recent years,

margins have averaged about +$31/head just after Thanksgiving.

This year it seems, there is something different about the hog

supply that is preventing packers from pushing cash hog prices

lower as they normally would at this time of year. I suspect that it

is because the herd has shrunk to the point where it is too small

for the amount of packing capacity and thus packers are having to

compete much more vigorously for uncommitted hogs. That is

not a problem that is going to go away anytime soon. Each

successive pig crop is a little smaller than the one before it and

that is likely to continue into 2023. Since its not likely that any

major packing plants will close in the near future, that means the

hog supply-to-packing capacity ratio will continue to shrink and

that should keep margins tighter than normal through most of

next year. The problem will be most acute in the middle of

summer when hog supplies are the tightest. We could see some

very red packer margins next summer. The immediate problem,

however, is that pork demand is still softening. Note the

combined margin chart. It is the same problem as with beef—

consumer demand just isn’t strong enough to provide good

margins for all of the supply chain players. This week it was the

hams and bellies that pressured the cutout lower while the retail

primals were steady to slightly higher. An important development

this week was the ham primal dropping almost $6 and that comes

after a $7 drop the week before. I am very concerned that the air

is starting to come out of the hams and they have been the main

support pillar for the cutout. We have lost $13 in two weeks off

the ham primal and we haven’t even reached the point in the

calendar when ham prices tend to crater (last 2 weeks of

December). The ham primal is still more than $20/cwt over last

year’s level and the five-year average, so there is plenty of air that

could still escape from this balloon. This week’s drop in the

bellies took that primal below the $100 mark for the first time in

almost two years. However, late in the week some of the bellies

were starting to be quoted higher. That may give some market

participants hope that the bellies are now on the upswing and that

may be true, but I want to see a few more data points before I call

the bellies substantially higher in December.

The last cold storage report told us that frozen belly stocks are about four

times larger than last year and are even larger than in pre-pandemic

years. That probably means that there isn’t much desire to put additional

bellies in the freezer now and thus more product will need to clear in the

fresh market. Also, processing activity tends to slow down during the

holidays and thus processors will try to keep their working inventories

rather low in the near term. All of that makes me cautious about expecting

significant increases in belly prices. They may not go down much from

here, but a big rally seems also unlikely. That’s unfortunate because a

rising belly market could be a nice counterbalance to a softening ham

market. Loins and butts are likely to hold in a mostly sideways pattern

until after the holidays. Pics are also carrying a lot of air, now almost $20

over last year and the five-year average. They too tend to break sharply

lower around mid-December, so that is another potential source of

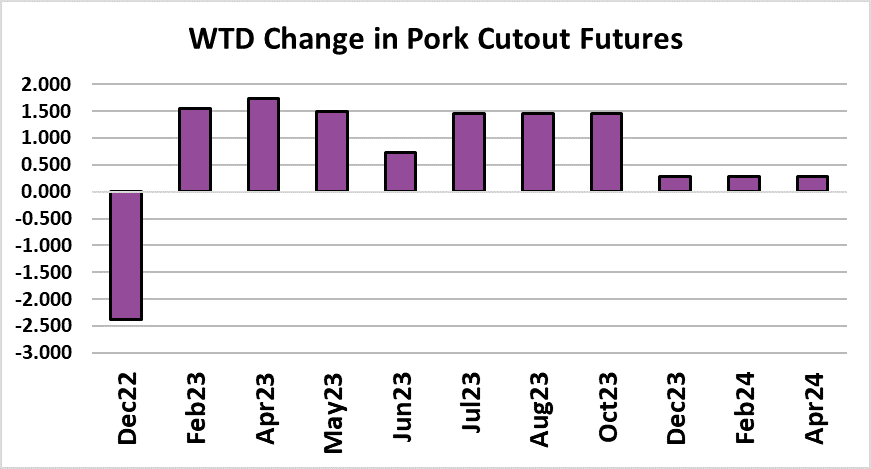

softness for the cutout. After updating the forecasts this week, I’ve got the

cutout continuing to ease very slowly lower until after Christmas when

buying for early January delivery should start to raise the cutout. This

week, the cutout had the benefit of coming off of a short kill the week

before and it still lost over $2. Next week the market will be asked to

chew through the pork resulting from this week’s 2.59 million head kill, so

the supply side pressure should be a little stronger. The weekly export

numbers make it pretty clear that the market isn’t going to get a big boost

from overseas buying here at the end of the year. Barrow and gilt carcass

weights were reported a pound higher this week, which is pretty typical for

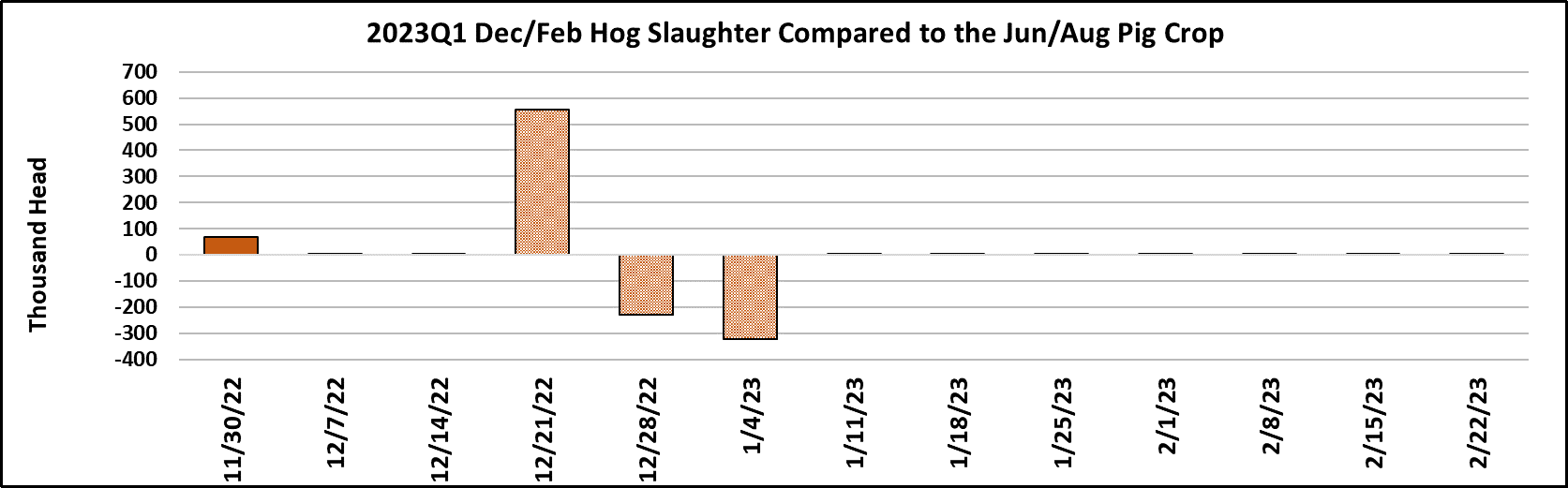

this time of year. The industry is now working on the Jun/Aug pig crop

and this week’s slaughter came in a little above what the pig crop implied,

so that is something to keep an eye on. Normally at this time of year,

producers have so many hogs to market that they are pretty much taking

whatever the packers offer in the spot market. Not this year. The supply/

capacity ratio is keeping negotiated prices elevated. The WCB

negotiated price is running $26 higher than this time last year, but recall

that last year at this time packers were struggling to find sufficient workers

to staff plants and that effectively reduced processing capacity. LH

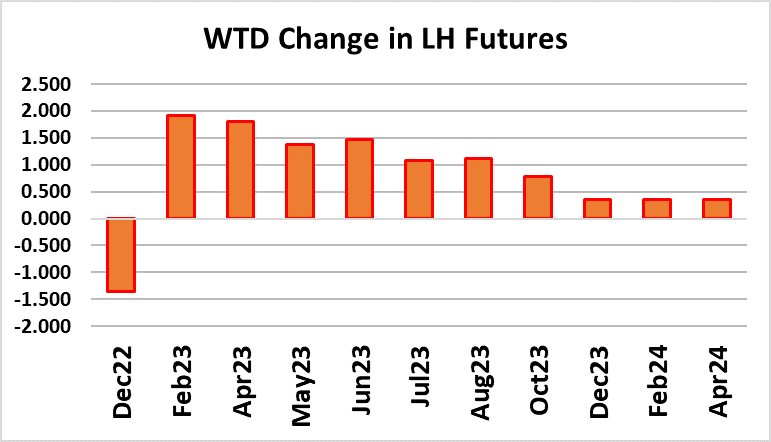

futures sold off hard on Monday, but recovered later in the week as

traders seemed to have a change of heart and the structure of prices

makes it look like they now expect a bottom in the LHI very soon. The

steep premium on Feb points to expectations that once the bottom is in,

then prices will step higher week after week. The one thing that favors

that scenario is that the combined margin is in a zone where we might

expect a bottom soon. Next week, watch the see-saw between the bellies

and the hams. If they can stay opposed to one another then the cutout

might stabilize, but if they both jump on the same end of the see-saw it

could be jarring experience.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}