Pork Wrap December 19

No pdf

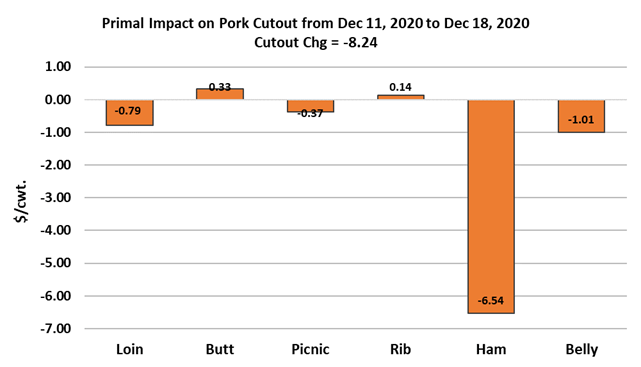

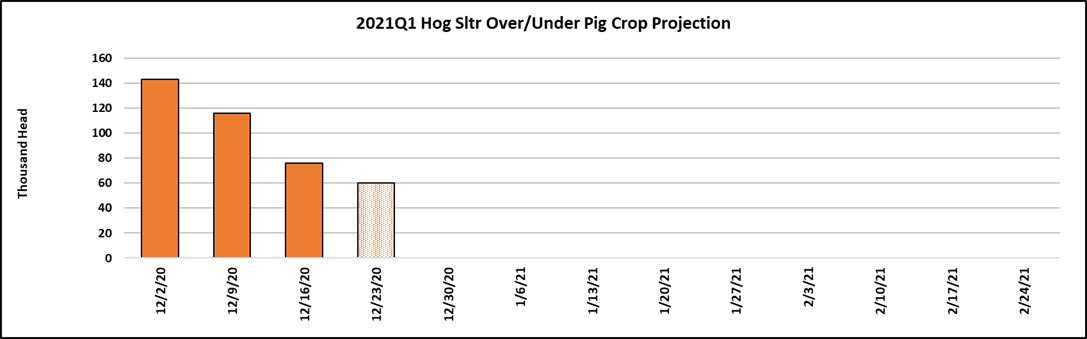

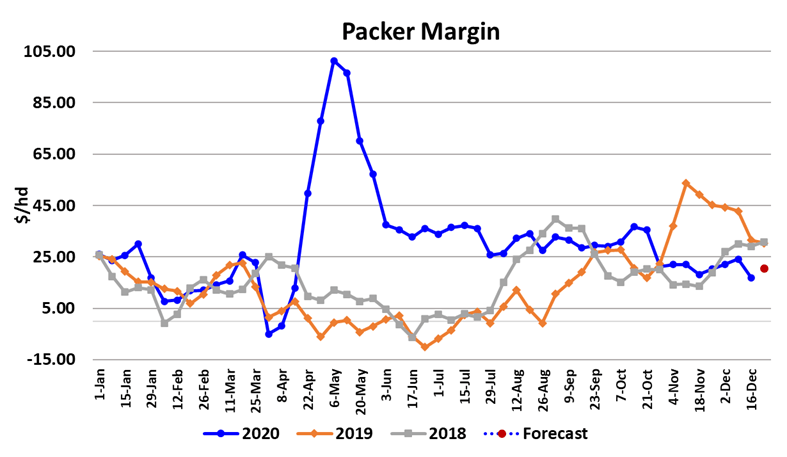

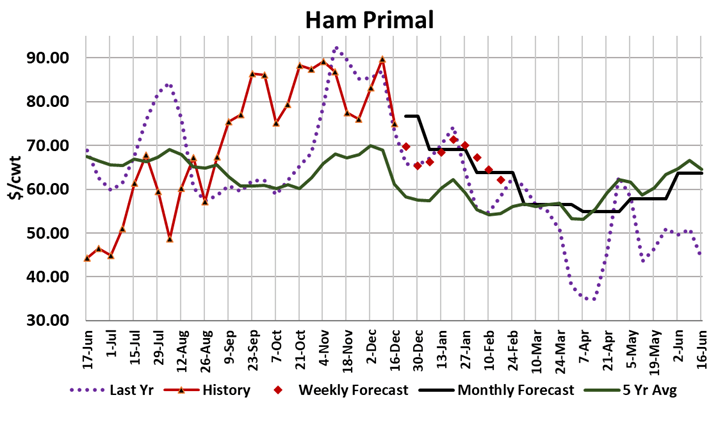

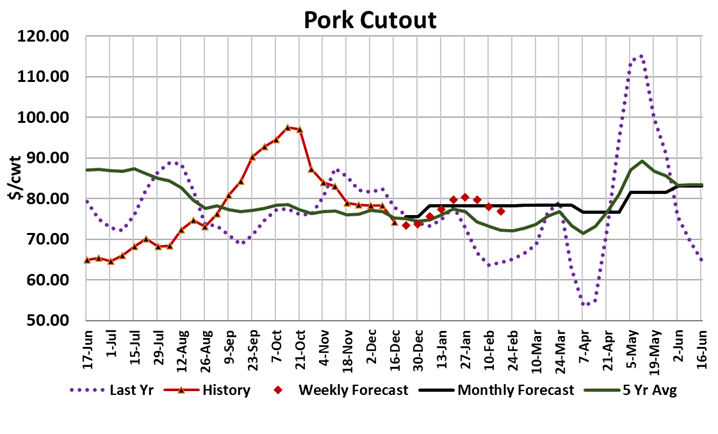

The pricing situation in the hog and pork complex is growing weaker. The cutout dropped over $8 Friday-to-Friday and the WCB negotiated market lost a little over $3. In this market, so much is driven by the cutout that it makes sense to put a lot of effort into understanding where it is headed. Right now, it is mostly about the hams. The holiday business is done and the hams are in the midst of their end-of-year break. The ham primal dropped almost $27 Friday-to-Friday. This happens to the hams every year right around the middle of December, so it should come as no surprise. Since the hams account for about one quarter of the cutout value, any big drop there is likely to have a significant negative impact on the cutout. The chart below indicates that almost all of this weekfs drop in the cutout was due to the hams. Bellies were down a little, but the hams were the main driver. My forecast has most of the other primals slowly working higher into early January, but that slight strength might not be enough to offset the losses coming from the hams. If the non-ham primals donft hold up as I expect, then the cutout is really in trouble. Time will tell, and the cutout should get some support from the two short kill weeks ahead, but there is a real risk that at some point the cutout moves below the $70 level in the next week or so. Hams normally see a modest rise in January as buyers looking to secure their Easter hams become active. Hopefully by then the bellies will be on the mend too and that, combined with modest increases in the other primals has the potential to bring the cutout back into the high $70s or lower $80s by the end of January. Since the cutout was falling faster than the negotiated hogs this week, packer margins compressed. I calculate this weeks margin just a bit below $17/hd. That is the lowest margin in this week of the year since 2014. However, I look for margins to widen next week because all of the impact of the falling cash hog markets and the cutout has not yet been fully incorporated into the LHI. It looks to me like the LHI has risk down to $62 next week. Clearly, packers still have some leverage with producers because theyfve been successful in pressuring the cash hog market as the cutout comes down and their leverage will only increase with the short kills on the horizon. That points to some modest expansion in packer margins, perhaps back to around $25/hd by the time we get into January. This week saw yet another over-killing of the Jun/Aug pig crop although it wasn’t as big as the previous two weeks (chart below). I am about ready to chuck USDAfs estimate of the Jun/Aug pig crop out the window and assume there are more hogs out there than USDA told us. Now of course, it is possible that the Jun/Aug pig crop was front-end loaded and we might see a string of under-kills in Jan/Feb that will balance things out, but with each passing week that becomes less likely. Packers put together a huge Saturday kill (380k) this week and that pushed the weekly total up to 2.79 million head. There were some modest plant disruptions this week as evidenced by lighter-than-expected daily kills Wednesday through Friday. I suspect that these were related to the snow storm that moved up the East Coast this week and not to serious covid outbreaks in the plants. There was a Bloomberg article this week that suggested meat plants were struggling once again with covid effects and maybe that caught traders attention and brought some unwarranted buying interest into the market today. However, packers easily made up the lost production on Saturday, which tells me that it’s probably not covid-related. Packers are not having much difficulty getting the hogs dead, but they are short on labor to fabricate the primals. We are still seeing a huge premium on de-boned hams relative to the bone-in items as a result. Ifd expect that to be a persistent feature in the market until spring, at least. Carcass weights continue to run heavy, about four pounds over last year. That is a concern, but the excessive weight is mostly in packer owned hogs, so it probably doesn’t say much about producer currentness at the moment. It does however, create additional tonnage that will have to clear the market and so it is a net negative overall. Export markets seem to be holding together ok, but they don’t seem to be exhibiting much growth and my fear is that export demand from China will subside in the first half of next year. That has the potential to offset much of the price improvement that is expected due to smaller supplies in 2021H1. We will get a Hogs & Pigs report on Wednesday and I expect it will show all hogs and pigs down about 0.2% from last year. More importantly, I have the breeding herd down 2.5% on Dec 1 and the Sep/Nov pig crop down 2.3%. Those two things will be the drivers of smaller supplies in the first half of 2021. The nearby Feb futures got a boost just as the Dec was expiring and traders have been reluctant to let it slip much lower in the ensuing days, even though the cutout and negotiated markets were deteriorating. Feb is now about $4 over where I calculate the LHI will print on Monday, and while that isnft a huge basis by historical standards, I suspect the longs will grow increasingly nervous next week as they watch the cutout struggle under the weight of this week’s big production and lack of pork buyer interest just ahead of Christmas. Next week, itfs all eyes on the hams and their impact on the cutout.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}