Pork Wrap December 17

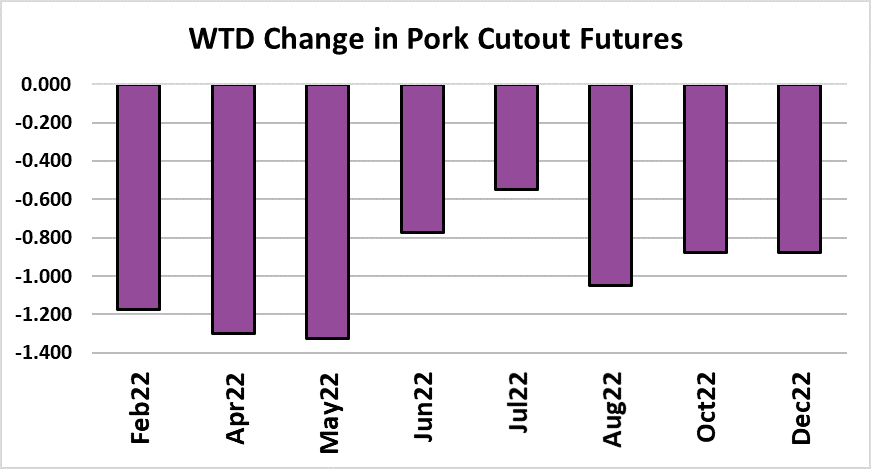

The Dec LH futures cash settled on Tuesday to a LHI of $72.30. At the

end of the week, the LHI was still very close to that level. The Feb

futures, which are now the nearby, moved lower the first three days of

the week, but then rebounded on Thursday and Friday to finish the

week almost unchanged. The thing that seemed to change trader’s

minds midweek, was the cutout printing in the high $80s and low $90s.

However, that was mostly an artifact of some boneless ham volume

that was spread out over more days than normal. By the end of the

week, the cutout was back below $86. There was also a sense that

the negotiated hog market was moving higher, but in actuality the WCB

market averaged $1.26 less than the week before and the NDD was

only $0.25 higher. This just highlights the difficulty that traders are

having figuring out a market that doesn’t seem to have a discernible

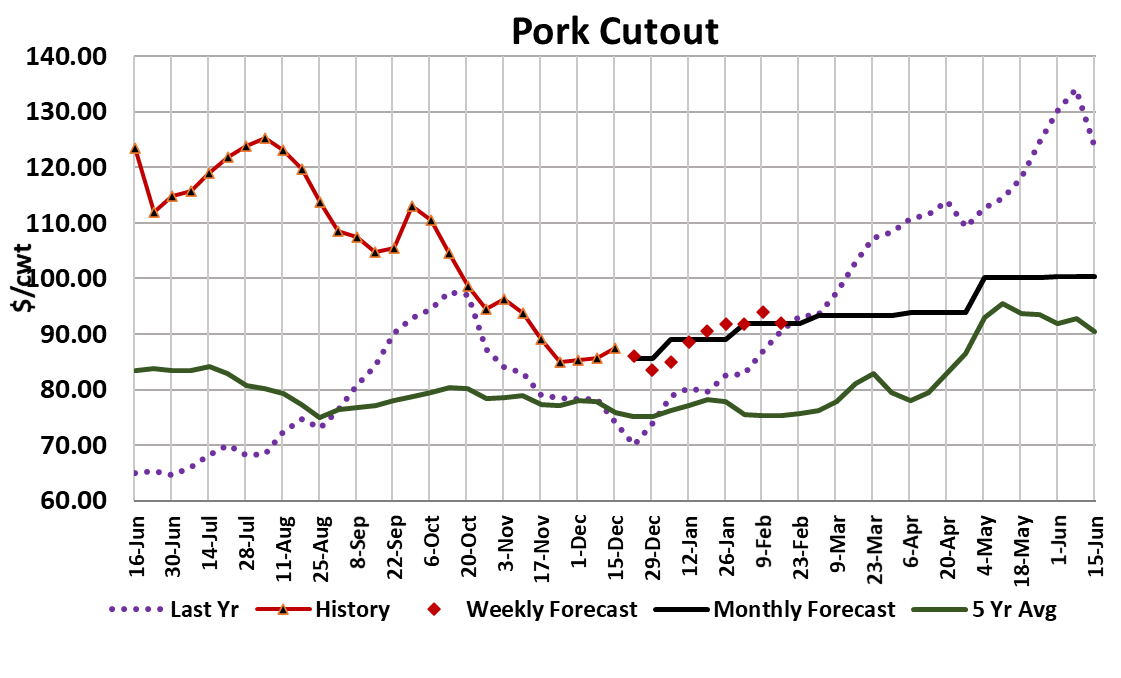

trend. The cutout has been stuck in the $80s for five weeks now, and

my forecast has it holding in the $80s for another 3-4 weeks. Some of

the weekday kills were smaller than expected this week and perhaps

that gave the impression that packers were having difficulty finding

hogs.

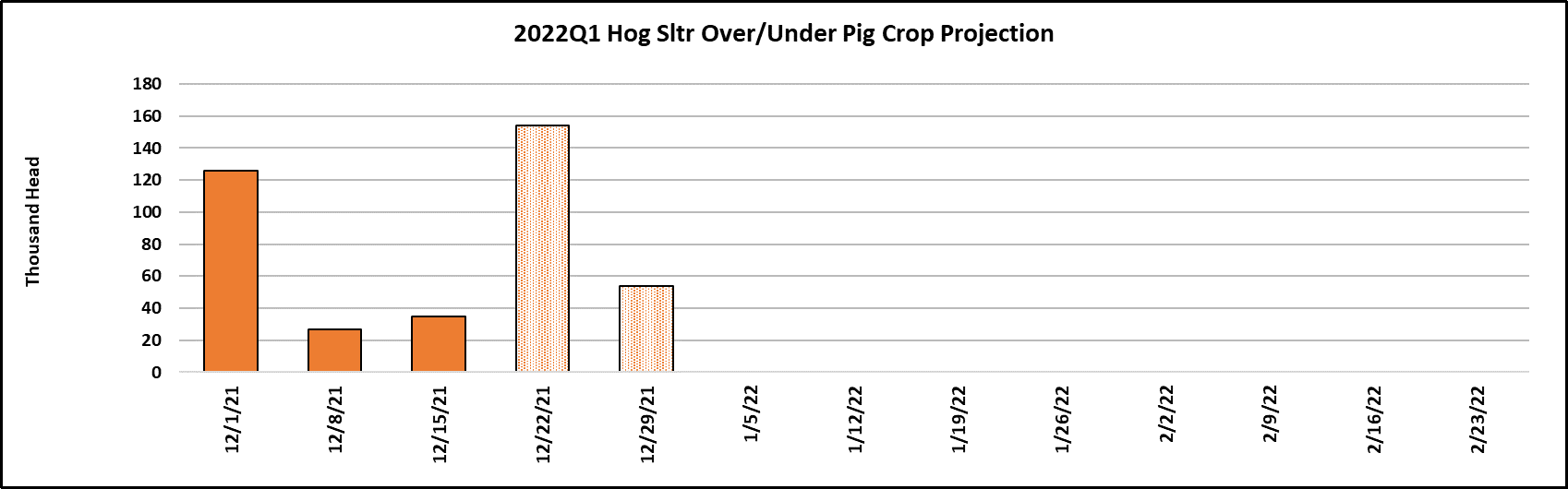

However, they didn’t have any trouble finding enough hogs to generate

a huge 332k Saturday kill. That put the weekly total at 2.65 million

head and was only a hair shy of the biggest kill this fall. The kill was

only down 4% YOY—well above the 6% smaller kills that USDA

indicated with its summer pig crop estimate. The chart below shows

that we’ve over-killed the pig crop every week so far in this quarter and

next week the over-kill is expected to be even larger as a result of the

way that Christmas falls on a Saturday this year. I haven’t found a

good explanation for the small weekday kills we saw, but the

windstorms in the Midwest this week may have played a role.

Hopefully, it wasn’t COVID-related absenteeism, but that is something

that could emerge as an important factor in the weeks ahead. Buyers

should be prepared for the possibility that this more-infectious variant

causes reduced production as workers come back from the Christmas

holiday

Next week, the Saturday kill will be zero and the Friday kill is likely to

be reduced. I’m expecting the weekly total to be only 2.07 million head.

In the week leading up to New Year’s, I have the kill closer to 2.2

million head. It is possible that the short production in the next two

weeks will produce some gains in the cutout, but that typically doesn’t

happen because everyone knows it is coming and prepares for it. This

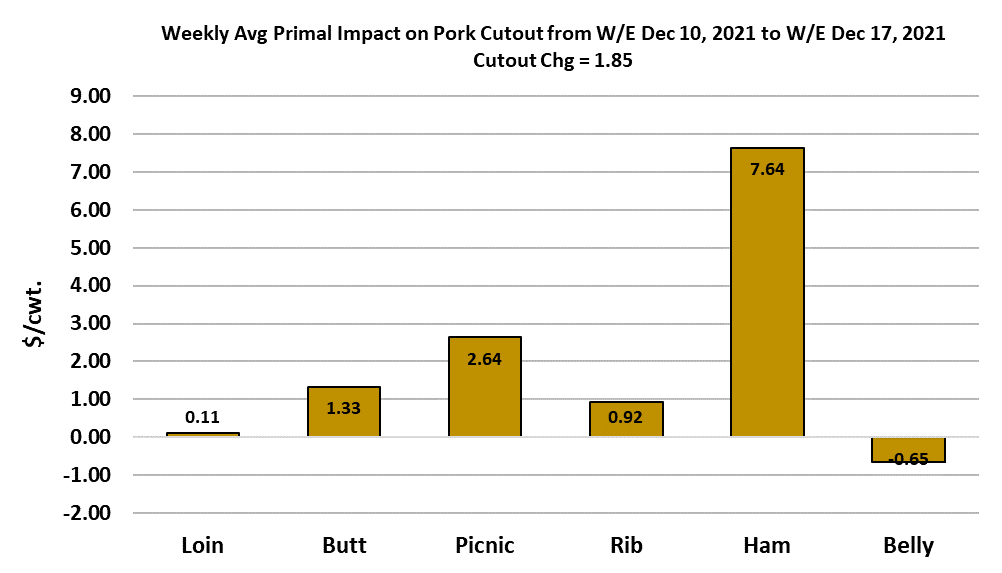

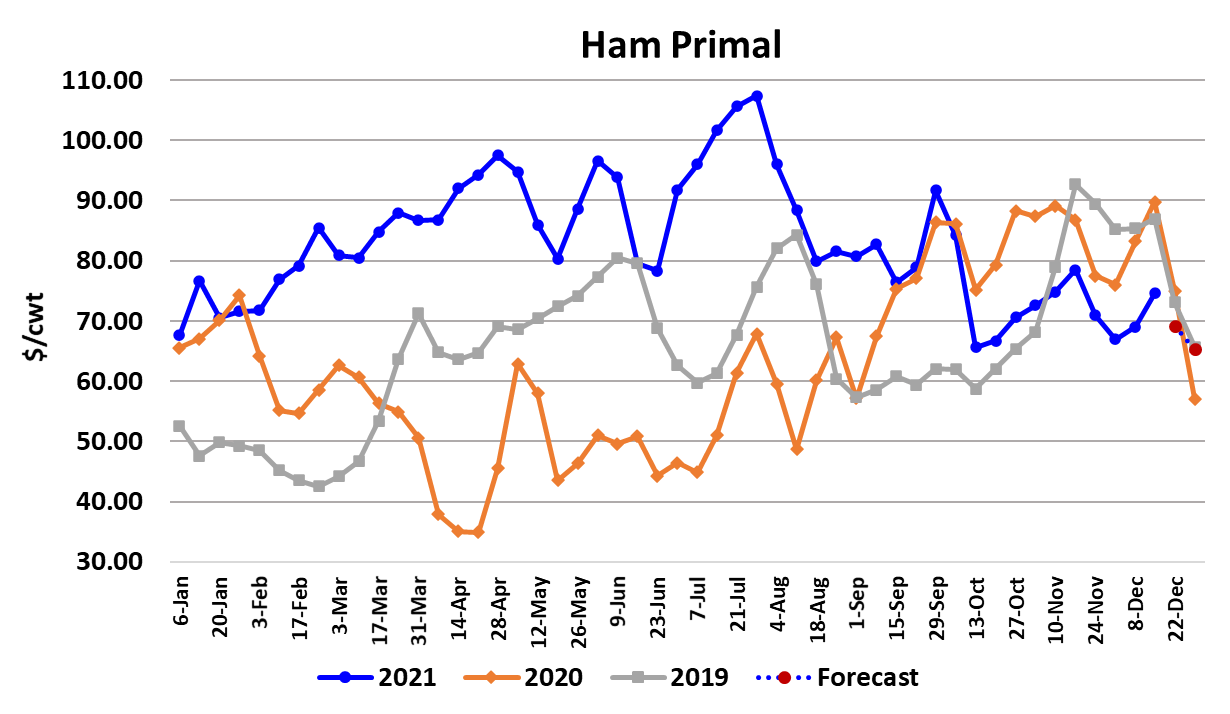

week, it was the hams that provided the most support to the cutout and

that is a little unusual because normally the hams are breaking lower at

this point in the calendar. It does look like packers sold forward a big

order of hams recently and negotiated volumes of bone-in hams were

unusually low, so perhaps that was limiting availability. My guess is

that their ham inventory will be replenished by the huge Saturday kill

and hams will come out of the gate next week trading lower.

Bellies have been stagnant as expected, with the primal holding

near $130 for the past few weeks. I don’t see them moving much in

either direction until after the holidays when they could see some

modest price gains. Other than that, I have most of the other primals

in a sideways pattern until mid-January and that is what leads me to

a cutout that holds in the $80s for the next few weeks. Packer

margins improved about $5/head to $32 this week and, while that

isn’t anywhere near the record for this time of year ($43/head), it

certainly doesn’t seem to be consistent with the very tight hog supply

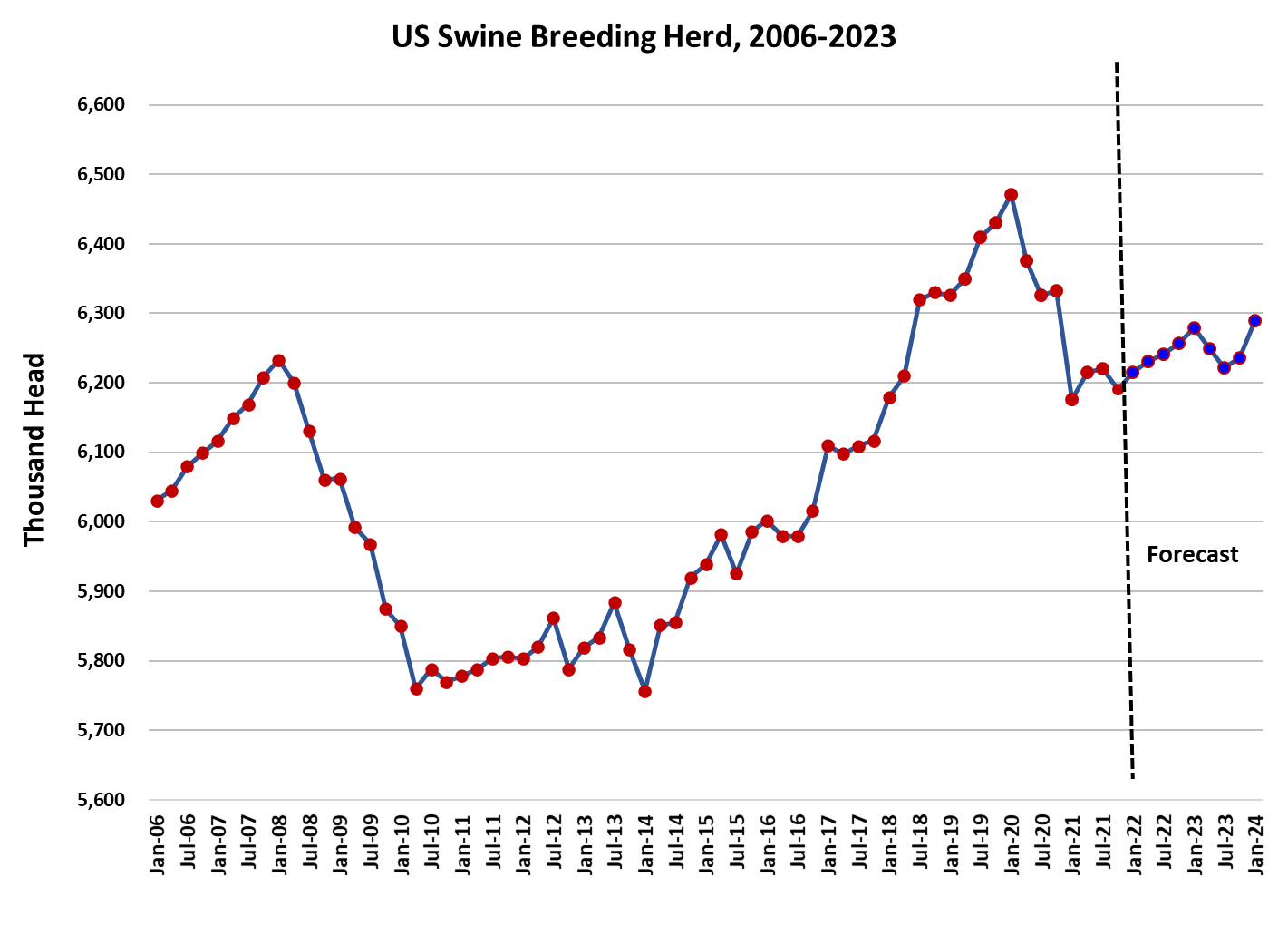

scenario that many have been anticipating. USDA will release

another issue of Hogs & Pigs on Thursday and I expect it to show

the swine herd down a little over 3% YOY and the near-term hog

supply about 4% below last year. The most important number will

be the estimate of the Sep/Nov pig crop and there I’m looking for a

3.2% YOY decline.

Those will be the hogs coming to market in the March/May quarter,

so its reasonable to expect both hog supplies and pork production to

be below year-ago levels at least through the first half of 2022. With

smaller supply being likely, the focus will turn to demand for price

determination and in particular export demand. China continues to

pull back from the US pork market and there is little reason to think

that will change in early 2022. That will leave a big hole to fill

because the China business was very strong in early 2021. Mexico

has been stepping up as a bigger buyer lately and that has helped to

temper the influence of dwindling Chinese business, but it won’t be

able to fully replace it. As a result, I’m projecting significant YOY

declines in pork exports for most of the first half of next year. It

won’t be enough to offset the smaller production in Q1 and thus per

capita availability could be down 5% or more through March, but by

Q2 we could have availability back near 2021 levels. Domestic pork

demand appears to be turning higher, albeit slowly.

The combined margin chart below makes it pretty clear that a bottom

has been established. This is the first bottom in negative territory

since the pandemic began. My guess is that the next peak in the

combined margin will be well below what we saw in the pandemic

also. So we have all of the elements for some price appreciation in

both hogs and pork, but the increases may be very small initially and

then gain more traction around the middle of January. There is risk

however, that the omicron variant will disrupt production and send

prices sharply higher. From what I know right now, I’d put the odds

of that kind of event at 1 in 4, so it’s not insignificant. Next week,

watch the hams for signs that the seasonal price break is taking hold

and watch the news closely for reports of escalating omicron

infections in or near packing plants.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}