Pork Wrap December 15

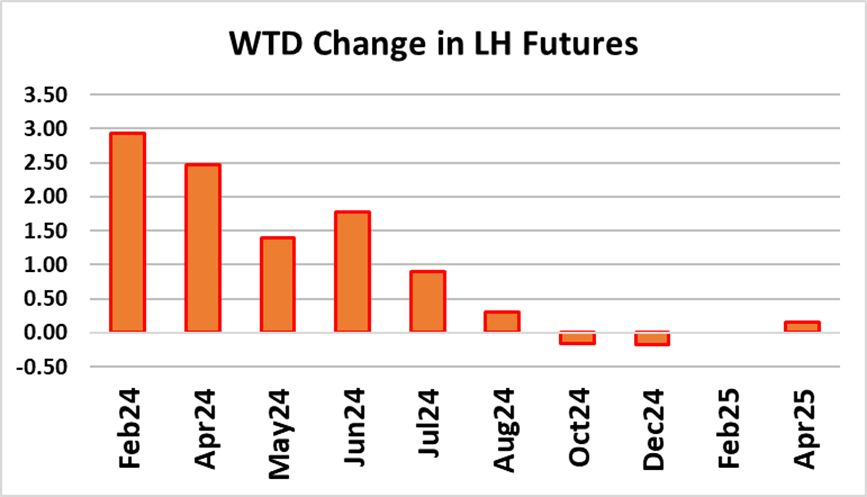

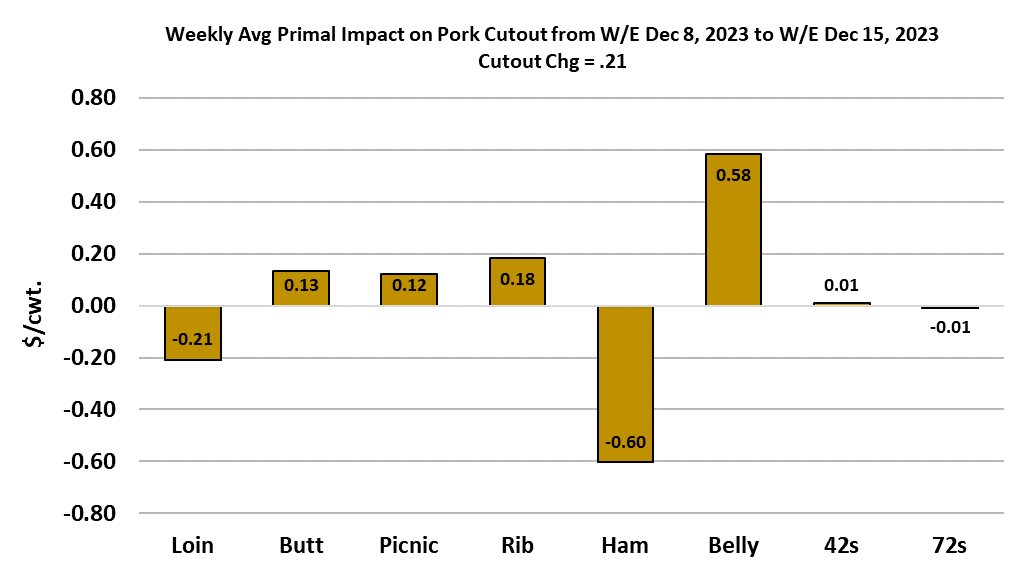

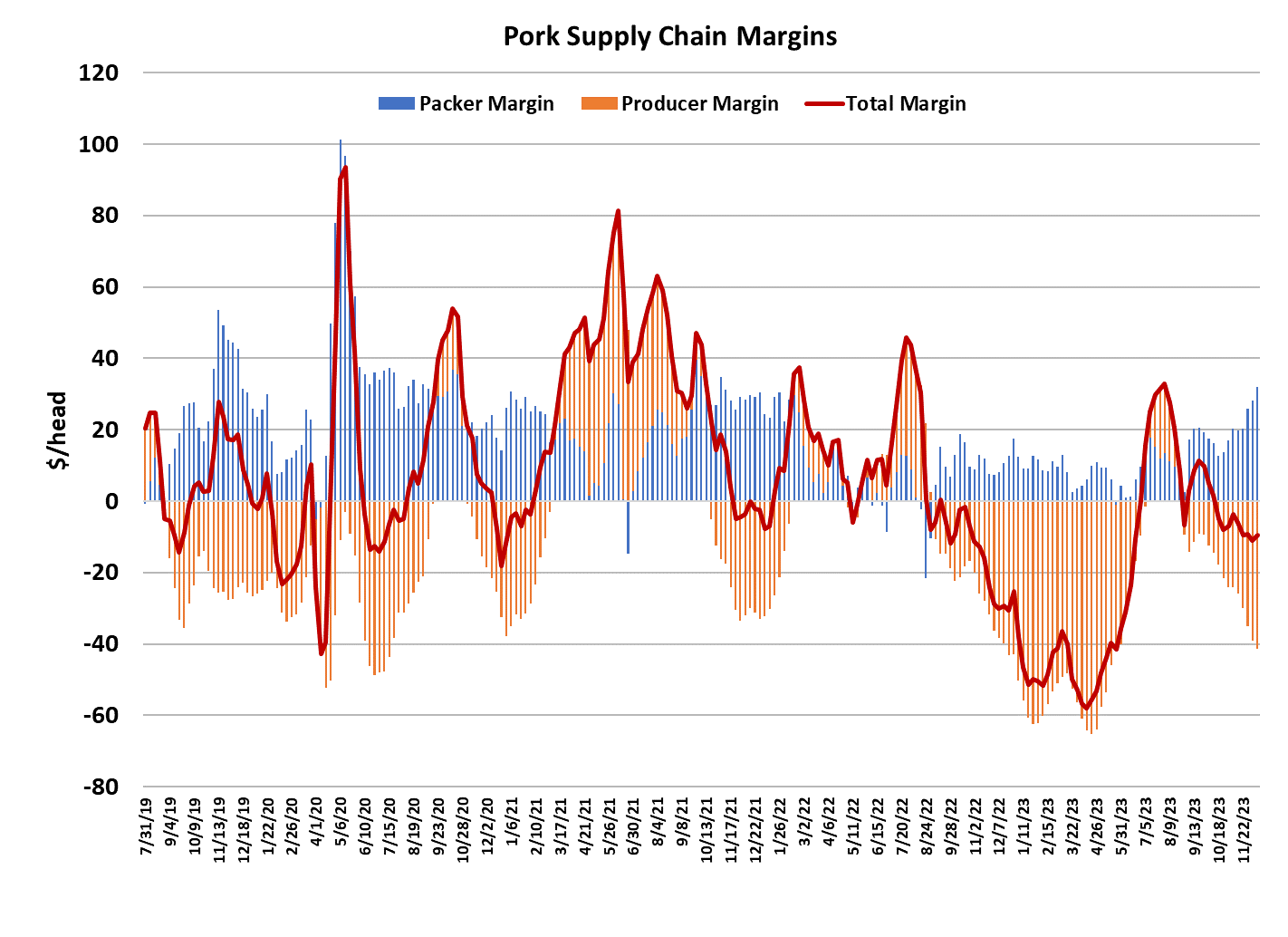

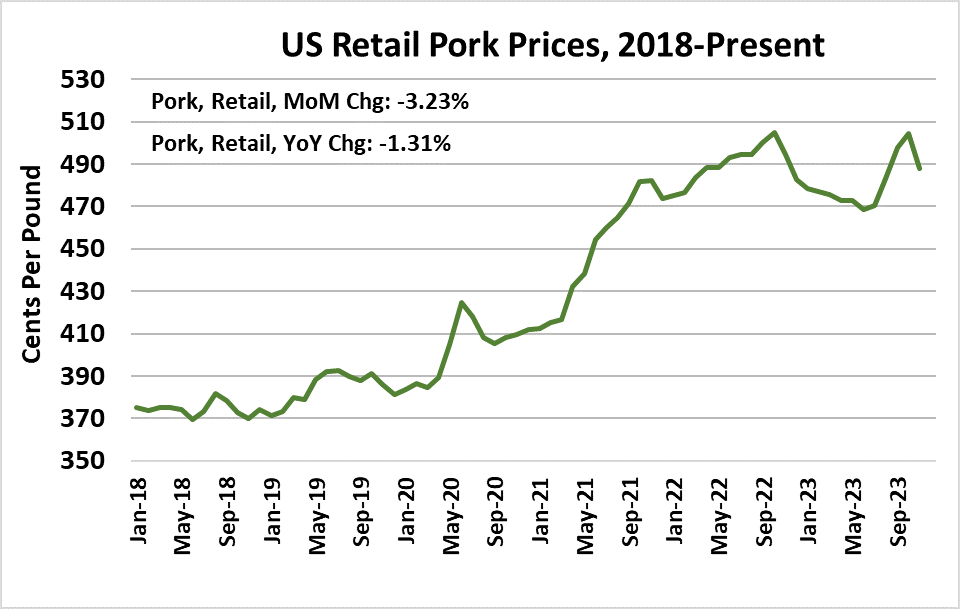

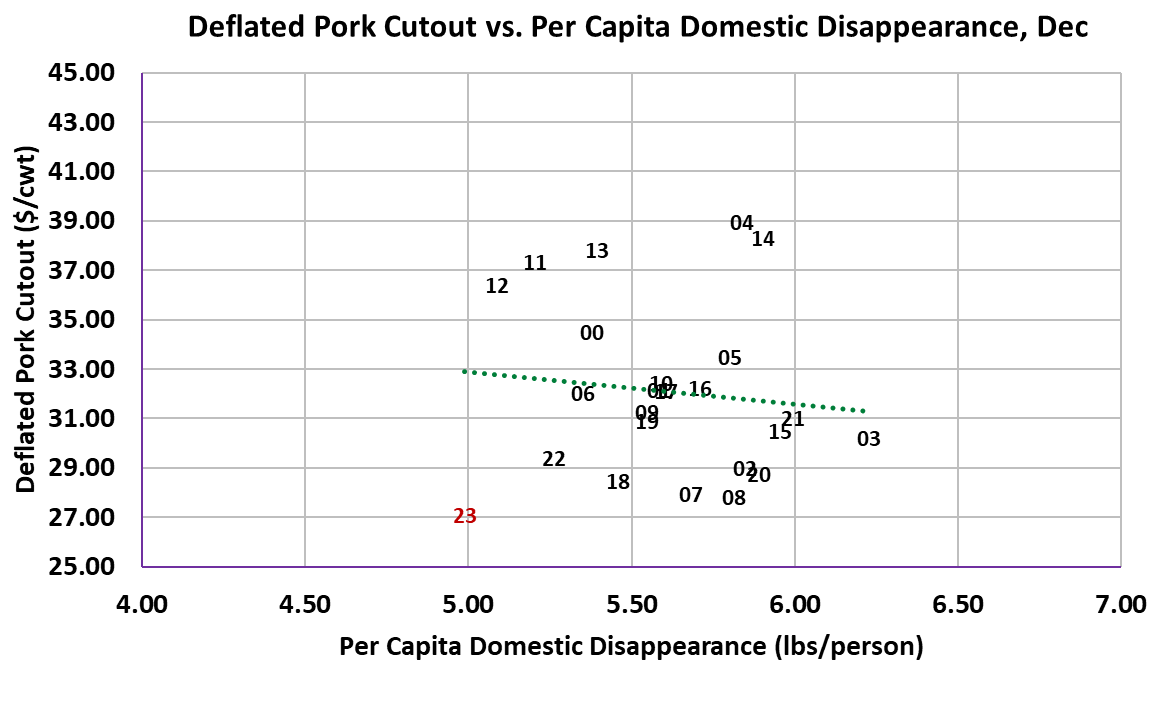

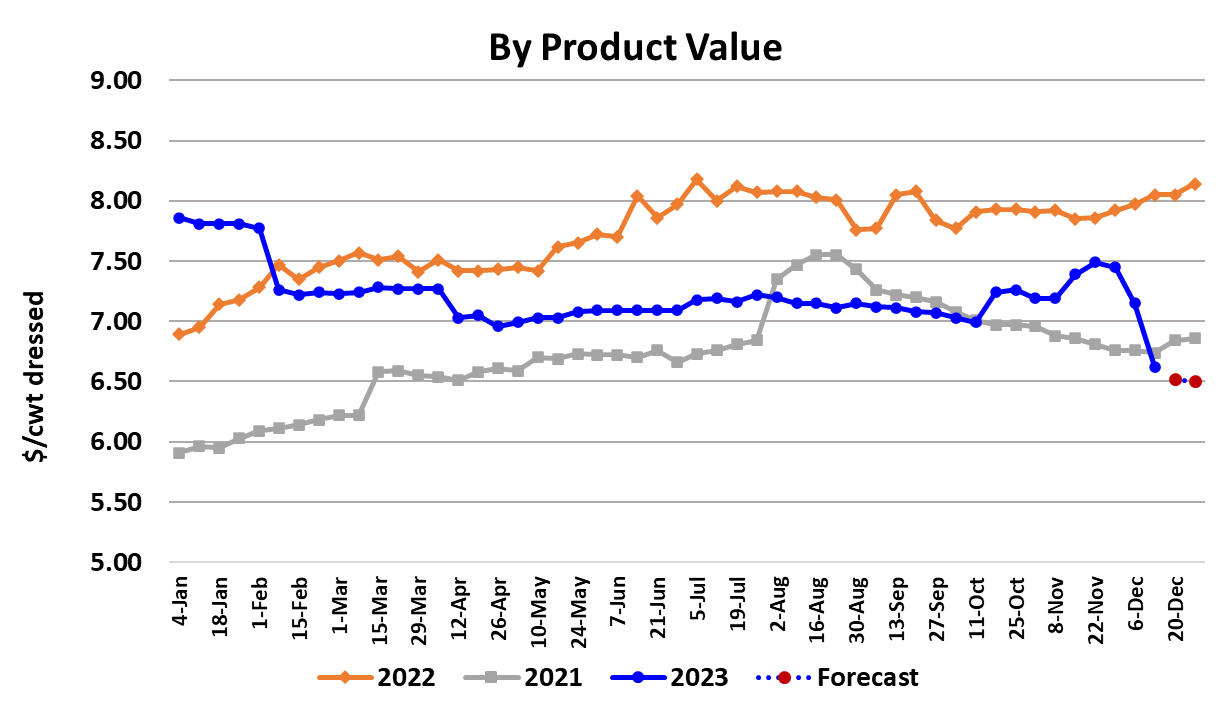

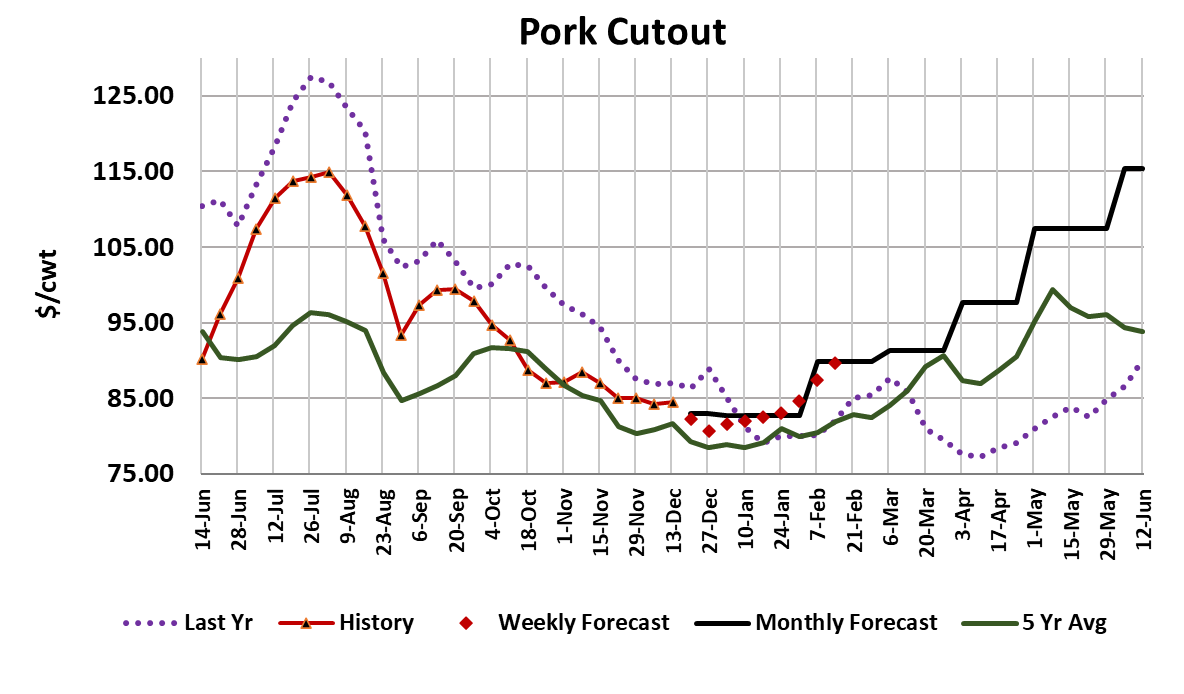

Negotiated base prices for hogs dropped below $50/cwt. this week, with the WCB market averaging $49, down $3.84 from the week before. The cutout posted a tiny gain, up $0.21 to average $84.48/cwt. The cutout has averaged in the $84-85 range for the past four weeks. That may give the impression that it is bottoming, but I wouldn’t be so fast to draw that conclusion. This week, a modest gain in the belly primal helped to offset a modest decline in the ham primal and thus kept the cutout near unchanged. However, the true value of the belly primal was probably overstated a bit because there were some days where very light volume caused a higher-than-typical print. Hams, on the other hand, appear to be heading south and while the pace of the decline has been slow so far, there is risk that it will accelerate in the next couple of weeks. That could result in a cutout that trades near $80 by the end of the year and a lean hog index that moves to the low $60s. The Dec futures expired on Thursday and will cash settle at $67.15. That is the lowest settlement value for a hog contract in the last three years. If we adjusted that for inflation, it would look really ugly. Futures traders seem to believe that better times are in store for February, as that contract has gained $5 in the past two days with very little fundamental information to support the move. The Feb contract often settles a few dollars over Dec and that may happen this year, but the near-term fundamentals suggest that the LHI could go lower before recovering near the end of January. And of course, there is always the risk that the market continues to ease lower right into Feb expiration. It doesn’t appear that we are about to get a new burst of demand that is going to lift the cutout dramatically, and there is still the issue of hog supplies that keep coming in bigger than expected, so the prospects for near-term price strength don’t look good. This week’s slaughter registered 2.69 million head, more than 100k larger than what the Jun/Aug pig crop implied. That is the second week in a row with a big over-kill. There could be a little relief next week, if packers run lighter than normal on the Saturday ahead of Christmas. During Christmas week, the kill will likely be down around 1.95 million head. That may help shore up the pork market temporarily, but it won’t be good for the cash hog markets. So far, producers have shown a willingness to market hogs aggressively, even if it means accepting lower prices, and that has helped to prevent a backlog. The light kills during the holidays could easily result in some hogs getting delayed and that could keep negotiated hog prices tracking lower. Packers are certainly being incentivized to keep kills high in non-holiday weeks as their margins are now just a smidge over $30/head. It seems reasonable that packer margins will expand a little more before starting to narrow in mid-January as hog supplies tighten a bit seasonally. Producer margins are now about $42/head underwater and the forecast has that growing to -$52/head in the next few weeks before it finally starts to improve. Next Friday, we will get a Hogs and Pigs report that is widely expected to show some contraction in the hog herd. I’m forecasting the breeding herd to be down 1.9% YOY and the total swine population to be down 1.3%. I wouldn’t be surprised to see the breeding herd reduced a little more than what I have dialed in. Productivity will be the wild card, and I’m projecting the number of pigs saved per litter to increase nearly 3% YOY, but the number of sows farrowing should be down about 5%. That would result in the Sep/Nov pig crop being down 2.4% YOY. Productivity could come in stronger than expected however, and that would result in a bigger-than-expected pig crop. The reductions that we see this quarter likely won’t be enough to get the industry back on track to profitability, so I’d expect further cuts to the breeding herd in ensuing quarters. This industry is just too large and too productive for the level of pork demand consumers are exhibiting. It may take a few quarters of cuts to get things back in better balance. USDA provided some welcome news this week in the form of lower retail prices. They reported November retail pork prices were down 3.2% from October, which almost erased the big gain that was seen from September to October. On a YOY basis, retail pork prices were down 1.3%. Lower retail pork prices are critical to keeping product moving through this period of big pork production. Pork demand is very poor at the moment. The attached scatter shows just how weak the cutout is in inflation-adjusted terms compared to other years. It is worse than last year, and that should give traders some pause before they go and get too bullish on the potential for price increases in Q1. I’m hopeful that the industry will cycle back out of this period of exceptionally soft demand, but I remember last spring when weak demand seemed to persist for months. The combined margin ticked a little higher this week, but that is unconvincing. I’d like to see a stronger move higher next week. Another ominous sign for demand is that by-product values have moved sharply lower in the past couple of weeks. It might be tied to the big kills that we’ve seen this fall, but we always have big kills in the fall and the recent drop seems well outside of the normal seasonal tendency. So we need to keep an eye on that. Fortunately, pork shipments into export channels seems to be fairly strong right now, but those will get curtailed during the upcoming holidays. It has been a long time since we’ve seen negotiated base prices for hogs drop into the $30s, but it sure feels like the market is on a trajectory now that could take prices close to that. It is imperative that producers aggressively work to rein in production. Packers that produce their own hogs are faring better in this environment than independent producers and the end result of this long stretch of poor profitability could be an acceleration in the trend toward more integrated pork operations. Next week, look for further pressure on both hog prices and the cutout. Watch the hams in particular, they hold the most downside risk.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}