Pork Wrap December 10

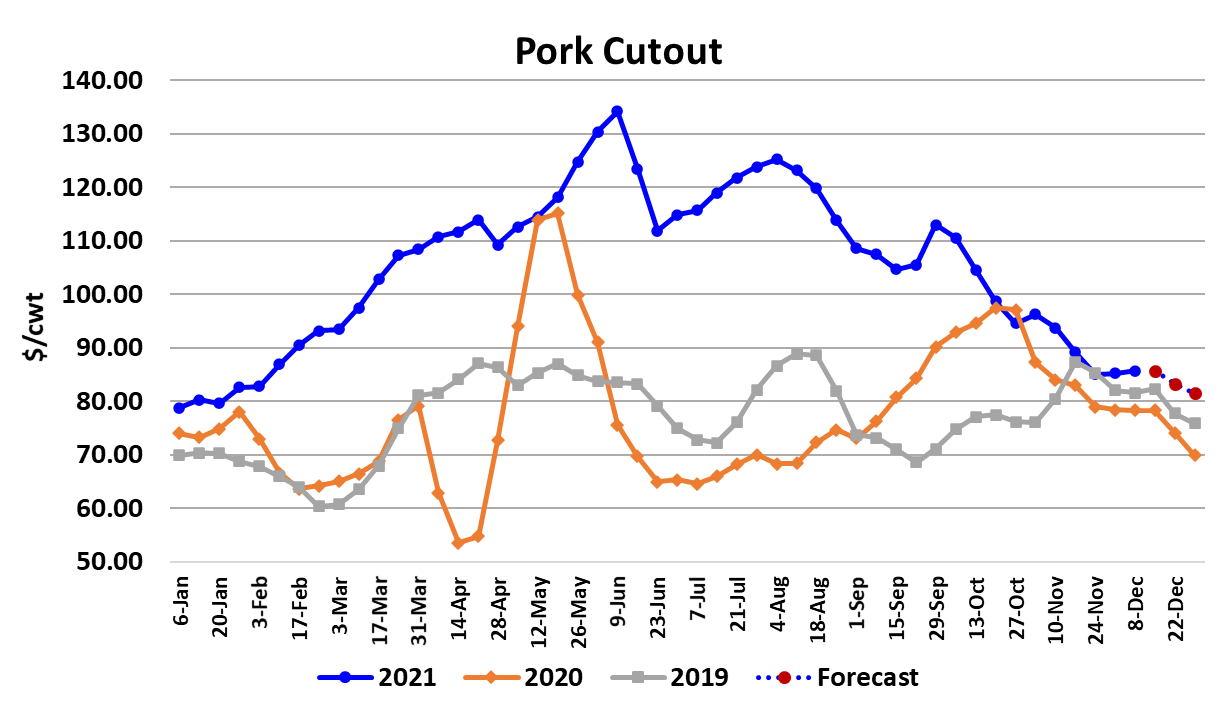

2020 and 2019 the cutout hit a flat spot from late November into

early December before turning lower in the last few weeks of the

year. I suspect that we will witness a similar pattern this year too.

The fact that the negotiated hog markets have moved higher in

the past couple of weeks has given hope to futures traders that

perhaps a new uptrend is now in place. That is possible, but I

suspect that the negotiated markets will struggle between now

and the end of the year if the cutout works lower as expected.

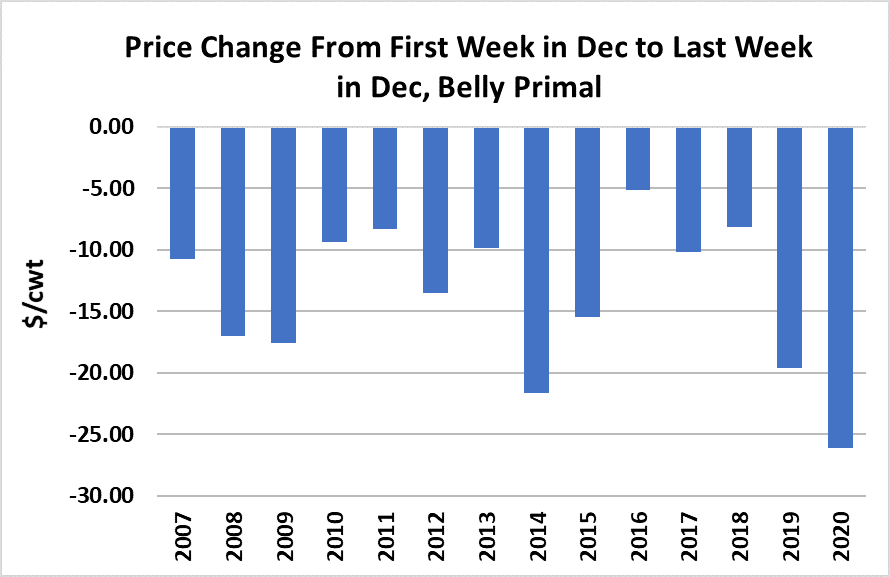

None of the primals posted significant gains or losses this week.

Hams got a big boost from strong boneless ham volumes on

Wednesday, but by the end of the week that effect had dissipated.

The outlook for hams has them trading lower into year’s end. The

chart below shows that in the last 14 years there has not been a

single year where the ham primal hasn’t been lower at the end of

December compared to where it started the month. I fully expect

that to be the case again this year. And, as the hams go, so goes

the cutout. That is the primary factor driving my forecast that has

the cutout working back toward $80 by year end. To be sure,

there are some parts of the carcass that are holding value pretty

well. Butts are one and ribs are another. Unfortunately, they

don’t make up a large enough percentage of the carcass to keep

the cutout afloat if the hams head south. Bellies also come to

mind as a potential source of strength for the cutout, with that

primal up about $10 from the low it made two weeks ago.

However, processing demand for bellies is generally pretty

lethargic during the holidays, so I’m not expecting them to rocket

higher anytime soon.

They could show some modest gains from here however. Export

demand continues to be soft. USDA reported an 8.2% YOY

decline in October exports this week. My guess is that November

and December exports will be down double digits and maybe as

much as 20% lower than last year. So, while pork production is

certainly smaller than it was last year, a lot of that benefit is being

negated by the slowdown in exports. Further, there has been a

surge in pork imports. In October, imports registered 35% above

last year. The net effect is that per capita availability during Q4 is

almost the same as it was last year. However, the cutout is about

$10 higher than it was in Q4 last year. That gives a pretty clear

picture of how much this year’s extra domestic demand has been

worth in Q4. That domestic demand strength is fading now that

stimulus money is in the rear-view mirror and vaccines have

allowed many consumers to resume normal lives.

The cutout demand index peaked in Q2 at 1.23, dropped to

1.16 in Q3 and for Q4 I’m projecting it to be around 1.13. I’d

expect that demand erosion to continue into Q1 unabated

unless the new COVID variant is able to evade the existing

vaccines and forces consumers back into the “stay-at-home”

mode that gave us the huge demand boost in the first place.

Balancing against that rather bearish demand outlook is a

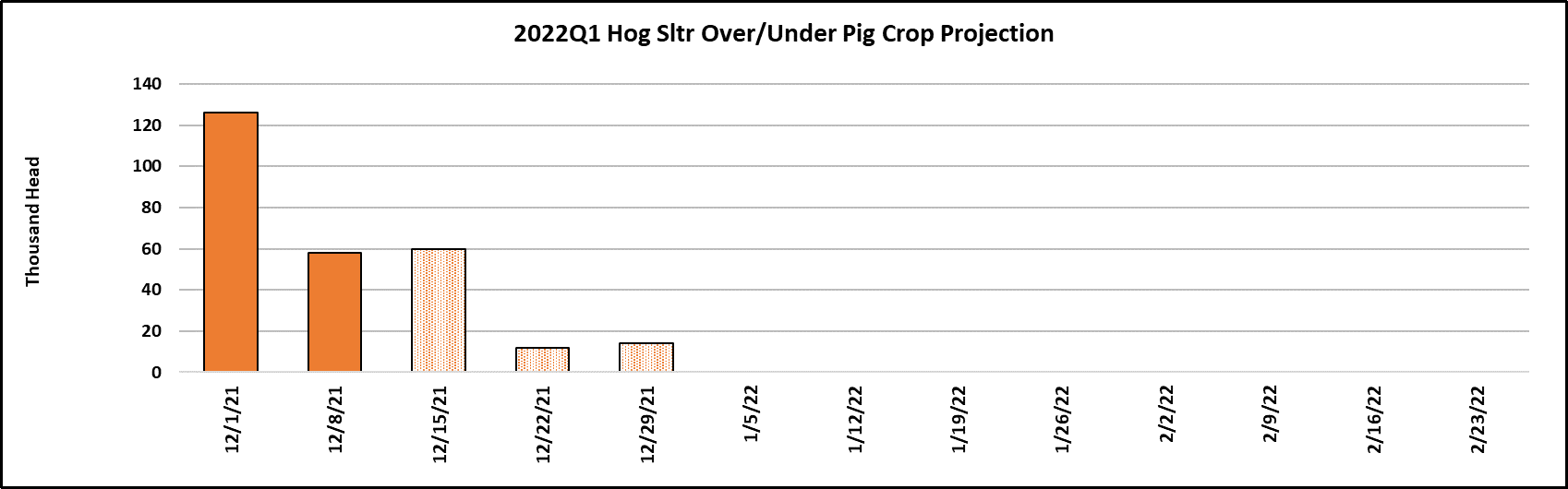

rather bullish supply picture. USDA pegged the pig crop that is

now being killed down 6% and that should keep hog and pork

supplies quite snug over the next few months.

However, we are two weeks into killing that summer pig crop

and already the kills have been almost 200k above what the pig

crop implied. Maybe the hog supply isn’t as tight as

advertised. The fact that negotiated hog prices turned higher

over the last couple of weeks tends to support the idea that

some supply tightening is occurring. This week’s kill came in

at 2.6 million head, down from 2.66 million the week before. I

see a pretty big kill coming our way next week—perhaps 2.67

million head—as packers try to get a little ahead of the holiday

weeks. Once we get beyond the holidays, the pig crop points to

kills around 2.5 million head per week or slightly under. That is

when we will get the best read on whether or not USDA was

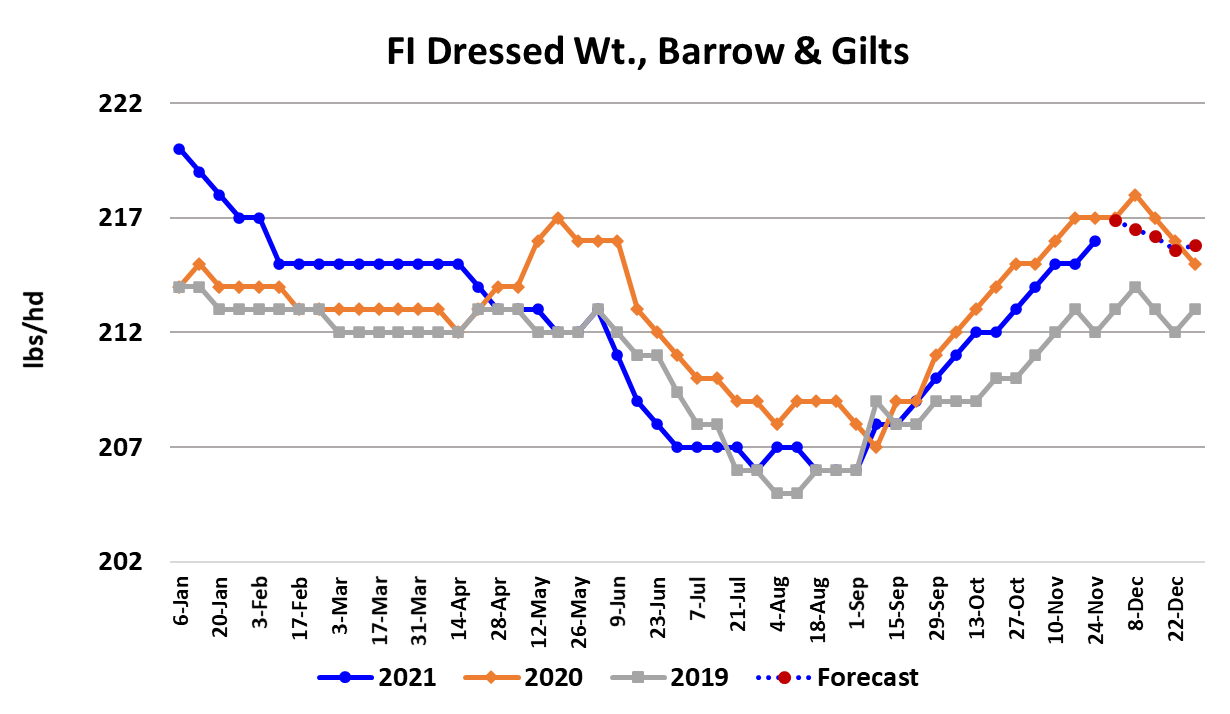

accurate with their pig crop estimate. Barrow and gilt weights

gained another pound this week and likely will add another

pound next week before flattening into January. Weights are

not excessively heavy, but they are not light either, and that is

adding to pork production.

The hog producing regions in the Midwest have seen

unseasonably warm temperatures over the past couple of

weeks and that is forecast to continue at least another week.

Anytime producers can dodge bitter cold weather in December

it is going to improve weight gains. So, if we look on the

surface at a 6% smaller summer pig crop, then yes it looks

pretty bullish, but when we consider the weight situation and

the fact that kills are already running higher than advertised,

that takes some of the luster off of the bullish supply argument.

Next week, watch the hams for possible price cracks and daily

kills for indications that the weekly total will be larger than what

the pig crop suggested once again.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}