Pork Wrap December 08

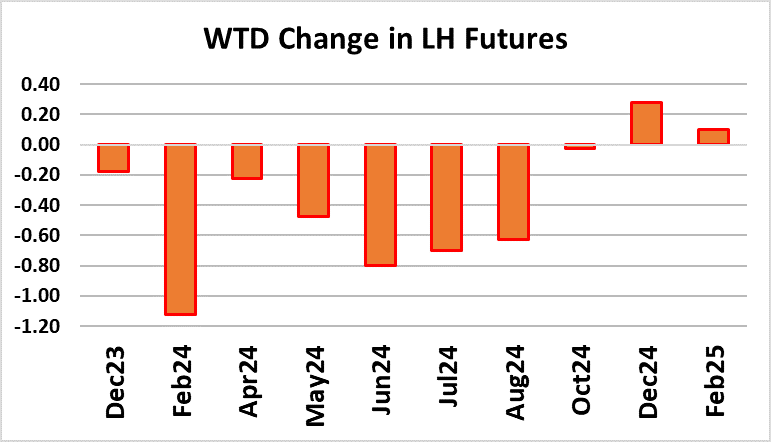

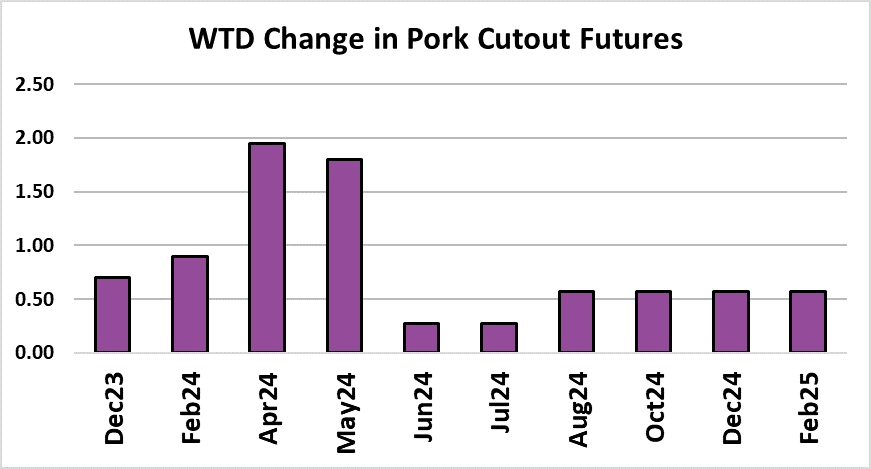

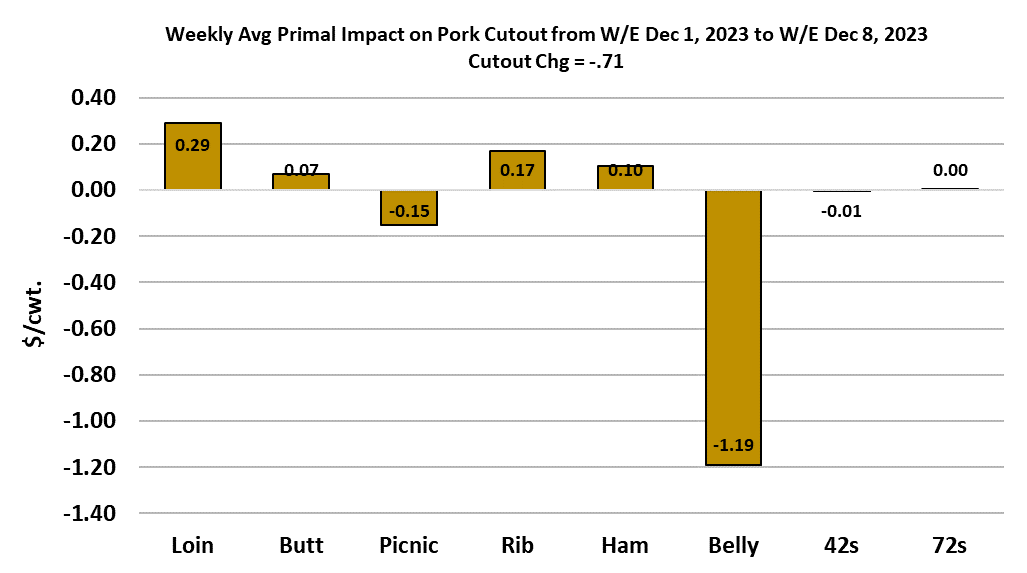

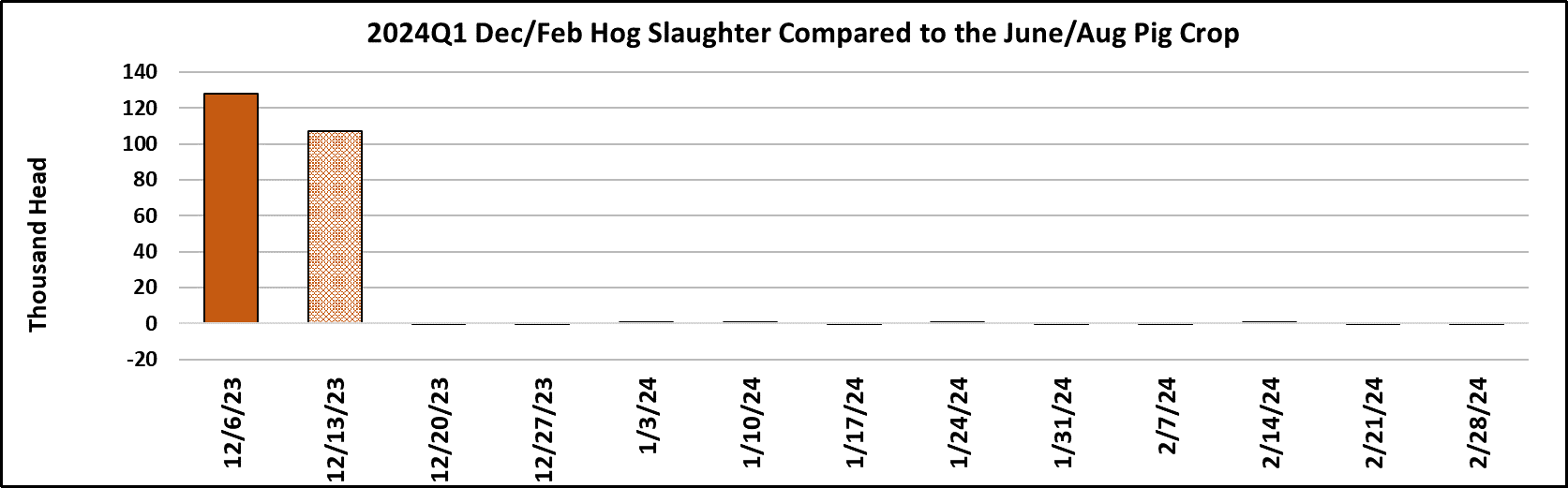

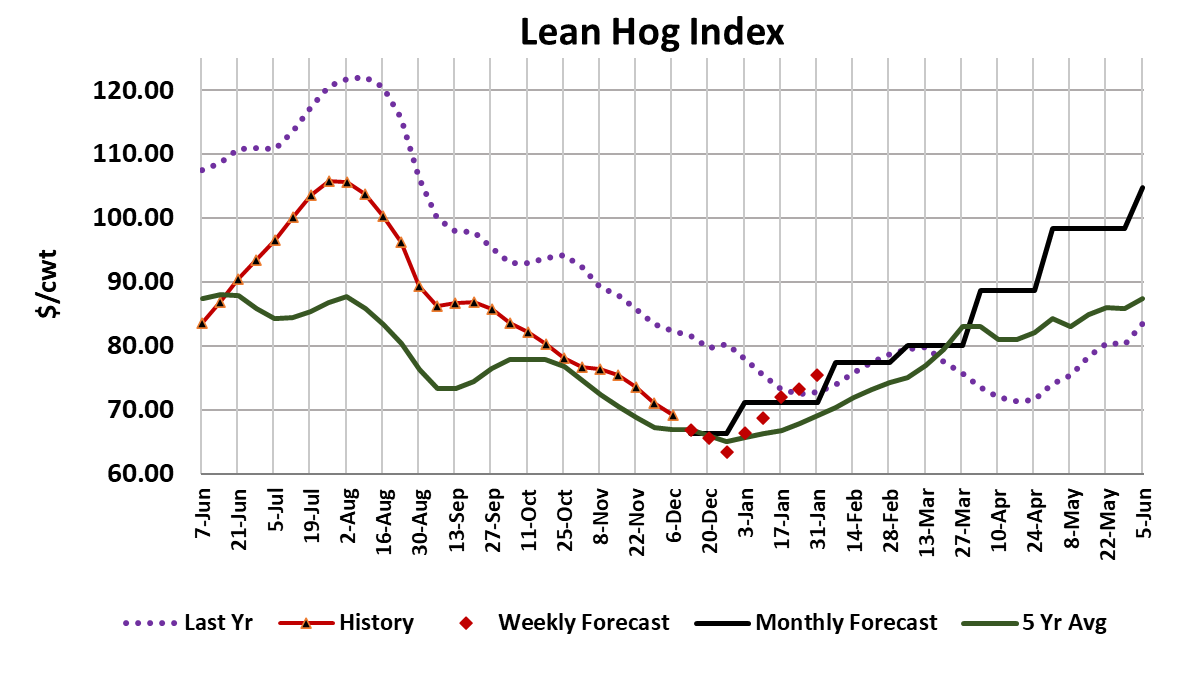

The pork cutout eased a little bit more this week, dropping $0.71/cwt. to average $84.27. However, the negotiated hog markets came under substantial pressure, with the WCB price dropping $3.75/cwt. on a weekly average basis and the NDD price down $4.54/cwt. There is a very real possibility that some hogs will trade for less than $50 in the negotiated market next week. With hogs losing ground much faster than pork, packer margins expanded to $28/head. I must admit that packer margins have gotten much wider than I would have anticipated just a month or so ago. The root cause of that, I believe, is that there are far more hogs out there than expected, and they just keep coming. This week’s kill came in at 2.69 million head. Not far off of the 2.7 million head recorded the week before and my crystal ball says that next week’s kill might reach 2.68 million head. In light of those numbers, it is pretty amazing that the pork cutout was only down less than a dollar this week. All of those hogs need to find a packer to slaughter them and the way that hog producers incentivize packers to kill an abundance of hogs is to make the hogs cheaper and thus put more money in the packer’s pocket. This was the first week of the Dec/Feb quarter and you can see from the attached chart that we have already over-killed the Jun/Aug pig crop by about 125k and next week is looking almost as big. This doesn’t bode well for hog producers. We already know that last quarter’s slaughter was over 500k more than what the pig crop implied and the way that this quarter has started, I wouldn’t be surprised if the cumulative over-kill reaches 800k or more by the end of February. The Midwest is seeing very mild temperatures for this time of year and the forecast has them staying warmer than normal at least until Christmas week. That does two things. First, hogs will gain better in milder weather, and second, conception rates will be better in milder weather. The first item is bearish for the near-term market and the second item is bearish for the longer-term picture. Of course, weather is a fickle thing and it could turn very cold in Jan/Feb and thus negate any productivity gains it provided in December, but given that there are already too many hogs on the ground, the prospect of better-than-expected productivity could just prolong the financial pain that hog producers will be forced to endure this winter (and possibly spring). This week, barrow and gilt weights caught up with last year and may rise above last year in the next few prints. My sense is that hogs are gaining weight well and in the next couple of months we might be talking about heavy hogs becoming burdensome on the market. We are not there yet, but it is something to keep an eye on. Overall, I rate the supply side of this market as pretty bearish right now. On the demand side, the combined margin moved a little lower this week, which means we have yet to reach the bottom in this demand cycle. It is encouraging that the rate of decline is fairly slow, but consumers are already a bit fatigued by all the pork they have been asked to consume this fall, so there is risk that if huge production continues, the consumer could buckle. The attached chart indicates that it was mainly the belly primal that forced the cutout lower this week. All of the other primals were either slightly higher or slightly lower. Bellies are trading just a little below last year’s dismal performance, and while I’m forecasting them a little higher in the near term, we must keep in mind that as we moved into 2023, the bellies didn’t improve hardly at all from January to May. If that happens again in 2024, it will be a difficult spring for both the cutout and hog prices. I’m also a little concerned that the hams may be losing some momentum and could accelerate lower as we get closer to the holidays. If both bellies and hams are underperforming, it will be difficult to move the cutout higher. Right now the forecast has the cutout drifting lower towards a bottom around $80 at the end of this month and then slowly working higher as kills start to moderate seasonally after the first of the year. If I’m wrong on that forecast, I’m probably too high because there are certainly plenty of supply concerns that could ultimately render today’s forecast too high. At one point, I was expecting Dec hogs to expire near $77 and it now looks like they may go off of the board a full $10 below that. Seasonally, the Feb contract should expire a few dollars over Dec, but with the way the supply side looks right now, it is entirely possible that prices keep on easing right through January and give us a Feb expiration in the $60s. This week, USDA reported total pork exports in October were up 6% YOY at 572 million pounds. Given relatively low pricing in the complex this fall, it seems reasonable that exports for November and December will also be above last year. Producers are fortunate that international buyers are helping to siphon off at least a portion of the large pork supplies they have been generating, otherwise price levels would be lower. There is not a lot to be bullish about at the moment. Domestic demand is weak compared to other years, hog supplies are huge, and carcass weights are getting heavier. Perhaps the best we can hope for is continued gentle easing in prices through December with some hope that supplies will moderate enough in January to give price levels a modest lift. Next week, expect more of the same: softer cutout and cash hogs and further expansion in packer margins.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}