Pork Wrap December 01

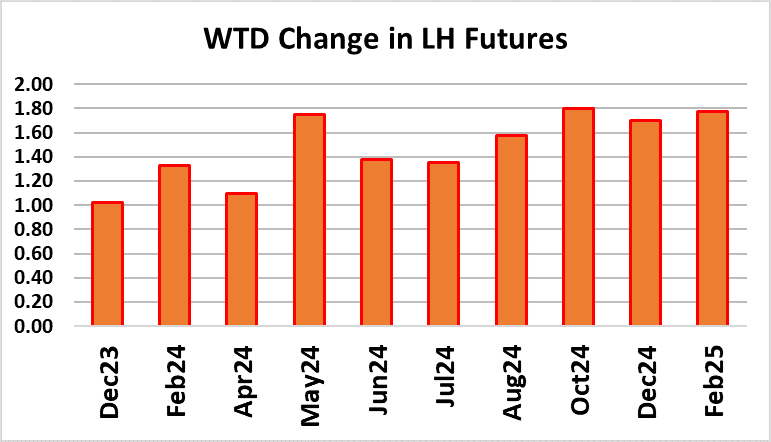

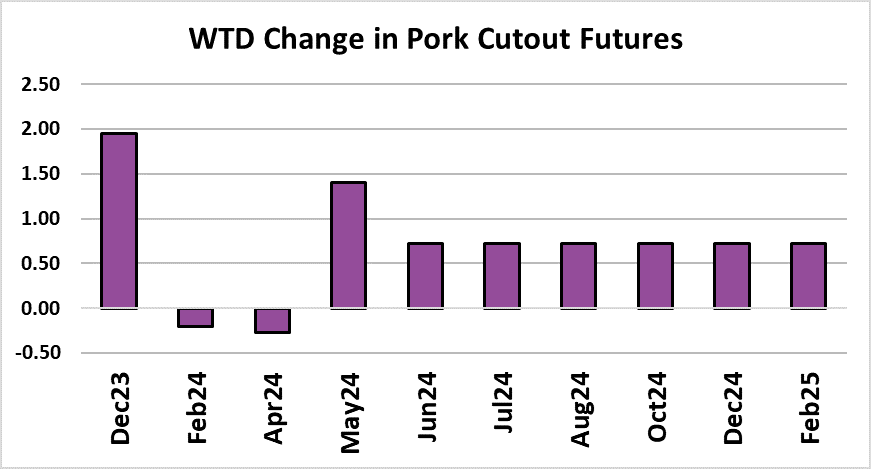

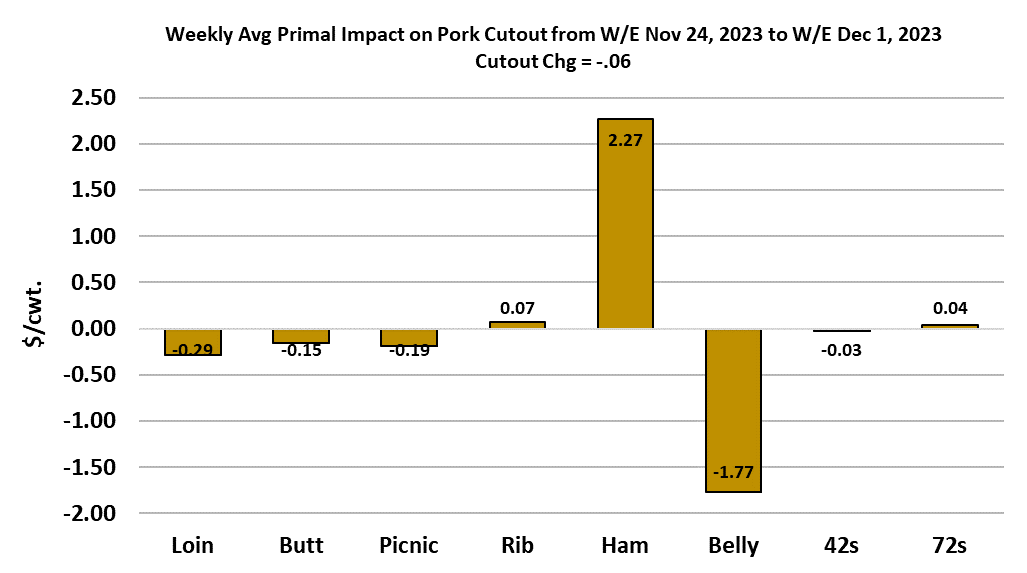

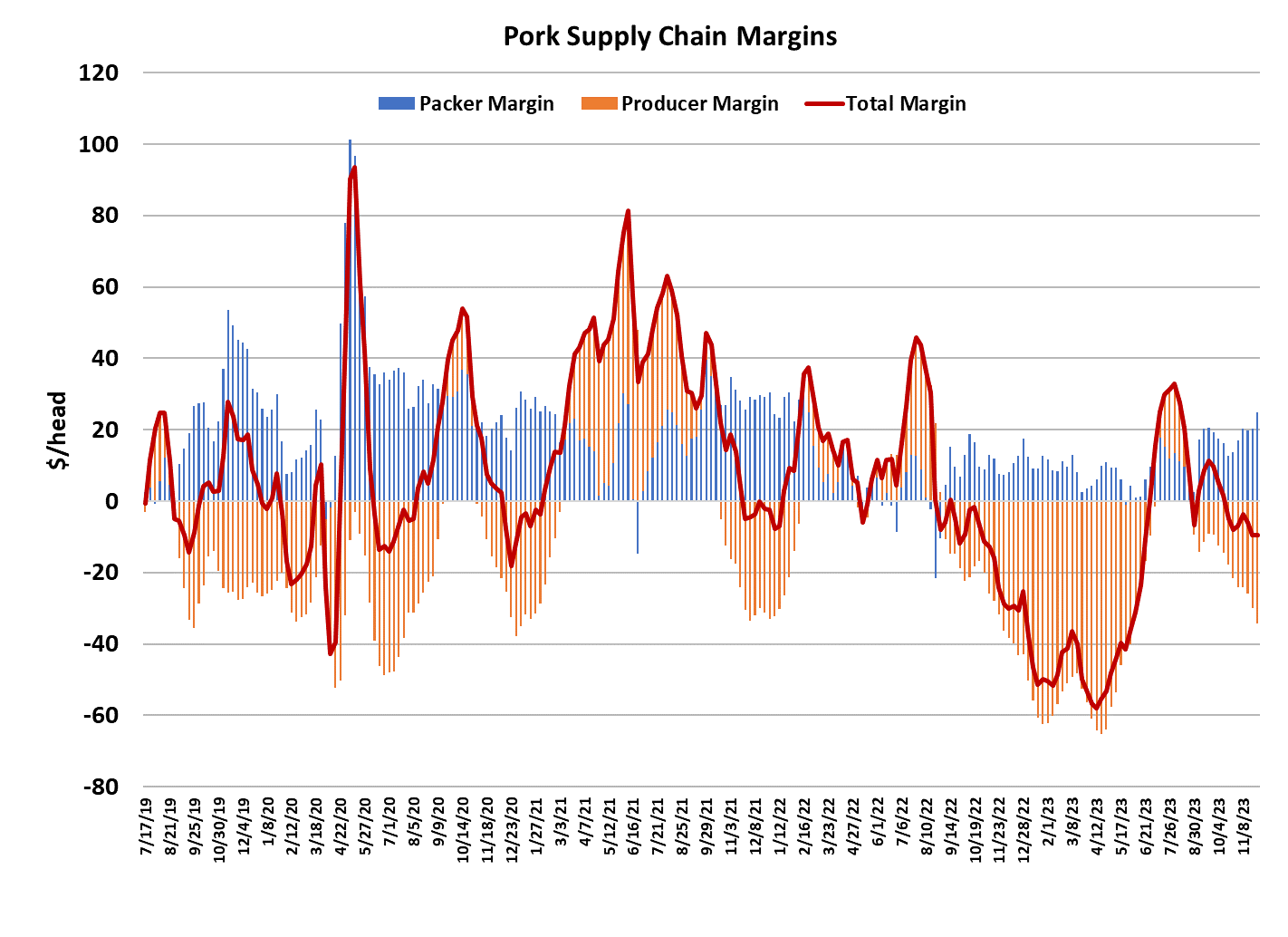

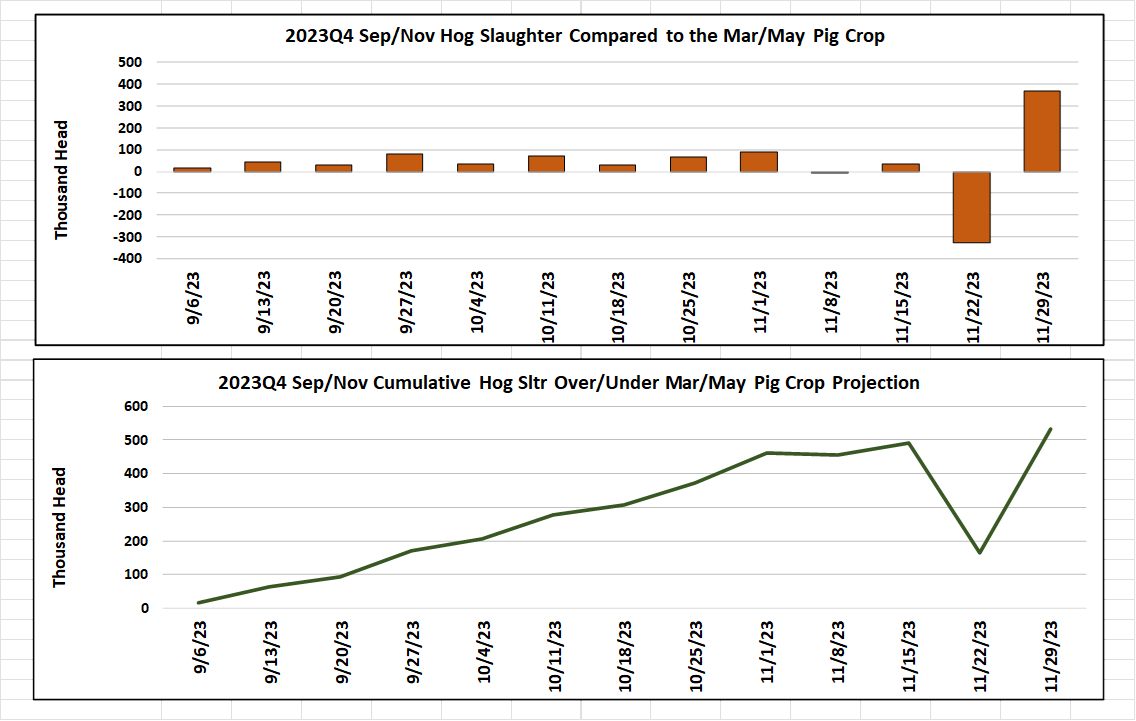

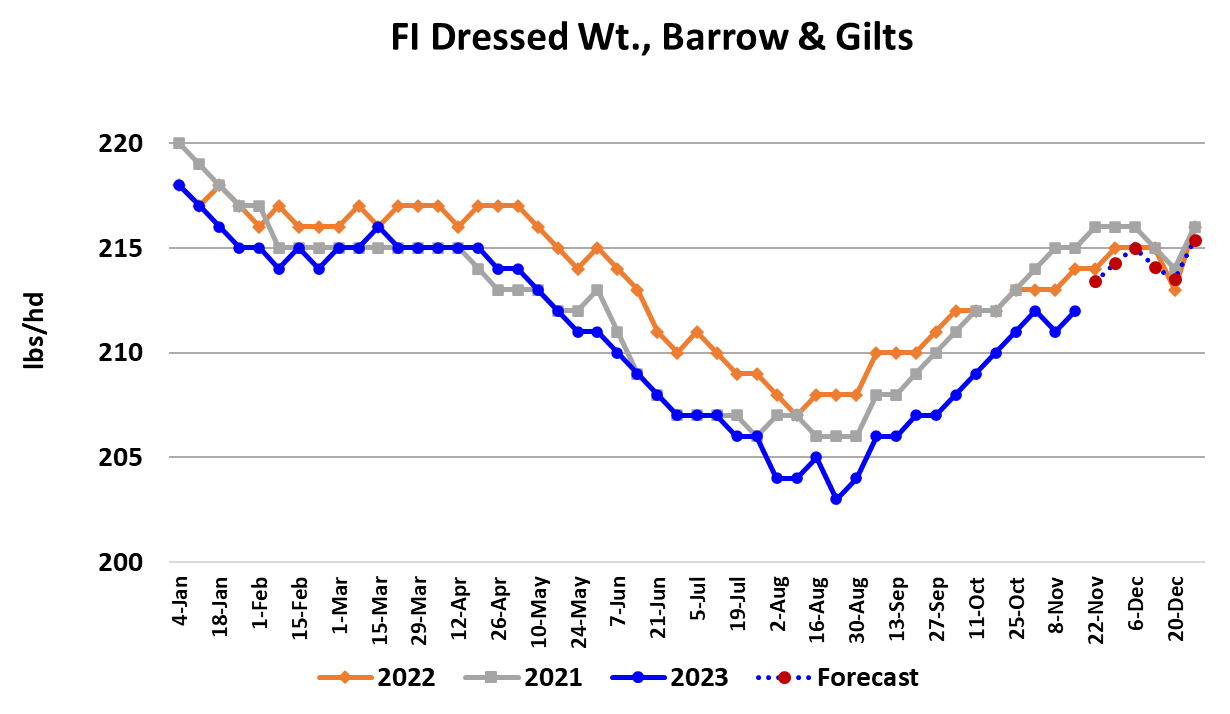

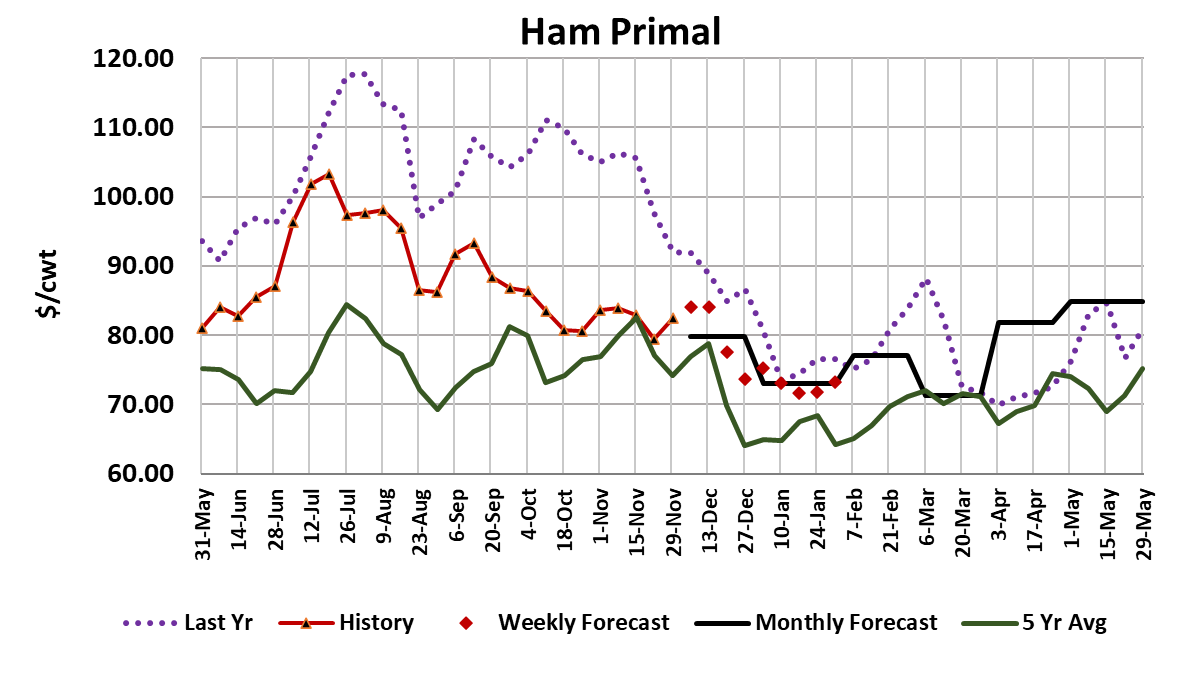

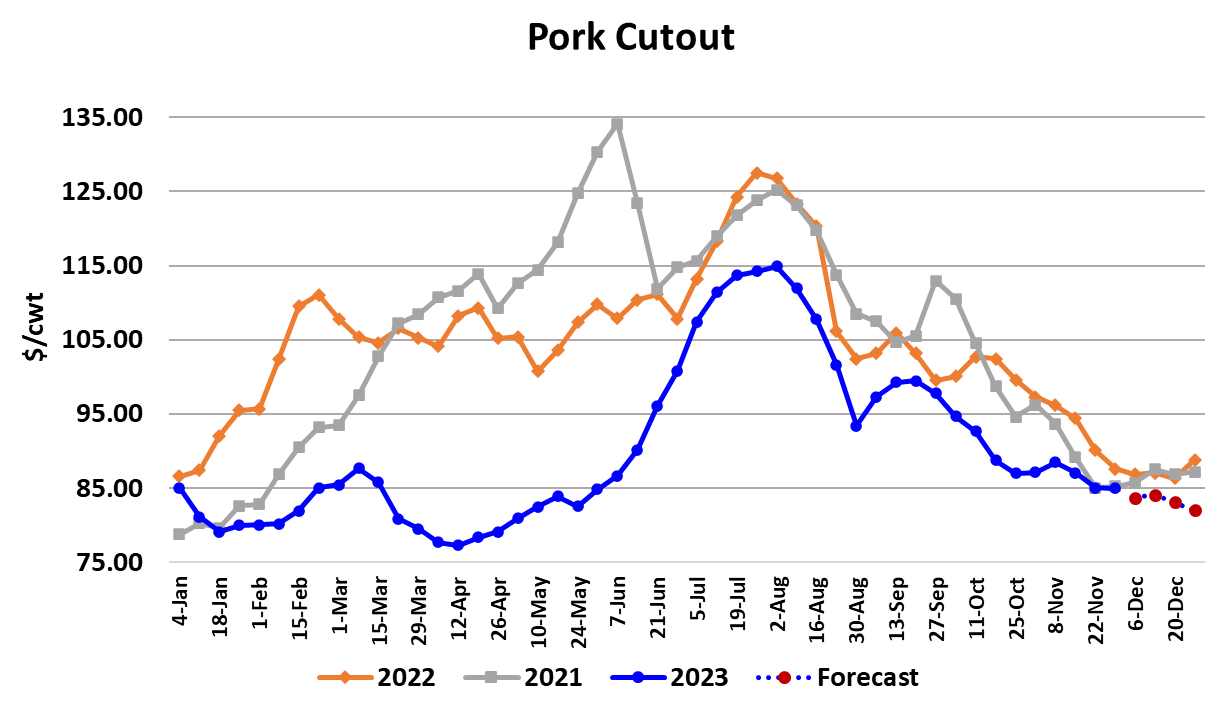

The pork cutout was nearly steady this week, down only $0.06/cwt. from last week’s average. Cash hog prices fared much worse however, as the NDD negotiated market dropped $3.32/cwt. to average $57.91. That caused packer margins to expand to almost $25/head, which is about $5 higher than last week. The action in the cutout this week was mostly a story of stronger ham pricing being offset by weaker belly pricing. The retail cuts joined with the bellies to keep the cutout from rising along with the hams. Ham movement has been really good lately at higher prices and it could be at least partly related to more interest from Mexican buyers following the suspension of Brazilian pork exports to Mexico in connection with a lawsuit filed by Mexican hog producers. That suspension isn’t likely to last long, but for now it may be forcing more sourcing of hams out of the US. On the other side of the coin, there just seems to be very little demand for bellies in the current environment. We know that belly stocks in cold storage are not burdensome, so it would seem that recent low prices would attract some buyers looking to put away bellies for next spring and summer. Week after week, I keep looking for bellies to trade higher, but it never seems to happen. Soon we will be up against the end-of-year holidays and that normally results in very light processing demand for both bellies and hams, so prices could sink further. Last week’s short kill didn’t seem to do much to help packers lift prices this week. This week’s kill came in at an eye-popping 2.7 million head. Packers put together very large Saturday kill that might have been designed to clean up some hogs left un-killed from the end of last week. This was just more evidence that there are more hogs out there than advertised. Coming into the Sep/Nov quarter, I was forecasting the peak weekly kill to be about 2.61 million head, but the industry exceeded that several times and it now looks like the March/May pig crop was under-estimated by about 530,000 head. Next, the industry will start working on the Jun/Aug pig crop, which was reported to be up only 0.4% YOY. The odds remain high that USDA was too low on that pig crop also and we may see weekly kills continue to run above expectations for a while. That will just add more pressure to the cash hog market and the upcoming short kills around the holidays won’t help either. Packer margins have been larger than expected mostly because kills have been larger than expected and that alters the balance between the hog supply and slaughter capacity, allowing packers to extract more margin from hog producers. Farrow to finish margins are running about $35/head in negative territory and could get even worse in the coming weeks. The combined margin was almost unchanged this week, but it still looks to me like it is trending lower. This is usually the point in the calendar when pork fatigue sets in and tempers demand. The good news is that kills are unlikely to be any larger than what we saw this week and that could be helpful to the cutout. The poor margin situation should help drive home to producers that more downsizing is needed across the production sector. Dec lean hog futures will expire in two weeks and the contract settled today at $68.60 and the LHI is at $70.58, suggesting that traders expect the Index to continue declining into expiration. However, it isn’t unusual for the LHI to stabilize or even rise a bit in early December, so it is possible that traders are too pessimistic. On the other hand, the over abundance of hogs this year may keep pressure on negotiated prices and that could be the element that drags the index lower into expiration rather than the cutout. Barrow and gilt carcass weights were reported up one pound this week to 212 pounds and I’m looking for another pound increase next week when the FI data for Thanksgiving week is reported. Weights are still two pounds lighter than last year, but I’d look for that gap to close by the end of the year. Pork exports seem to be healthy and there is no reason to think that they won’t remain that way, especially with many prices near annual lows. I’m still concerned that the big increase in retail prices that was posted back in October carried into November and may stifle pork movement in the midst of big supply. It is already known that domestic pork demand is currently very soft, so the last thing we need is for retailers to keep raising prices and driving consumers to purchase other sources of protein. The next look at future hog and pork supplies will come on Dec 22 when USDA releases the next issue of Hogs and Pigs. It is hard to imagine that it won’t show significant breeding herd liquidation, but there is significant risk that strong productivity will more than offset the breeding herd reduction, thus leaving the industry with yet another huge pig crop to market. Next week, watch the bellies and hams because that is what will move the cutout. If they both get moving in the same direction, the impact on the cutout could be sizable. Also watch prices in the negotiated hog markets for further deterioration as packers take advantage of better leverage and look to expand margins further.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}