Pork Wrap August 31

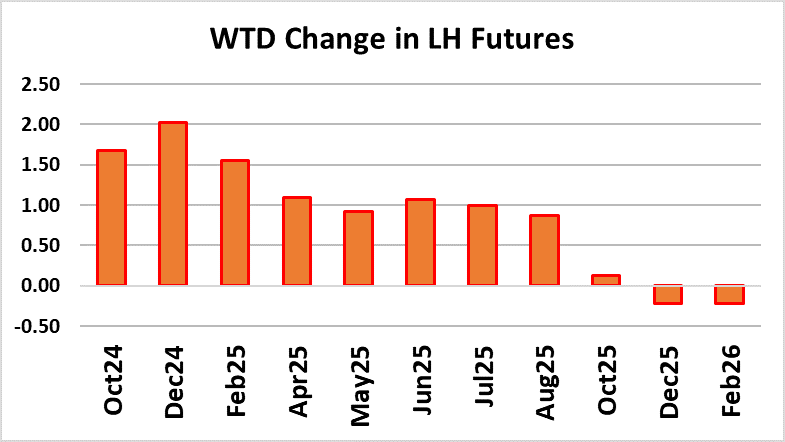

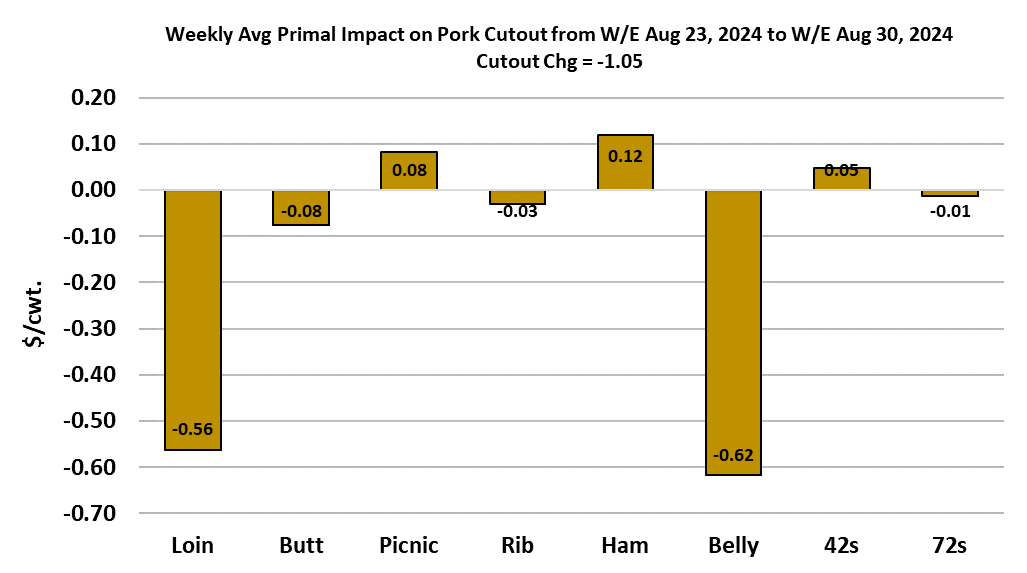

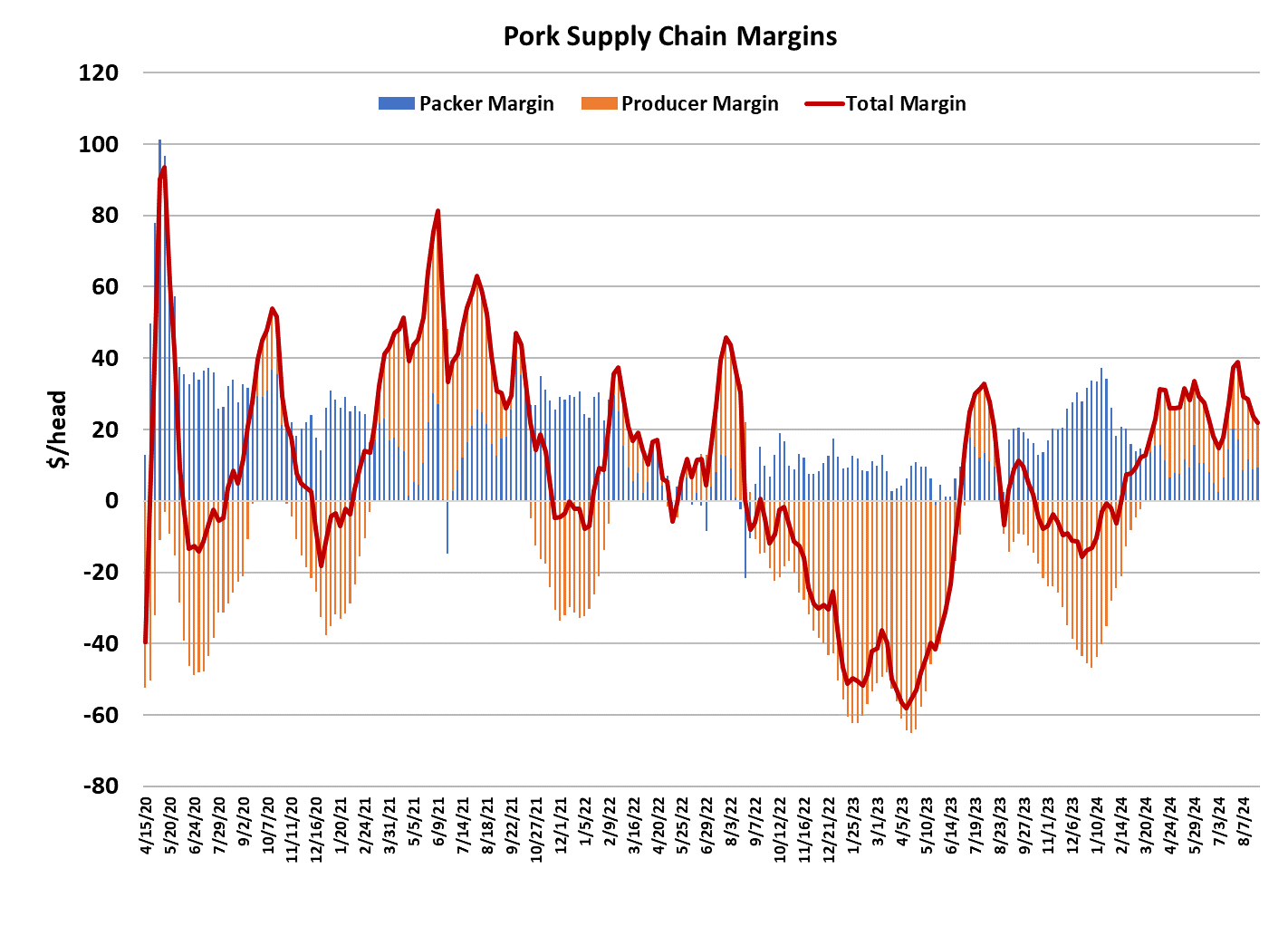

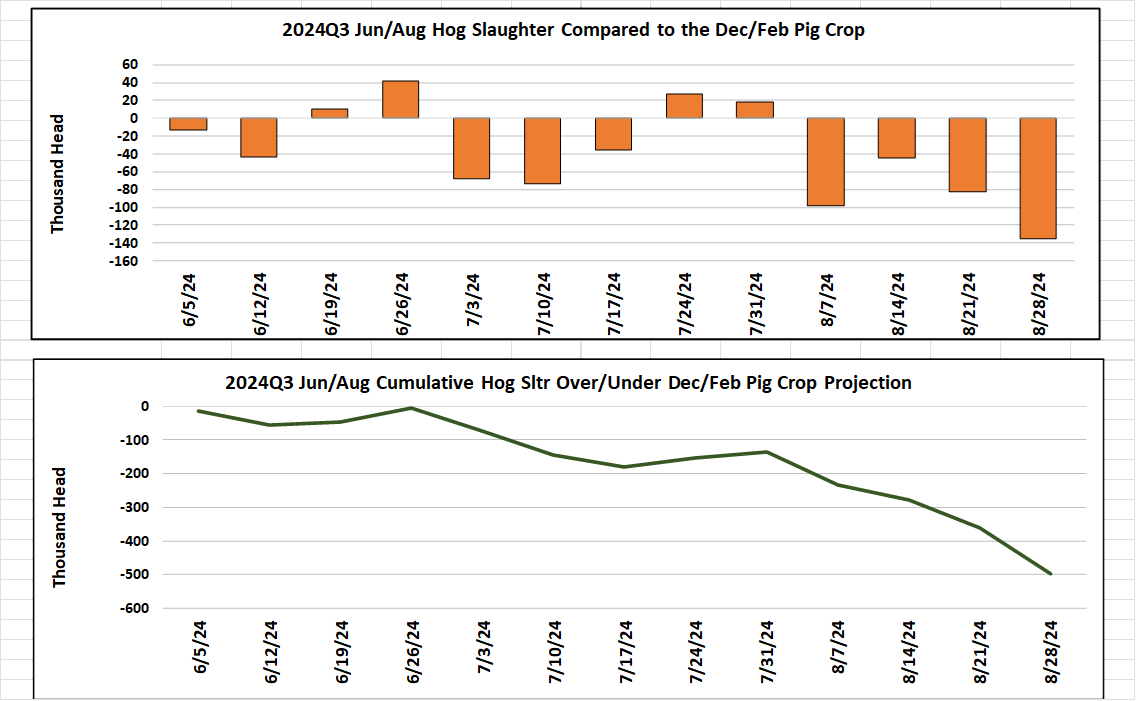

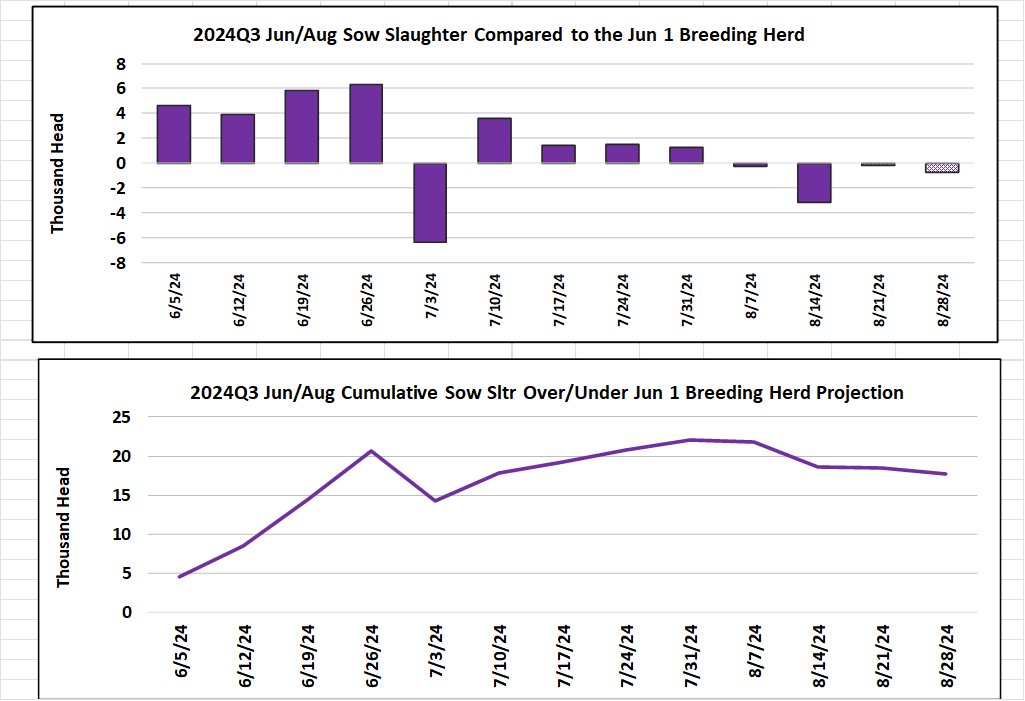

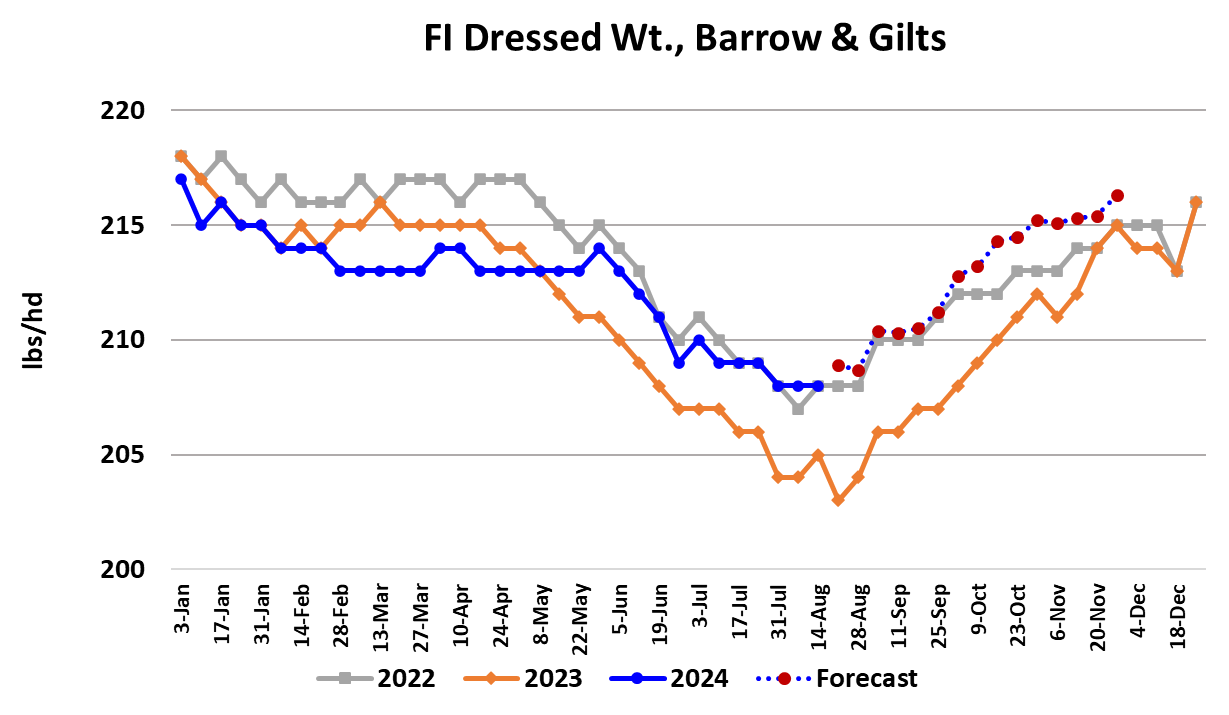

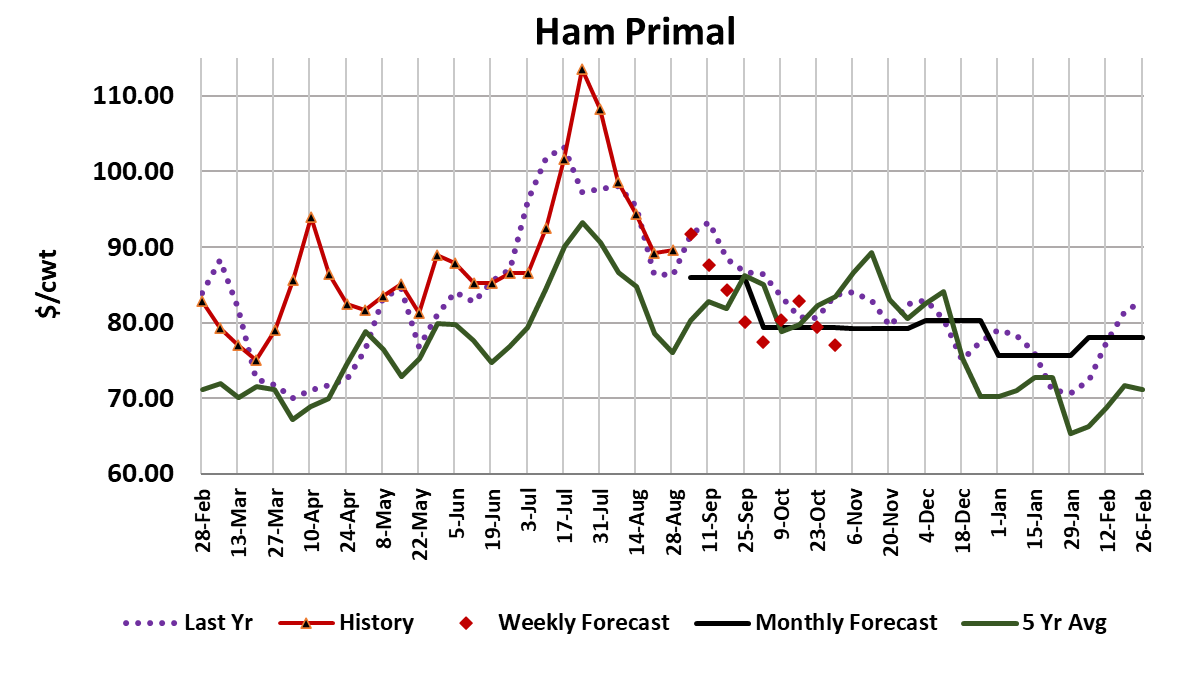

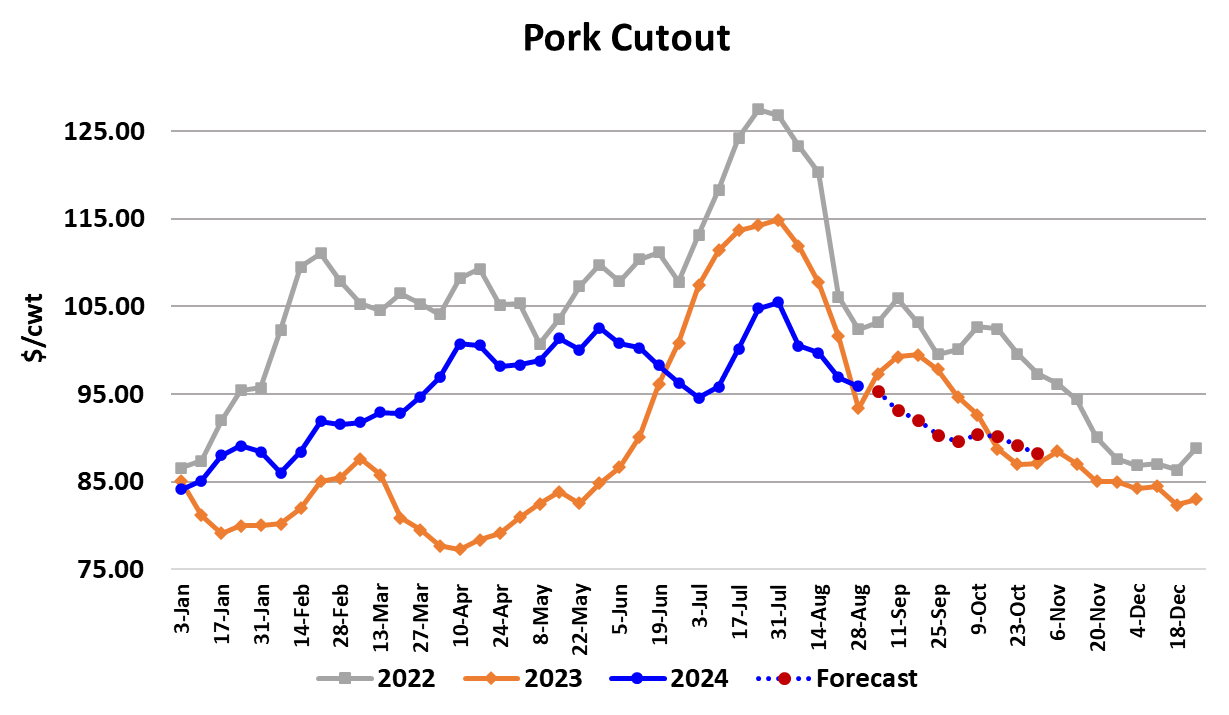

Negotiated hog prices came under pressure this week, with the WCB base price falling $4.50/cwt. on a weekly average basis to $78.11. That was the biggest weekly price decline in almost a year. There isn’t much doubt that hog supplies are increasing seasonally, but some of this week’s big decline is also probably due lighter demand from packers facing a short kill next week. The cutout continued its slow, methodical easing, dropping $1.05 to average $95.89. The October futures moved higher yet again, adding a little over $1.50 on the week and settling at $82.22 today. That puts the nearby futures only about $4 under the cash index, which should print around $86.30 on Monday. This week’s drop in the cutout was driven by the bellies and loins, but neither moved dramatically lower. Hams aided the cutout, but only slightly as the primal was just 0.40/cwt. higher on the week. Hams look set to advance a bit more next week before they start to track lower again. It is very likely that further softening in the other primals will more than offset what the hams might add next week, so the call for the cutout is lower once again. Pork demand isn’t really all that good at the moment, despite the cutout holding in the mid-$90s. I suspect that once kills ramp back up following the holidays, the supply pressure will start to move the cutout downward at a faster clip than what we saw during August. The combined margin is still trending lower, suggesting that the complex is still in a demand downcycle. My guess is that this downcycle will be deeper than the one earlier this summer and could see the combined margin reach zero before turning higher. The most surprising factor in the market recently has been the light kills in the past few weeks. This week’s kill came in at 2.43 million head, which was more than 100k below what the pig crop implied. Now that the Jun/Aug quarter is complete, it looks like the industry under-killed the Dec/Feb pig crop by close to half a million head. We will be keeping a close eye on the September kills to ascertain whether or not USDA’s over-counting of the pigs born extends into the next quarter. Next week’s holiday-reduced kill is projected to come in near 2.24 million head, but after that the March/May pig crop suggests that weekly kills will quickly bounce back toward 2.55 million head. The March/May pig crop was reported to be up 1.8% YOY and those are the hogs that will be slaughtered from Sep to Nov. The attached bar chart indicates that a lot of the under-killing in this quarter happened during August, not June and July. It may also partially explain why the cutout has been reluctant to soften here at the end of summer. The cumulative sow kill in the Jun/Aug quarter is only about 19k larger than normal, given the size of the breeding herd on June 1, which suggests that the culling pace has slowed considerably. In the March/May quarter the number of extra sows slaughtered was around 50k and in the Dec/Feb quarter it was close to 65k. It seems like producers may be abandoning herd reduction effort before the job is done. That doesn’t bode well for pricing in 2025. Packer margins were higher this week and are now close to $10/head. My expectation is that by mid-to-late October, packer margins will be over $20/head. The forecast has packer margins for Q4 as a whole averaging close to $25/head, which would be a 15% increase over last year. If I’m wrong on that, I may be too low because I can envision a situation in November where there are too many hogs for the available hooks and that tends to drive margins sharply higher. Much will depend on how closely kills follow the pig crop projection this fall. Producer margins are declining at a fairly fast clip now and this week the were close to +$12 per head. I think that by the end of September, producer margins will be slipping below zero. Federally-inspected Barrow and gilt weights were reported steady at 208 lbs. for the third week in a row and are probably at their annual low point and poised to move higher in the next few weeks. Weights are currently three pounds higher than last year and with corn prices much lower than last year, I’d expect that differential to persist into the fall and perhaps even expand a bit. With a bigger pig crop and heavier weights this fall compared to last, pork availability should be better than last year. The current forecast has per-capita domestic availability in Q4 up 1.7% YOY and that follows on the heels of a 2% increase in Q3. Next week look for another dollar or so to come off of the cutout and further softening in the cash hog markets.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}