Pork Wrap August 19

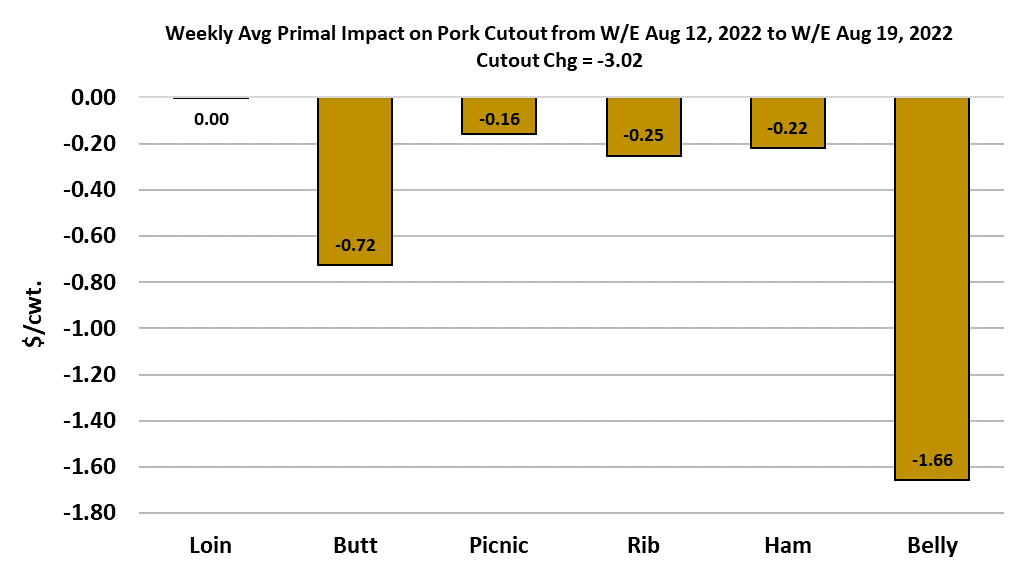

The hog and pork complex continued to ease lower this week as

the cutout dropped $3.02/cwt and the WCB negotiated market

was down $3.32/cwt. The losses in the cutout were largely

driven by big declines in the belly primal. Hams also moved a

little lower, but the downtrend there seems to be slowing.

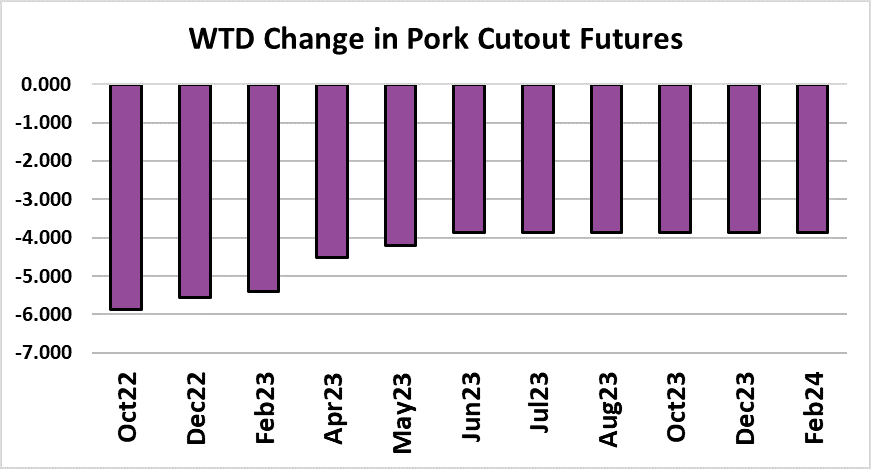

Perhaps the most surprising event this week was the collapse of

the Oct futures, which lost close to $7. It is not unusual for the

next nearby contract to make a big move around the time when

the front month expires, but I had assumed that move would be

upward this time because of the large gap between the LHI and

the Oct contract when the Aug expired. Instead, traders sensed

that a top had been made in the cash market and the fear of a

rapid price decline created a lot of selling pressure in the

futures. That futures selloff took the Oct contract down close to

my forecast for the LHI at Oct expiration, so it is now very close

to fair value.

However, I think the risk to that forecast lies to the upside and

could easily see the Oct contract expiring $5-10 over the $93

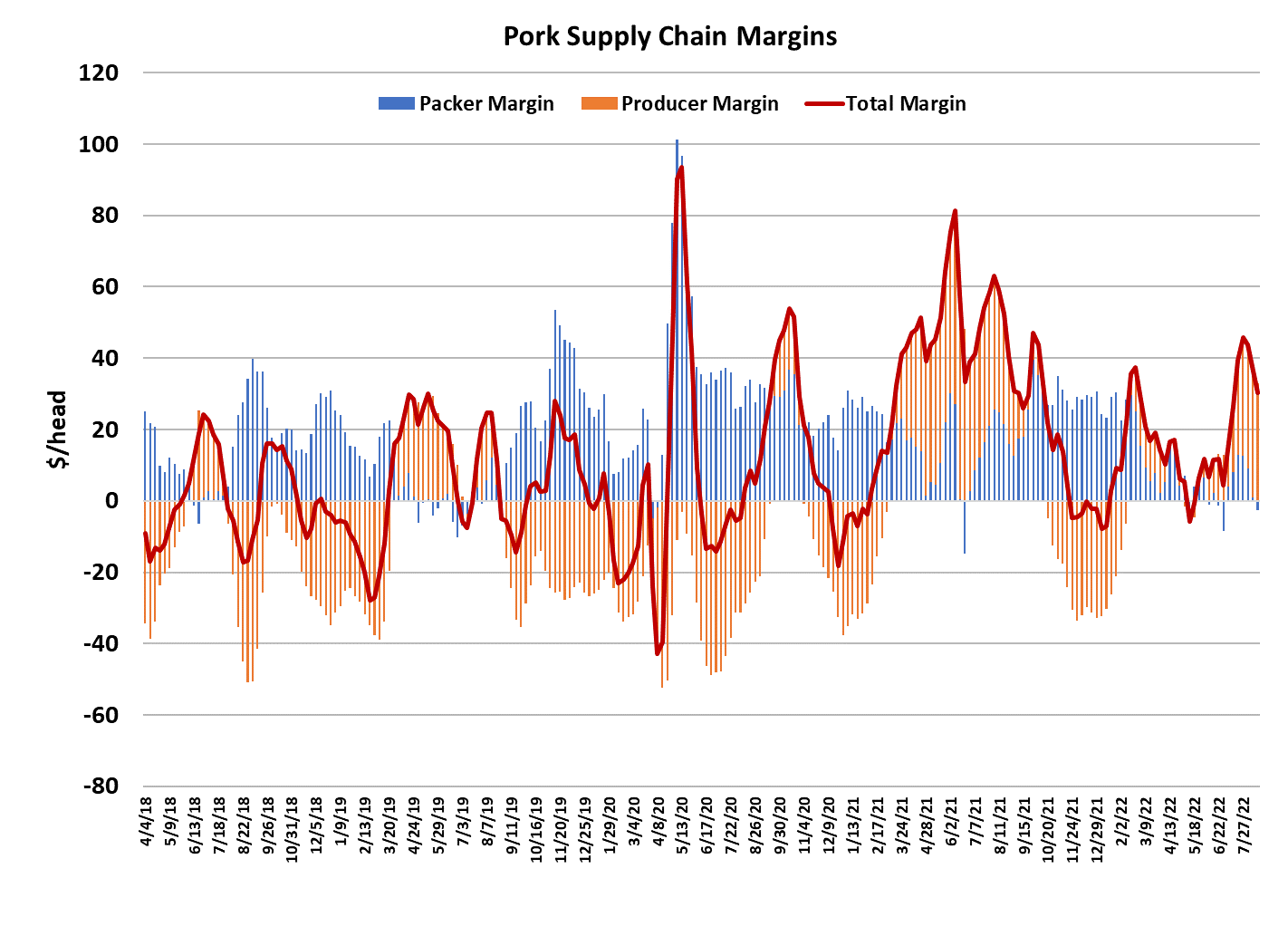

level where it traded today. The combined margin continued

lower this week, helping to confirm that a new downcycle in

demand is firmly in place. If you look closely at the combined

margin chart, you will see that hog producers are the ones

making all of the money in the current market and packers

actually posted a small negative margin this week. That gives

you an idea of who has the upper hand in this market:

producers. The supply of uncommitted, market-ready hogs

remains very tight and as a result, packers continue to pay a lot

for the spot hogs they need to fill out their kill schedules. It is

that tight supply of uncommitted hogs that makes me think

prices in the hog and pork complex won’t decline as fast as the

futures wanted to imply this week.

Of course, hog supplies will grow a little every week as the

seasonal expansion takes hold, so prices should slowly work

lower, but they probably won’t come crashing down as they

have in some years. Skinny packer margins are a symptom of

not enough hogs to meet slaughter capacity and it is pretty

uncommon for packers to still have negative margins this deep

into August. In fact, the last time that packer margins went

negative in the third week of August was 15 years ago. Even in

2014 when PEDv slashed hog supplies, packers managed a

small positive margin throughout August. So, the supply side is

pretty tight. Barrow and gilt carcass weights were reported

another pound lower this week and the DTDS weights also

moved lower.

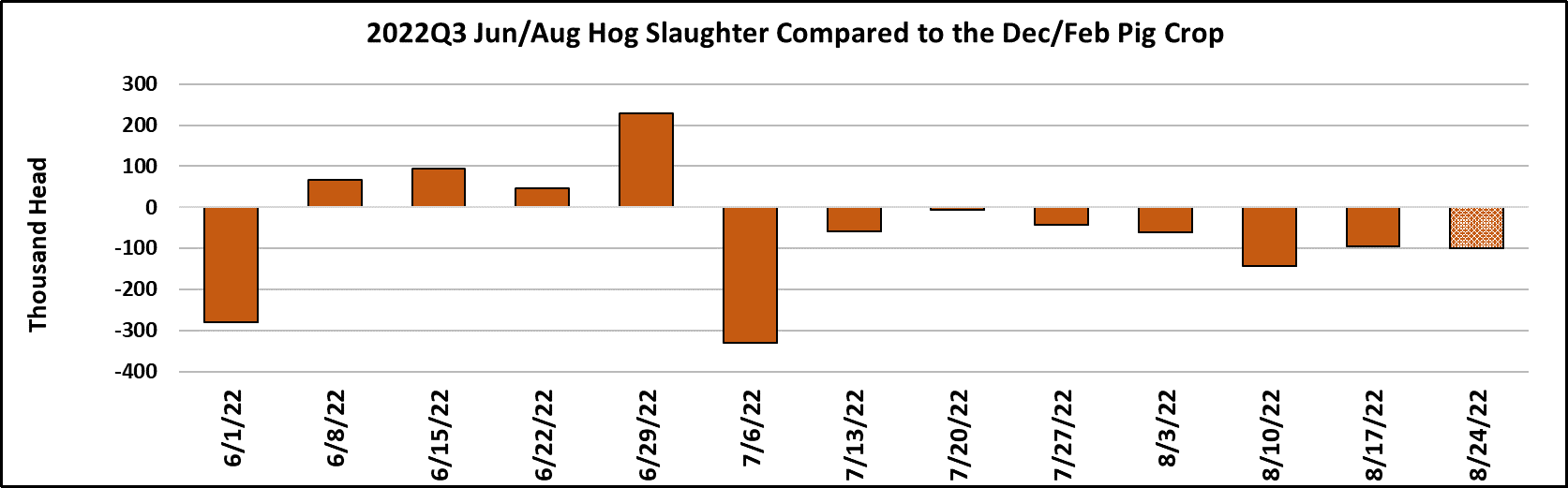

That is another sign of tightness in the hog supply. This week’s kill

registered just a little shy of 2.4 million head, with a small Saturday kill.

Once again, slaughter was below what the Dec/Feb pig crop projected.

It now looks like USDA might have over-estimated that pig crop by as

much as 700k head. Next week’s kill should also be near 2.4 million

head and then there will be two smaller kill weeks around the Labor

Day holiday.Packers will likely give employees the Saturday before

Labor Day off, which will reduce the kill in the week prior to Labor Day,

and then there will be no kill on Monday of Labor Day week. The

holiday will provide packers with a chance to rebalance the hog supply

with capacity and perhaps get their margins back in the black. As we

move into September, the industry will begin killing the Mar/May pig

crop, which was reported by USDA to be down 1% from last year.

Given that USDA clearly over-estimated the Dec/Feb pig crop, we

shouldn’t be surprised if they are a little too high on the Mar/May as

well.

Domestic pork demand does seem to be slowing a little, but most of

that seems to be concentrated in the processing items. Butts

continued working lower this week and are nearly back to where they

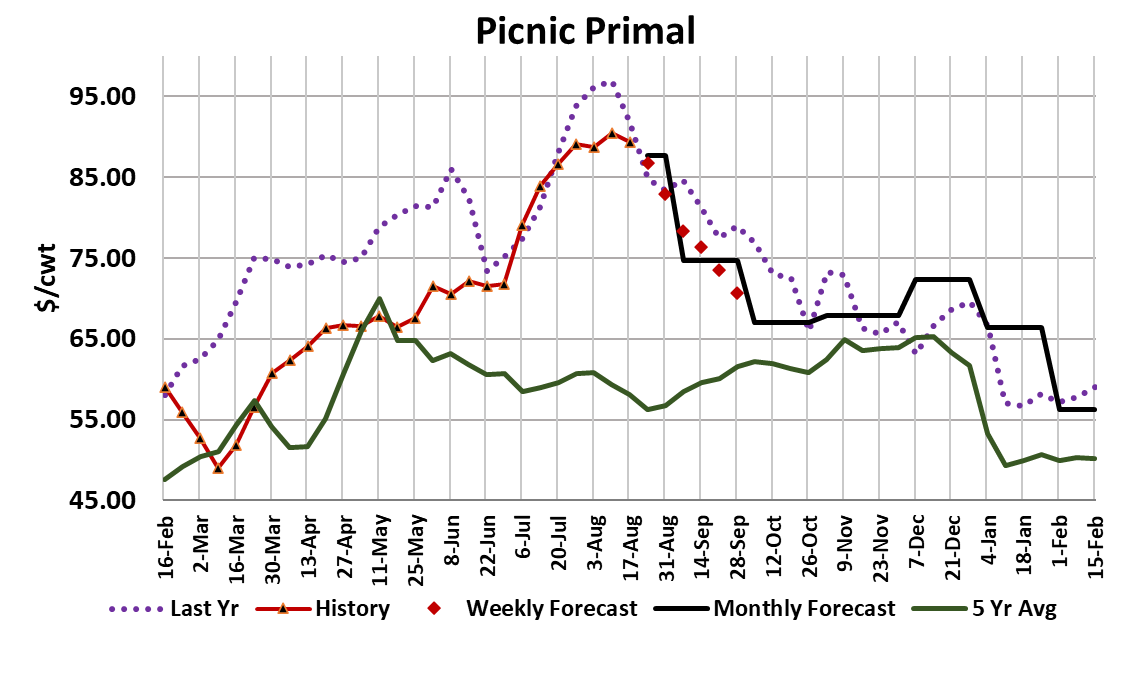

were this spring before the great summer rally began. Picnics seem

to be following the same pattern as butts, only a month or so behind

them. Picnics are currently topping and are forecast lower from here.

The trim products remain firm and that could slow the decline in the

picnics, which are often used in the same applications as trim. Loins

should see good retail interest just after Labor Day and so I think they

can hold current values for a few weeks longer. There is not much

doubt that the majority of pork items will see lower pricing in the next

couple of months as hog supplies expand and the demand downcycle

continues.

There is less certainty around how fast the price declines will come.

With spot hog supplies so tight, packers may have to keep the kill

contained by necessity and thus the product markets could outperform

my forecasts in the next few weeks. There isn’t much new to report in

the export markets. Weekly volumes seem to have stabilized at a level

that is about 5-10% below last year and I don’t see any reason for that

to change in the next couple of months. Next week, look for the cutout

and the negotiated hog markets to continue to ease as supplies slowly

grow. Futures are likely to recover some of this week’s huge selloff.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}