Pork Wrap August 18

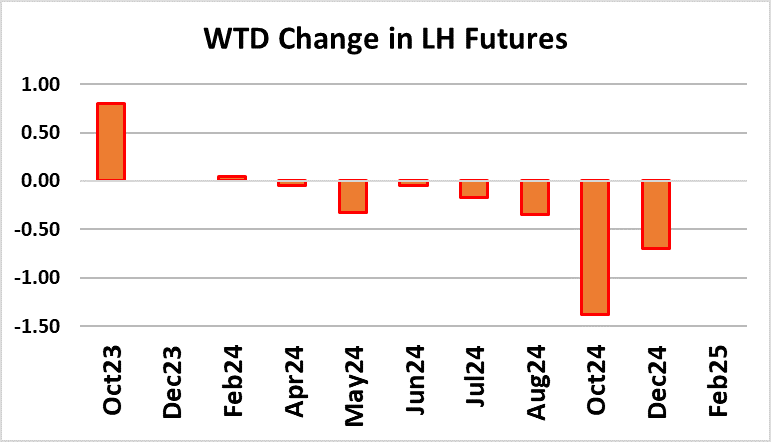

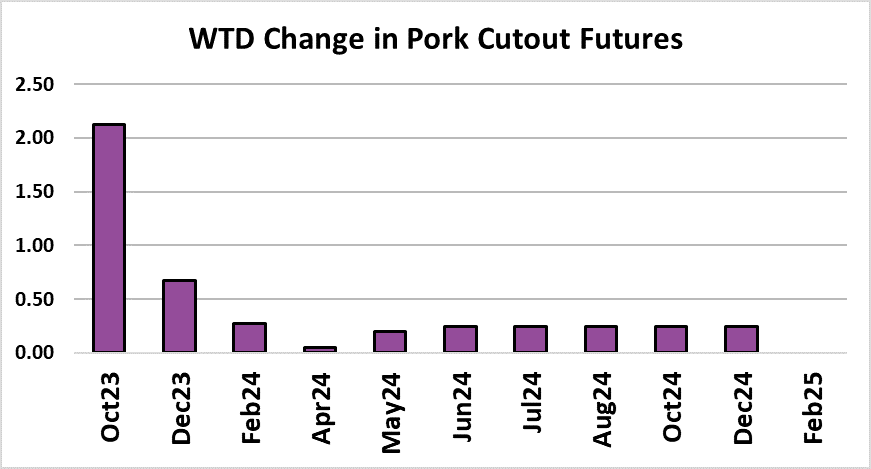

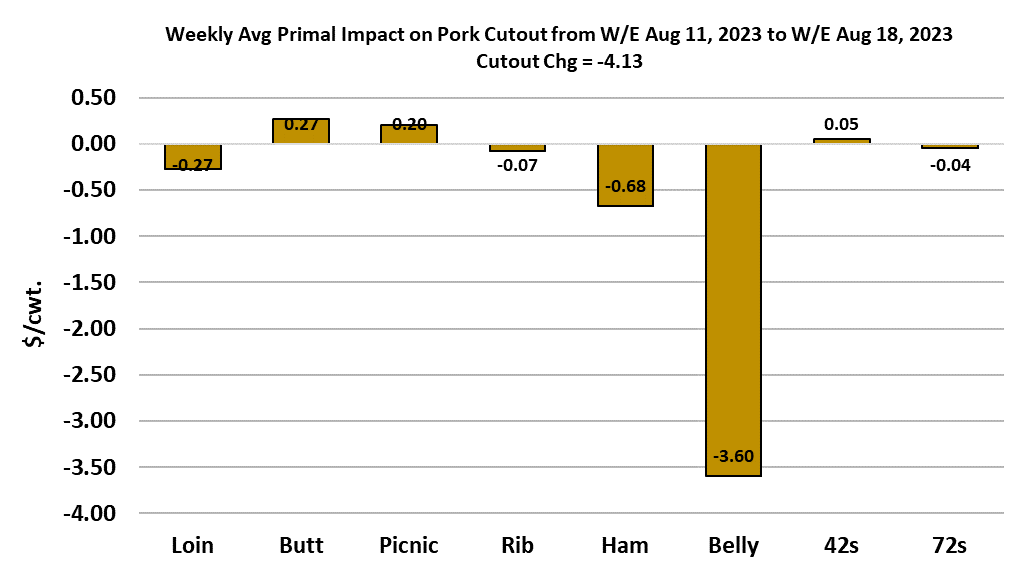

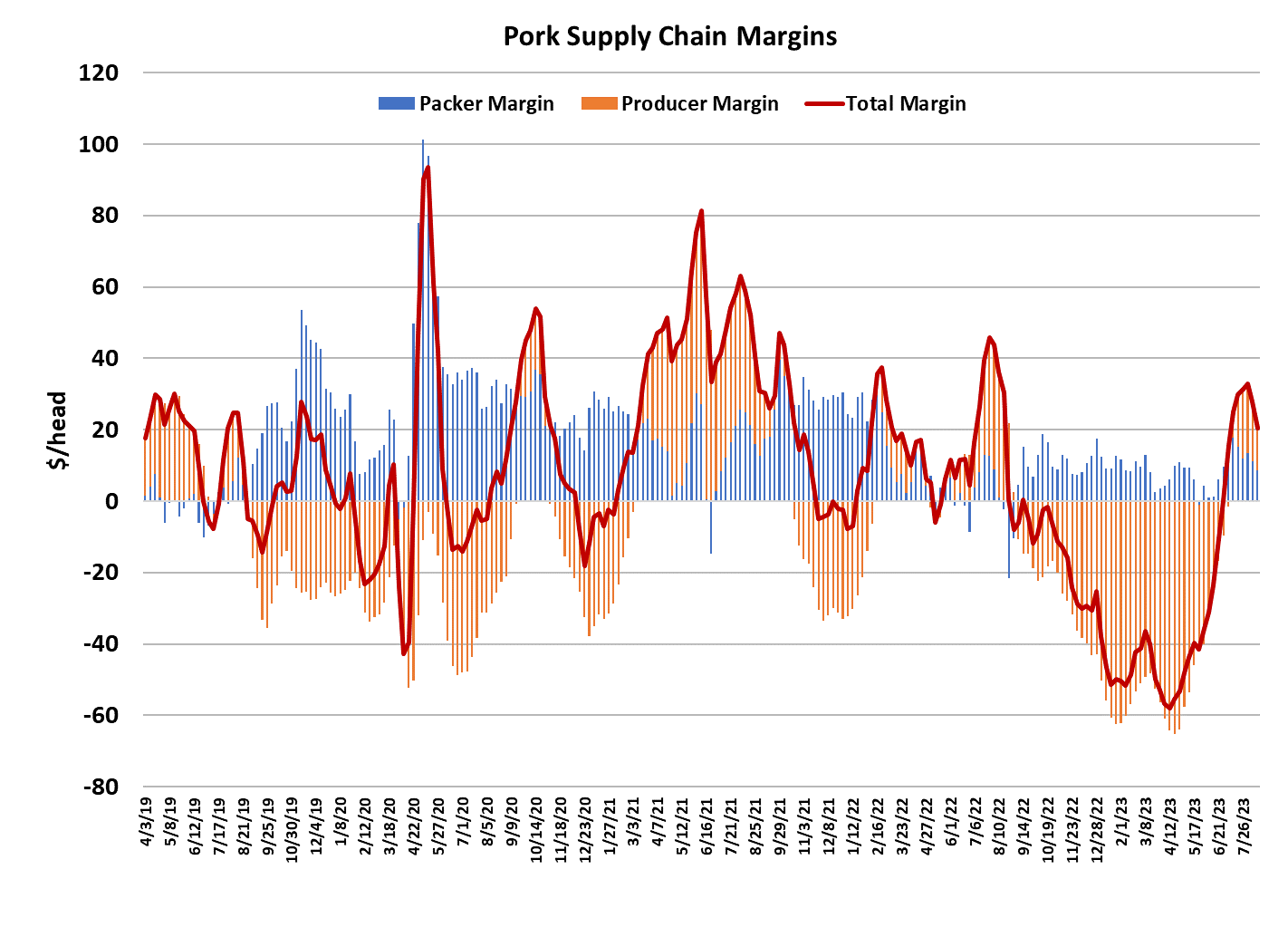

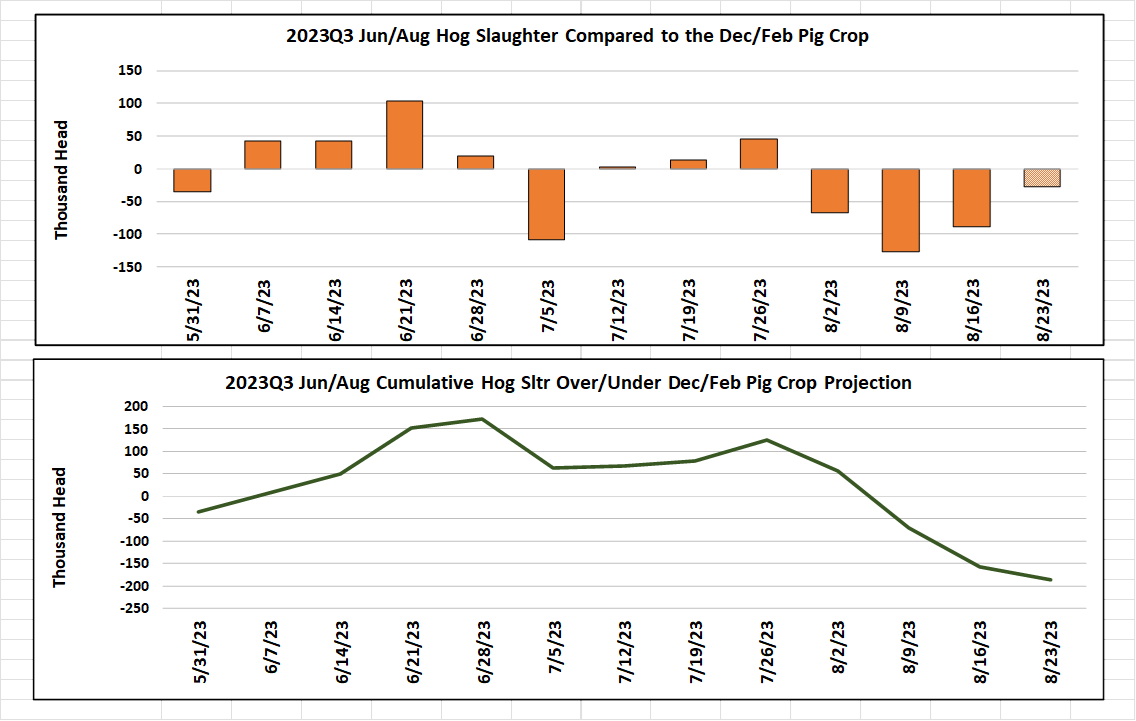

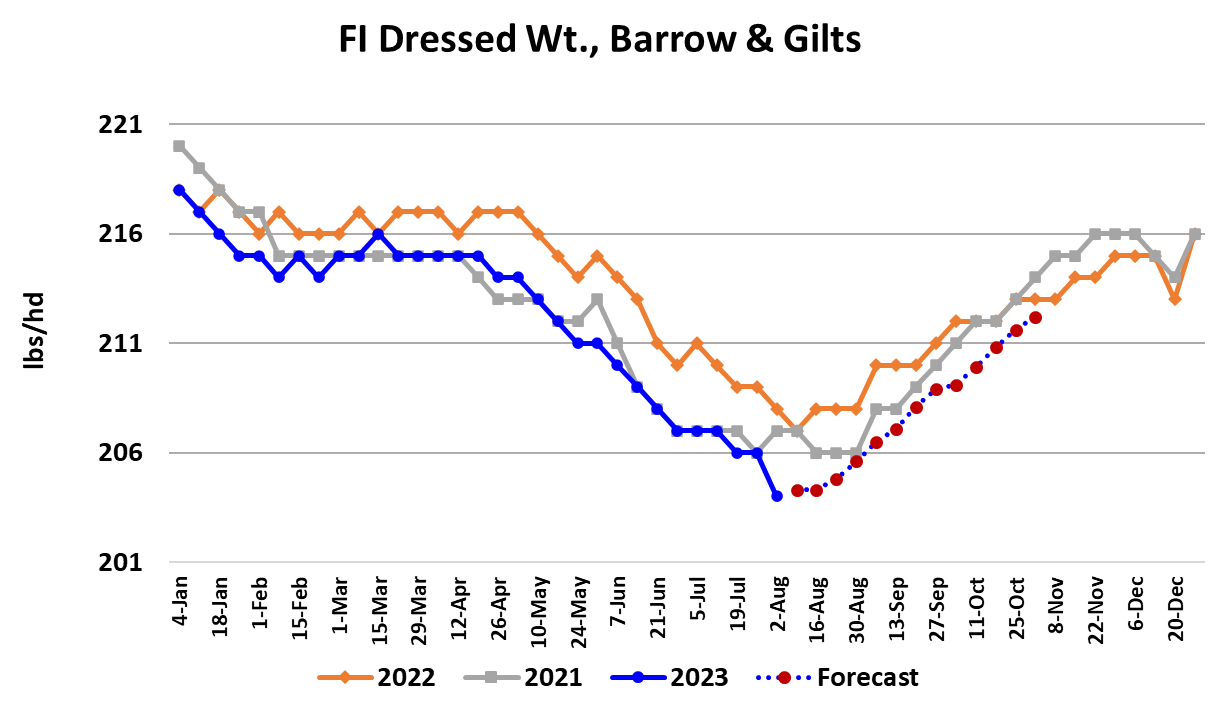

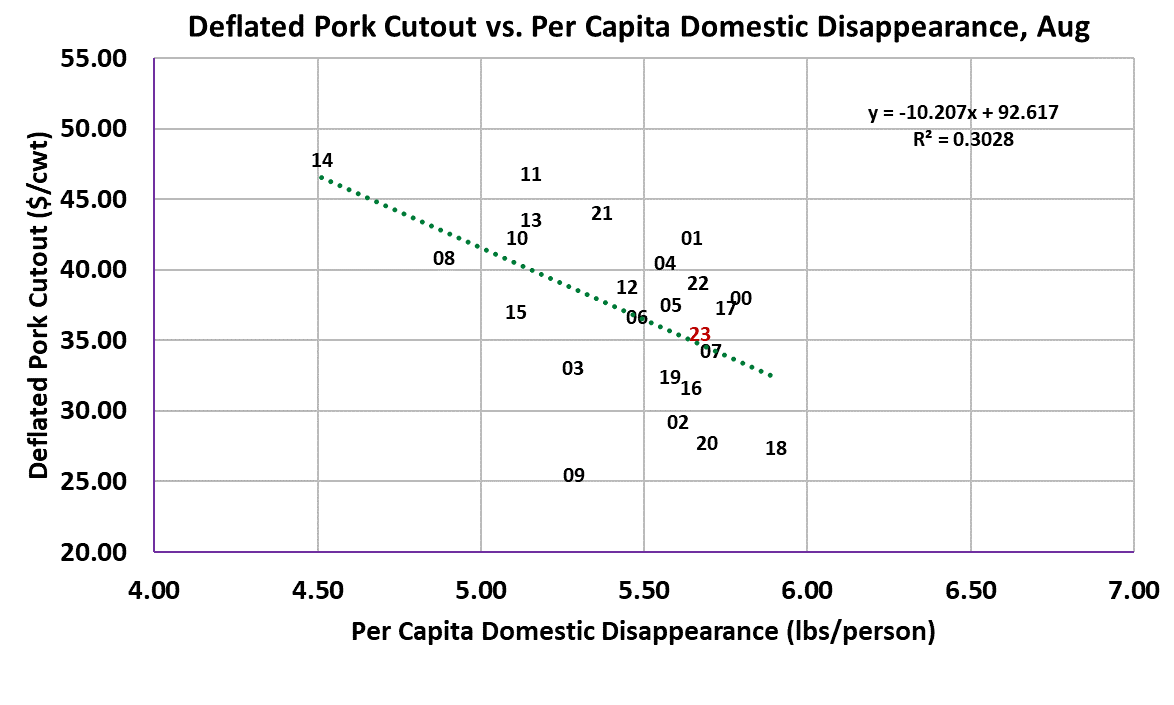

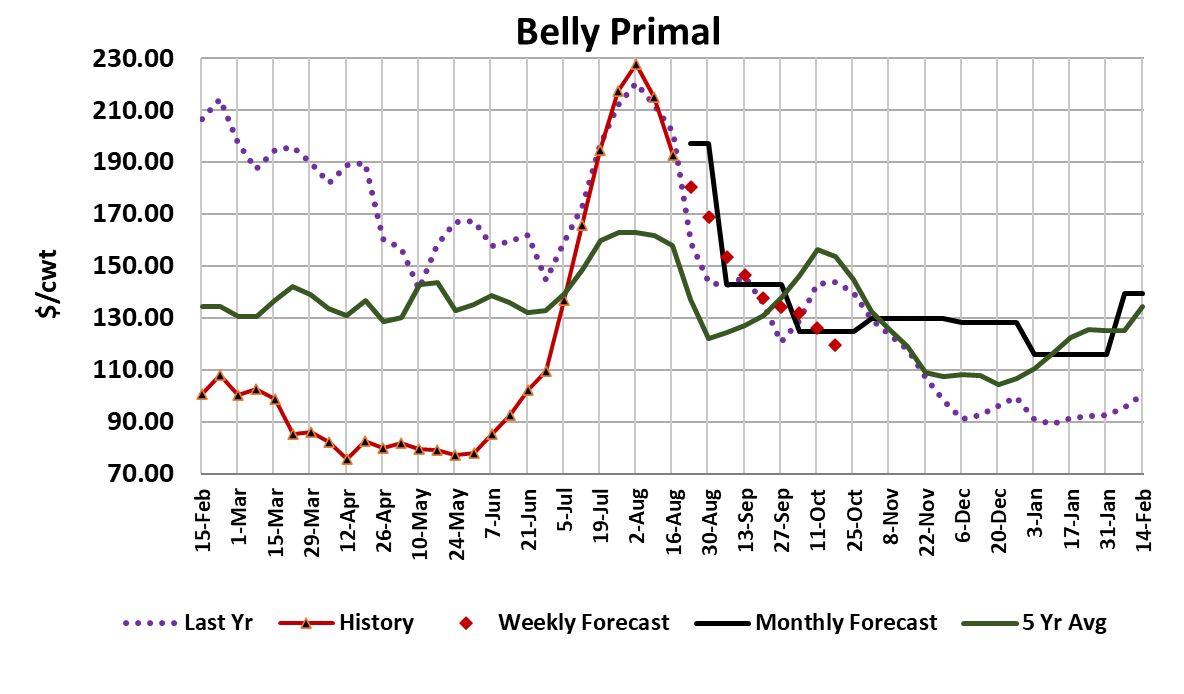

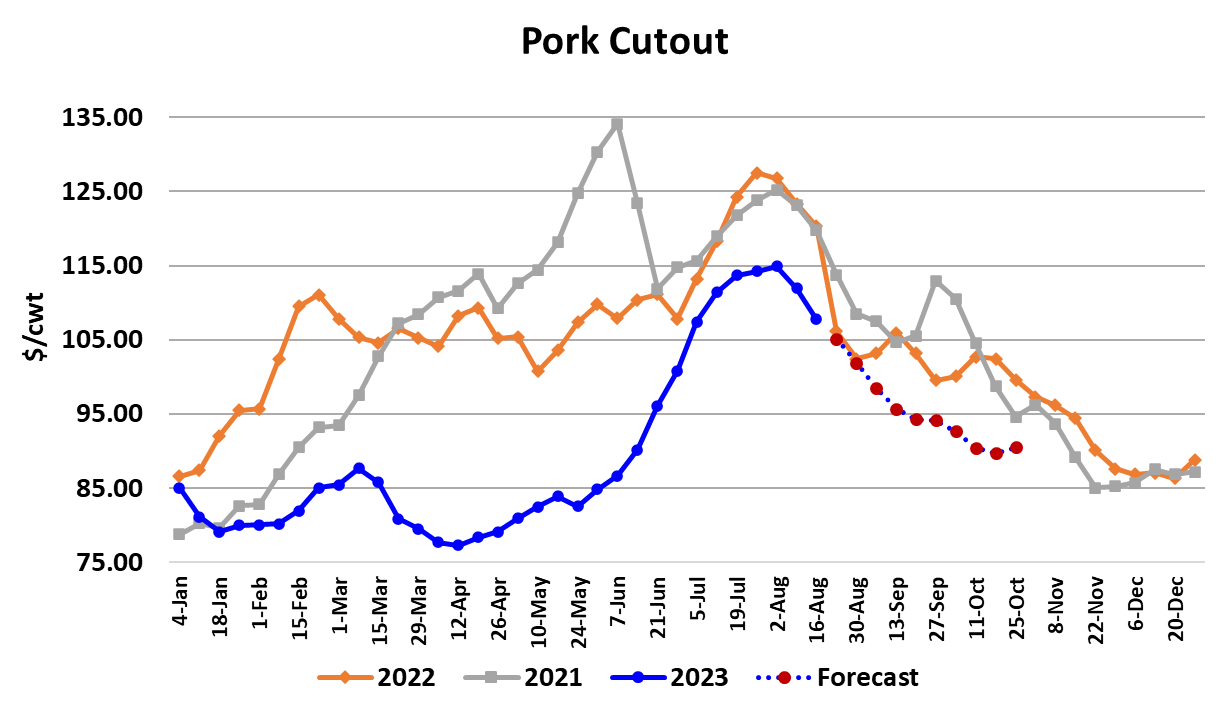

The pork cutout continued lower this week, dropping $4.13/cwt. on a weekly average basis to $107.79. Cash hog prices were also in retreat with the WCB negotiated market losing $3.47/cwt to average $94.26/cwt. Once again, it was losses by the bellies that were largely responsible for bringing the cutout down. Hams also turned lower late in the week and thus it looks like we are going to have one of those bearish situations where both hams and bellies are working lower at the same time. The price downturn feels more like it is related to a softening in demand for the processing items rather than being driven by bigger pork supplies. It is true that hog supplies are increasing seasonally and that will ultimately be the big driver of softer pricing this fall, but so far here at the end of summer the increase in pork production has been rather modest. This week’s kill clocked in at 2.42 million head—the first kill to exceed 2.4 million head this summer. I thought we might see 2.4 million head killed in the first week of August, so the fact that it didn’t show up until the third week is a bit surprising. The attached chart shows that the industry has underkilled the Dec/Feb pig crop for the past three weeks. Is that a symptom of packers managing margin or is it due to the hog supply being tighter than expected? My guess is that it is some of both because hog weights sure make it look like the hog supply is pretty tight and maybe packers sense that and so they are keeping a lid on the kill in order to preserve what has been very good margins over the past few weeks. I calculate packer margins this week were close to $9/head, down about $2 from the week before. Packers know that if they can just make it past Labor Day, their margin situation should get considerably better as more hogs become available. Since Memorial Day, packer margins have averaged a little over $10/head, with no instances of negative margins. That is very impressive for the summer and it makes me think that packers have found the magic balance between slaughter rates and hog supplies that kept them out of the red. That might not be possible next summer as it appears that producers are shedding sows and thus we should expect smaller hog supplies to pinch packer margins more than what we saw this year. I have been expecting at least one week where slaughter was close to 2.5 million head before Labor Day, but now it is looking like that level might not be reached until early September. Once September arrives, the industry will begin harvesting the March/May pig crop, which USDA found to be up 0.8% from the year before. However, if the last few weeks are any indication, USDA might have overestimated that pig crop and maybe kills will down from last year rather than up. We need to monitor that closely. Barrow and gilt weights surprised this week by dropping 2 pounds to average 204. The attached chart shows that is well below the last two years and probably marks the annual low in carcass weights for 2023. The DTDS weights also dropped to another record low this week, so from that perspective it appears that producers have kept their hogs moving at a good clip and thus it is a bit of a mystery to me why packers had such an easy time moving negotiated hog prices down $3-4/cwt. this week. Temperatures in the middle of the country are scheduled to ramp up over the next 7-10 days and that could slow weight gains and thus the flow of hogs to market in the next couple of weeks, but I wouldn’t expect that to be enough to turn hog prices substantially higher. It may slow the decline or perhaps put prices in a sideways pattern for a little while, but isn’t likely to turn them higher. There doesn’t seem to be much evidence of a Prop 12 effect in the pork market yet since I would expect that to show up as unexpected weakness in the retail primals, but the price movement there has only been a modest drift lower. Most of the price weakness recently has been centered on the bellies which looks more like buyer resistance to extraordinarily high pricing rather than something related to Prop 12. If there is going to be pressure on prices due to the new California requirements, I’d look for it to happen late in the year when pork supplies are abundant and Prop 12 enforcement efforts are ramping up. The attached scatter shows August pork demand just a little better than average when we use CPI-deflated prices. That is way better than what the scatters were showing this spring. However, my sense is that demand is in a new downcycle and September will likely see that trend continue. The fact that the combined margin is tracking lower now supports that theory. The biggest threat to the cutout right now is the bellies, which have been known to collapse around Labor Day. Demand for hams is also looking weaker and I think the combination of the two moving lower together has the potential to move the cutout back below $100 before we reach Labor Day. Futures traders are wary of a price collapse also, as the now-nearby Oct contract traded below $78 for a bit this week. It rallied back to $82 late in the week, but if belly prices start to wobble even more, they will be quick to put a seven handle back on the Oct futures. Next week, watch for further slippage in both cash hog pricing and the cutout. Keep an eye on the hams and bellies because those are the items that present the most risk to the cutout at present.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}