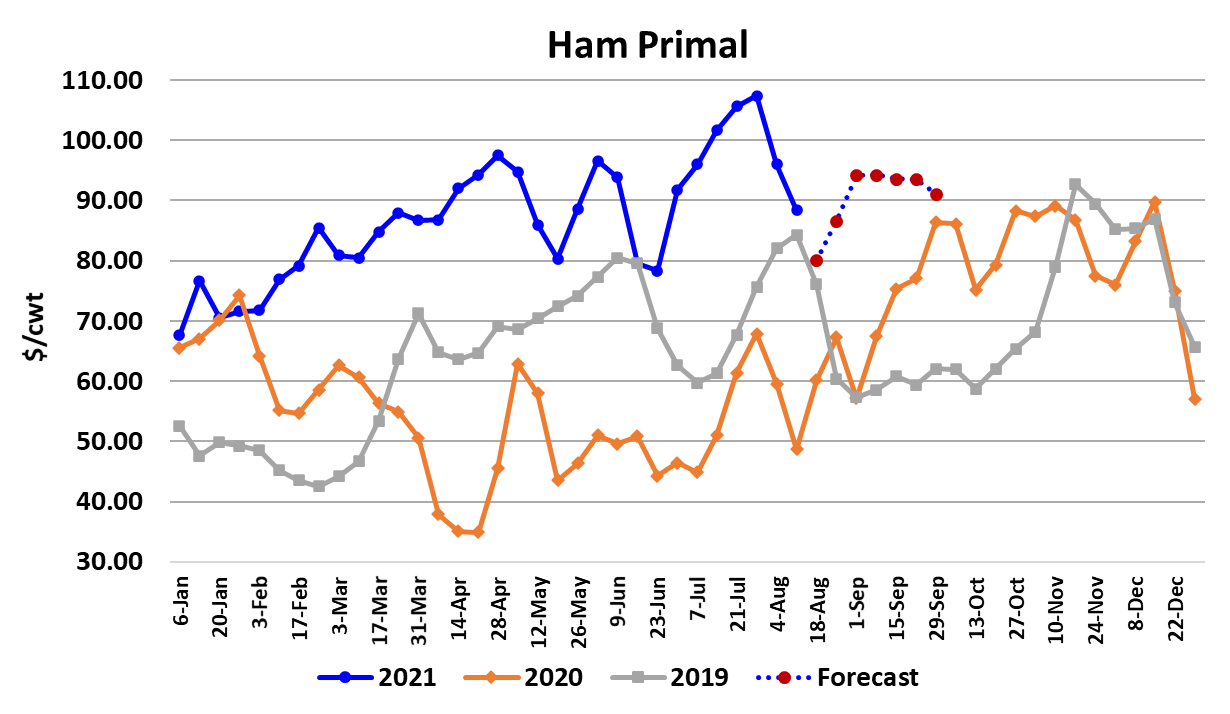

Pork Wrap August 13

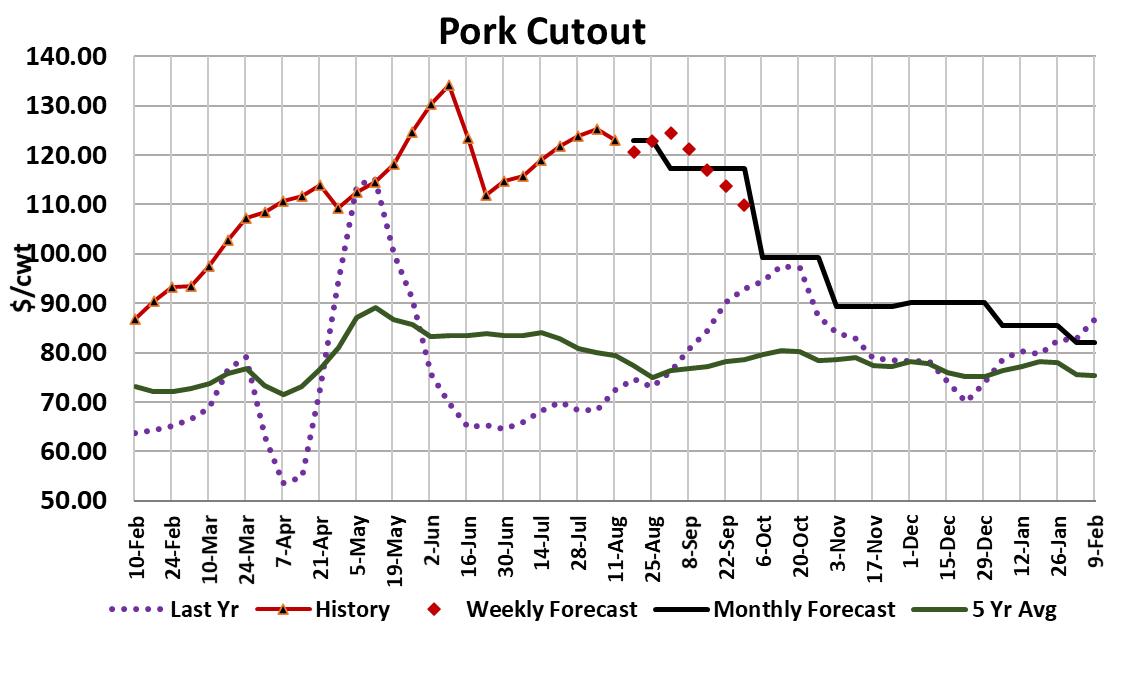

The hog and pork complex was a little softer this week, as the cutout

dropped $2.10 on a weekly average basis and both the LHI and the

NDD negotiated market were down about $1.50. The important

question is whether or not this week’s little dip in the cutout is the

beginning of a downtrend or just a one-week anomaly. I see it as a

one-week dip, mostly because nearly all of the softness seemed to

originate from the ham primal this week (chart below). That won’t last

forever since processors need to be building inventories for their

holiday ham business. At the first indication that the hams have

bottomed, I would look for a rush of buying to lift the primal quickly

higher.

None of the other primals show much sign of backing down. That said,

the bellies are right up against all-time highs, so there is some risk that

we could see a belly correction that forces the cutout lower. But as it

stands now, if the hams turn higher then the cutout is likely to move

higher. The negotiated hog market in the WCB showed some lateweek strength, so perhaps packers are comfortable enough with their

margins now that they don’t feel like they need to exert additional

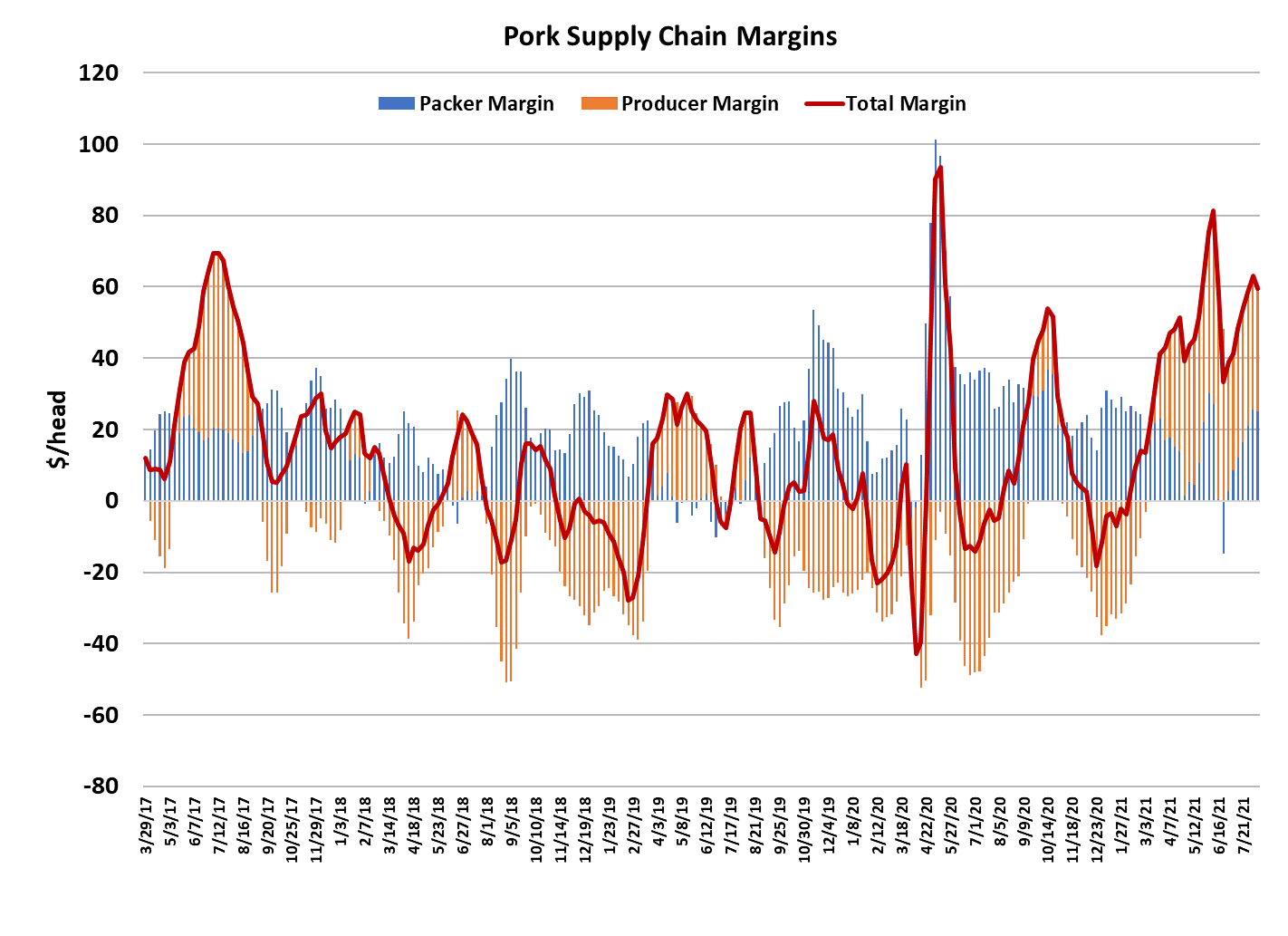

pressure on the hog market. I calculate packer margins this week at

$23/head, down slightly from last week. The combined margin chart

below shows a top being formed, but I suspect that is a head-fake and

we could see it move higher again in the next couple of weeks. It is

hard for me to imagine the pork cuts sold at retail will see significant

demand erosion while beef prices are soaring by leaps and bounds.

The supply side situation in pork is way different than what is going on

in beef, however. Kills are starting to expand seasonally.

This week’s kill was estimated at 2.42 million head and I think it is

reasonable to expect the kill to eclipse 2.5 million head by the end of

August. Even though we are seeing the normal seasonal growth in

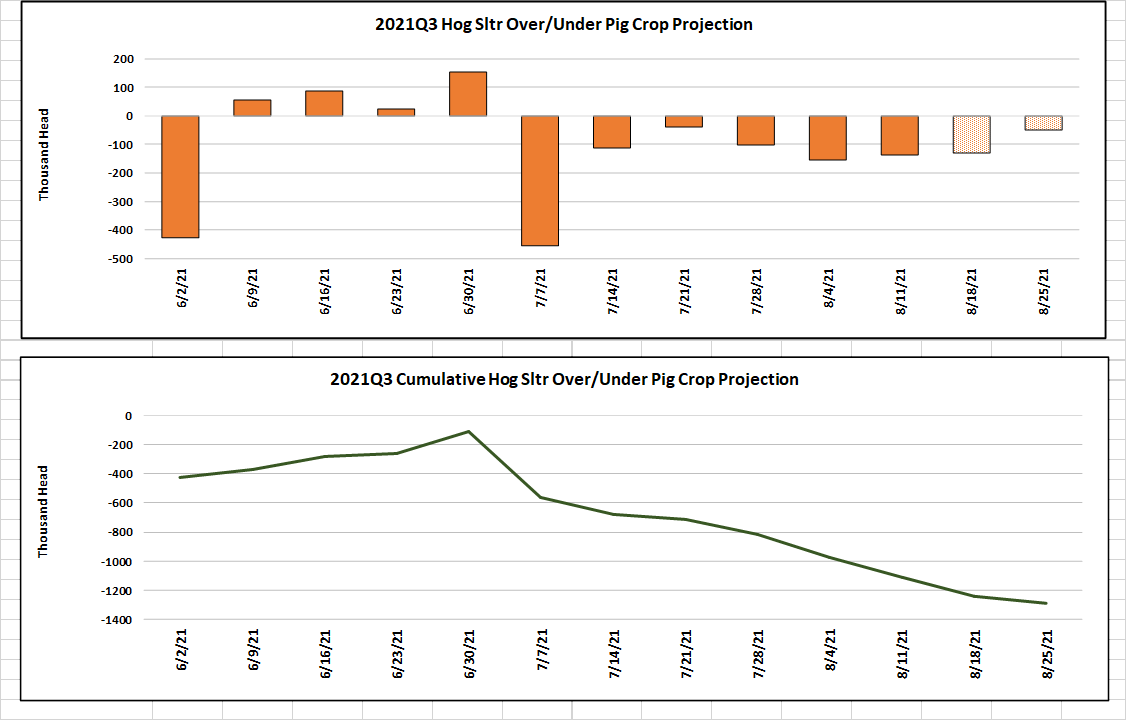

slaughter levels, the kills have not matched up very well with the Dec/

Feb pig crop reported by USDA. The charts below indicate that kills for

all of July and August have been well below what the pig crop implied.

For the quarter as a whole, it now looks like the gap between the pig

crop and this summer’s slaughter will approach 1.3 million head.

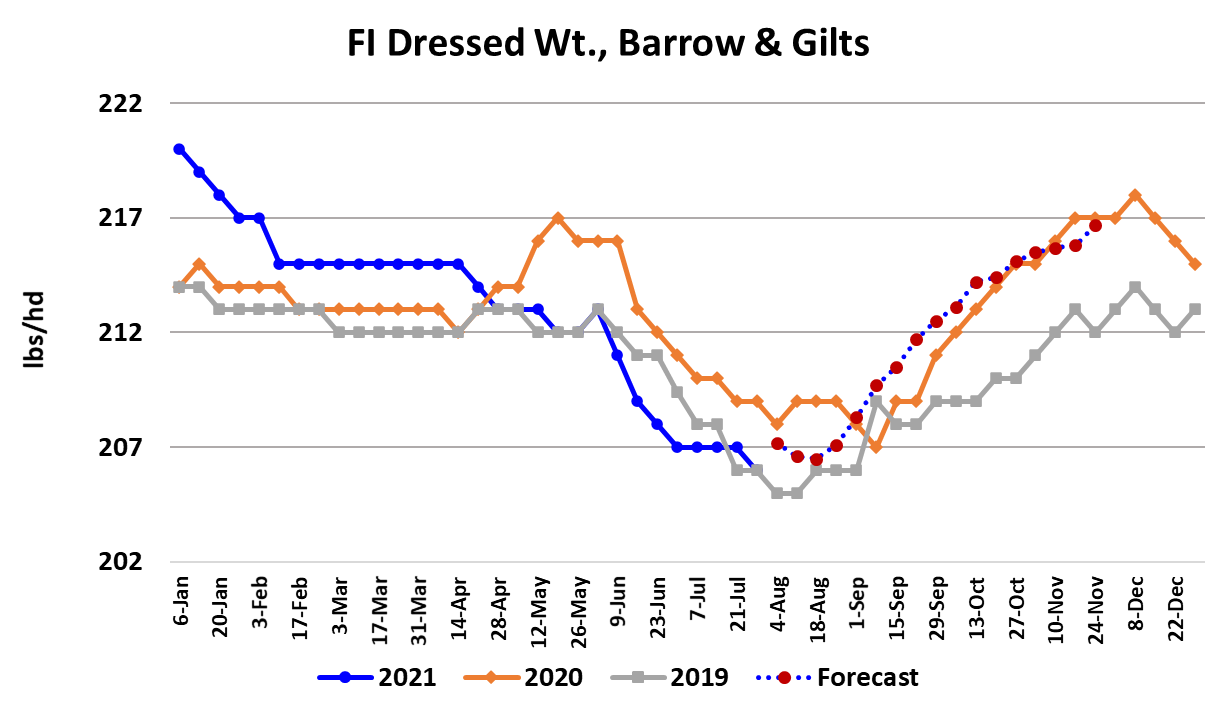

Clearly, USDA will need to make some revisions. Carcass weights are

behaving as expected, now approaching their annual low and set to

start rising around Labor Day. Once September arrives, the industry

will start slaughtering pigs that were born in the March/May quarter and

that pig crop was down 3.1% from the year prior. The risk is that USDA

also over-estimated that pig crop and that kills this fall will not be as

strong as advertised. We will learn a lot about the labor situation in

pork plants over the next couple of months as hog supplies start to

grow.

If, similar to what is happening in beef plants, packers cannot find

sufficient labor to process all of the hogs coming to market this fall,

then we can expect an outcome similar to what we are seeing with

beef right now, namely extraordinary packer margins, higher-thanexpected pork prices and lower-than-expected hog prices. That is

a wild card for sure, but there are also two other wild cards out

there lurking in the shadows for fall. The first is the discovery of

ASF in the Dominican Republic and the potential for that dreaded

disease jumping to the US or a Central American nation.

If that happens it would be very negative to both hog and pork

prices in the US since all exports would be shut down immediately

and there would also be some negative consumer reaction to

reports of “diseased pigs.” If it were to hit Mexico, then Mexico’s

exports would immediately cease and they would be awash in pork

and not need to import much, if any from the US. The second wild

card is US exports to China. The US has grown increasingly

dependent upon China as an outlet for its pork over the past couple

of years and now it looks as though China is backing away from the

US market. The weekly export data out of USDA shows movement

to China in a solid downtrend. If that continues unabated, then the

amount of pork that has to be consumed in the domestic market

might actually rise even though the pig crop is down over 3%. Both

of those wild cards would be negative to US pricing if they occur.

On the positive side, we have super strong beef pricing that will

likely support pork heading into fall and consumer demand still

registering very strong as the US is engulfed in another wave of

COVID.

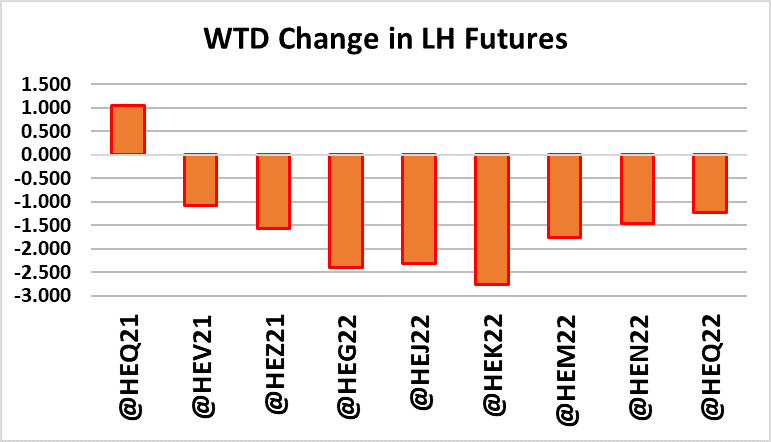

The wild cards mentioned above have made futures traders

nervous and this week we saw further declines in the lean hog

futures, with the exception of the expiring Aug contract. It is

important to remember that pork has a very high elasticity of

demand, so small changes in the available supply (up or down) can

bring about big price changes. Next week, watch the ham primal

for signs that it has finally cheapened up enough to attract fresh

buying interest. Also keep an eye on those negotiated markets as

an indicator of whether or not packer margins have made a shortterm top.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}