Pork Wrap August 12

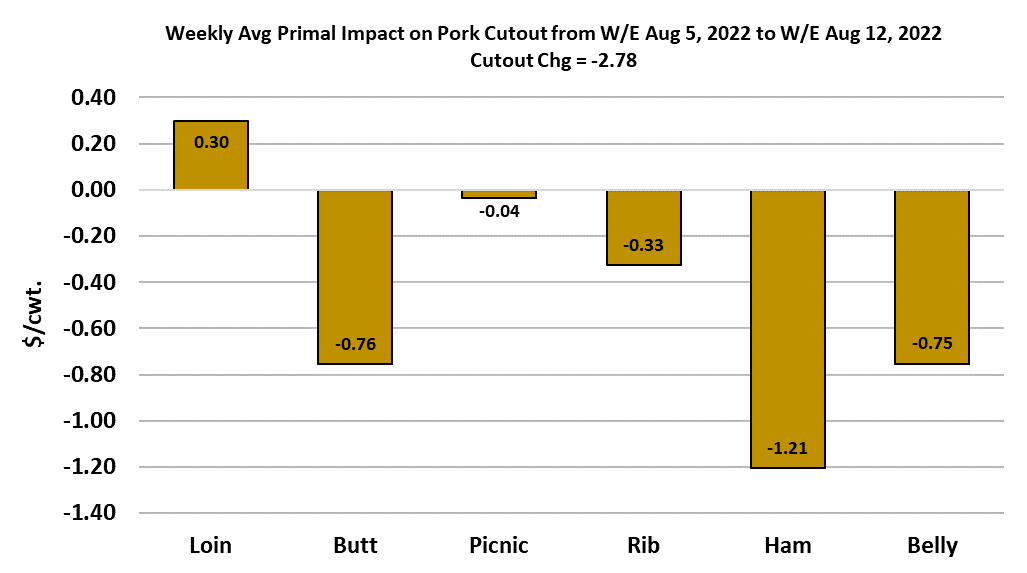

The pork cutout took another step lower this week, dropping $3.46/

cwt to average $123.34. Unfortunately for packers, the cost of

hogs going into their plants increased this week. The LHI was up

only $0.40/cwt, but the WCB negotiated market gained $3.61/cwt.

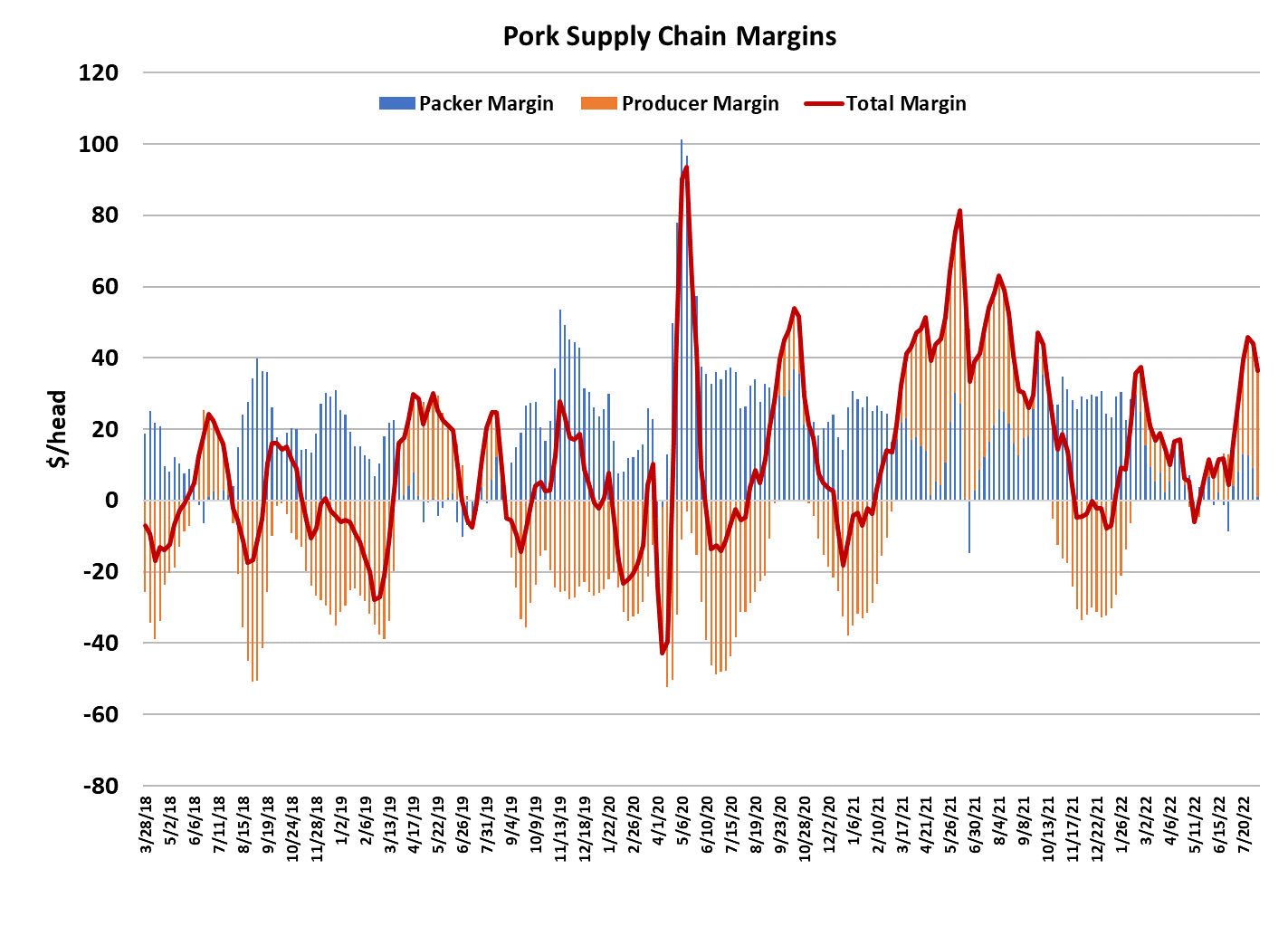

The falling cutout combined with rising hog prices caused packer

margins to crash from about $9/head last week to a little less than

$1/head this week. What’s more, I’m expecting margins to go

negative by several dollars next week as the cutout continues to

ease, yet cash hogs remain stubbornly firm. The turn lower in the

cutout has been led by the hams. The bellwether 23/27 lb bone-in

ham has moved from $121/cwt at the end of July to $105/cwt in

today’s print. We are also seeing bigger volumes of hams traded

in the spot market, and that is likely a sign that the stout pricing in

late July was caused by bigger-than-normal commitment to deliver

hams that took them out of the spot market.

Whether that was an export or domestic commitment is unclear,

but with volumes now rising, it appears that source of demand has

faded. Fortunately for packers, the bellies have held up well while

the hams have been on the defensive over the past couple of

weeks or else the cutout would have been down a lot more. The

bellies did slip some this week and I suspect that they are living on

borrowed time, with further, and probably bigger, price declines

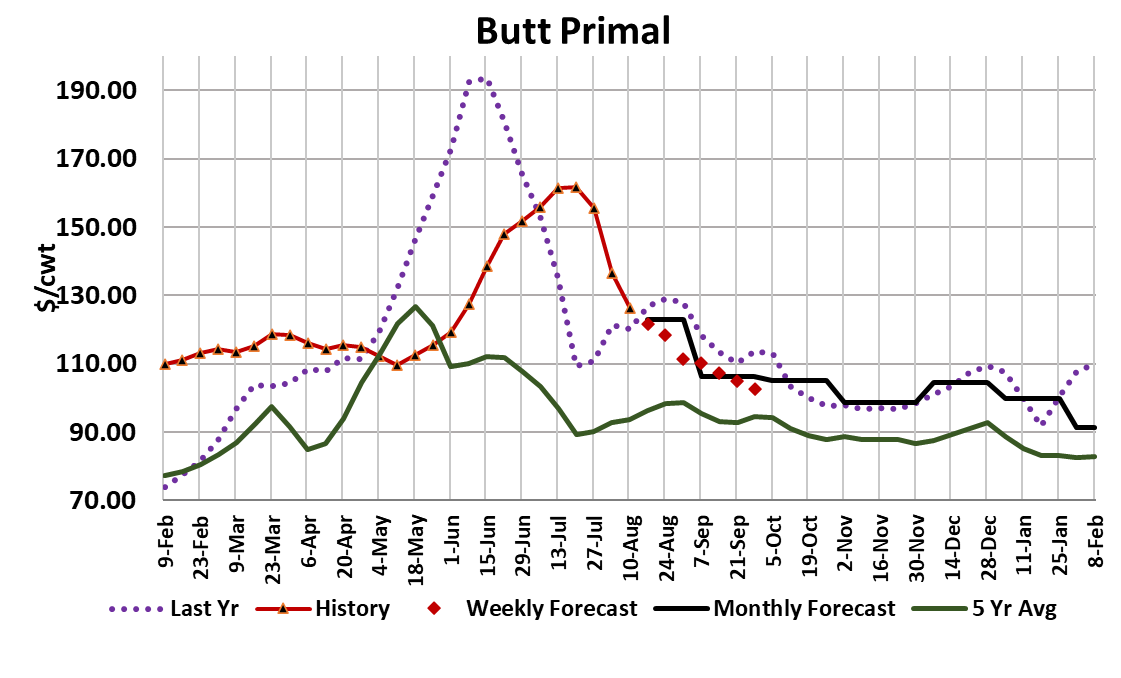

just over the horizon. As far as the retail primals go, the butts have

had a tremendous reset over the past few weeks with the primal

price dropping from $160/cwt down to $126/cwt this week. We

always expect some price increases over the summer when

supplies get tight, but the move that the butts put in this summer

was very impressive. The butt primal is now back to last year’s

level and should continue to ease lower in the weeks ahead as

kills expand. Loins have held together very well and will likely be a

post-Labor Day favorite for retail features.

Ribs have been in steady decline for weeks, but could stabilize in

late August as retailers square up their needs for Labor Day

promotions. So, as I look across the cutout over the next several

weeks, I see it being dragged lower primarily by a reset in the

bellies and some further erosion in the hams. The retail items

should contribute to the decline in a much smaller way. The

combined margin has made a solid turn lower now, signaling a

new downcycle in demand. The recent upcycle was stronger than

expected, mostly because hams got so strong in the spot market.

As demand fades lower, packers will need to find some way to

pressure the negotiated market lower or else they face the

prospect of an ugly September. Margins for hog producers have

been stellar lately, holding in the $30-35/head range for the past

month or so.

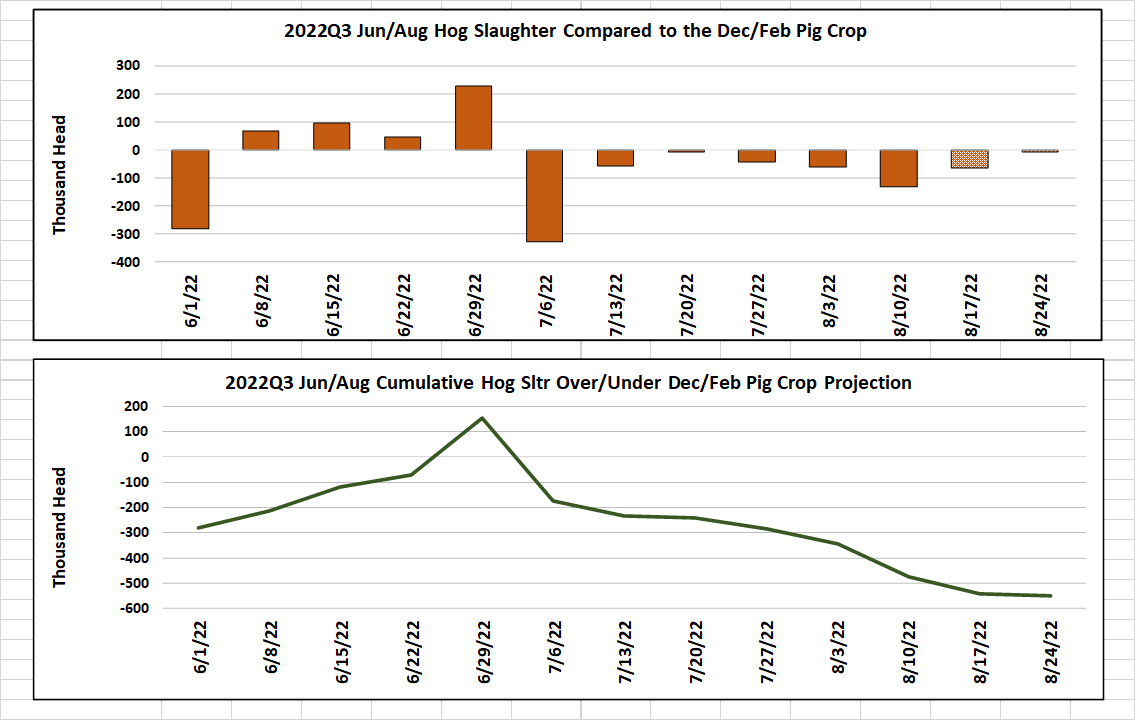

It may be Oct 1 or later before hog producers have to worry about

margins going negative. This week’s kill came in at 2.34 million head,

which was only a tiny fraction larger than last week’s total. The normal

seasonal pattern tells us that kills should be expanding more rapidly than

that, but it seems as though the hog supply isn’t large enough to allow

that to happen just yet. Once again, this week’s kill was smaller than

what the Dec/Feb pig crop implied and my forecast has it falling short

again next week. As we approach the end of the Jun/Aug quarter, it is

looking like cumulative slaughter will be about 500-600k below the pig

crop estimate. USDA will need to get their revision pencils sharpened for

the next Hogs & Pigs report. I have the peak kill this fall at 2.61 million

head in the second week of November. The risk to that forecast is that it

might be too high because it is entirely possible that USDA overestimated the Mar/May pig crop also.

The seasonal increase in supply should keep downward pressure on the

prices for almost all parts of the carcass between now and November,

but don’t take that as a given. We have seen times in the past when a

strong demand upcycle in October or November produces impressive

price gains even though pork production is steadily increasing. Barrow

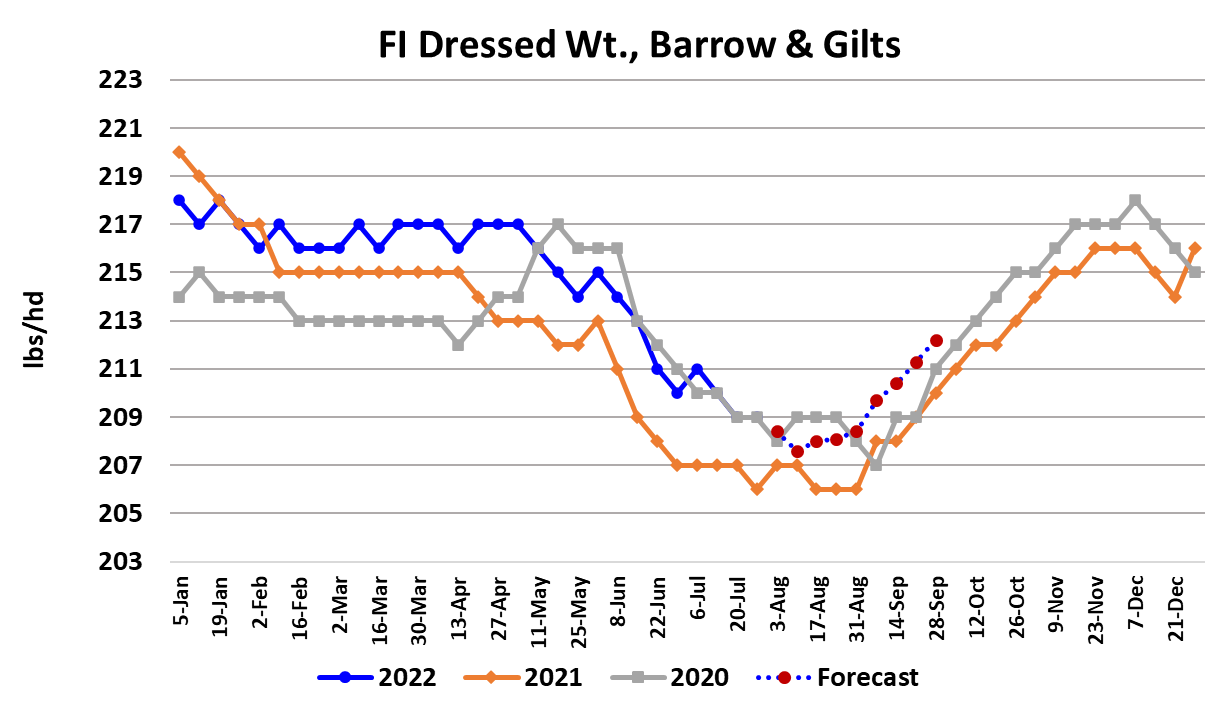

and gilt carcass weights held steady this week, which was a bit of a

surprise given how high temperatures have been in the Midwest, but I

don’t think that weights have found a bottom just yet. That may come in

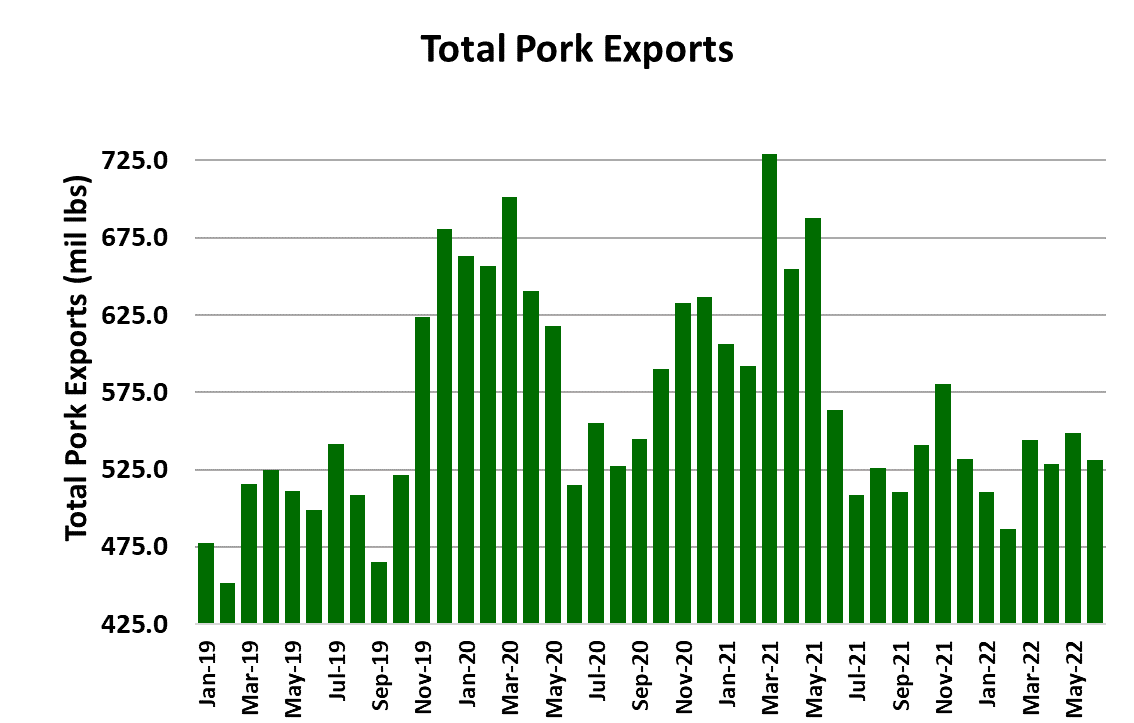

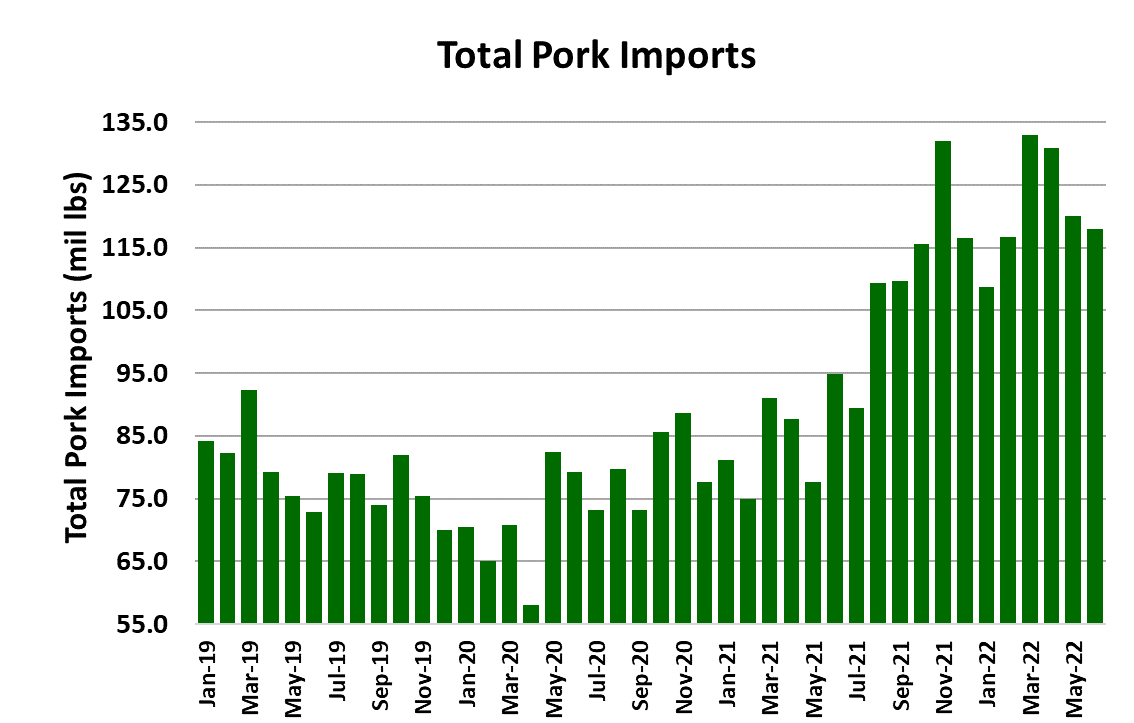

a couple of weeks. USDA released the trade data for June this week

and it showed pork exports down about 6% YOY. That wasn’t a surprise

to anyone since we have known for months that exports are much softer

than in 2021. The weekly data issued since June doesn’t suggest that

there has been any big improvement in the interim. Pork imports

continue to run strong, with the data for June showing a 24% YOY

increase.

By the time we get the import data for August, the big YOY increases

should have dissipated, but only because we will be lapping the point in

last year’s calendar where imports started to surge. The Aug LH futures

expired today just a touch under $122 and that probably marks the top in

the LHI for this year. Traders will now focus on October which is trading

near $100. That is a long way for the index to travel in just two months,

but it has done it before. If LHI is going to reach $100 by October, there

will need to be some sharp price corrections in the processing items, as

well as negotiated spot hog prices, to help it reach that goal.

Deteriorating macro conditions this fall are also a key piece of the puzzle

that would take the LHI and cutout back into double digits. Next week,

watch for the bellies to give up more ground, perhaps in big chunks.

Packer margins should go negative, so watch the daily kills for signs that

packers might be tempering slaughter levels in an effort to preserve what

little profitability they have.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}