Pork Wrap August 11

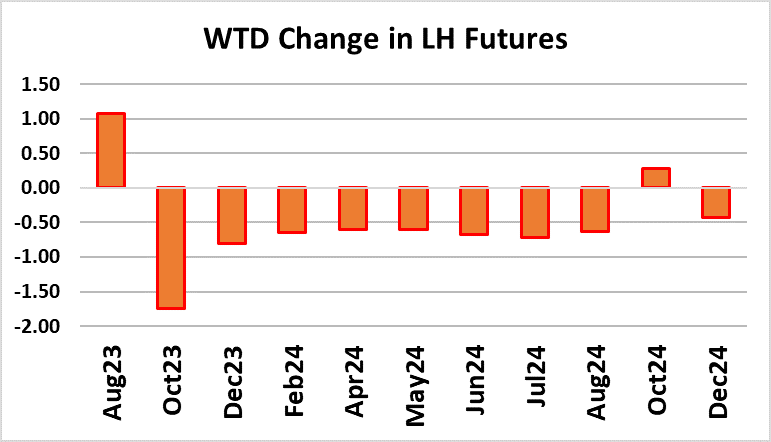

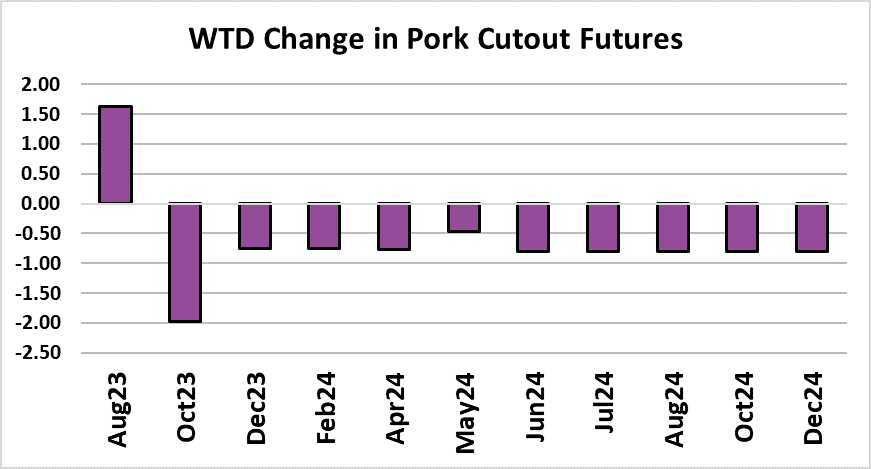

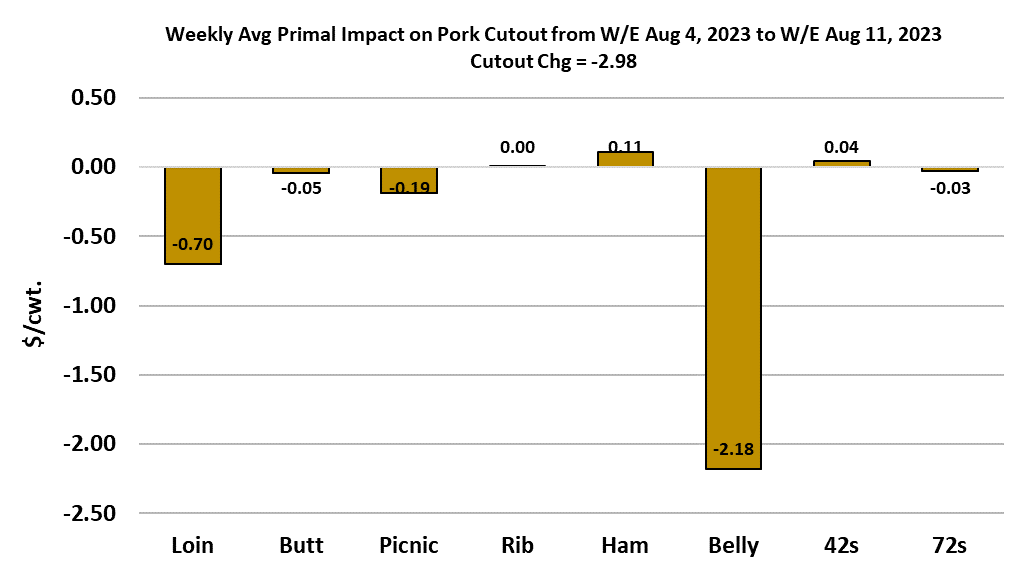

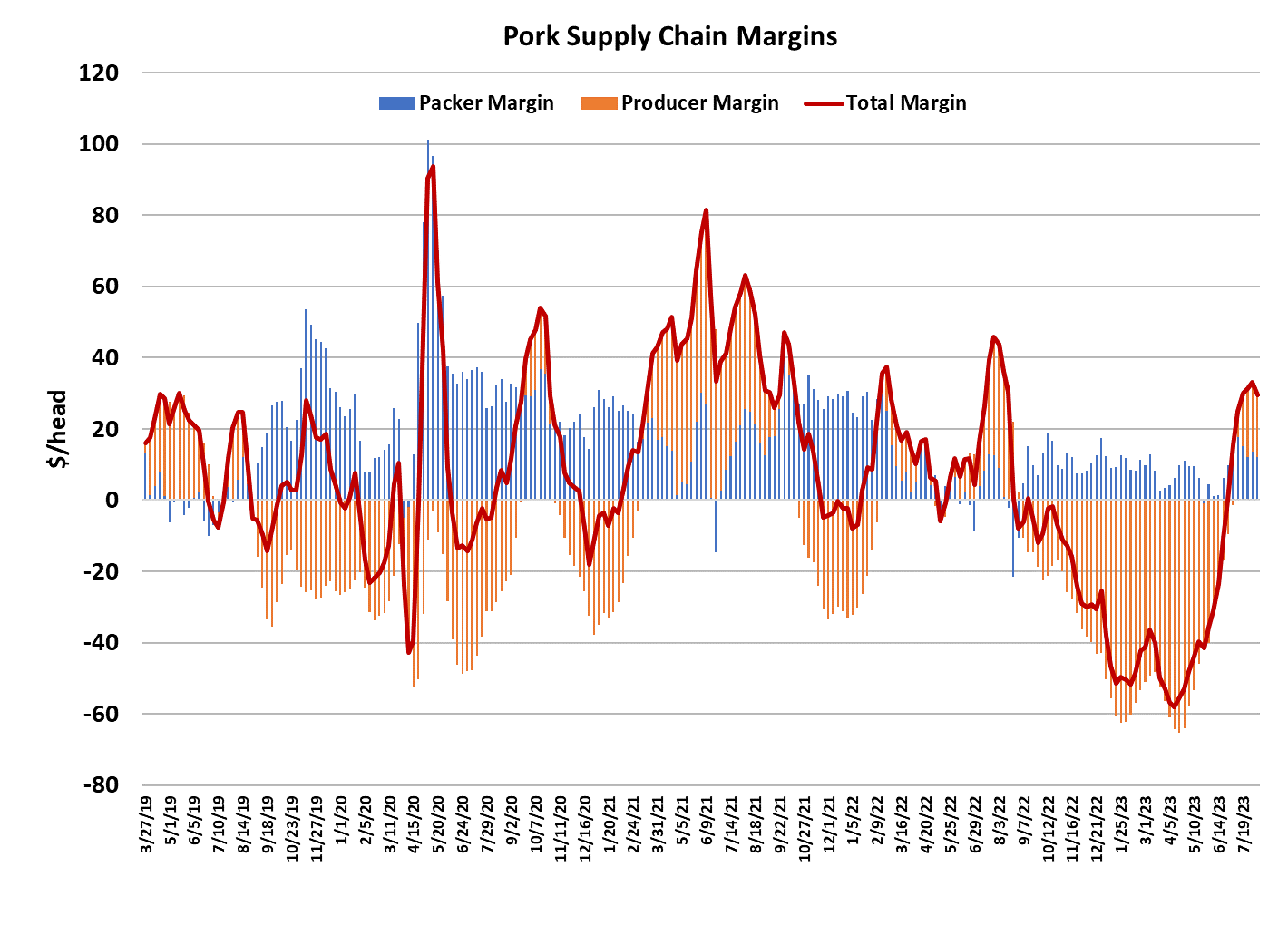

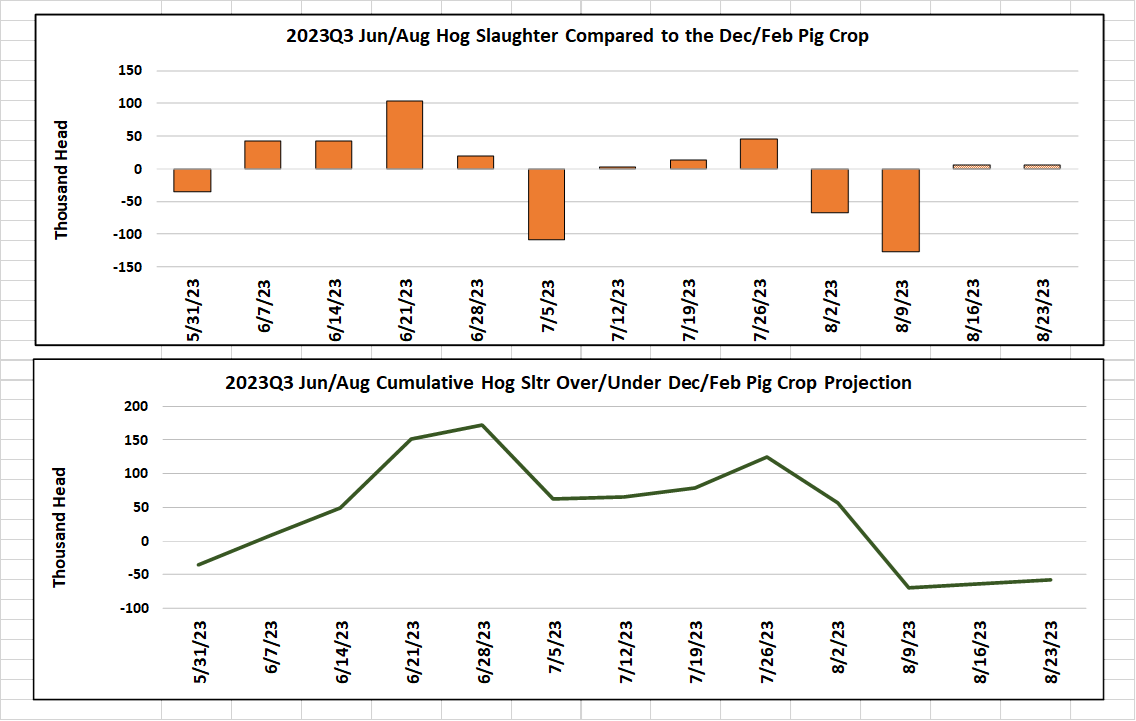

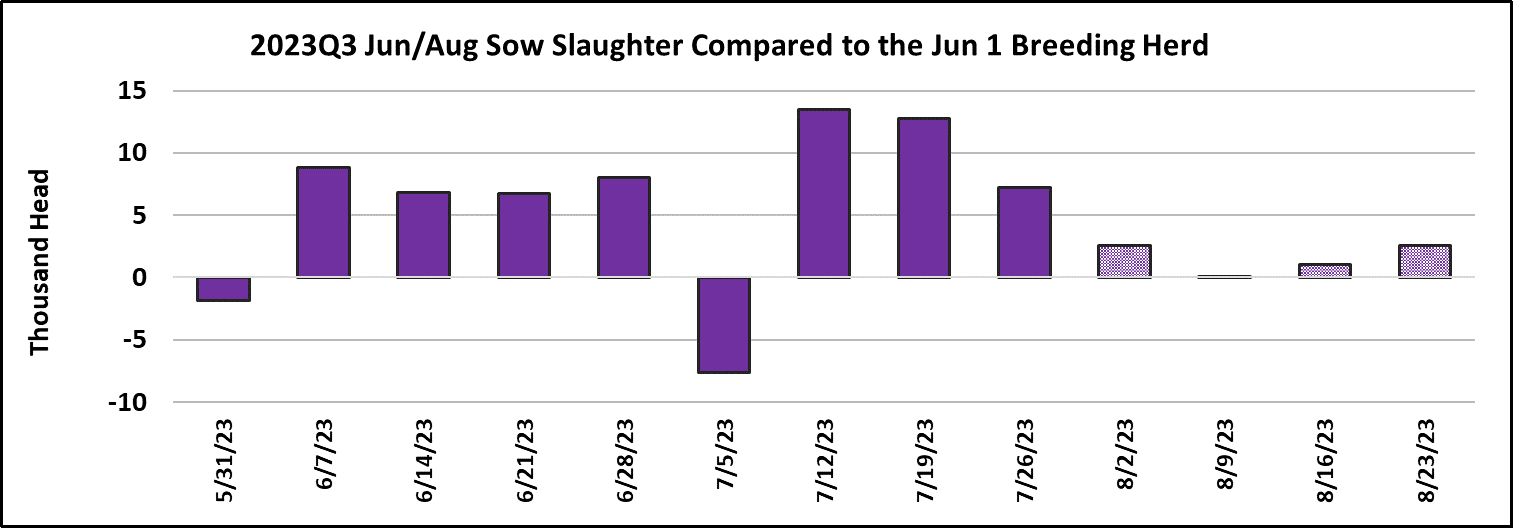

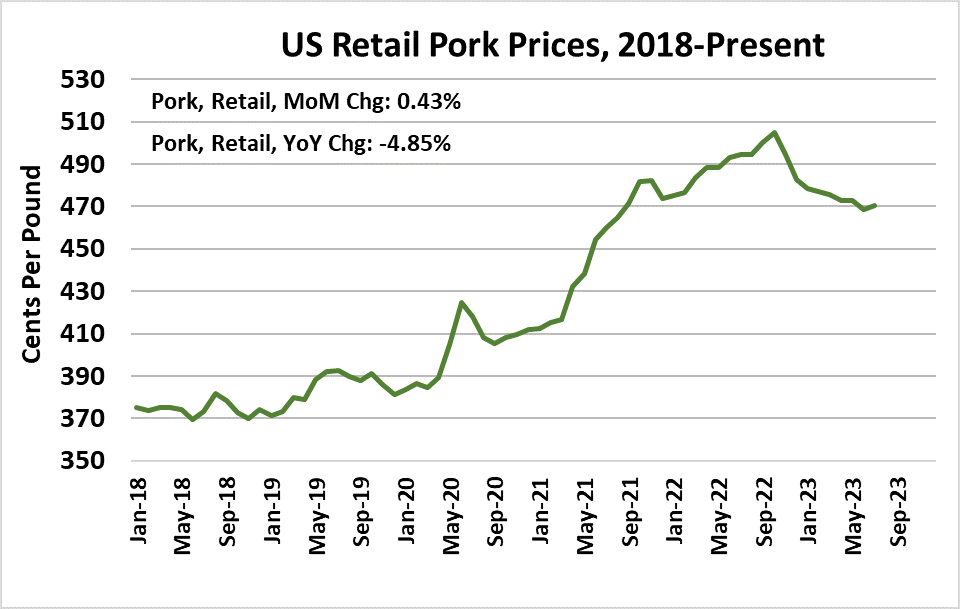

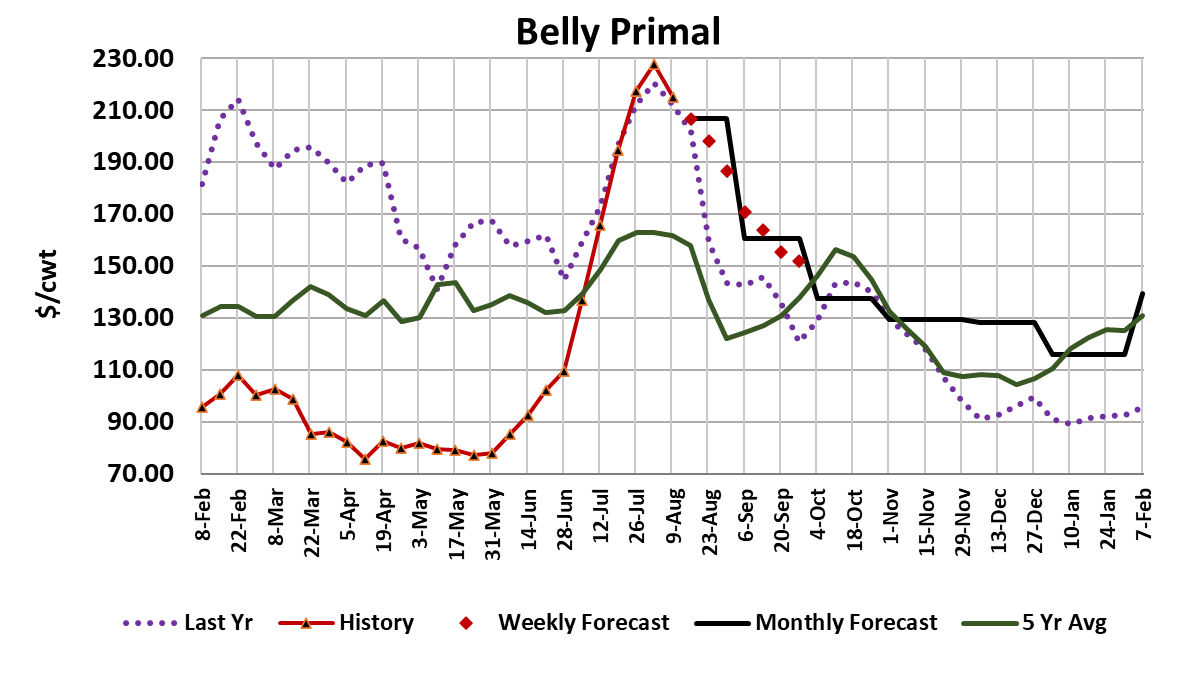

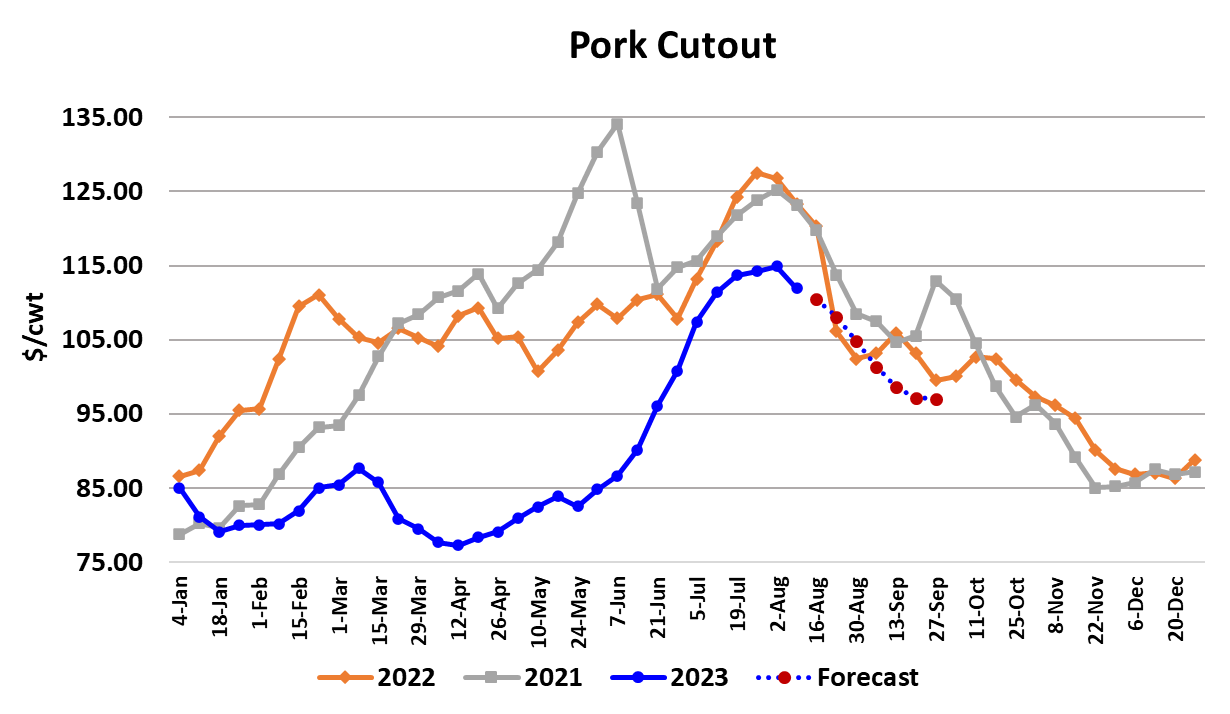

Prices in the hog and pork complex took a step lower this week and in doing so, they have cemented the top in the summer market and begun the long slide lower into winter. After being mostly straight up since April, the cutout dropped $2.98/cwt. to average $111.92. Right on cue, the negotiated cash markets also tracked lower, with the WCB dropping $4.73/cwt. and the NDD down $3.93/cwt. The Lean Hog Index, which is a little slower to reflect the full effect of changes in the cash market, dropped $1.64/cwt. to average $103.97. The Aug futures will expire on Monday at close to $102 based on the data currently in hand. Attention will now turn to the October contract, which is trading more than $20 discount to the Aug. While the index could certainly lose that much over a 2-month period, the discount seems excessively wide given my read on the fundamentals. Of course, everyone expects the index to trend lower heading from summer into fall, so it just becomes a question of how quickly prices retreat. I have been a little surprised at how rapidly cash hog markets have moved lower given that weights seem light and thus the barns should be pretty current. However, the hog market is not like the cattle market where every week is an intense fight between producers and packers. With hogs, it seems that packers are almost always in control and the cash hog market moves in conjunction with the cutout, helping to protect packer margins. This week, those margins were close to $11/head, which is down a little from the prior week, but still pretty strong for the middle of August. My expectation is that packer margins will expand over the next couple of weeks and will probably stay positive until sometime next spring when hog numbers start to tighten seasonally. The turn lower in the cutout this week was largely driven by softening belly prices. Hams were a little bit stronger, but that couldn’t outweigh a $13 drop in the belly primal. The combined margin chart shows that the top in this very long demand cycle has now been made and some softening in overall demand should occur over the next month or two. Certainly, bellies have a lot of air under them and that is likely where the biggest price declines will occur. Among the retail items, butts seem to have finally bottomed after a big drop from summer peaks but loins likely have further downside risk once Labor Day buying is complete. This points to a cutout that works lower in the next few weeks, but I expect the decline to be measured and orderly, much like the trip upward this summer. This week’s kill registered 2.35 million head, which was smaller than what the pig crop indicated, likely as a result of some plants undergoing maintenance this week. However, that makes two weeks in a row where the kill has come up short and, with only two weeks left in this quarter, there is a reasonable chance that the kill will conform very closely to what the Dec/Feb pig crop indicated. Speaking of kills, one thing that stands out is larger than expected sow slaughter. The attached chart gives the difference between observed sow slaughter and what would be expected given the sow inventory at the beginning of the quarter and normal turnover rates. It is pretty clear from these data that some sow liquidation is occurring above and beyond the normal turnover rate. So far, the futures market seems oblivious to this, preferring instead to focus on the turn lower in spot prices. That has resulted in nearly all of the futures curve being underpriced relative to my fundamental forecast. The mispricing is largest in the summer 2024 issues which are currently trading in the $93-94 range despite an abundant spate of triple-digit pricing this summer. If we exceeded $100 easily this summer and herd liquidation is currently underway, shouldn’t next summer’s price indications be at least equal to this year’s or higher? Yes, the hog and pork complex went through a very rough patch back in winter and early spring, but that is now behind us, and pork is likely to keep a strong price advantage relative to beef for the foreseeable future. With a smaller hog herd on the horizon, it seems that the industry will be in great position to post stronger prices next year relative to what we have seen in 2023. Retail pork prices advanced a tiny amount in July according to the data that USDA released this week. The increase shouldn’t be too surprising given that wholesale pork prices were generally moving higher through June and July, but the size of the increase was miniscule compared to the monthly change in retail beef prices, which were up 2-3%. Retail pork prices are currently 4.9% lower than last year while retail beef prices are 9% stronger than last year. Clearly, pork should have the upper hand when it comes to the retail battle for the consumer’s dollar. USDA also provided us with the trade data for June this week and that indicated a 10% YOY increase in pork exports. That makes the seventh month in a row where exports have bested last year and thus I have to conclude that export demand is relatively healthy at present. Now that the price trend in the complex has peaked and turned lower, the focus will be on increasing production and lower pricing. That is a normal seasonal occurrence, but it looks to me like futures traders are too fearful at present. It does look like the start of a new demand downcycle will coincide with increasing production this fall, so that might be the reason for the sharp discounts on the fall futures. Next week, watch for further easing in the cutout, led by the bellies, and further softening in the cash hog markets.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}