Pork Wrap April 8

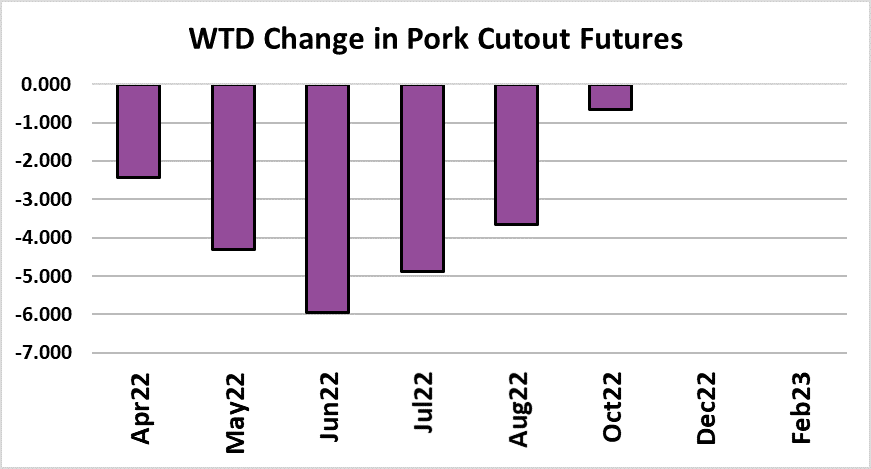

The pork complex continued to ease lower this week, with the

cutout dropping $1.16 on a weekly average basis. It is really a

very gentle easing, with the cutout down only $2.40 in the last two

weeks. For the past five weeks, the cutout has been stuck in the

$104-106 range on a weekly average basis. Packers were

relieved to see their margins increase this week as cash hog

prices declined more than the cutout. The WCB cash market was

down $4.32 and the NDD market was off $3.60. It appears that the

disease/supply issues that were plaguing the WCB earlier this year

have now started to fade. The spread between the WCB

negotiated cash price and the National average has narrowed a lot

in recent weeks (chart attached). Packer margins this week

increased about $2.50/head to average $4.75 and the forecast has

them gaining another $2 or so next week. Once again, it was the

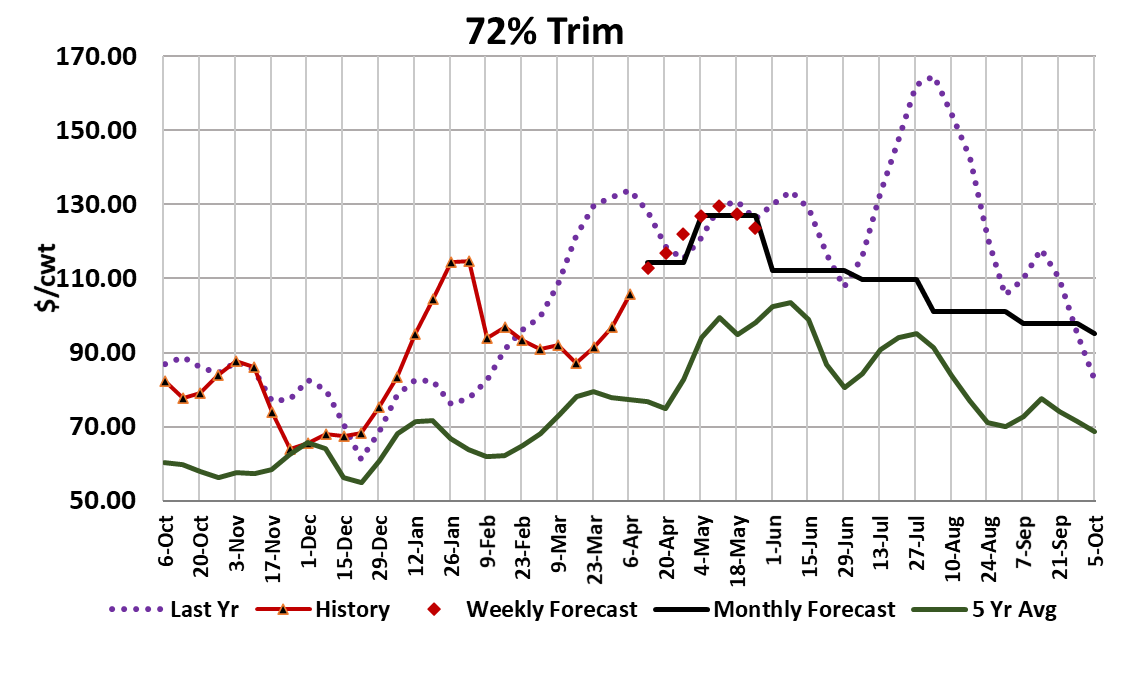

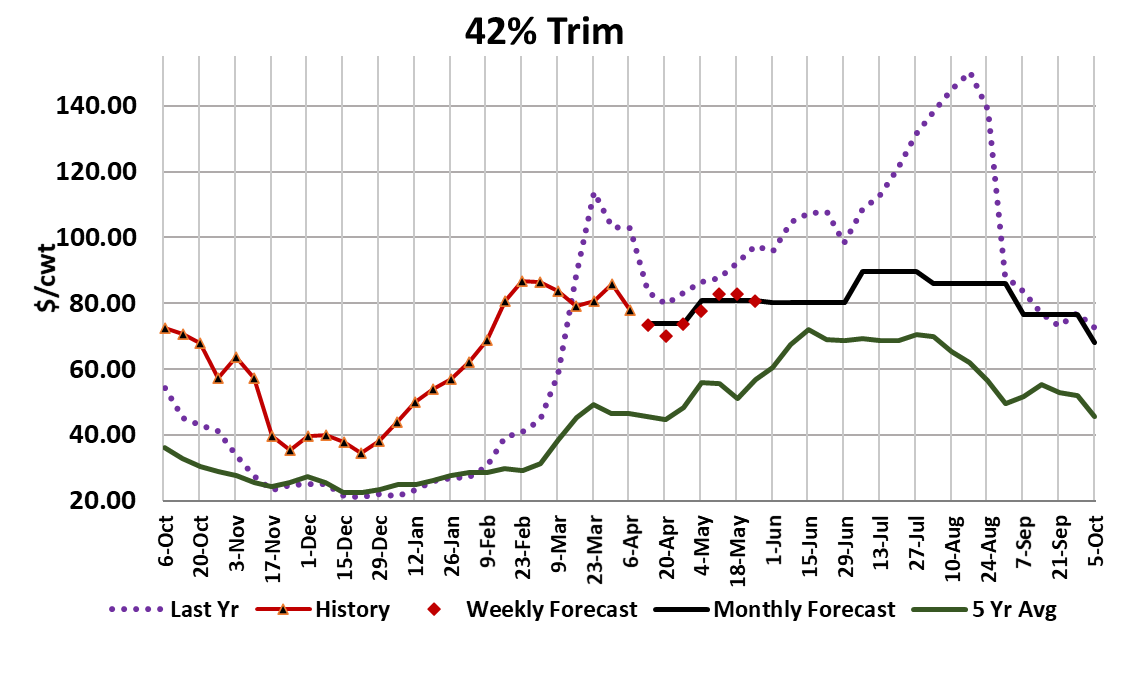

bellies that were the biggest drag on the cutout, while the other

primals held together pretty well. The belly primal dropped over $7

this week and remains on the downward trajectory that began after

the top was made in late February.

The hams, which had been lower last week, managed a small

increase this week, but don’t appear to be poised for a lot of

additional strength in the near-term. As I look out across the next

couple of weeks, this is what I’ve got forecast: loins a little higher,

butts a little lower, pics a little higher, ribs definitely higher, hams a

little softer and bellies also softer. None of these forecasted price

moves are particularly large and in aggregate they might only take

$2-3 off of the cutout over the next couple of weeks. So, I’m really

expecting the current quiet market to continue beyond Easter.

After we get a week or two beyond Easter, then I look for smaller

production and perhaps a little stronger demand to start to work

price levels higher again.

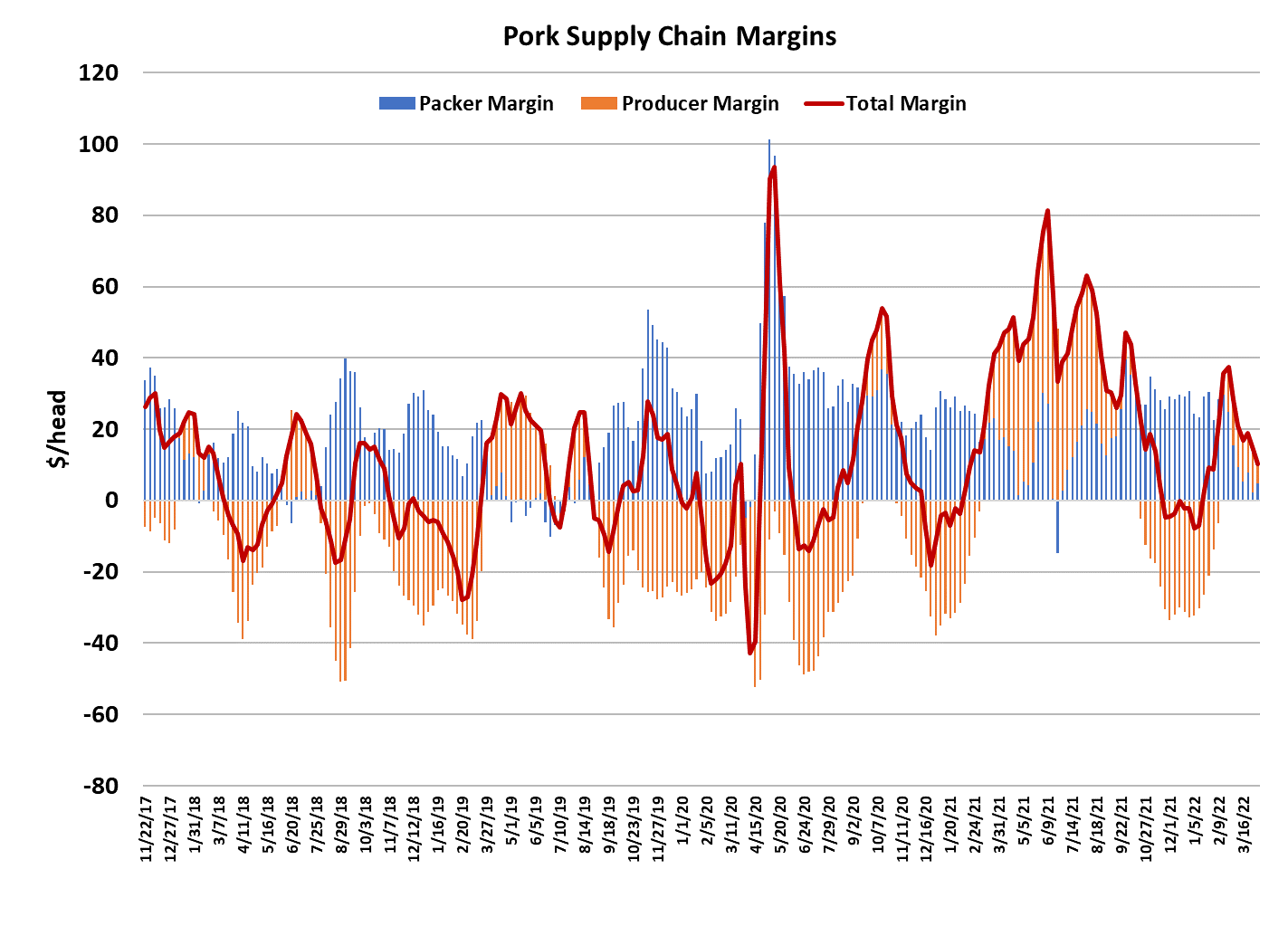

We may not even get the cutout below $100 on a weekly average

basis before the price increases take hold. The combined margin

chart tells us that we are still in a demand downcycle after the little

head-fake that was generated a couple of weeks ago. I look for

the combined margin to turn north just about the time it reaches

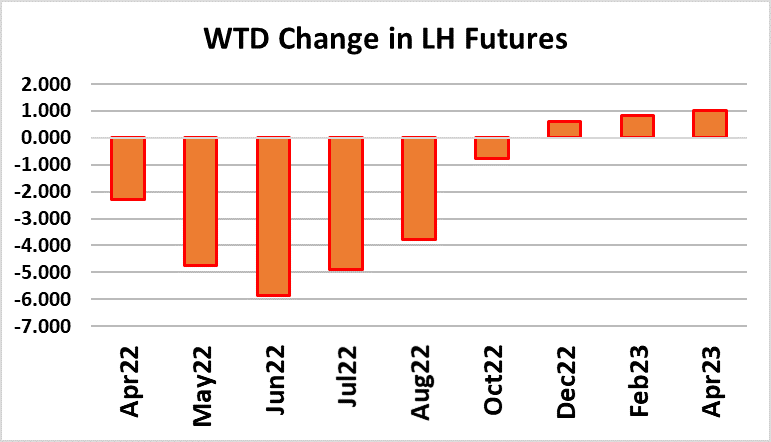

the zero line. Futures traders did a major re-think this week on the

summer contracts, with Jun dropping almost $6 and Jul moving

down close to $5. I think that traders are beginning to sense that

the disease story has just about run its course now and thus we

won’t see super-tight hog supplies this summer. Oh well, it was a

good ride while it lasted. A lot of the mis-pricing has been

removed from the summer contracts, but I still think they are

overly-optimistic about how strong price levels might get this

summer.

A good part of that view is based on expectations for a much

softer export market this summer compared to last. This week,

USDA reported that February pork exports were down 18% YOY.

My guess is that the March and April comparisons will be down

even more. February imports were up a whopping 56% YOY.

Both trends are likely to persist into the summer and thus while

domestic pork production is scheduled to be smaller than last

year, total availability in the US market could actually be close to

even with last year in the Jun-Aug period. Now, if we assume

that demand will fall short of last summer’s phenomenal level,

then it is pretty easy to forecast summer pricing in the pork

complex below last year. Futures traders seem to be just

catching on to that. Of course, they are still super-optimistic

about pricing in the fall, but my guess is that they will also see the

error in their ways once we get closer to that time period. This

week’s slaughter tallied 2.43 million head, almost even with the

week before.

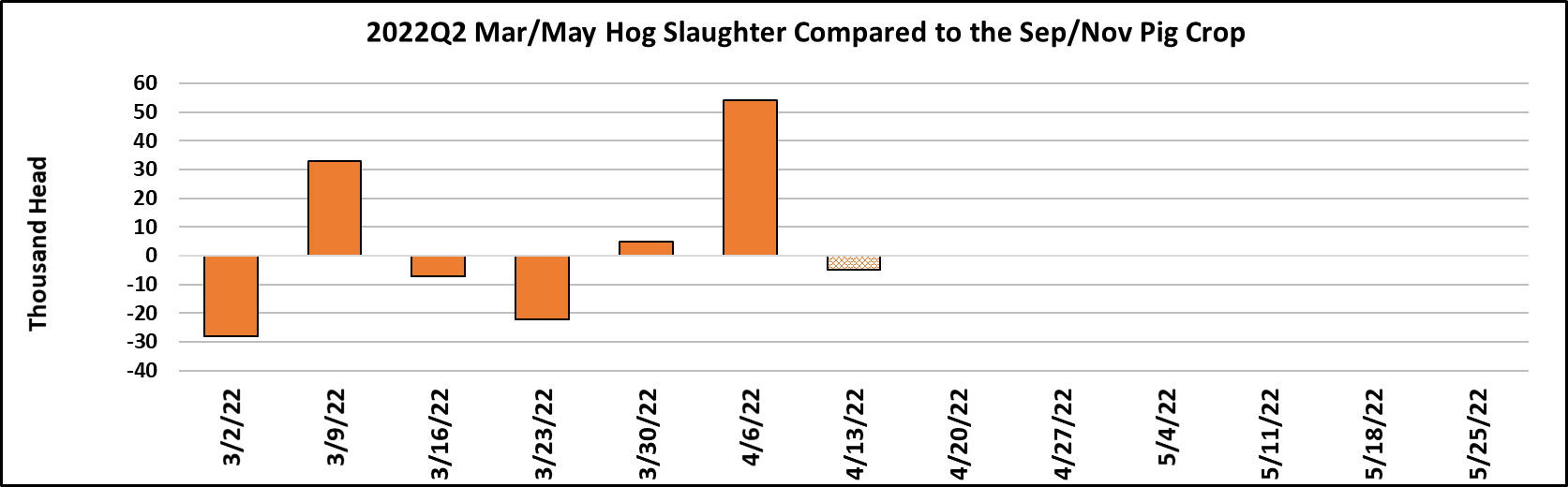

Relative to what the Sep/Nov pig crop projected, this week’s

slaughter looks big, but since we began this quarter, the positive

and negative deviations in slaughter relative to the pig crop have

been pretty well balanced so that in aggregate it looks like

USDA’s estimate of the Sep/Nov pig crop was quite close. When

June rolls around, we will start killing the Dec/Feb pig crop and

that one was only 1% below last year. It is interesting that just a

little over a week ago, USDA issued a very bullish Hogs and Pigs

report that showed supplies solidly below analysts’ estimates

and, in the intervening period, the Jun futures have dropped over

$10. That is a testament to just how over-priced those summer

futures were.

Next week’s kill should be a bit lighter than normal as some

packers scale back the kill on Good Friday and the Saturday

before Easter. The drop probably won’t be large and they can

easily make it up the following week. This week’s carcass weight

data didn’t hold any surprises and we still have weights moving

mostly sideways before they begin their summer descent in about

three weeks. There is not a whole lot more to say about this

market. It seems well-behaved on both the supply side and the

demand side. However, in my experience, these quiet markets

generally don’t last long before something comes along to inject

additional risk and thus increase the forecasting difficulty. For

now though, it is a pleasant change to have such a well behaved

hog and pork complex.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}