Pork Wrap April 7

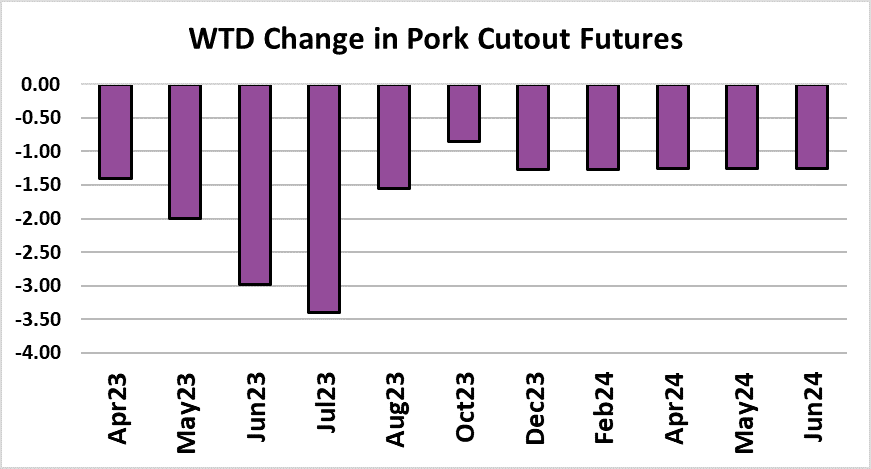

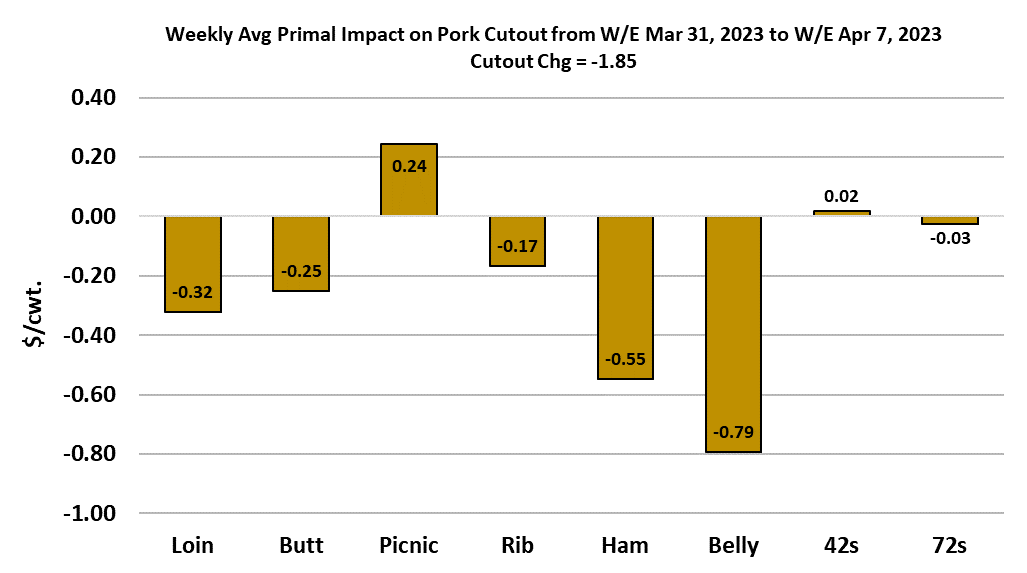

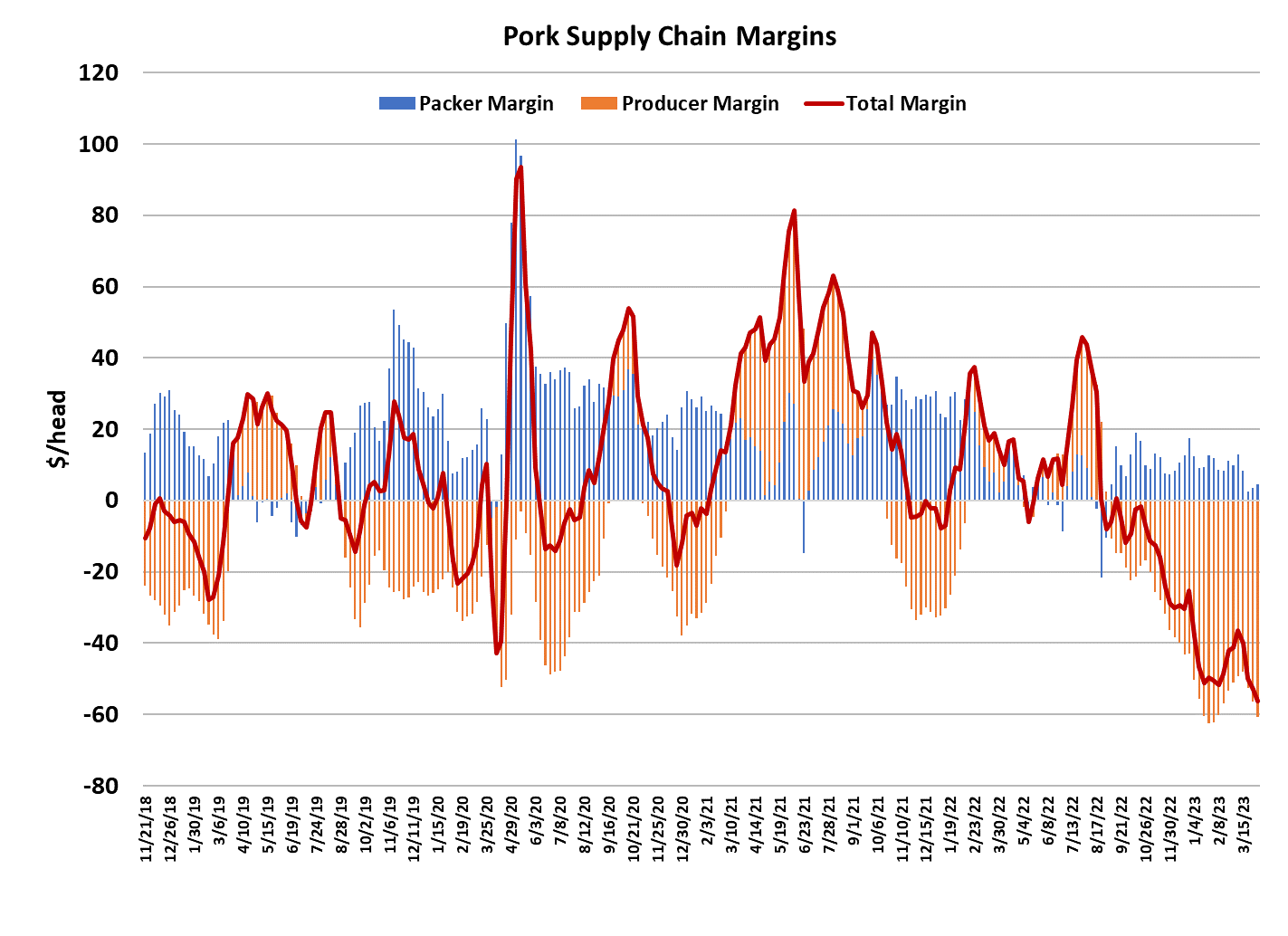

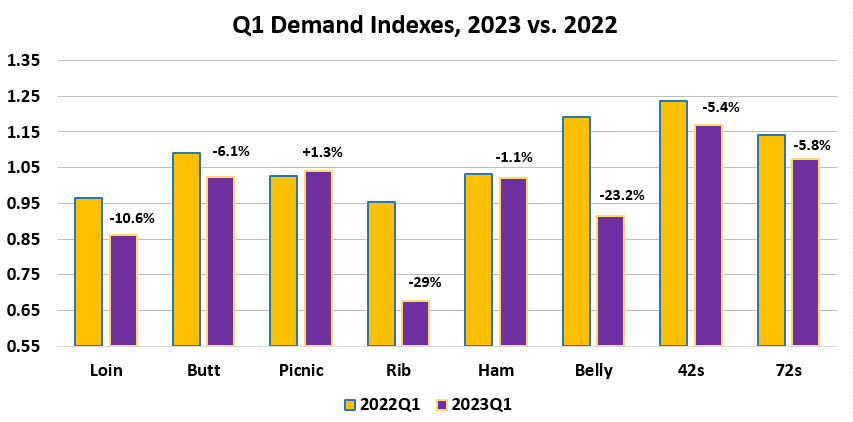

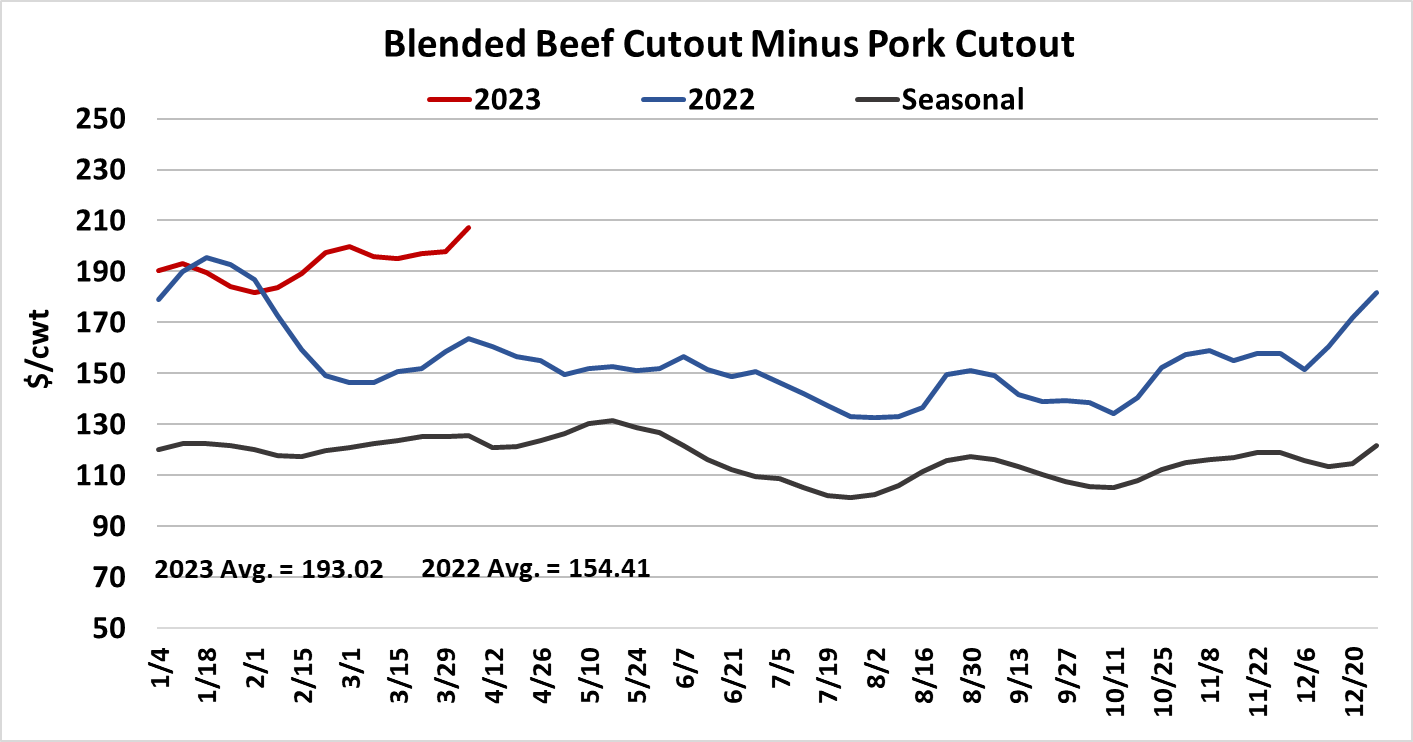

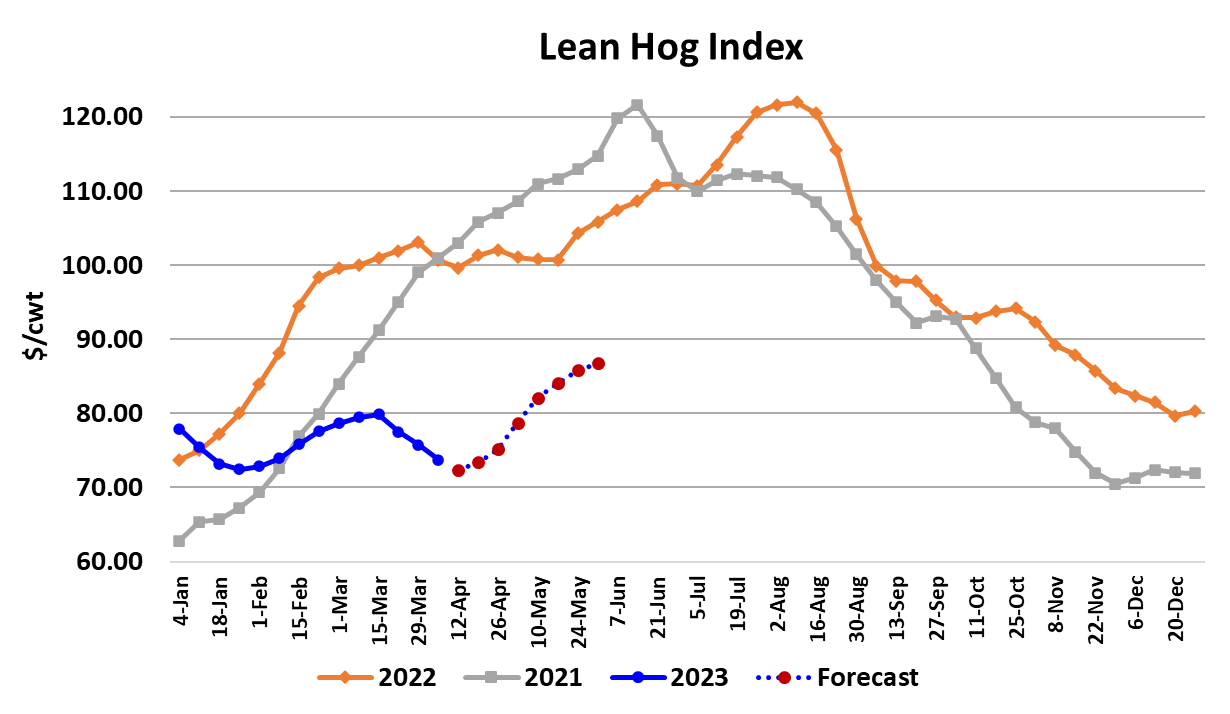

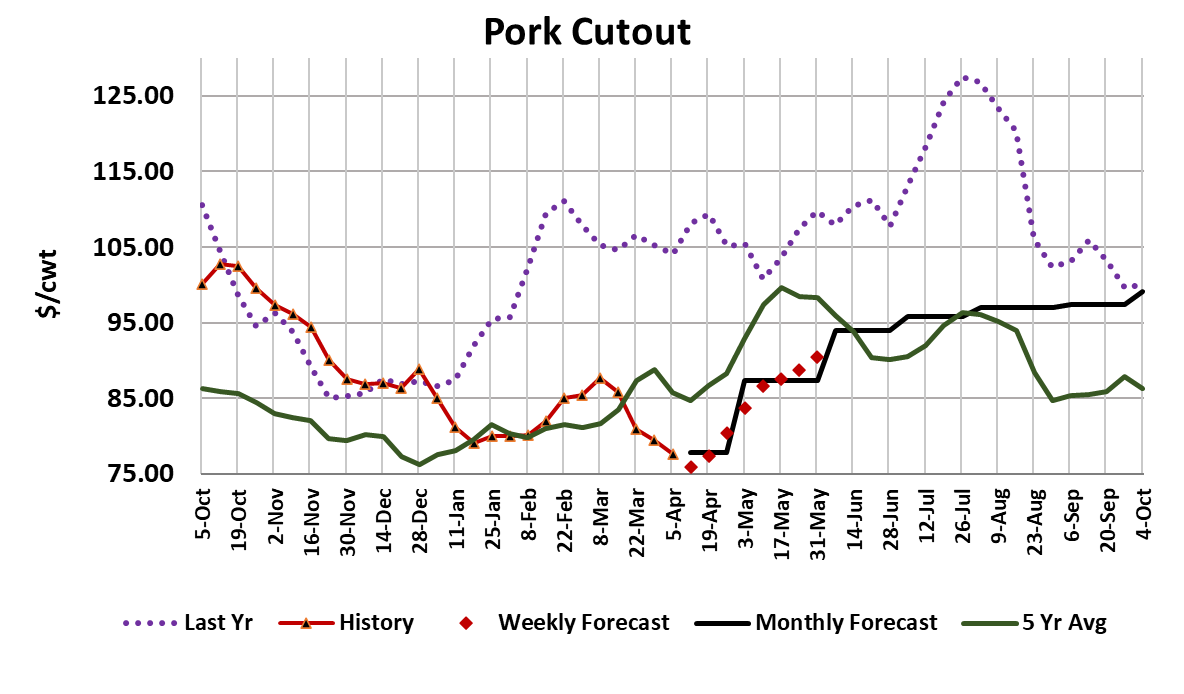

The pork market continued on its downward trajectory this week as the cutout dropped $1.85/cwt. to average $77.66 for the week. The cutout has now lost $10 in very methodical fashion over the past four weeks. Packers have responded by pressing down on the negotiated hog market and we saw the WCB price lose $3.57/cwt. this week. With both the cutout and the cash hog markets moving lower, the LHI came under pressure again, dropping $2.02 to average $73.70. It looks like the LHI still has a couple more prints before all of this week’s decline is fully reflected in the Index, so we should see the LHI print close to $72.50 by early next week. The April contract has only 6 trading sessions until it expires on Monday, April 17 and, after a brief trip to the $72 area, it rallied near the end of the week and is now hovering around $74. Those traders that are buying the futures at $74 are betting on something to change in order to break the downtrend that the market has been in for the better part of two months. Perhaps the bulls think that this week’s holiday shortened kill will boost the cutout next week. That is certainly possible, but it may be a long shot bet because packers look like they are gearing up for a big kill next week to fill in the gaps. This week’s total slaughter registered 2.37 million head, down 4.7% from the week before, as most packers were planning to be dark on the Saturday ahead of Easter and some shifts were cut on Good Friday. However, the MPR data suggests next Saturday’s kill could be close to 140k, and that has the potential to push weekly slaughter to about 2.54 million head. That big production will be happening right as the Apr contract is set to expire. The market struggled to digest last week’s 2.49 million head kill and prices for all of the primals except the picnics were lower on a weekly average basis. Bellies and hams were both softer again and there doesn’t seem to be any evidence that those are going to turn higher in the short run. The combined margin moved lower again this week, setting another all-time low. Domestic demand continues to look awful. The Q1 demand index for the cutout is down almost 11% from Q1 last year. The attached chart shows the YOY change in the Q1 demand indexes for each primal. We got the February trade data from ERS this week and it showed pork exports up 3.7% from February, 2022, but last year’s number was particularly weak. The more-timely weekly export data has been tracking pretty closely to last year, so I don’t expect that the data for March and April will show big YOY gains, when it becomes available. All that said, the market should be getting pretty close to a turning point. After next week’s catch-up kill, we should start to see weekly slaughter tracking seasonally lower. If we don’t, I will be really concerned. Demand too, seems like it should be poised for a rebound. Beef packers are going to have to raise prices yet again after paying up sharply for cash cattle this week and that is going to make pork look very attractive for retail features this grilling season. Let’s just hope that consumers will buy pork. We know they will purchase beef, even at very high price levels. Maybe retailers will be concerned that pork features just won’t resonate with consumers and thus they continue to stick with beef until consumers revolt at high beef prices. The attached chart shows just how high the beef cutout is relative to the pork cutout right now. There have been a few times in the past when that spread got as wide as it is today, but they didn’t last long. Packer margins were almost unchanged this week at $3.81/head but hog production margins slipped even deeper in the red, now close to -$60/head. Q1 producer margins this year will be the worst in my dataset going back to 2007. It is reasonable to expect they will scale back production in the second half of this year. The front five futures contracts all look pretty close to my estimate of fair value, but from October onward they look $6-8 too cheap. Perhaps traders are not counting on producers to scale back production as much as I am. Given how high feed costs are, if all of the prices reflected by the hog futures market come true, it is going to be a dismal year indeed for producers. Next week, watch to see if this week’s restricted production can lift the cutout a few dollars. If it doesn’t, that’s a pretty bearish sign and there will likely be more selling by futures traders. Either way, expect cash hog prices to continue to ease lower.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}