Pork Wrap April 5

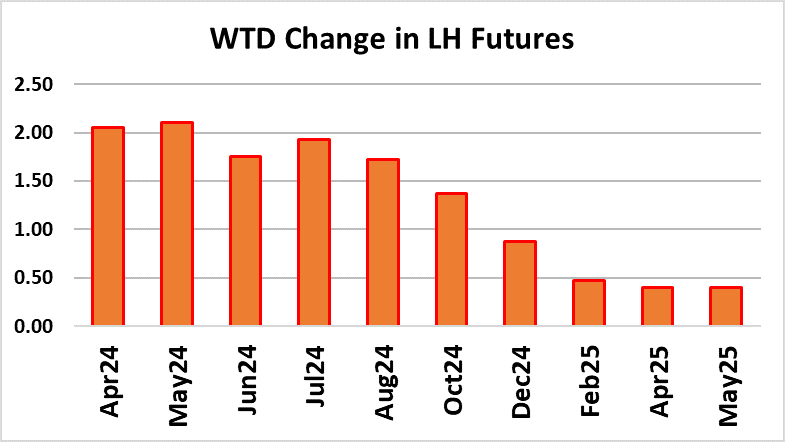

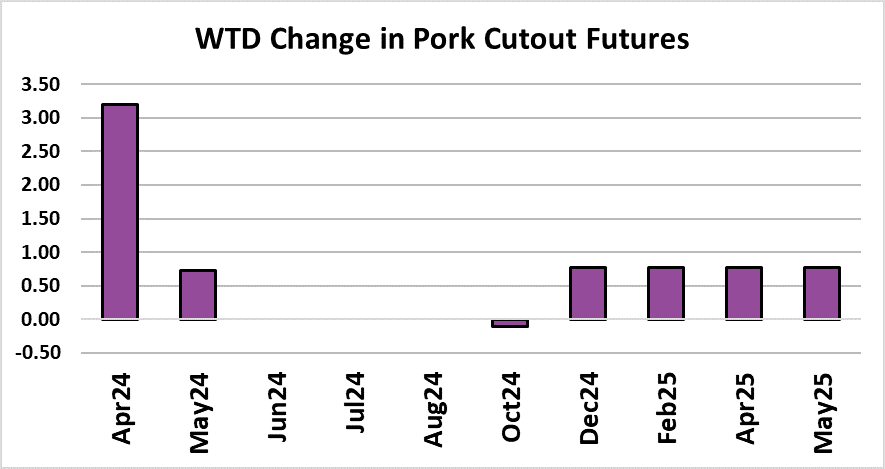

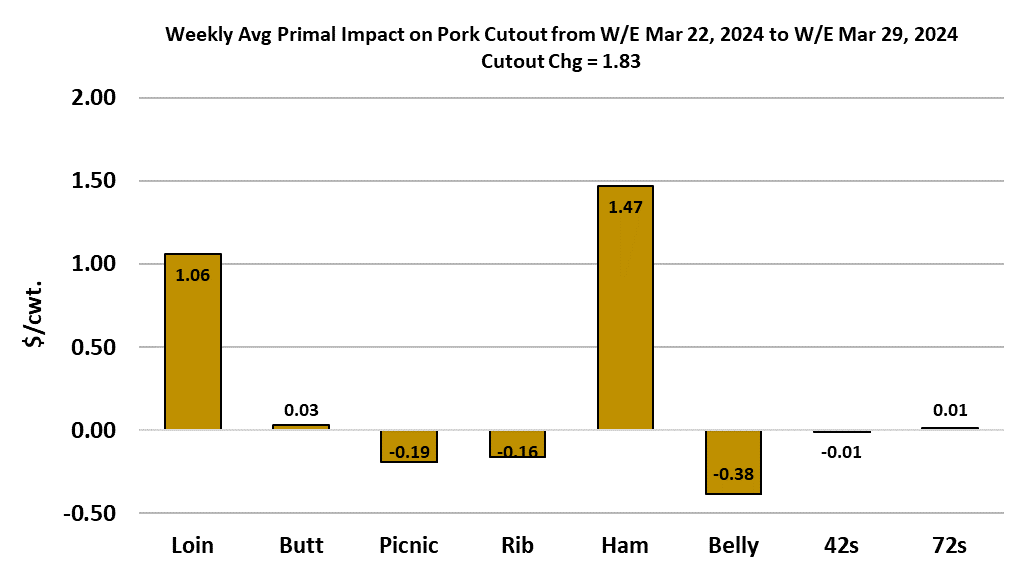

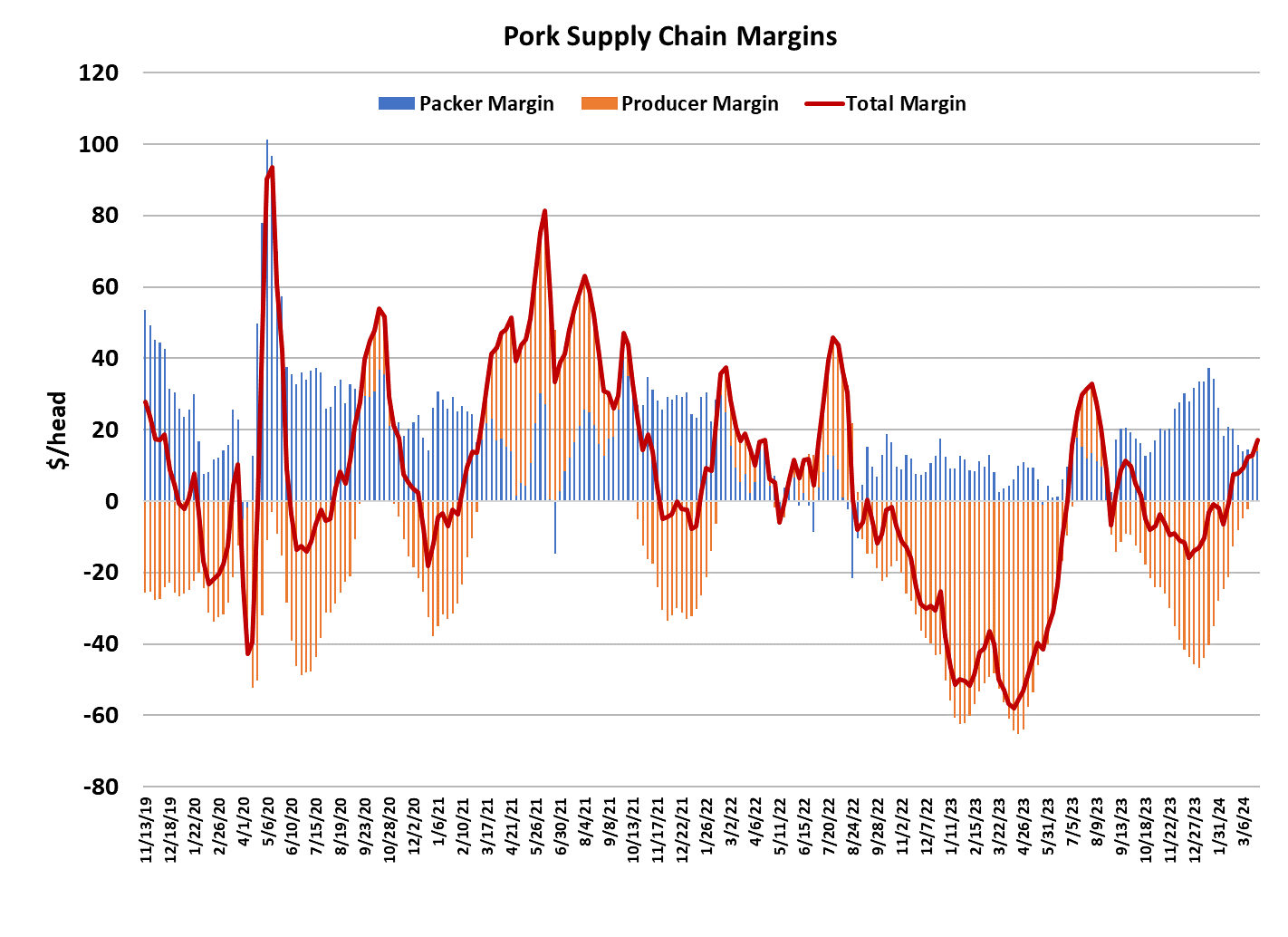

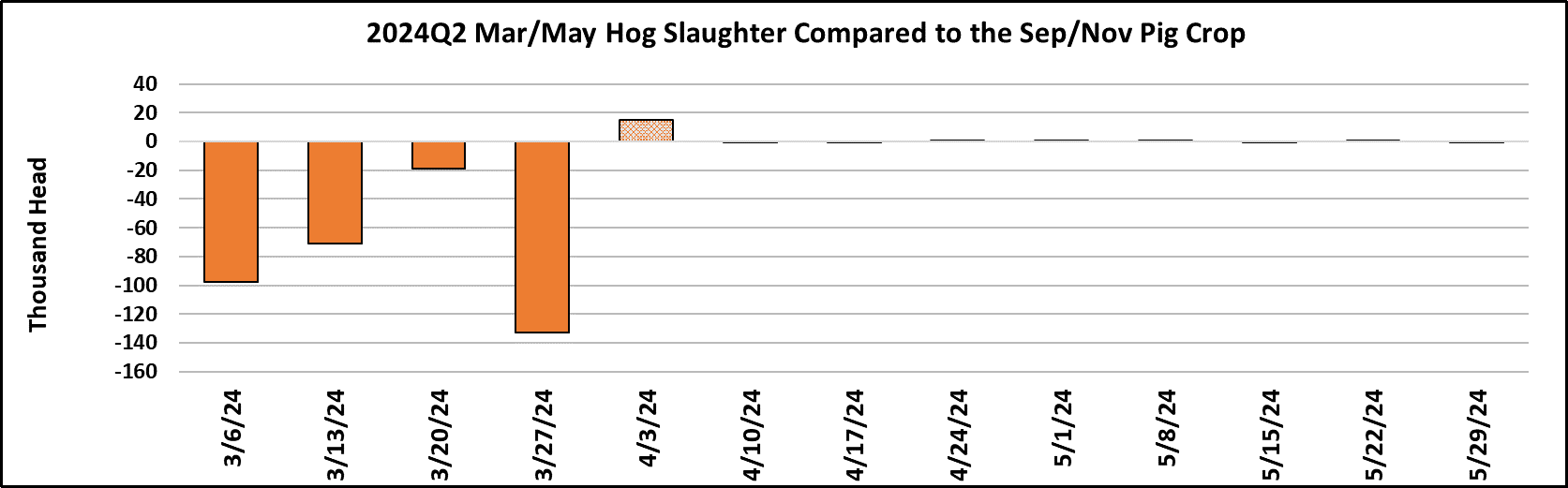

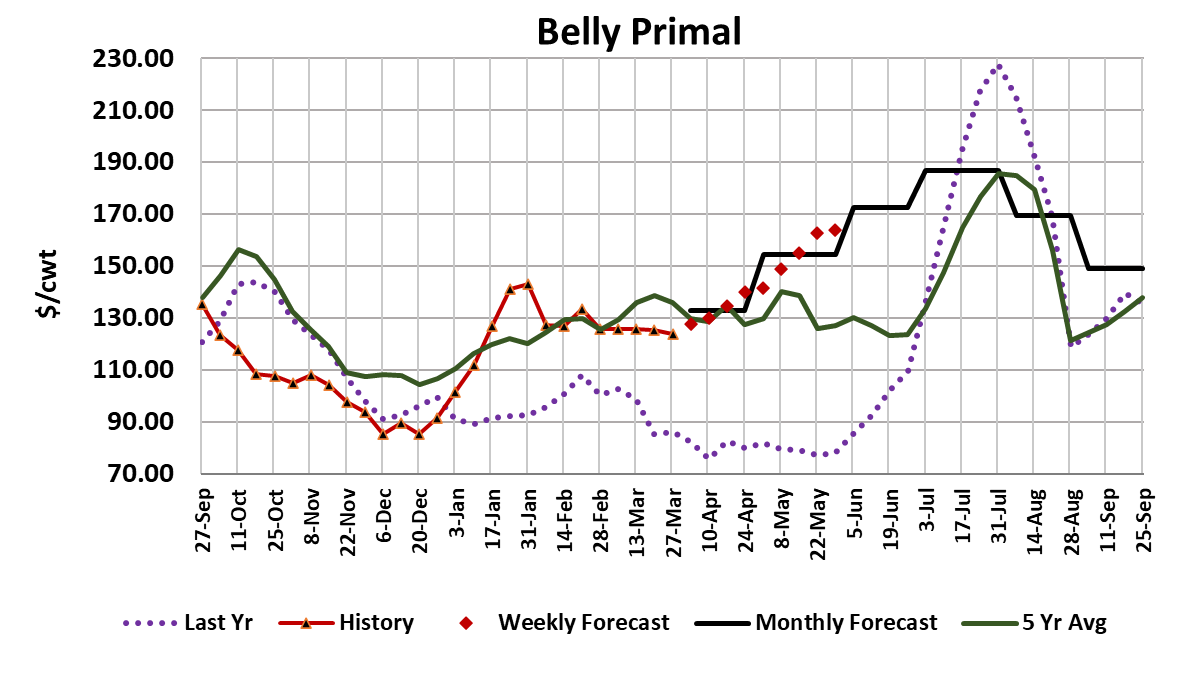

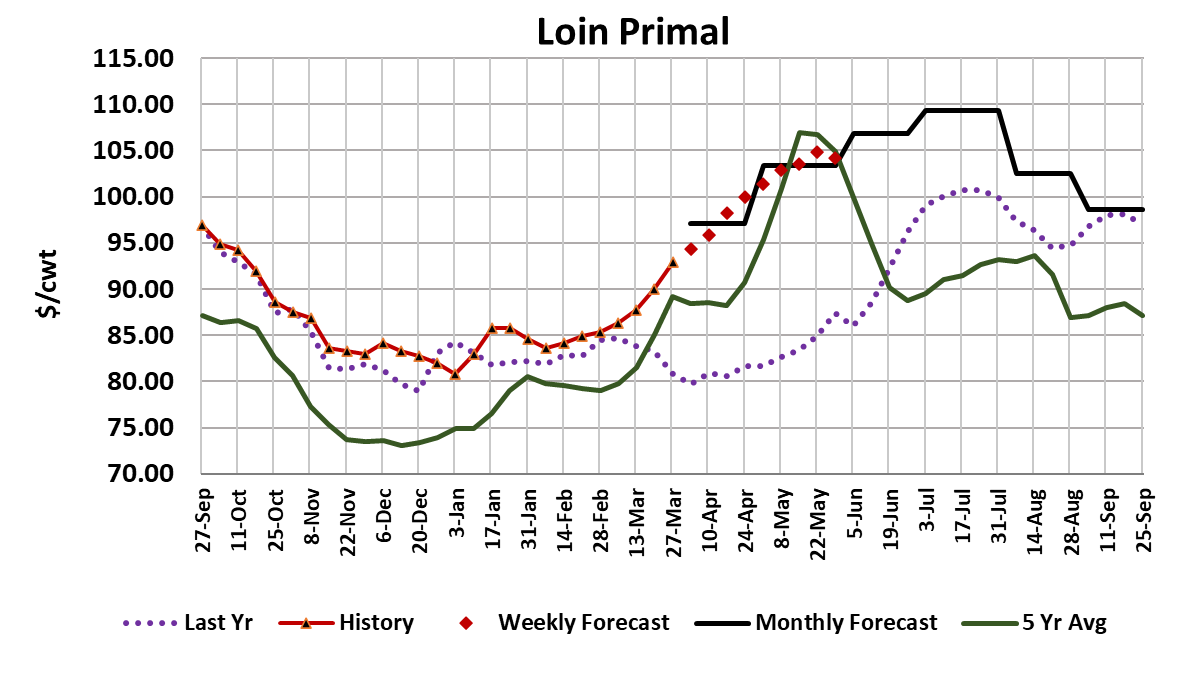

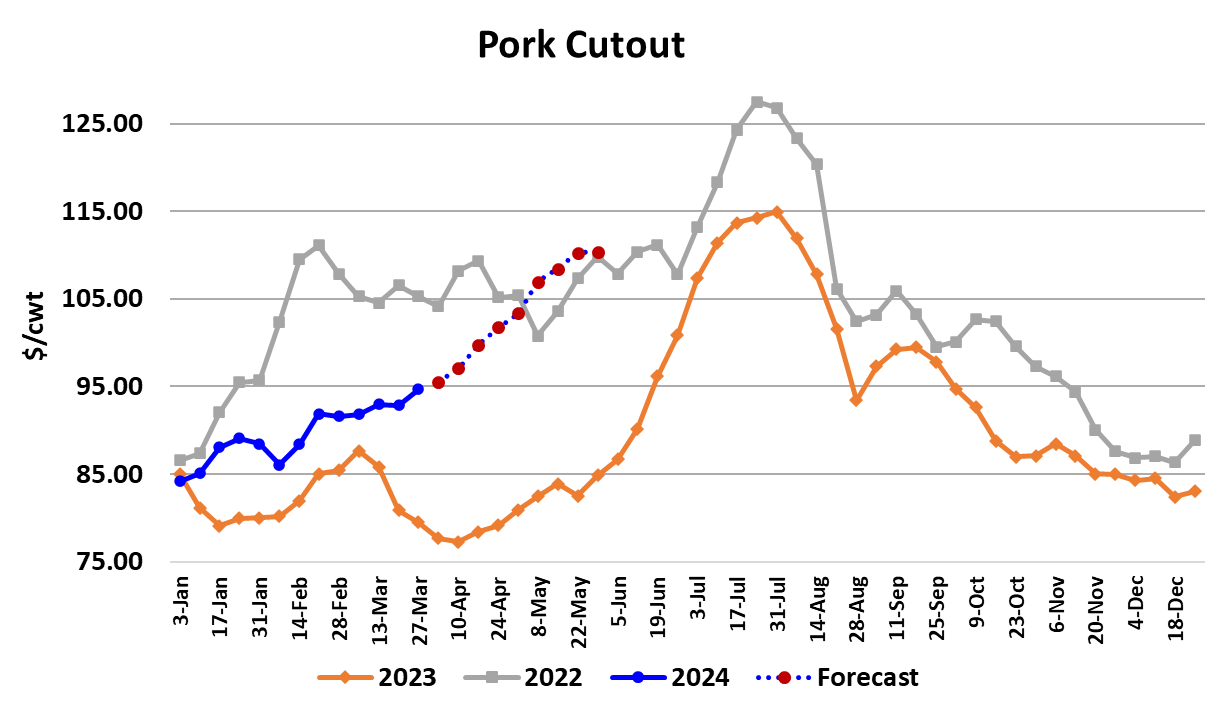

Cash hog prices jumped this week and it could be a sign that near-term hog supplies are already starting to tighten up. The WCB negotiated market added $5.01 to average $85.39. The cutout also saw good gains, adding $2.25/cwt on a weekly average basis. Most of the gains came later in the week and haven’t fully flowed through to the LHI, but when that happens next week we could see the LHI push over the $90 mark. This flurry of higher prices woke up the front end of the futures curve, allowing Apr to gain $2.70 on the week and the May through July issues adding $5-6. Hams were the big driver of the cutout’s improvement this week and it doesn’t look like the upward move in ham prices is done yet. For bellies however, it was more of the same as the belly primal averaged $123.40, down $0.47 from the week before. The retail cuts also contributed positively to the cutout and most of the forecast revisions to those items were upward. Suddenly, prices in the complex have regained upward momentum and if that carries into next week, there is a strong possibility that the LHI will reach $90 or better before the Apr contract expires next Friday. It is also starting to look like kills are ready to trend seasonally lower. This week’s slaughter registered 2.42 million head, but that was influenced by a short kill on the Monday following Easter. Next week’s slaughter could be closer to 2.46 million head unless there is a plant disruption. More importantly, we are now five weeks into the March/May quarter and all five weeks have seen kills below what the Sep/Nov pig crop implied. The cumulative under-kill for the quarter to date is now about 360k. It is starting to look like, for the first time in a long while, USDA may have actually over-estimated the size of the pig crop. That means less hogs than expected in the near term and could portend continued strong increases in negotiated prices to the detriment of packer margins. Once all of this week’s price increases have fully flowed into the LHI next week, packer margins should be near $11/head and by the time we get to Memorial Day, I’d expect margins to be down around $5-6/head. The packer’s loss has been the producer’s gain, but the combined margin continues to rise. Soon it may challenge the top set last summer. Obviously, pork demand is now strong enough to allow both packers and producers to enjoy positive margins. That is a very constructive development that has been a long time coming. Last’s week’s bearish Hogs & Pigs report didn’t even get a second look from traders who were more concerned with keeping pace with rising cash markets. This week’s futures gains brought the Apr through Jul futures into alignment with the fundamental forecast and rendered the Aug and Oct contracts about $5 too high relative to the fundamentals. USDA released the official export data for February this week and it showed a 17.7% YOY increase that impounded a nearly 69% YOY gain in shipments to S. Korea. Further, exports to Mexico were up 22%YOY, so it appears that interest in US pork remains high among international buyers. This week the ham primal added over $6/cwt. to average $85.59 and the forecast has it continuing on an upward path for at least a couple more weeks. Bellies, on the other hand, just can’t seem to get any traction. However, as kills start to shrink in the next few weeks, I expect bellies to wake up and add $10-15 to the primal value. I think there is a reasonable chance that the cutout will print in triple digits at least one day next week and by the following week we could have the weekly average over $100. Last year, the cutout didn’t print in triple digits until the last week of June. Going back to the beginning of this year, the cutout has averaged just about a $1 increase every week. From this point forward, it seems reasonable that the pace of increases should quicken and it is likely that summer price targets will need to be raised. I’m looking for the top to come in July this year, but could see it developing sooner given the early start to seasonal price increases. Next week, watch for the hams to continue pushing the cutout higher. Further gains in negotiated prices are likely to materialize as well. The price target for Apr expiration is now slightly north of $90.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}