Pork Wrap April 30

Something changed this week in the hog and pork complex. For once,

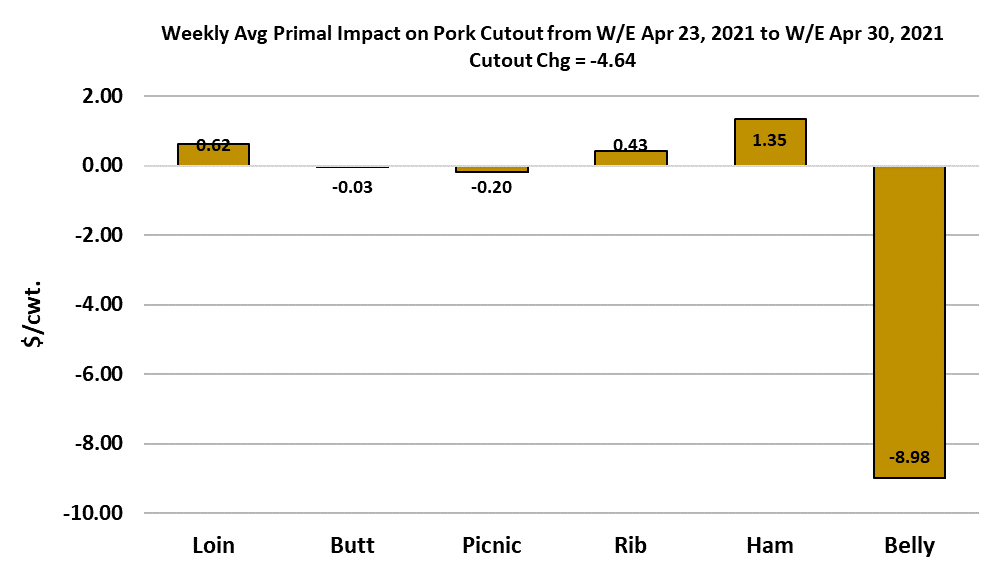

everything did not move higher. The pork cutout dropped nearly $5 on a

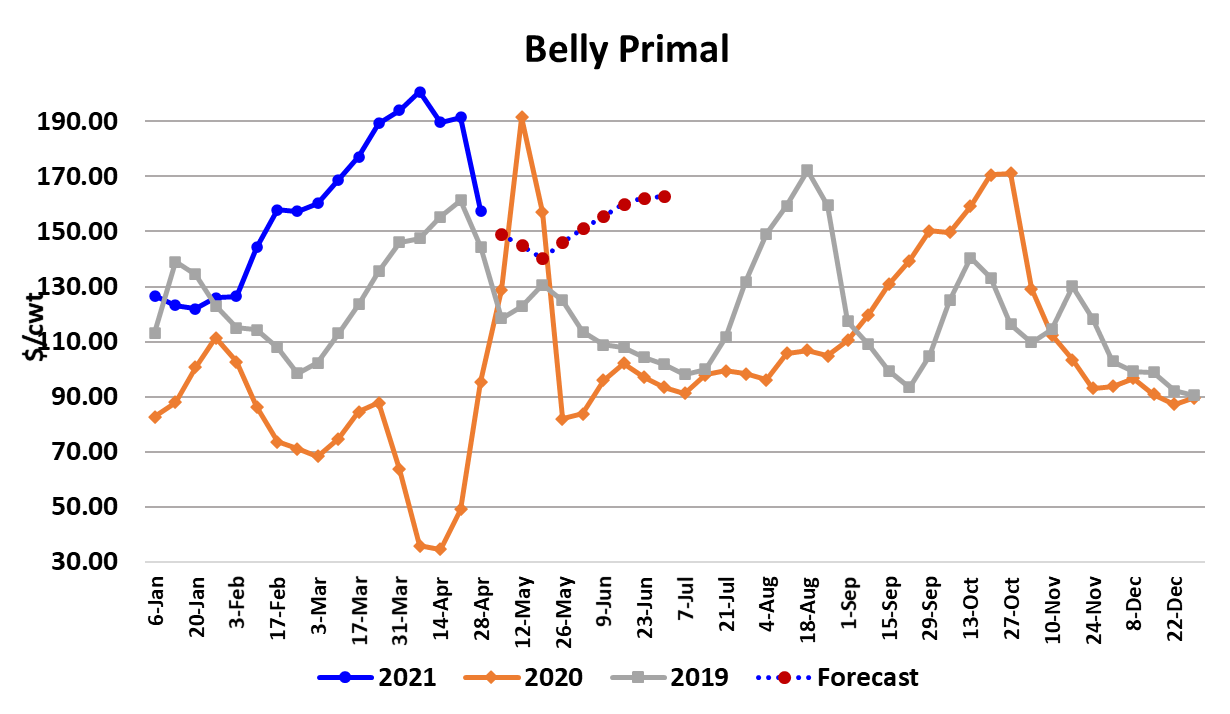

weekly average basis. That drop was driven almost exclusively by weakness in the belly primal, which lost $34 this week and is now at its lowest level since early February.

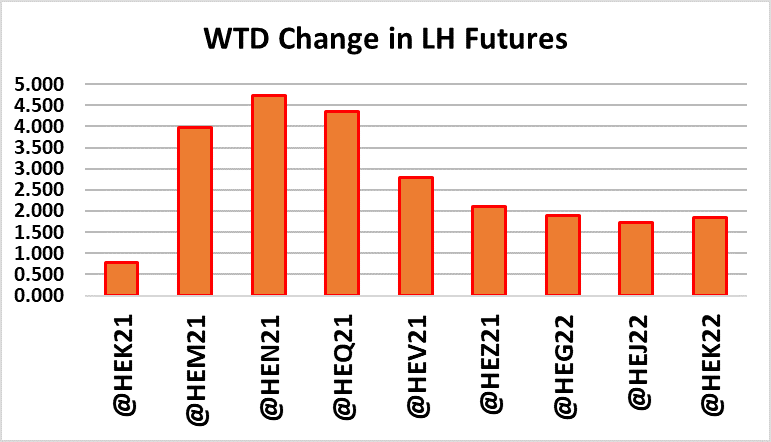

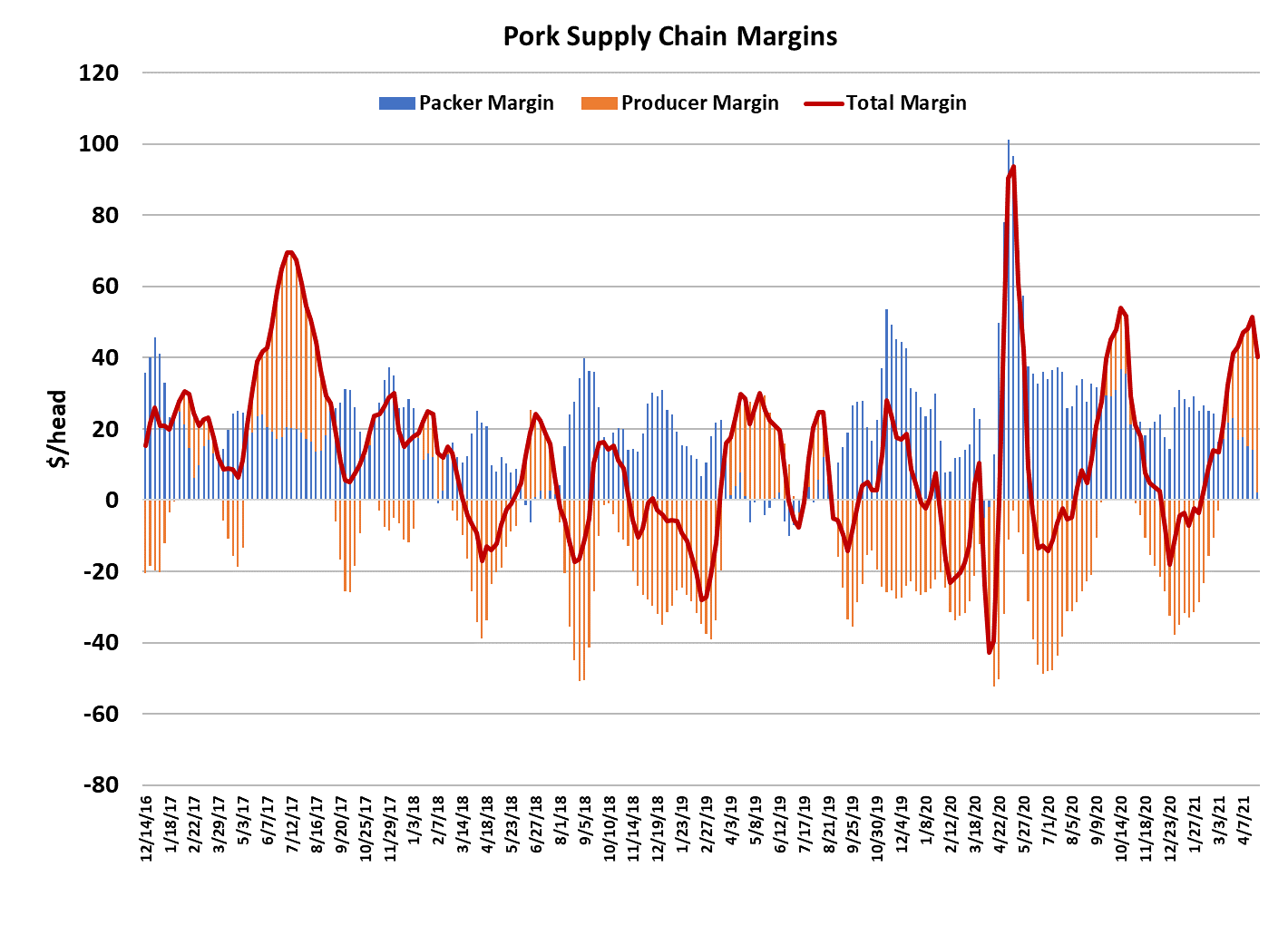

While the cutout was pulling back, the negotiated hog market just kept marching higher, with the NDD market up $4.50 on weekly averages. Cutout down, hog prices up, means packer margin compression and boy did that happen this week. Packer margins for last week are calculated to be only $1.58 per head. Margins will likely go negative next week.

To illustrate just how unusual this is, the pre-COVID, 5-year average margin for the last week of April is over $11/head. There have only been a very few instances of negative margins over the past five years and most of those have occurred in June or July when hog supplies were very tight.

What can packers do to rectify this margin problem? Not much. The normal response would be to scale back on the kill, but kills are already getting small seasonally and packer’s per-unit costs would escalate if they purposefully reduced the kill now. Besides, no packers want to tell workers that they must work reduced hours when labor is so tight already. So, packers will just deal with negative margins for a while and hope to make it up when hog supplies begin to increase again after mid-summer. It will hurt more for the packers who are pork-only than for other majors who slaughter both hogs and cattle.

Cattle margins this week were over $700/head. The chart to the right shows that there was very little change in the contribution of the non-belly primals to the cutout this week—most showed very little change. So, it appears that if one

wants to know the direction of the cutout, one needs to have a good handle on where the bellies are headed from here. The bellies actually peaked three weeks ago (chart to right), but this week featured the most dramatic price decline. I’ve got the forecast drawn to allow just a few more weeks of small declines in the bellies before they start to work higher again once vacation season gets into full swing after Memorial Day.

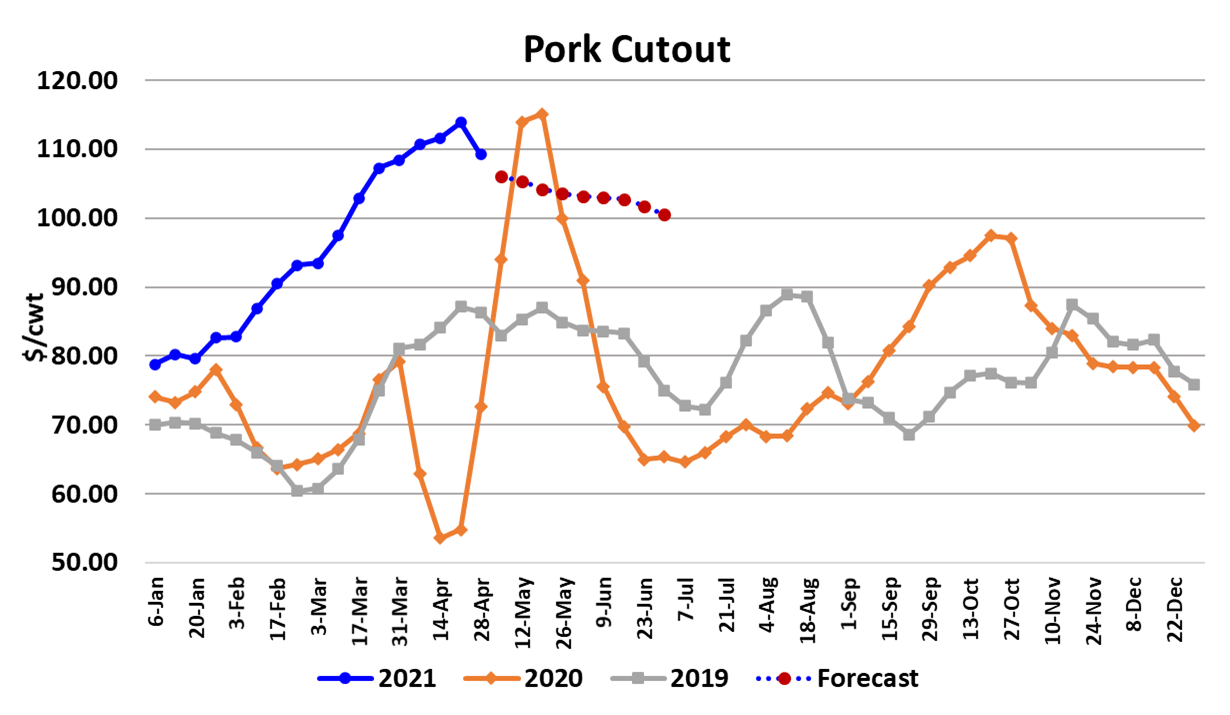

Last October when the hog and pork markets were on fire, it was the peak in the bellies that marked the beginning of the end in that rally. The cutout essentially followed the bellies lower and eventually all of the other primals capitulated as well. Will that be the case this time? Maybe, but it is hard to know because the situation is so different now. We are in a period of tightening hog supplies, whereas last fall hog supplies were expanding. That made ending the rally a whole lot easier. I do have the cutout working lower from here, but slowly, and there could be brief rallies along the way. I’m keeping the cutout forecast over $100 into early July.

The cutout futures are more bullish, keeping it over $100 until October. We must not forget the old adage that the “cure for high prices is high prices” and this won’t last forever. With prices staying so elevated for so long, it will likely generate a supply response and give producers reason to expand. The one obstacle to that in the current environment is corn prices in the $7-8/bu range. If they hold there through the summer then producers might be more reluctant to expand and thus the period of high hog and pork prices might last months longer than it would if corn prices were down at a more typical $3-4/bu level. Consumer demand will play a big role as well. Demand for pork has been red hot, but this week the combined packer +producer margin turned decidedly lower (chart to the right), and this doesn’t look like a head-fake type turn.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}