Pork Wrap April 29

The pork market got back on its downward trajectory this week,

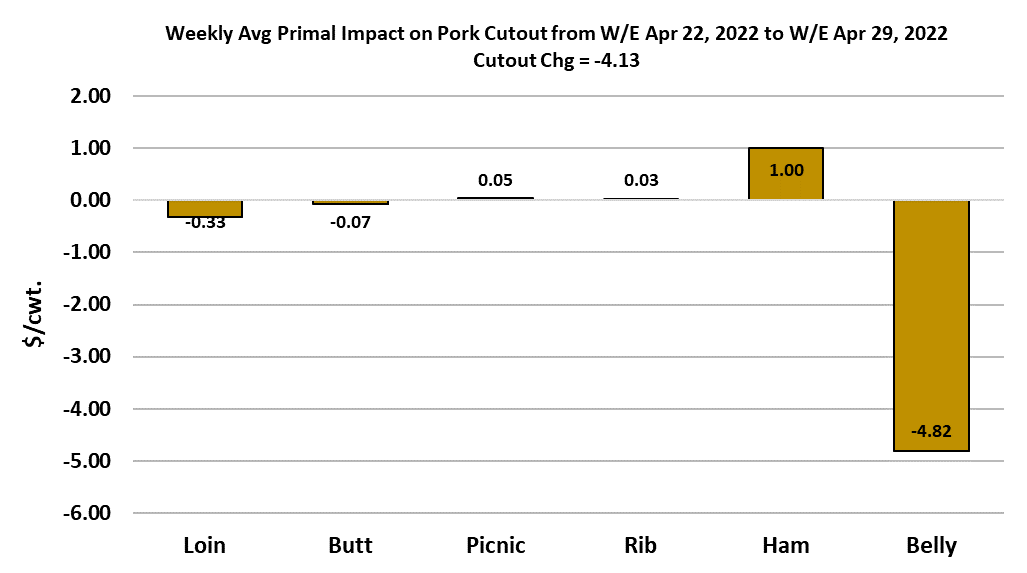

with the cutout dropping $4.13/cwt to average $105.18. Cash hog

markets were higher, with the WCB negotiated market rising

$2.81 and the NDD up $0.86. The LHI gained almost $1 to

$102.20. Hogs up and pork down is a bad combination for

packers and this week their margins fell to $4/head from $14/head

the week before. The drop in the cutout was almost entirely

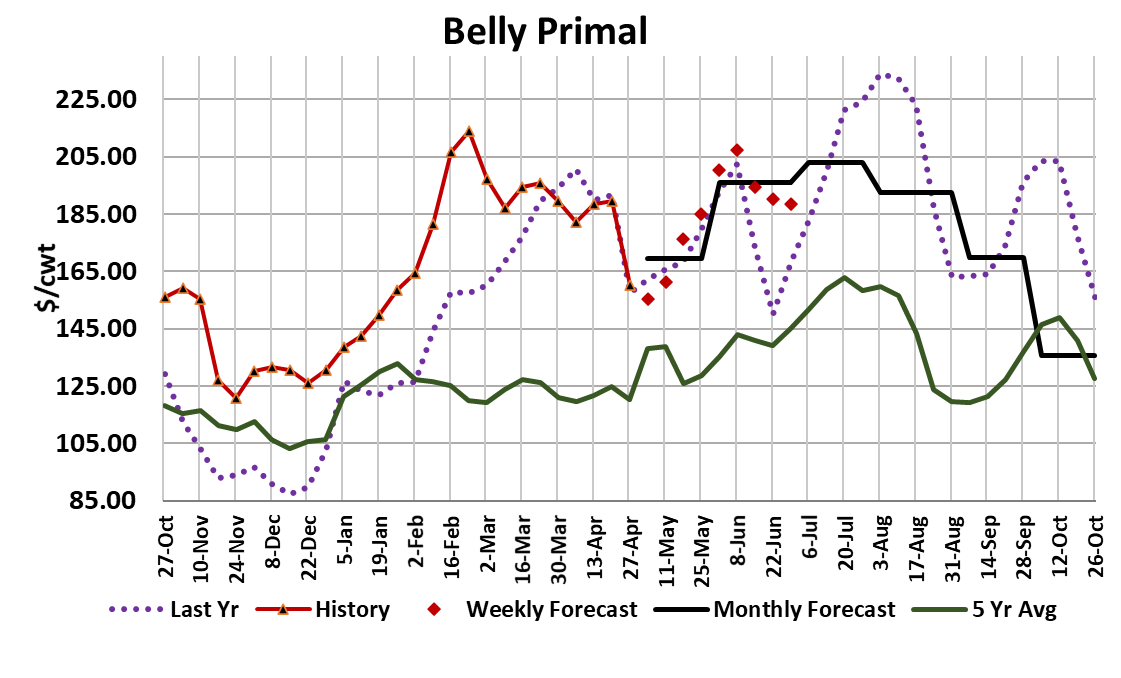

sponsored by the belly primal as the attached chart indicates.

Belly corrections are often severe and scary for market bulls and

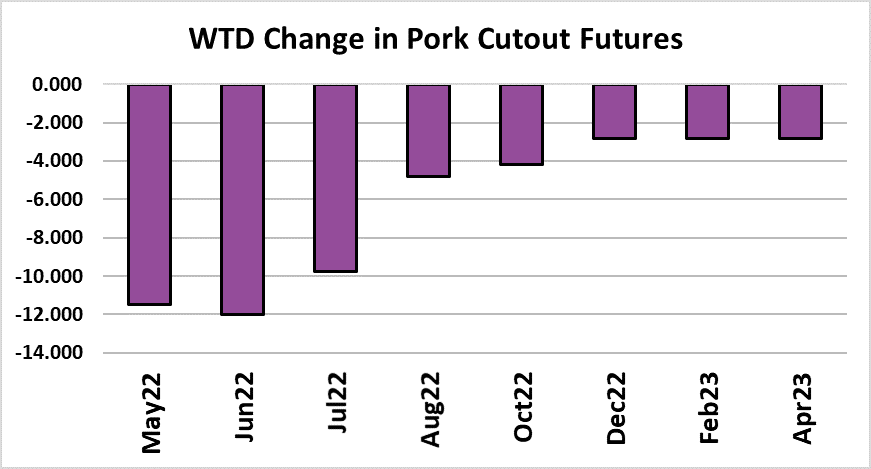

this one has been both. The futures market has undergone a

significant correction, with the Jun contract losing over $12 this

week. As scary as the belly correction has been, it is important to

keep in mind that the other primals seem to be holding value quite

well. I would be much more concerned if this was a broad sell-off

affecting all of the primals. Bellies will soon find a level that starts

to attract buyers.

I think maybe one more week of softness and belly prices should

begin to recover. Hams continue to do very well and what the

bulls need to hope for is that the hams continue to hold up until

the bellies can get back on track. If both show weakness

simultaneously, that would be a real problem. The retail primals—

loins, butts, ribs—have been sideways to higher recently and I

suspect that is due to consumers trading down from beef to pork

items in the retail environment. That isn’t likely to last forever and

eventually we will see demand soften for those items, but for now

they are providing a much needed ballast against the volatility in

the belly and ham markets. This week’s action removed most of

the mis-pricing from the front three contracts. More overpricing is

likely to come out of the deferreds as they get closer to the front of

the curve.

Pork demand is likely to follow the same path that beef demand is

on right now (weakening back to pre-pandemic levels), but

because of the trading-down effect, the impact on pork will

probably be a few months behind beef. Pork, unlike beef, has the

advantage that kills will be declining seasonally over the next two

months and that should prove to be price supportive. This week’s

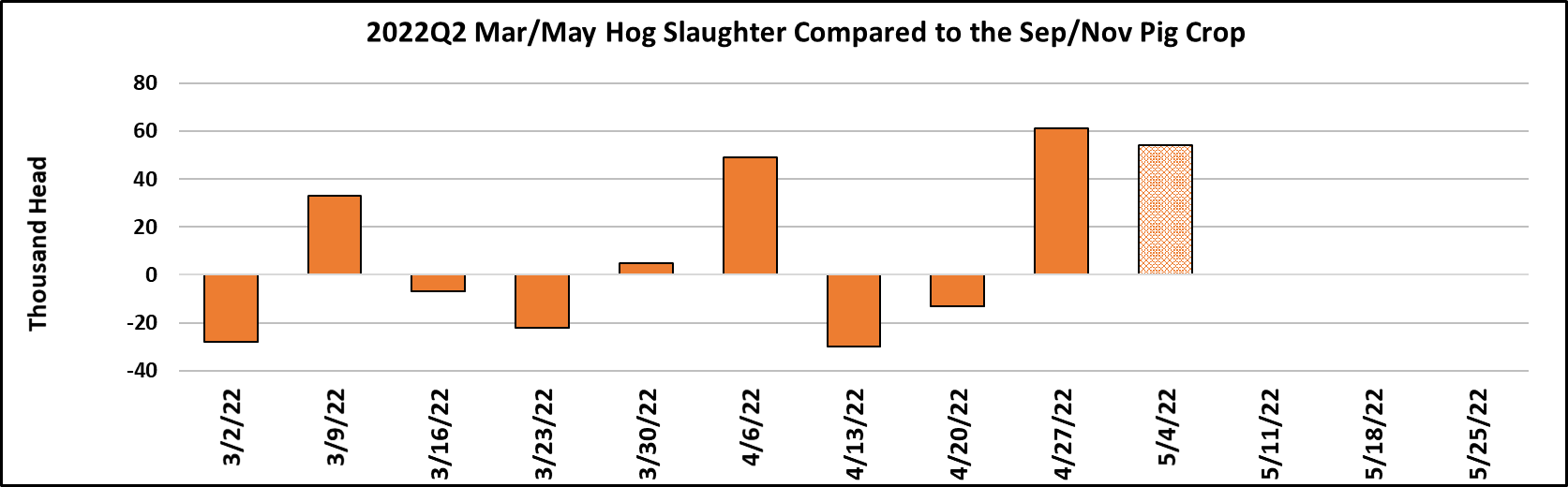

slaughter registered 2.4 million head, up about 30k from last week

and about 60k more than what the pig crop suggested. I’d expect

that packers temper the kill next week in an effort to limit further

margin erosion. The combined margin chart indicates that the

little bump up in the combined margin in the previous 2 weeks

was a head fake and it is now back on its downward trajectory.

My guess is that it at least touches the zero line before it starts to

improve.

Of course, there is a risk that pork buyers will pull back next

week after the big downdraft in hog futures and the huge sell-off

in the stock market. If they do, that might take a few more dollars

off of the cutout, but they can’t stay on the sidelines forever,

particularly during grilling season. One might think that hog

producers are doing pretty good with the LHI at $102, but their

breakevens are only about a dollar below that, so they aren’t

seeing much in the way of margin currently. That is the problem

with a declining demand environment—there isn’t enough margin

in the system to go around. For the next two months, packers

and producers will be arm-wrestling for what little margin is

available. Carcass weights were reported one pound lower this

week and that could be the first step in a seasonal downtrend

that will take weights progressively lower from now until

Independence Day.

There doesn’t seem to be any abnormalities with weights

currently. There must still be some lingering disease problems in

the WCB market because prices there have been erratic again

this week. However, I don’t think it is going to turn into a largescale shortage of hogs. Exports are still very soft compared to

last year and that is important to keep in mind when considering

domestic supplies this summer. We know that the pig crop that

will be slaughtered from June to August was reported down 1%

by USDA, but much weaker exports this year (and stronger

imports), could cause Jun-Aug availability to be as much as 2%

greater than last year. So we could see a summer where pork

availability is larger than last year, yet demand is way softer than

last year. That is why I haven’t been a proponent of super-high

pork pricing for summer.

The cutout is expected to be in triple digits for sure, but likely not

into the $120-130 range that the futures have wanted to project

for so long. Instead, buyers should be thinking about summer

cutouts in the $100-$112 range. I think the risk to that forecast is

that actual cutouts turn out to be lower, rather than higher, than

the forecast. Sow pricing moved lower again this week, but it is

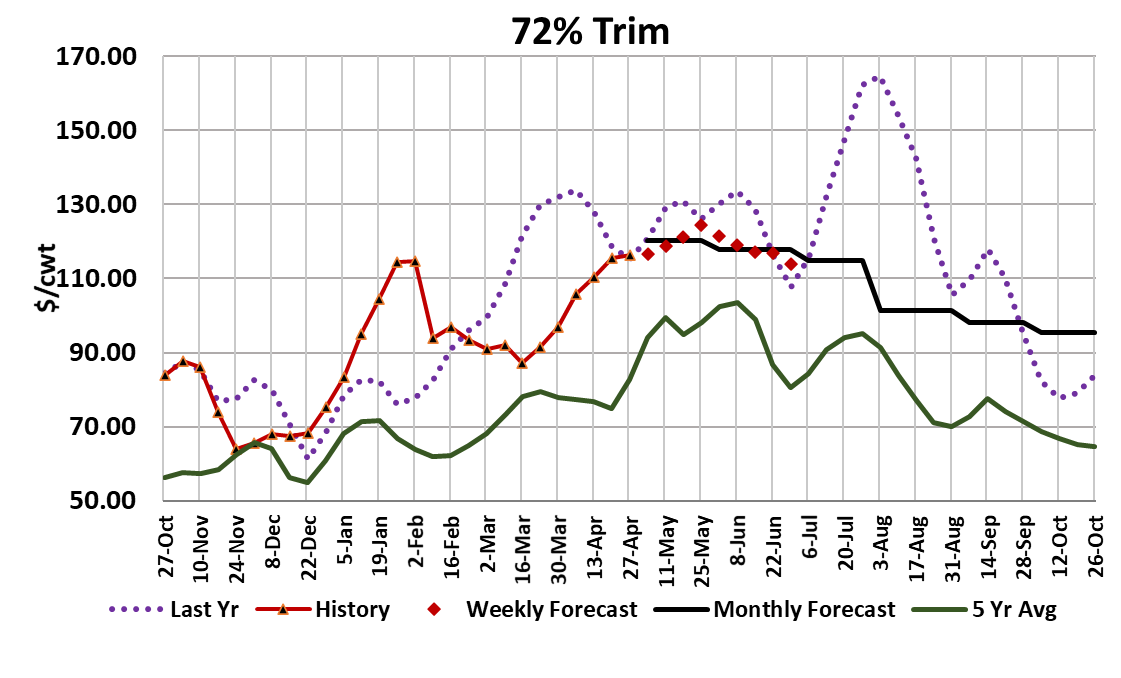

still very high in a historical context. Trims are also very high and

that is a big supporting factor for sow prices. It is just another

example of consumers trading down to cheaper protein sources.

Next week, watch the bellies for signs that they are making a

bottom, since that will likely determine the direction of the cutout

and the mood in the futures market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}