Pork Wrap April 27

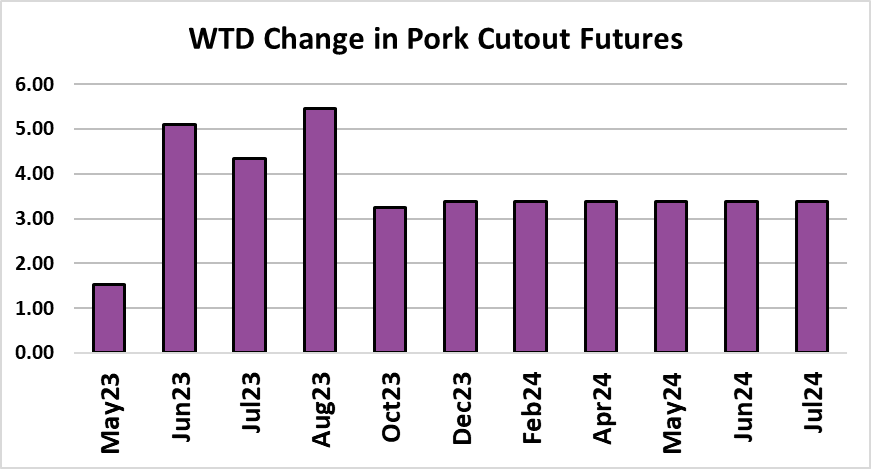

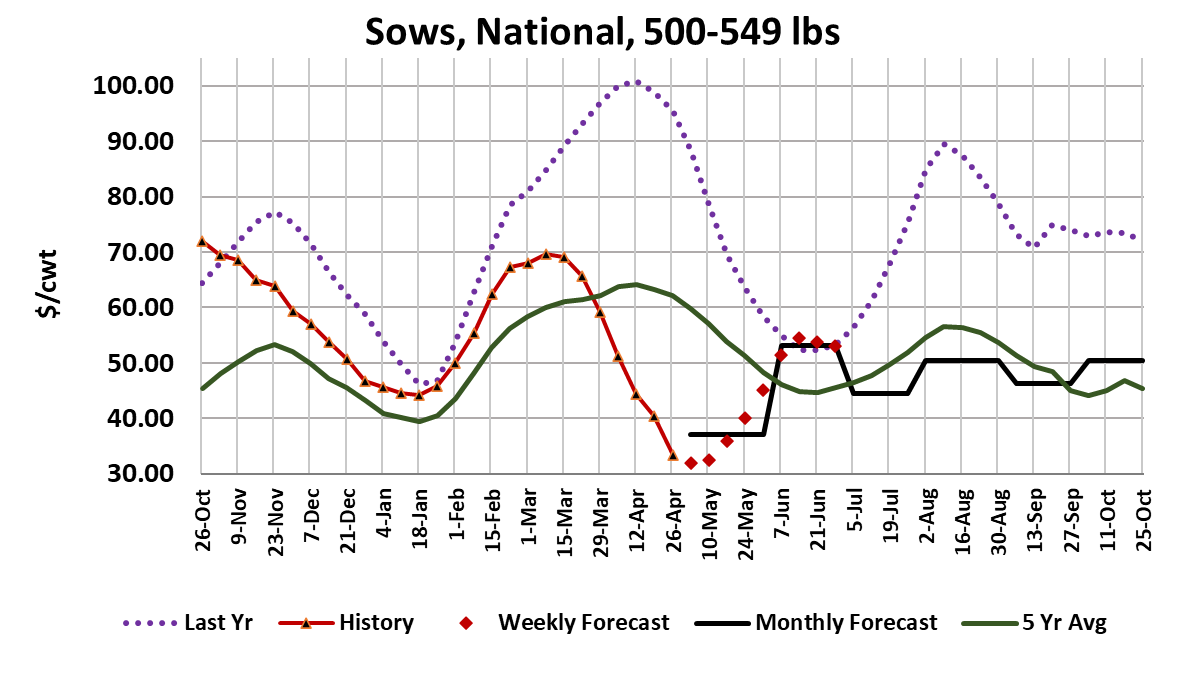

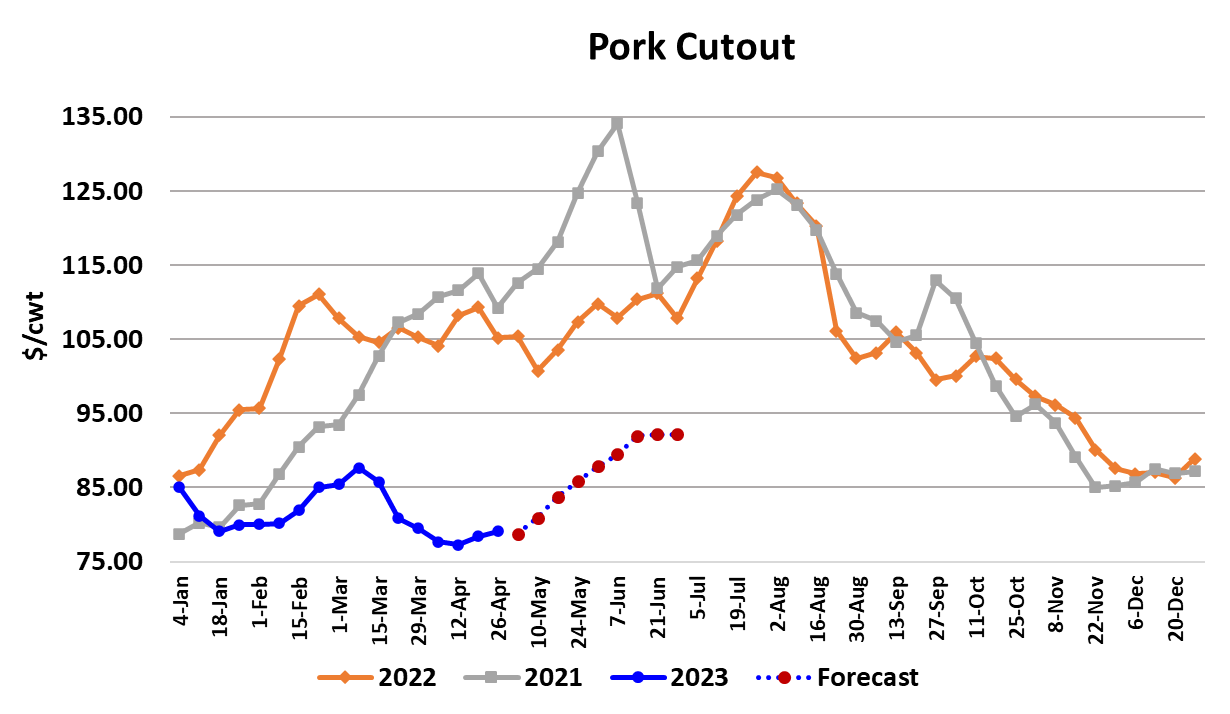

It was more of the same for the pork cutout this week, posting a tiny $0.73/cwt. gain to average $79.12 for the week. The real excitement however, was in the cash hog market where the WCB negotiated price moved $3.24/cwt higher to average $71.69/cwt. The NDD also gained, but it was up only $1.82/cwt. on a weekly average basis. The futures market leapt with joy at this newfound strength in cash hogs. The May contract added over $2 and the June contract was up almost $6. Both were already carrying significant premiums to the cash index, but that didn’t seem to matter to traders. The other important news this week was a fire at Tyson’s harvest facility in Madison, Nebraska. That plant was killing about 8,000 hogs per day, so it isn’t insignificant. Tyson indicated that the plant would likely remain idled until mid-May, when repairs are completed. In the meantime, they are shuttling hogs to their other plants in the vicinity so customers need not worry that their orders will be shorted. Normally when a plant goes down, that is negative for live animal prices because it reduces near-term demand for animals. However, in this case, the opposite seems to have happened. This plant probably draws hogs mostly out of the Iowa-S. Minnesota region, which overlaps with the Western Corn Belt region. Both regions saw negotiated hog prices spike. I guess it is possible that Tyson had to add a shift at one or more other plants in order to handle the influx from Madison and maybe they needed extra negotiated hogs to round out that kill. Or, it could just be that time of year when hog supplies start to tighten and prices rise. The cutout stayed stuck in the $78s up until Friday when it printed a little over $81, so it doesn’t look like the strong draw in the negotiated market is being driven by unusual strength in the pork market. Pork packer margins will definitely come under pressure next week as the gains in the negotiated market get fully reflected in the LHI. It looks to me like it could rise to $74/cwt. by mid-week and that is without any additional strength in cash hogs or the cutout. We really shouldn’t be surprised that the futures market reacted with a sharp increase because spec longs were carrying a huge short position and this market has been beaten down for so long that just a glimmer of good news was all it needed to trigger the bullish reaction. I calculate this week’s packer margin at $11.70/head, but that will likely shrink to $5-6/head next week. There were also some interesting things happening with the kill this week. Total slaughter came in at 2.39 million head and that was fairly close to what the pig crop implied. The Saturday kill was small at only 47,000 head. However, packers seem to be planning on a very large Saturday kill next week that could drive the weekly total up to 2.48 million head. If they go ahead with that kill it would be huge for the first week in May. So there seems to be some juggling of hogs going on, which may or may not have any relation to the plant closure. All through the spring we have noted how hog kills have been coming in larger than expected, but I guess that wasn’t going to last forever. So maybe now the supply side of the hog market is looking a bit more bullish than it has recently. Producer hog weights have started to decline in the daily MPR data, but hasn’t yet showed up in the delayed FI data. It is definitely time for the normal seasonal downtrend in hog weights to materialize. If recent Hogs & Pigs surveys are correct, we should expect hog supplies this summer to be about 0.5% larger than last year. Carcass weights should run a little below last year, if they remain on their current trajectory, so the two effects may offset and give us pork production this summer very close to what we had last year. The demand side is likely to be more subdued this year compared to last. Just to give you a sense of how much worse pork demand is this year, consider that the average demand index from Jan-Apr was 1.065 last year and this year in those same months it is 0.926. If that continues into summer, we can expect pricing well below last year’s strong market. The bellies remain a drag on the cutout and that will likely be the case in May also. All of the other primals posted modest gains this week, so that is a good sign. Will packers be able to force the cutout higher in response to the stronger cash hog market? I’m not so sure. In the cattle and beef complex, it is fairly common for packers to have success raising the cutout whenever their cattle costs increase. We just saw a good example of that in recent weeks. In the hog and pork complex however, it seems that more often the direction of causality flows the other way, with changes in the cutout resulting in commiserate changes in hog pricing. One reason for that is that a lot of hog pricing formulas have a lagged component tied to the cutout and the fact that such a tiny percentage of all hog prices are actually negotiated (thus giving packers a greater ability to move cash hog prices as they see fit). But there are always exceptions to those general observations and if hog prices were going to drive changes in the cutout it would most likely happen in the spring and summer when hog numbers are the tightest. It will be interesting to watch what happens to the cutout next week. This week’s export data for pork looked stronger and that is a welcome development. Apparently, low pricing has attracted the interest of international buyers. So, as the calendar turns toward May, maybe we are leaving the weak pricing environment that has persisted for months and heading for better days ahead. I’m sure hog producers hope so because there margins continue to run deep in the red. Next week, watch for changes in the deliveries scheduled for Saturday, since a big Saturday could end up producing a lot of pork for expiration week in the May futures. Also watch the relationship between prices in the negotiated hog market and the pork cutout.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}