Pork Wrap April 26

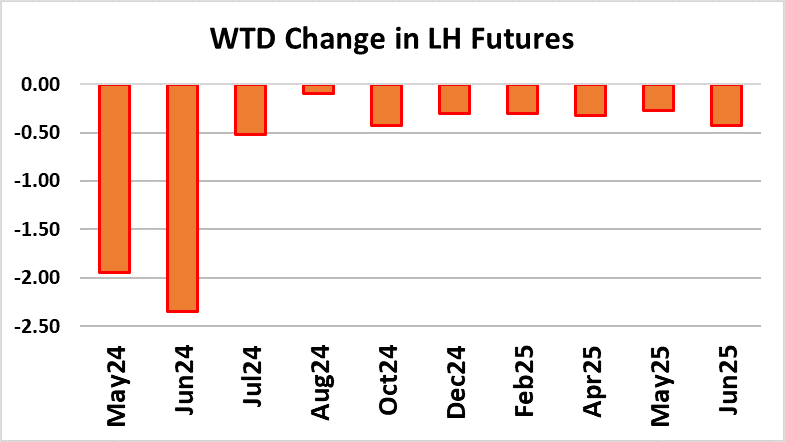

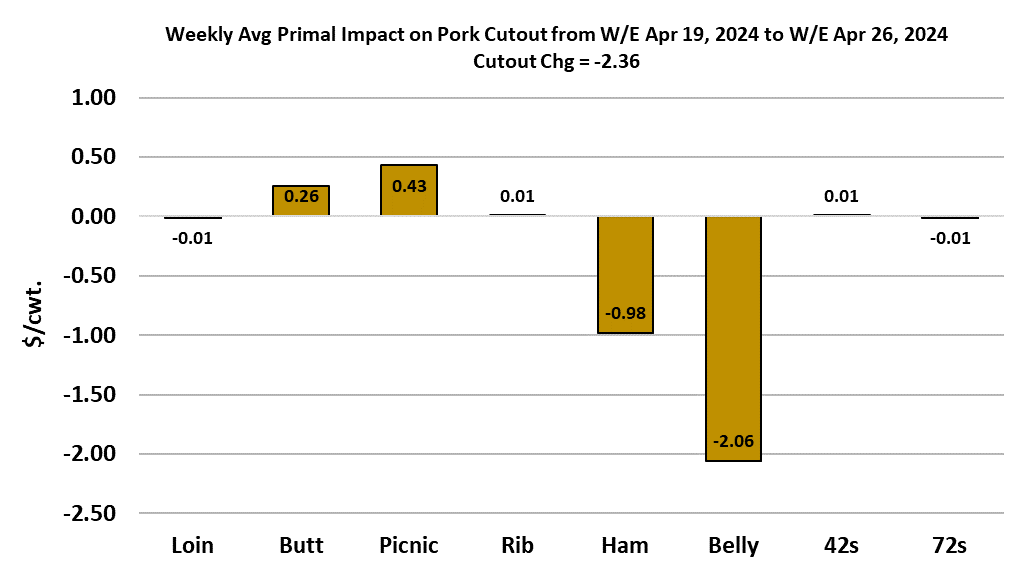

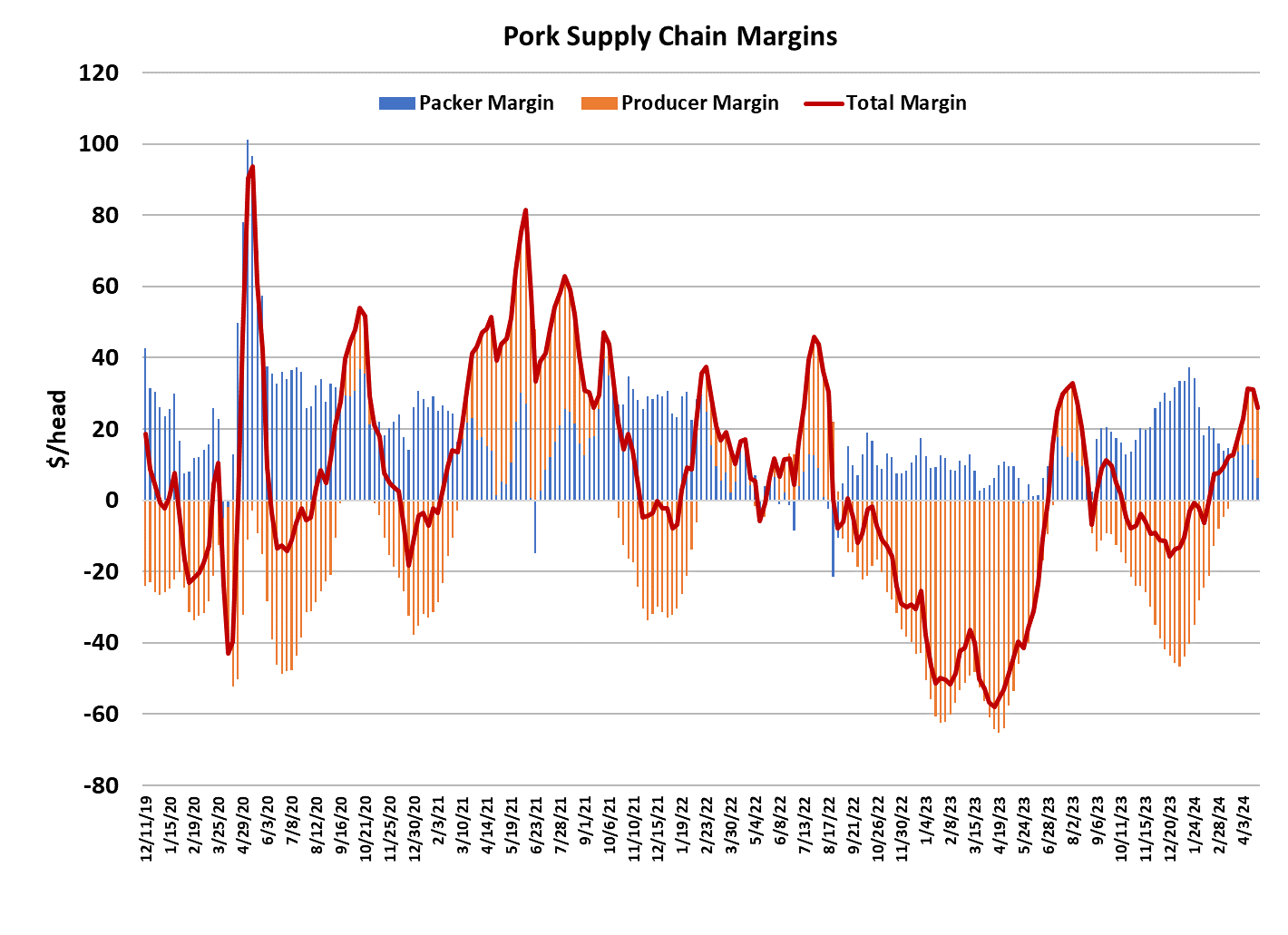

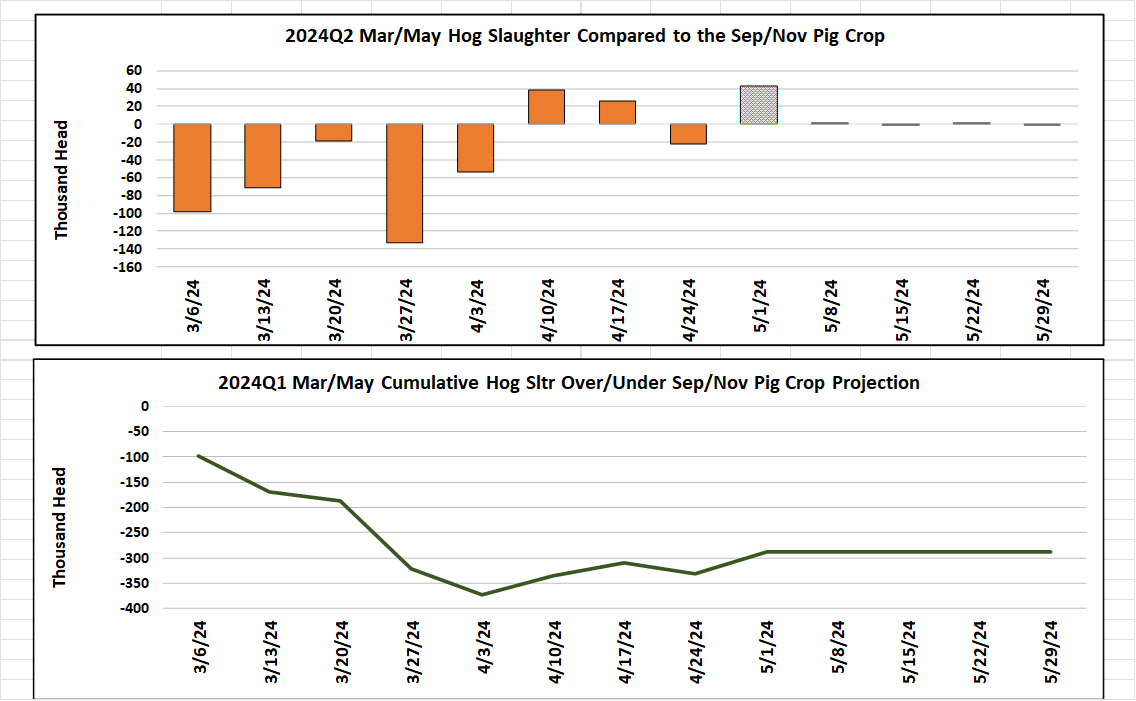

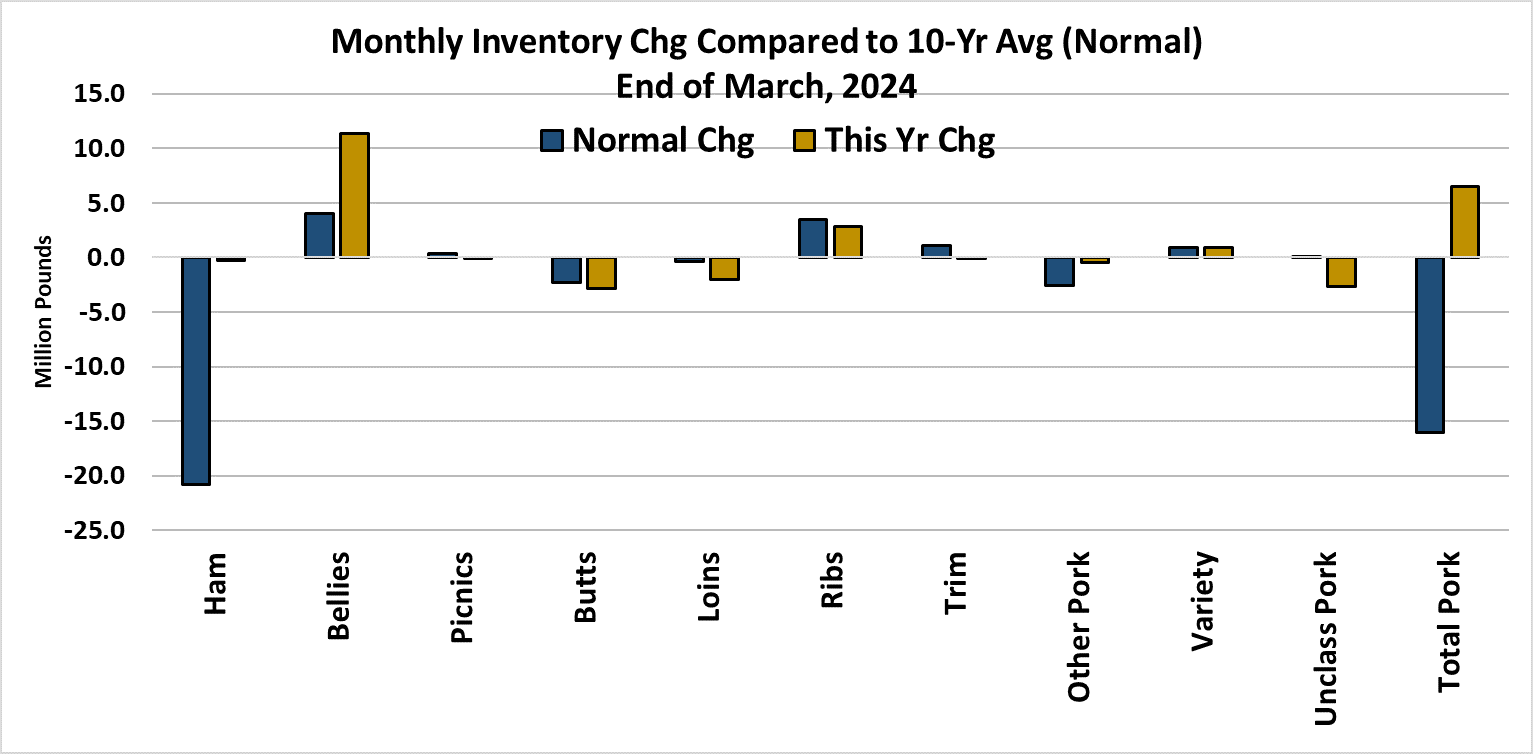

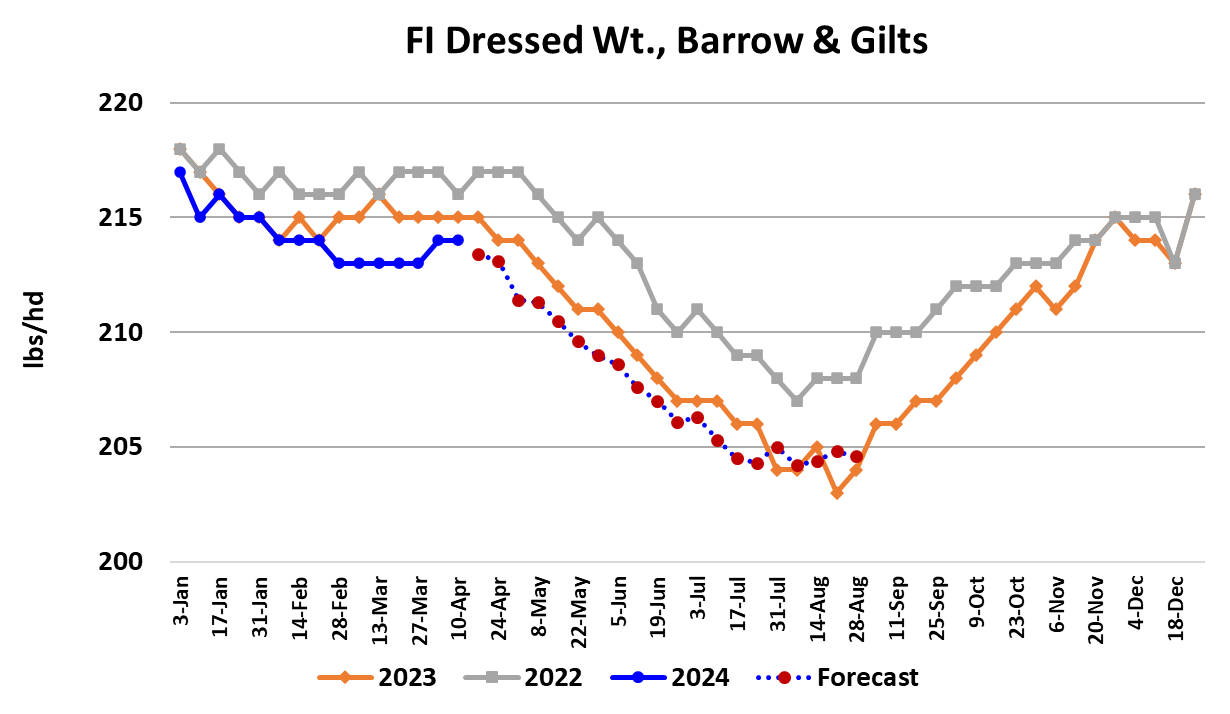

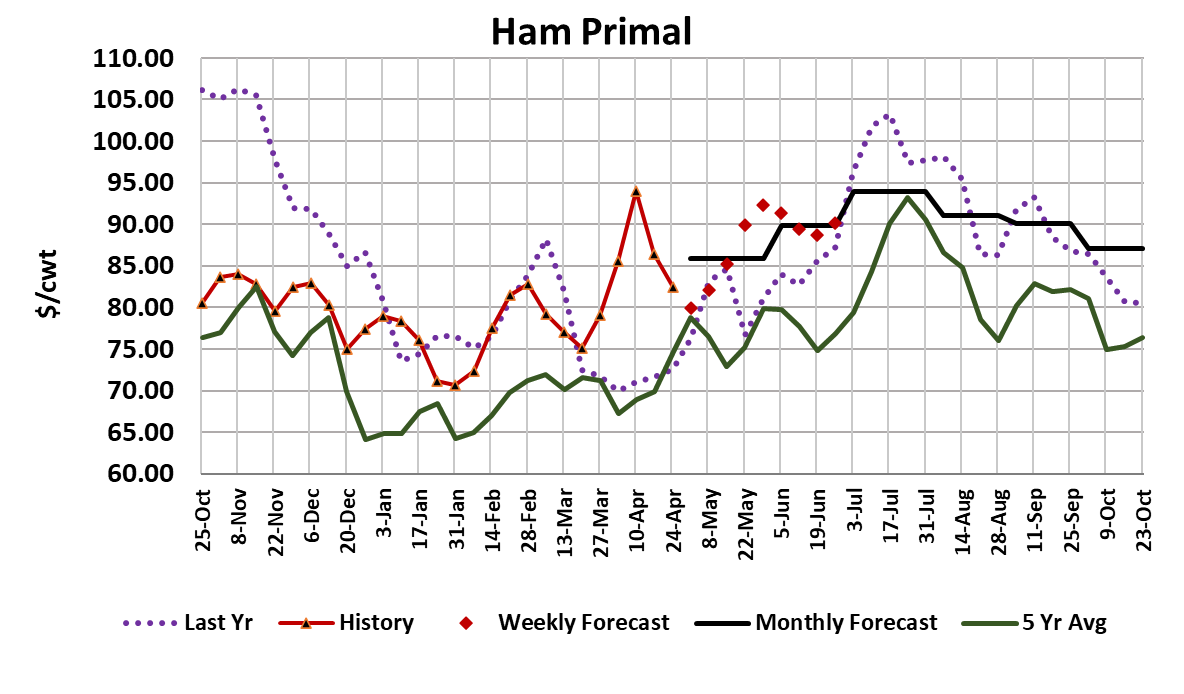

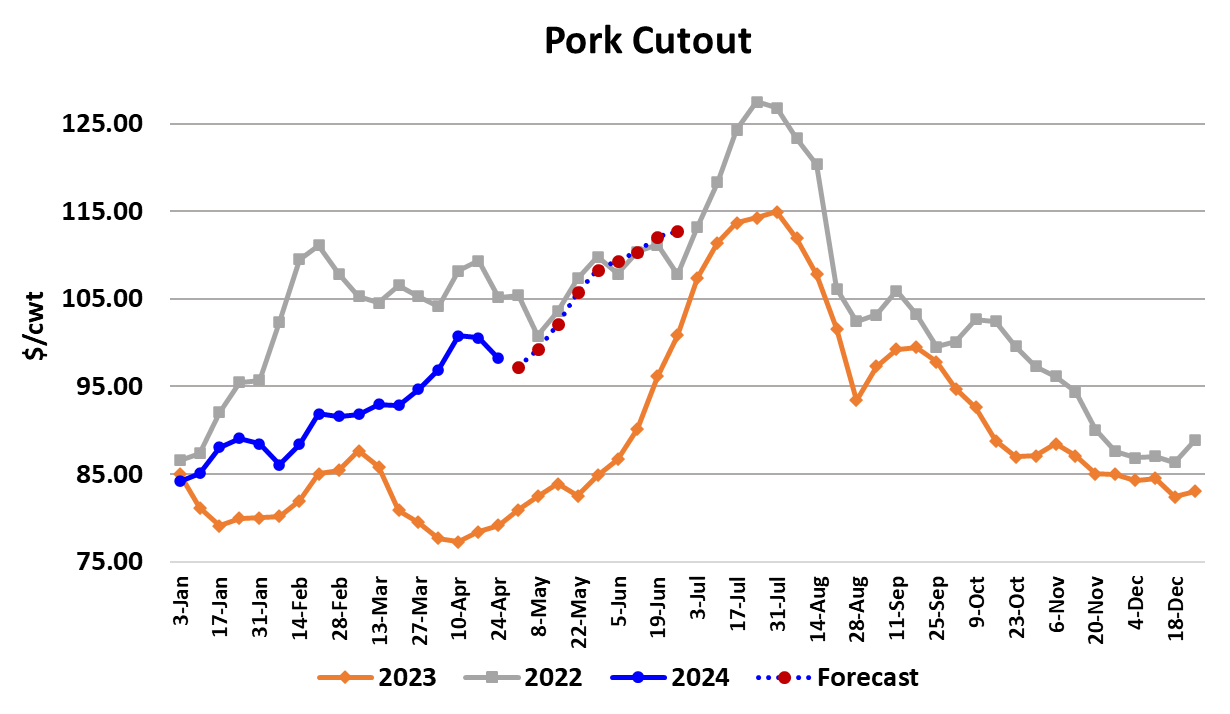

Last week, I talked about how the hog and pork complex had taken a breather following the Apr futures expiration and this week that breather turned into a full-on nap. The pork cutout dropped $2.36/cwt. to average $98.19. At the same time, the negotiated hog markets moved a little higher, with the WCB adding $1.93/cwt. on a weekly average basis. The LHI was nearly unchanged and that, combined with the drop in the cutout, caused packer margins to plunge down close to $6/head after averaging nearly $12/head the week before. In response, packers slashed the Saturday kill down to nearly nothing (only 4,000 head), causing weekly slaughter to total only 2.38 million head, down 100k from the week prior. The downturn in the cutout came at an inopportune time for futures bulls, who had blindly run the May contract up close to $99 on Tuesday. Now, suddenly faced with a declining cutout and the LHI poised to move lower, traders reversed course and sold the board hard in the final three sessions of the week. Of course, the big question on everyone’s mind is whether or not this is the beginning of period of softer pricing that might run for several weeks. That is possible, but I wouldn’t expect a long run lower simply because kills will be shrinking seasonally over the next couple of months and weights will be coming down at the same time. That said, the combined margin has now made a substantial move lower after trending mostly higher for the better part of four months. Could this be the beginning of a demand air pocket? Maybe, but its not likely at this time of year. I think the problem lies in the fact that both hams and bellies went into softening mode at the same time. The hams probably have another week or so where prices are vulnerable and after that I’d expect the smaller kills to lift them higher. The bellies, on the other hand, look like they could be in for a sustained period of weakness. This week’s cold storage data showed a larger-than-normal build in bellies during March and belly inventories are very close to where they were this time last year when belly prices were struggling. It’s hard to imagine that bellies have a lot of downside price risk from current low levels, but they may be slow to rise also. As a result, the near-term price forecast for bellies was lowered this week. Another concerning feature this week was sideways movement in the loins and ribs. Up until this point, we were able to consistently count on prices for the retail items grinding higher, but now that is being called into question. Of course, seasonally smaller production can help paper over any demand side weakness, so I don’t expect the cutout to retreat much further. The fundamental forecast has it holding in the high $90s for a couple of weeks before moving back over $100 with the help of improving ham prices. By eliminating the Saturday kill this week, packers may be trying to cool off the negotiated hog market and my guess is that they will succeed, at least for a little while. It is worth noting that, while the kill did come down a lot this week, it was still only modestly under what the pig crop projected. Further, hog weights are suggesting that producers are current on their marketings, so there is little risk of backing hogs up in the pipeline. Barrow and gilt carcass weights held steady at 214 pounds in this week’s FI data and should be very close to starting their seasonal downturn. The early data suggest that packers intend on another very small Saturday kill next week. Pork exports continue to look good in the weekly data, with China being the only major destination that is showing large YOY declines. In fact, strong exports may keep domestic pork availability slightly below last year this summer, even though overall pork production is expected to be higher YOY. In short, it was probably unreasonable to expect hog and pork prices to rise from January to the summer top without one or two soft patches along the way. This week was one of those soft patches, but I don’t expect it to be the start of an extended downturn. Next week, watch both hams and bellies. If they both remain under pressure then we should expect the cutout to lose a little more ground and cash hog markets to soften a little. Expect another small kill and perhaps an easing in carcass weights. The May futures expire two weeks from Tuesday and under these conditions it is going to be very difficult to get the LHI much above $92-93 before it rolls off the board.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}