Pork Wrap April 23

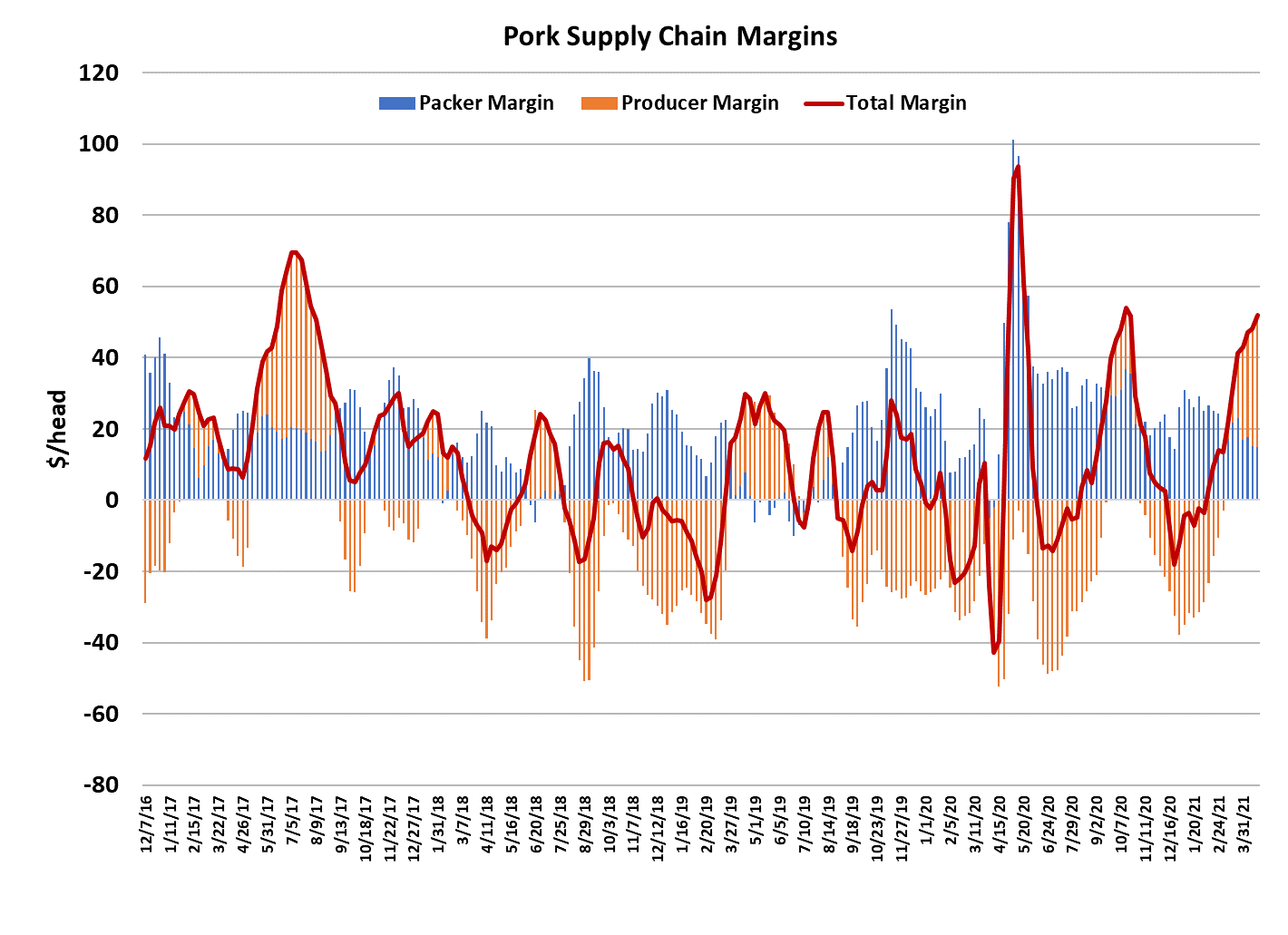

As usual, both pork prices and hog prices moved higher this week.

The cutout was up $2.25 on a weekly average basis while the WCB

negotiated market was almost $6 higher. That was enough to

move packer margins down below $15/hd and those margins will

get even smaller next week when the full brunt of the cutout and

WCB advance is registered in the Lean Hog Index.

On the supply side, there wasn’t really very much unusual about

this week. Barrow and gilt carcass weights held at 215, which is

where they have been for the past 9 weeks now. The weekly kill

totaled 2.47 million head, which is right on schedule with where the

Sep/Nov pig crop indicated. Corn prices surged higher this week,

with the May contract now over $6.50/bu. That is starting to eat into

producer margins by raising their cost of gain, but the cash hog

price is rising even faster, so I doubt many hog producers are

overly concerned about high corn prices right now. That will

change quickly if the cash hog markets ever stop going up. The

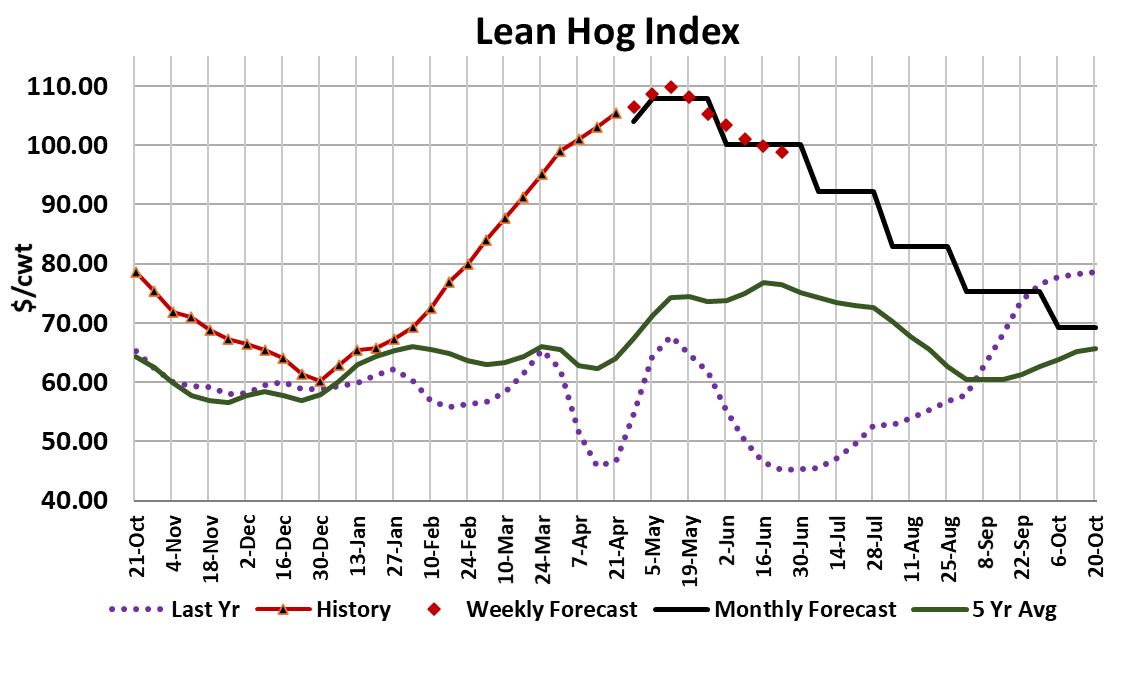

seasonal tightening in hog supplies is becoming evident now.

Negotiated hogs in the WCB market sold for almost $113 today.

That is the highest price on record outside of the spring of 2014,

when the PEDv outbreak sent hog prices briefly into the $125-30

range. Packer margins are compressing.

As supplies get smaller between now and early July, a real margin

risk exists for packers if the cutout ever stops going up because

they might not have enough leverage to pressure the cash hog

market lower and preserve their margin. Right now I’ve got packer

margins going slightly negative in July and averaging a little less

than $5 per head in June. That assumes the cutout comes down

some, but not a lot, from current levels. Outside of the crazy period

last spring when COVID was disrupting the industry, packer

margins haven’t been in single digits for almost 2 years.

Producers, on the other hand, are enjoying astounding margins

over $35/hd, so you can see why high corn prices are not a huge

issue for them at the moment. The combined margin continued

higher again this week and is now challenging the top that it made

last fall in that very strong demand cycle. My guess is that the

current cycle is going to shoot way beyond last fall’s peak and

remain very elevated for weeks or even months. I really don’t know

what else to say about the demand side of this market other than it

seems to be originating with domestic consumers and is

extraordinarily strong.

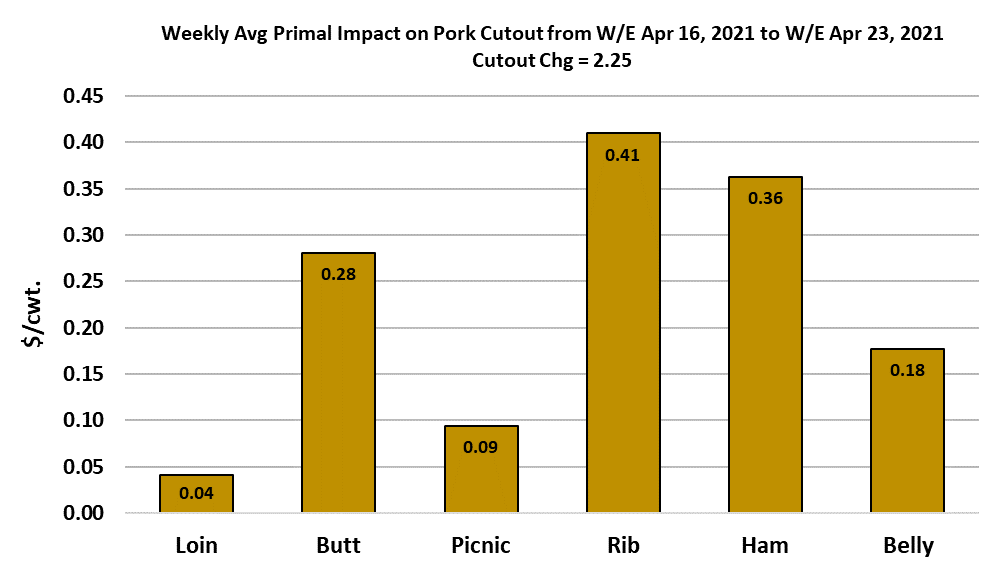

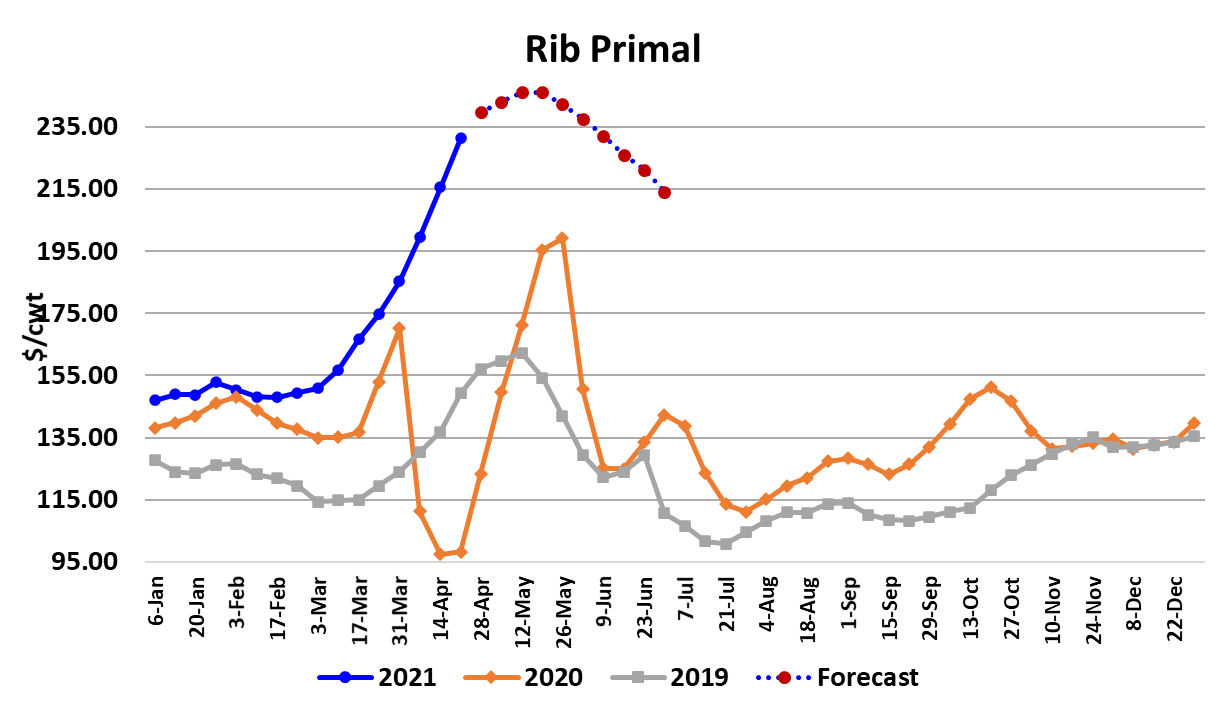

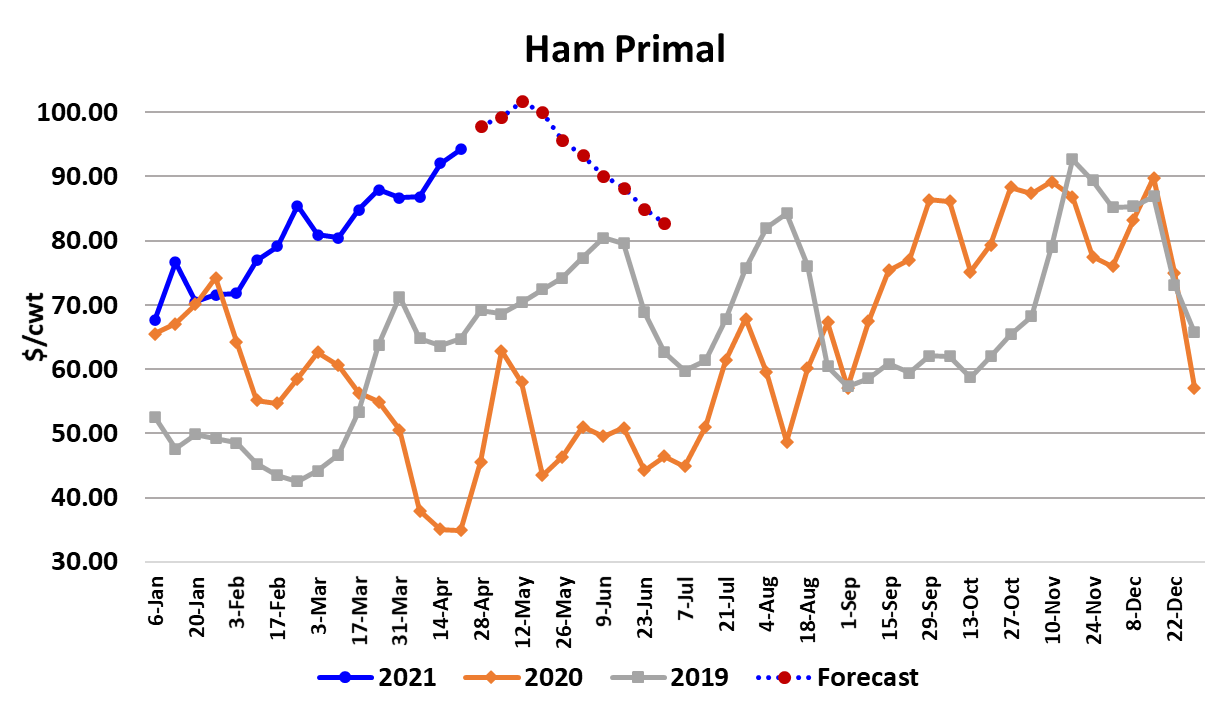

The chart below indicates that all of the primals were higher

this week on an average basis, with the ribs and hams leading

the way. Ribs I can understand because there are a lot of

those used in foodservice applications and that sector is

rebuilding inventories. Plus they are a favorite retail feature

items across the Southern US in the spring. The persistent

strength in hams however, is a bit perplexing. The 23/27 lb

hams averaged almost $92.50 today, which is extremely high

for a bone-in ham at this time of year.

Of course, cold storage stocks of pork in general are well

below normal levels. This week USDA reported total pork in

cold storage at the end of March was down 27% from last

year. Hams in cold storage are down 31% and belly stocks

are 55% lower than last year. Those low stocks are forcing

some buyers into the spot market that would normally be

drawing from the freezer in spring and summer, so it is very

much price-enhancing. Bellies showed a little softness toward

the end of the week, but with stocks so low, I really don’t

expect belly prices to drop sharply anytime soon. That

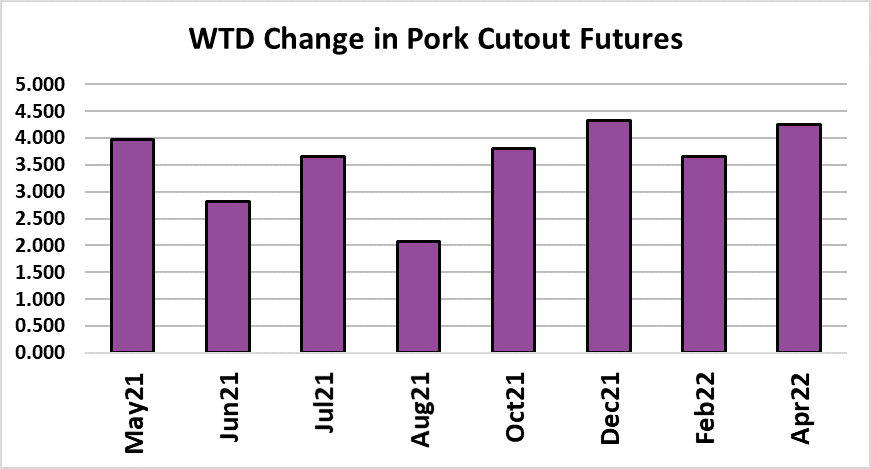

probably means that the cutout doesn’t fall apart either and so

buyers had better get used to paying a lot more for pork than

they are accustomed to.

The real danger, as I see it, is that demand stays superelevated right into July when hog supplies are shrinking

seasonally. In that scenario, it wouldn’t be all that surprising to

see the cutout and cash hog prices both top $125. The

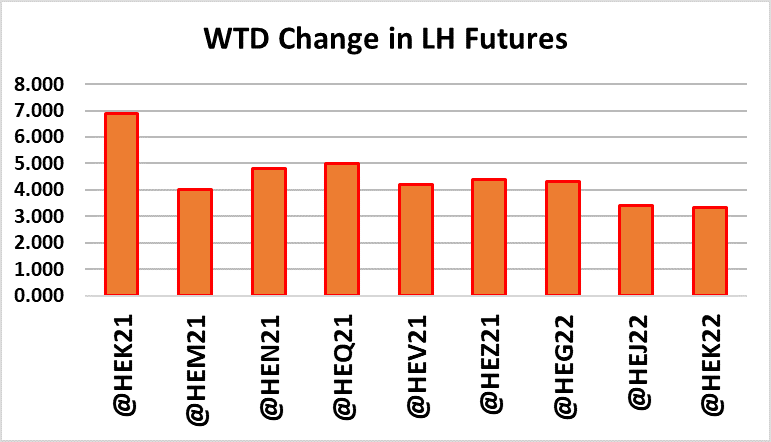

futures bulls would have a heyday with that. Those bulls are

already having an extended party, particularly those that

adhere to the front of the curve where the rising cash markets

have forced the futures higher and higher. The May contract

set a life-of-contract high today at $109.45. I will say that the

futures are very jumpy and volatile at these high levels. Any

little hitch in a daily cutout print seems to send the futures

down several dollars, particularly the Jun contract. Next week

watch for further advances in the cutout and negotiated hog

market as a sign that this rally still has life. My guess is that it

does.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}