Pork Wrap April 22

Last week, I said it was important that we see the cutout hold on to its

gains. It managed to do that this week, but it didn’t add very much.

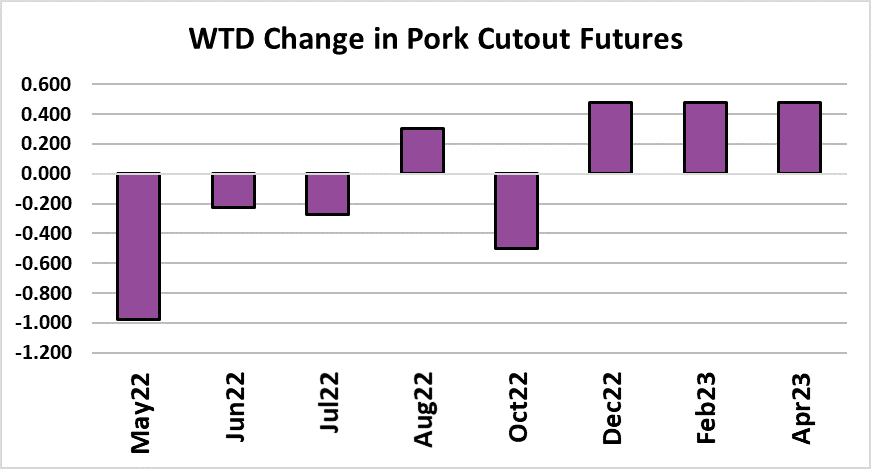

The cutout was up $1.10 on a weekly average basis and the attached

chart shows that all of the primals contributed a little bit to this result.

That type of pattern, where all of the primals rise by a similar amount,

makes me think that the gains were more a result of the holiday shortened kill last week (and Monday of this week), rather than any significant improvement in demand. The fact that neither the hams or the bellies moved lower this week is a positive, but it certainly isn’t a rapidly-improving demand environment. The combined margin was essentially flat this week, which further attests to how weak the demand gains were. A big question in my mind is what happens to the cutout as supply returns to normal. Packers killed an estimated 114,000 head this Saturday compared to only 8,000 last Saturday. That will refill the product pipeline early next week and it will be interesting to see if product pricing can continue higher when packers have more meat to sell.

This week’s total kill came to 2.37 million head, but that number

includes a very weak Monday kill of only 353,000 head. This Monday’s

kill should be a lot bigger and could push the weekly total back over 2.4

million head. Seasonally, demand should be improving as grilling

season takes hold, but I’m concerned that given the high level of prices

already, that further gains might be hard to come by. The beef cutouts

seem to be faltering right in the sweet spot of the calendar for beef

demand and that makes me wonder if beef is just the “canary in the

coal mine” for pork and eventually pork demand will meet the same

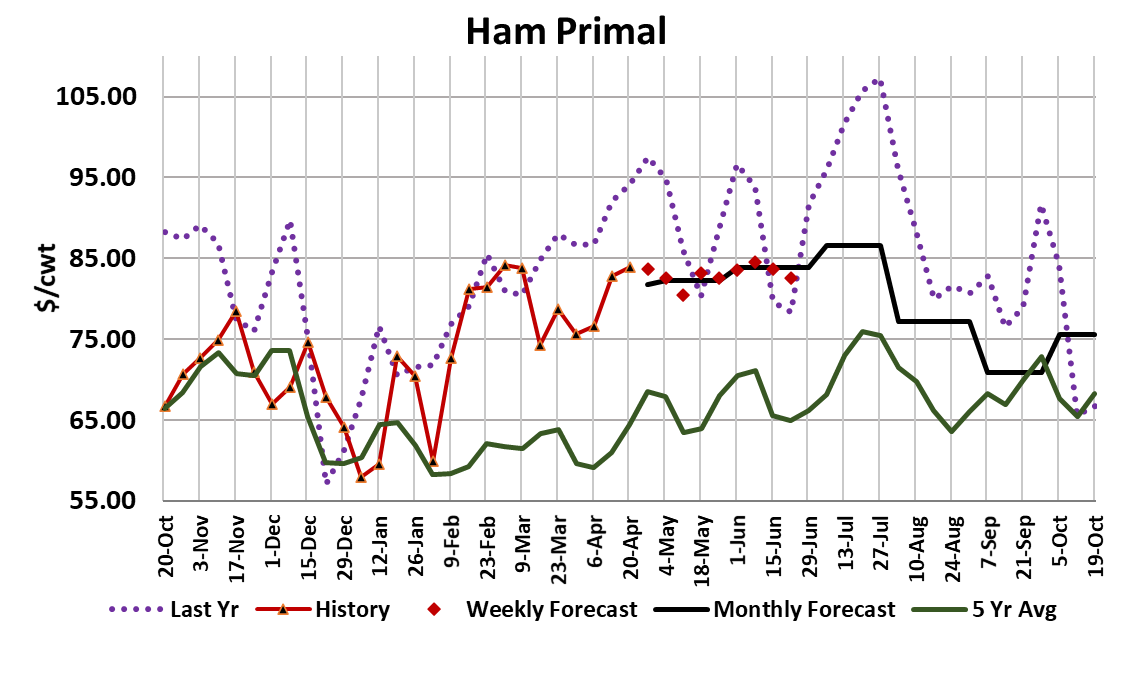

fate. Hams have already advanced further than I thought they would

this spring, so that is one primal that I’m concerned about. Bellies are

another, but the big rallies in bellies normally are driven by aggressive

retail bacon features and I don’t think we are going to see consumers

respond very strongly to retail bacon features this spring and summer.

Instead, consumers will get their bacon on sandwiches at fast food

outlets or off the buffet at the hotel while they are traveling.

Cooking bacon at home is probably not a high priority for consumers

who have finally been set free from pandemic restrictions. That said,

prices could continue to work higher without a big demand boost,

simply on the back of shrinking pork production over the next couple of

months. However, in order to get pork prices rocketing higher, we

would need to see a boost from the demand side as well. And that is

the part that I think futures traders are missing. They have been

pricing the summer contracts like the cutout is just going to rocket

higher (a la 2021), but without a strong demand surge we may only see

moderate price increases this summer that look more ordinary that

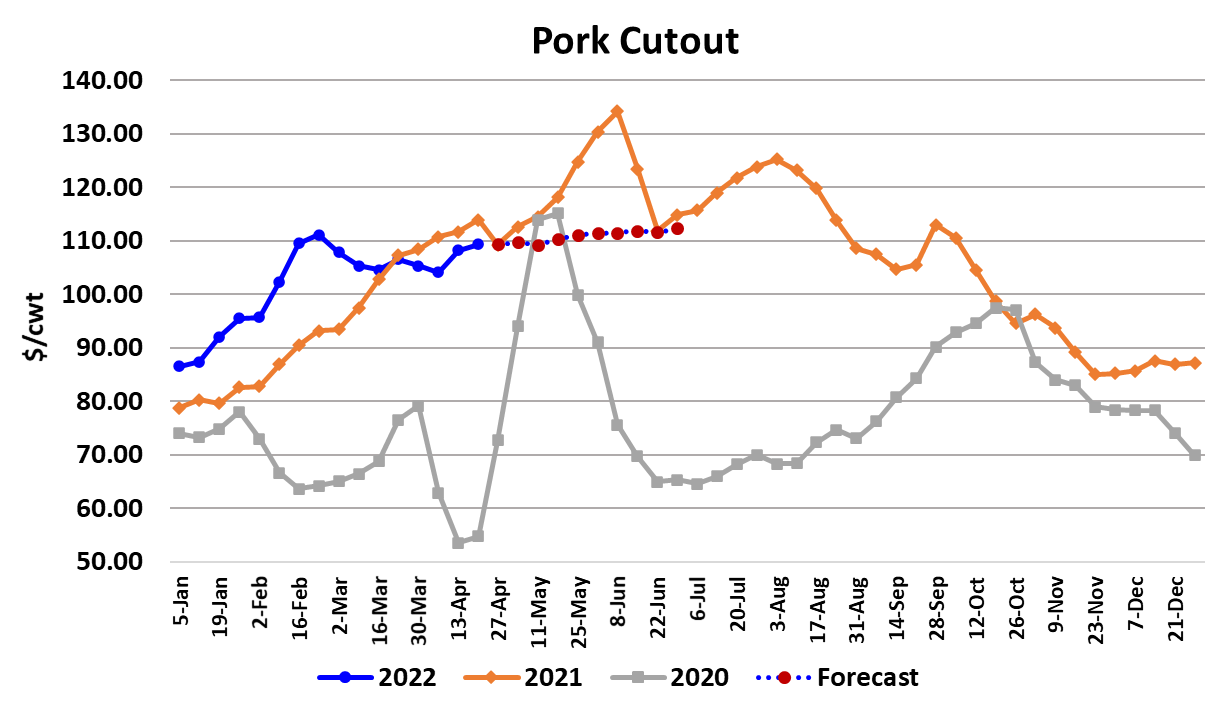

exceptional. A case in point is the May futures, which was trading near

$116 on Tuesday of this week when the LHI was only at $101, implying

a $15 increase in the LHI over the three weeks remaining in that

contract’s life.

That kind of a rally has happened before, but only under

exceptional circumstances that I just don’t think exist right now.

Eventually, traders did a re-think and the May contract finished the

week below $112. That is still probably out of reach. I have fair

value for May expiration at around $106, although I could concede

a couple dollars above that. The negotiated cash hog markets

were interesting this week. They got off to a fast start with the

WCB price printing $108 on Tuesday after finishing the week

before at $100. However, that didn’t hold and by Friday afternoon

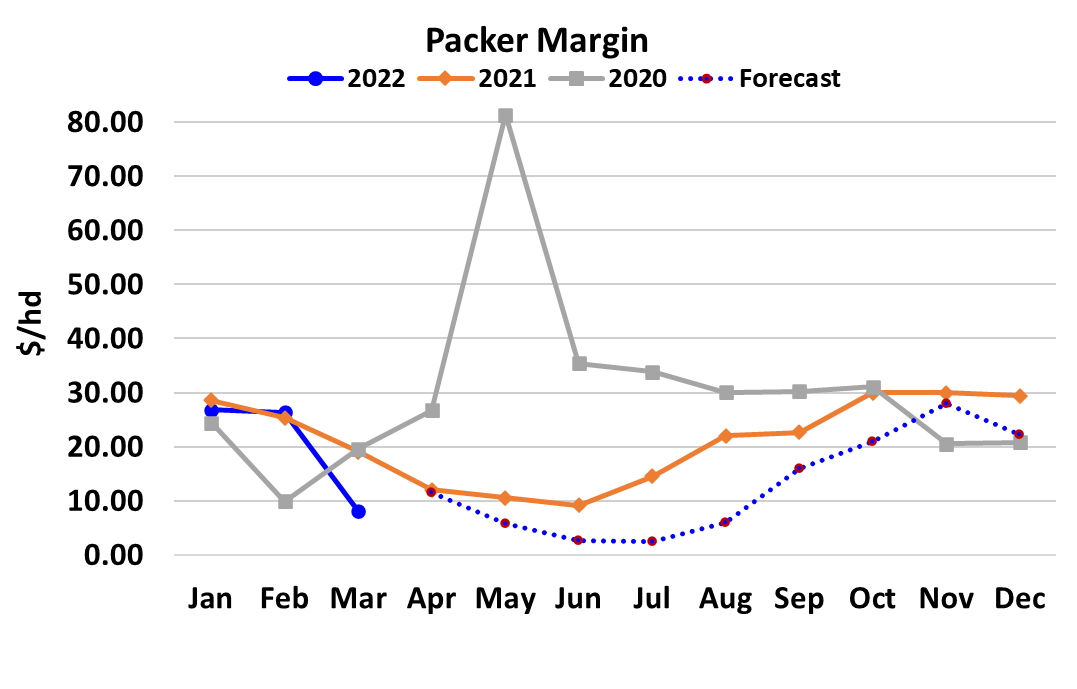

the WCB was quoted at $103.72. On a weekly average basis, the

cash markets were higher, with the WCB up $4.81 and the NDD

quote up $3.06. That just about offset the gain in the cutout, so

margins were unchanged at $16/head. By early next week, the LHI

will register more of the negotiated gains and thus I’d look for next

week’s margins to be closer to $10/head unless the cutout makes a

surprising jump. That brings up another point.

For the LHI to escalate as rapidly as the May and Jun contracts

want to imply, it is almost imperative to have a rapidly rising

negotiated cash market and I don’t sense that at present. There

seems to be some goofiness going on in the WCB, where it will

print sharply higher prices for a day or two and then pull back.

Some have suggested that one packer in that region lost more of its

own hogs than normal to disease this spring and thus have been

forced to be more aggressive in the spot market. When that packer

is in the market, prices jump and when it is out of the market, prices

fall back. That makes for a lot of volatility in the WCB price, but it

isn’t the type of situation that is going to drive negotiated prices

higher each and every day as would be needed to move the LHI

rapidly higher. The attached chart gives the change in the LHI from

the third week in March to the third week in April. This year, that

change has been very near zero.

There have been some years when the index was moving quickly

higher, but this doesn’t seem to be one of them. I suspect that

traders are remembering last year’s move and expecting that

to repeat this year. The weekly export data looked pretty soft

again this week and that is another headwind that the market is

facing this spring that it didn’t have to deal with last year when

exports were actually a pretty strong tailwind. Carcass

weights were reported steady this week and seem to be behaving

normally, so I don’t have any concerns about the supply pipeline at

this point. In all, I think this is shaping up to be a rather

sedate spring and early summer hog and pork market.

Moderate price gains are likely as hog supplies tighten seasonally,

but the risk of a runaway market to the upside seems limited.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}