Pork Wrap April 21

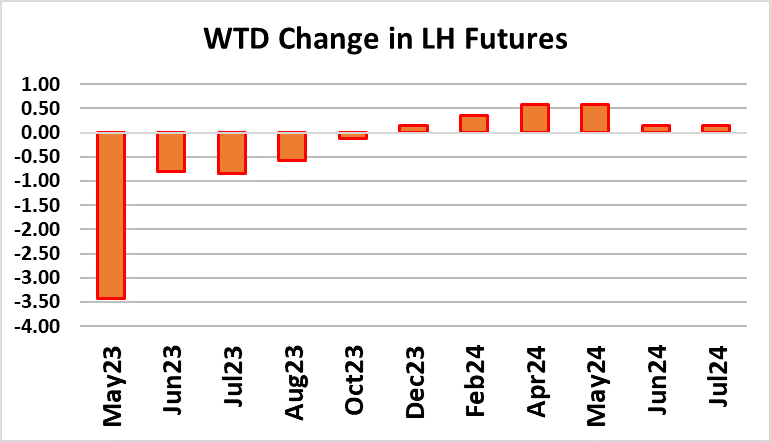

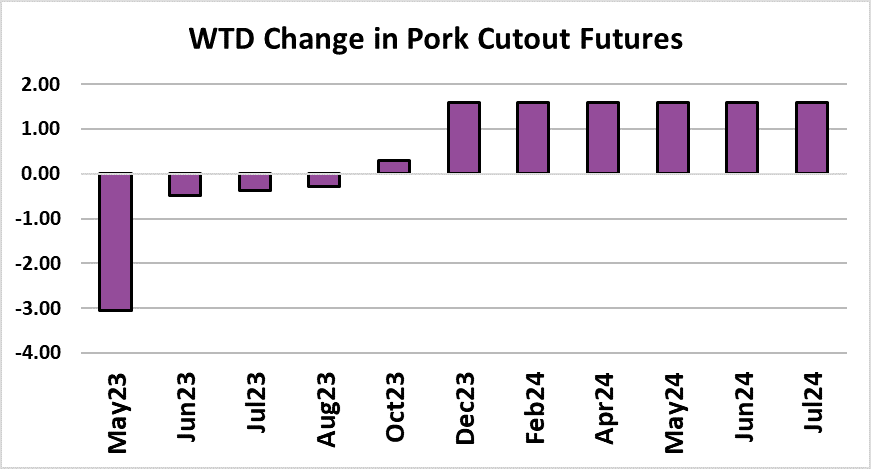

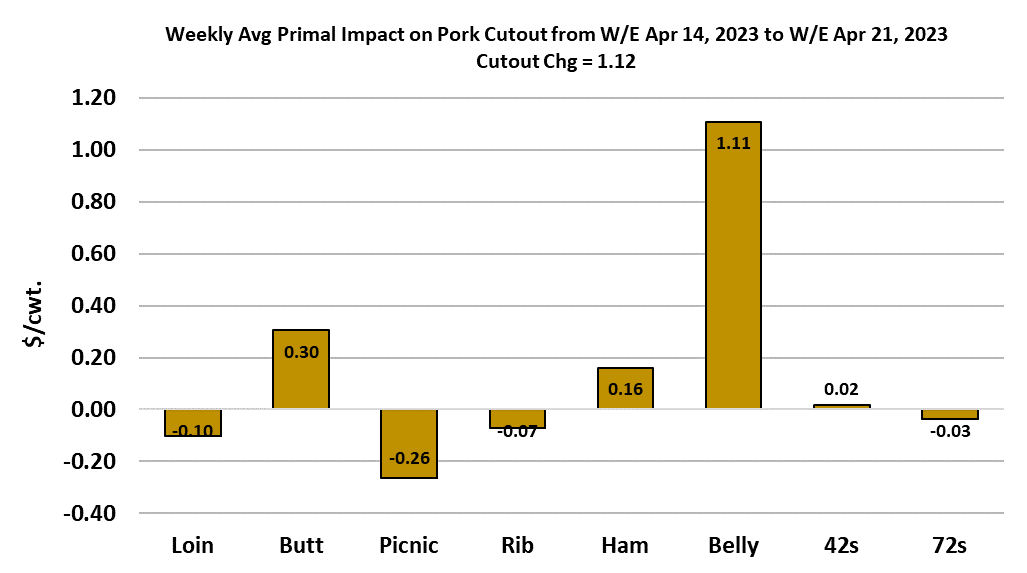

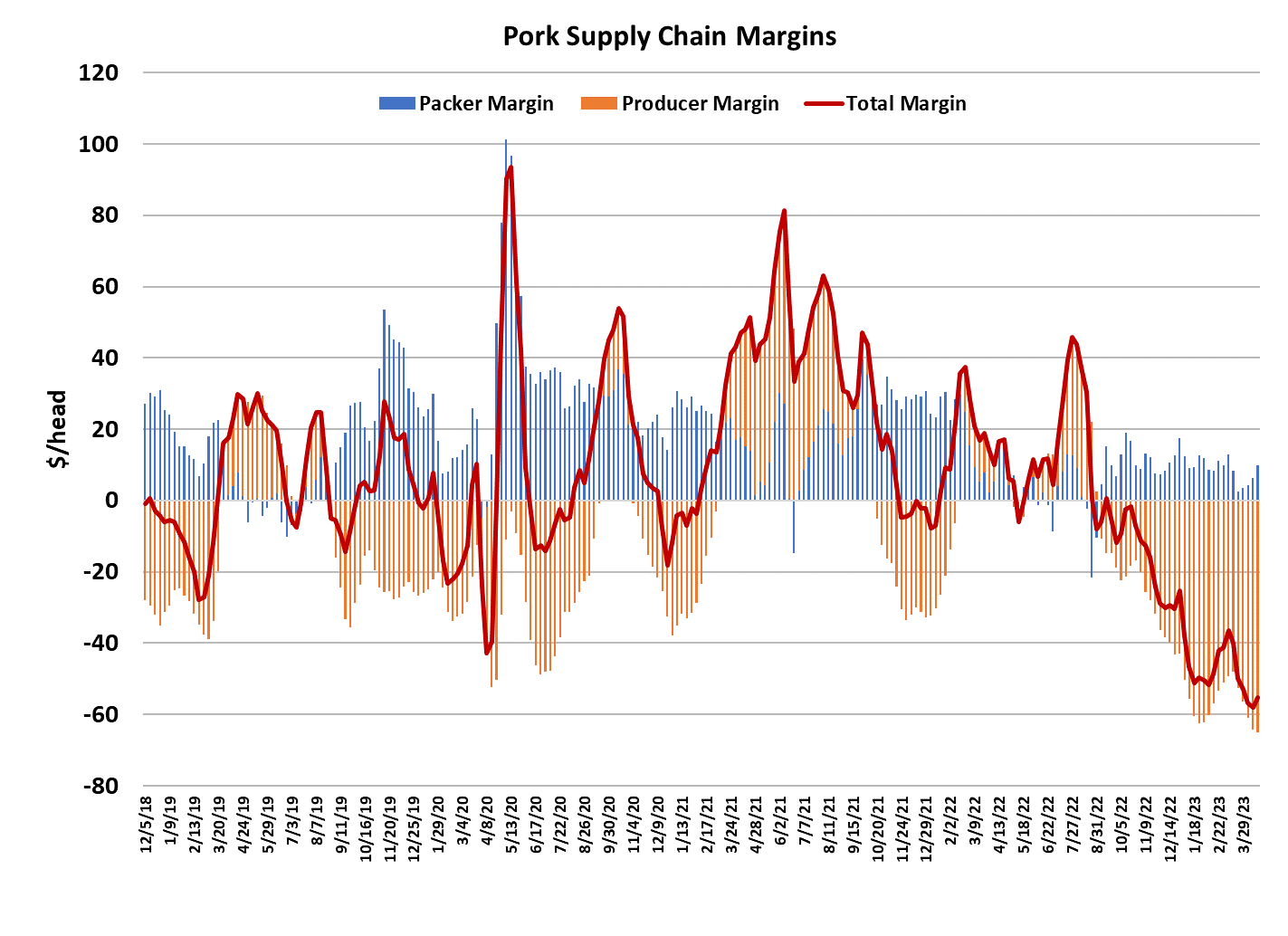

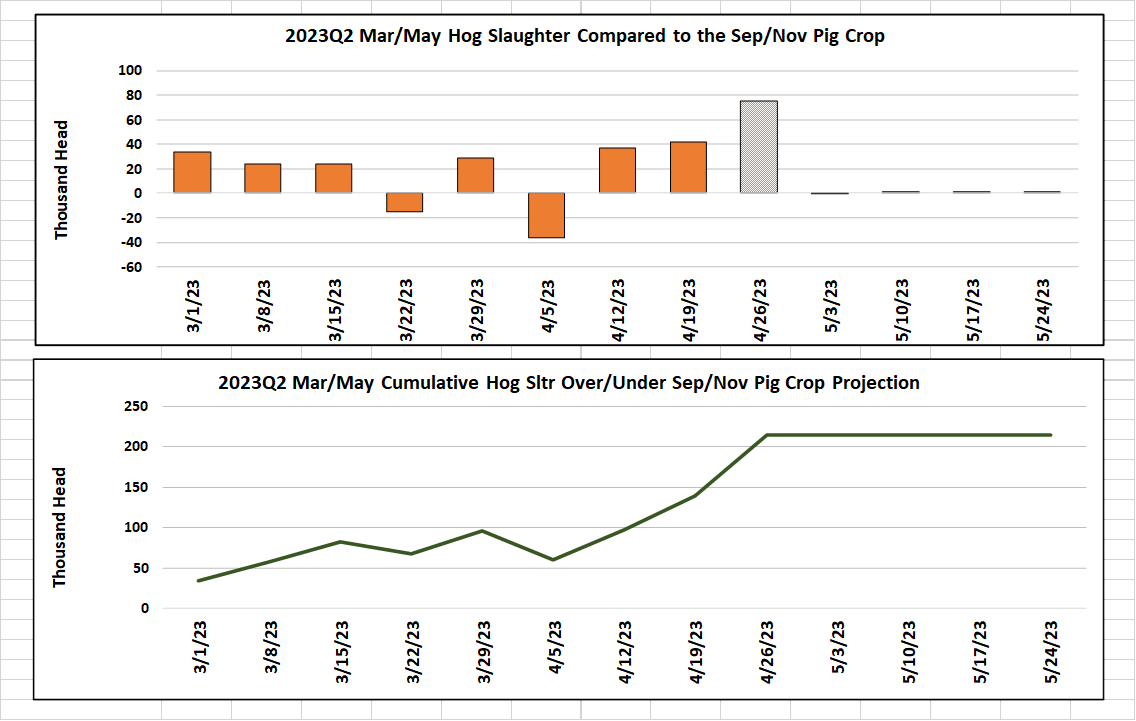

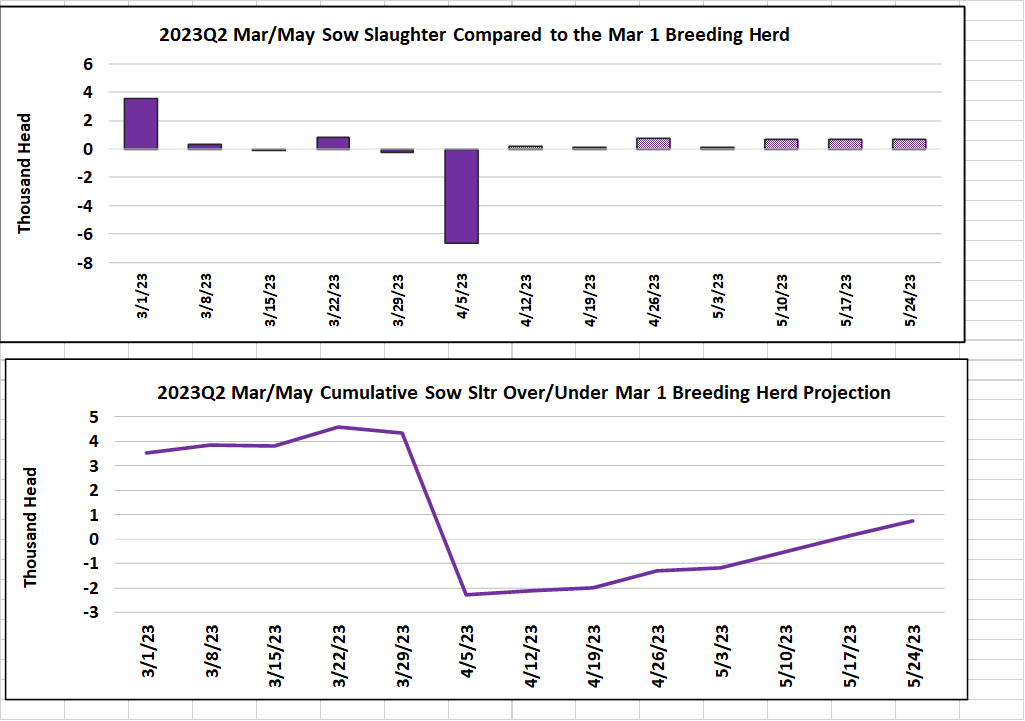

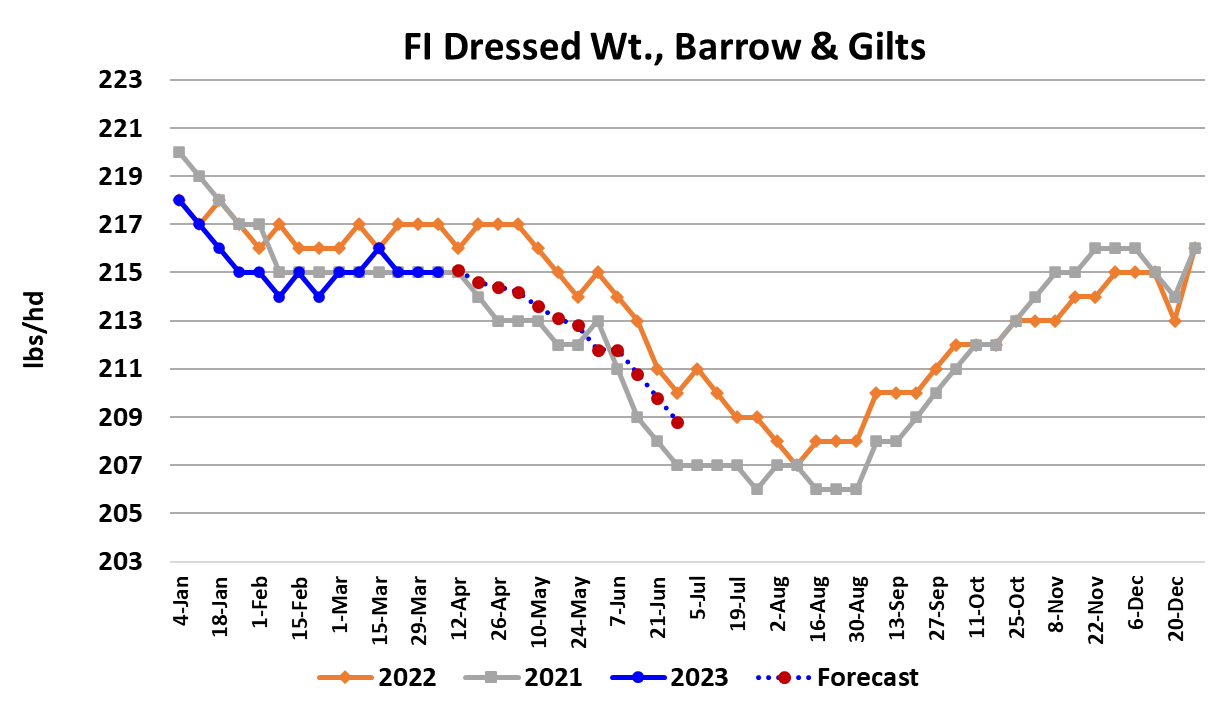

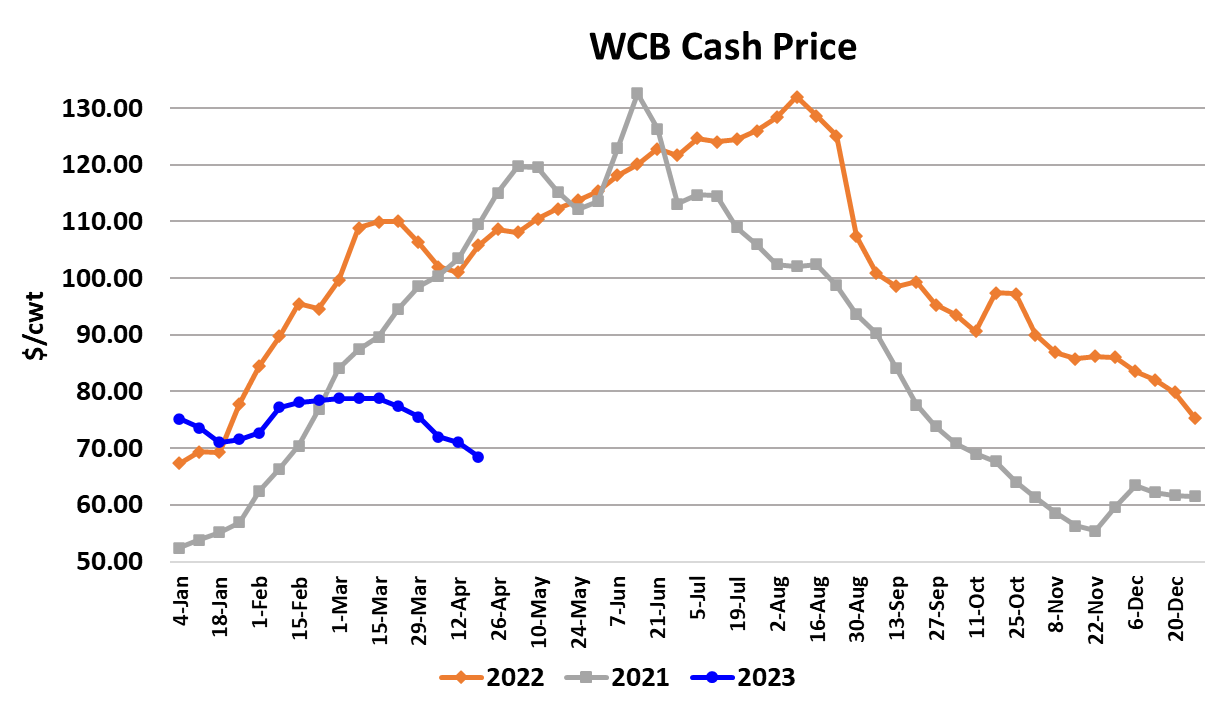

This week, cash hog prices continued to track lower, with the WCB negotiated market losing $2.57/cwt. on a weekly average basis. Clearly, the supply of market-ready hogs has not tightened up much and that has provided packers with leverage to keep hog prices on the defensive. The cutout was up $1.12/cwt. this week, so that, combined with a declining cash hog market helped packer margins improve to almost $10/head. That isn’t an unusually large margin for this time of year, but it is stronger than what we expected a few months back. The headline story so far this year in the hog and pork complex has to be larger-than-expected hog supplies. This week’s kill totaled 2.46 million head, up 70k from the holiday-reduced kill the week before. Next week’s kill is also likely to be close to 2.45 million head. Summer can’t come soon enough for hog producers, who are currently losing about $65/head on every animal they produce. That has kept them motivated to keep hogs moving out the door just as soon as they are ready. Breakevens are still in the $100-103/cwt. range and that high breakeven will probably persist right through May. The summer futures contracts are telling producers that the best they can expect for their hogs this summer is something in the high $80s, so that means the red ink could continue for many months to come. Carcass weights are still treading water in a sideways pattern, but soon we should start to see some seasonal weight declines. However, the weather forecast over the next couple of weeks in the Midwest calls for unseasonably cool temperatures, so that could delay the start of the spring weight declines by a couple of weeks. The market just hasn’t been able to digest all of the pork that is being produced without lower prices. At some point that will change and the market will start to move higher, but it may be a very gradual grind higher, much like the market has been grinding lower by $1-2 per week for months now. The week, the bellies were the biggest supporter in the cutout, but I don’t get the sense that they are about to launch higher. Cold storage stocks of bellies are still very high and that is likely to temper the upside potential in bellies for most of the summer. The thing that concerns me most at present is the trim markets, which continue trade lower. Normally, at this time of year, hot dog manufacturing is ramping up ahead of baseball season and that generally supports trim pricing, but this year it has been mostly lower in trim pricing since late February. The difference in pricing between pork trim and beef trim is stark—beef 50s are in the stratosphere and pork trims seem to be headed for the basement. I take this as an ominous sign for demand in the next few weeks and thus am not building in very big increases in the cutout over the near term. If that comes true, it could be a real problem for the May and Jun futures, which are still at elevated levels that suggest the cutout is suddenly going to start tacking on $3-4 per week consistently. Maybe in June, but I don’t see it happening here in late April/early May. Hams look like they are wobbling again, up one day and down the next, but what concerns me most there is that spot volumes have been very light recently and I wonder if ham prices are going to have to take another leg down soon in order to clean up inventories. The retail primals remain lukewarm, not going down, but not rising much either. It would make sense that retailers should start leaning more heavily on pork, given the high price of beef right now, but that doesn’t seem to be the case. I have to believe that pork demand, which has greater exposure to low income consumers than beef does, is struggling because of the outsized impact that inflation is having on the food budgets of those lower income Americans. If that is the problem, it isn’t likely to get resolved soon. The combined margin did tick a little higher this week, so there is reason to hope that the demand situation is starting to improve, but it is a long trip back to the zero line and I’m not sure that pork demand has enough gas in the tank to make it that far. They say that “low prices cure low prices”, but for that to happen in the pork market, the impetus has to come from the supply side in the form of producers liquidating breeding stock, downsizing their operations or leaving the industry all together. So far, sow slaughter this quarter hasn’t been out of line with what we would expect given the size of the breeding herd on March 1. That suggests that maybe producers aren’t liquidating much, if any, and if that is the case the I may end up having to lower price forecasts from late summer onward. The one positive thing that soft pork prices do is to encourage exports and we have seen decent volumes moving on the weekly export reports lately. I don’t think that will be enough to lift prices substantially, but it may keep them from getting much lower. For now, it is just a waiting game—waiting for the hog supply to tighten up enough to turn the LHI higher. Waiting for some spark on the demand side that never seems to come. Next week, watch the hams and trim closely. Neither looks very good right now and if that continues, or gets worse, we might just have to wait a few more weeks before the cutout recovery begins.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}