Pork Wrap April 19

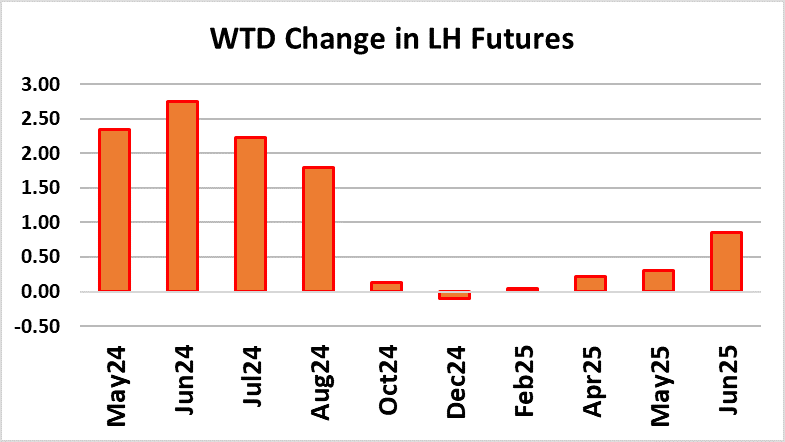

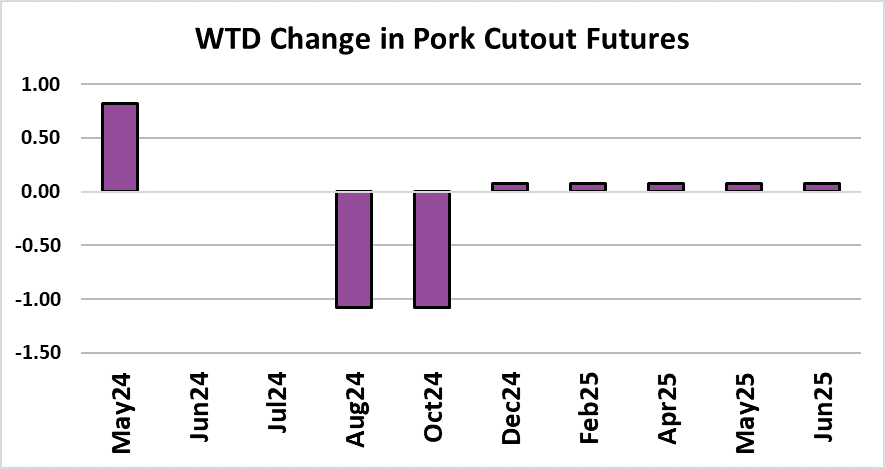

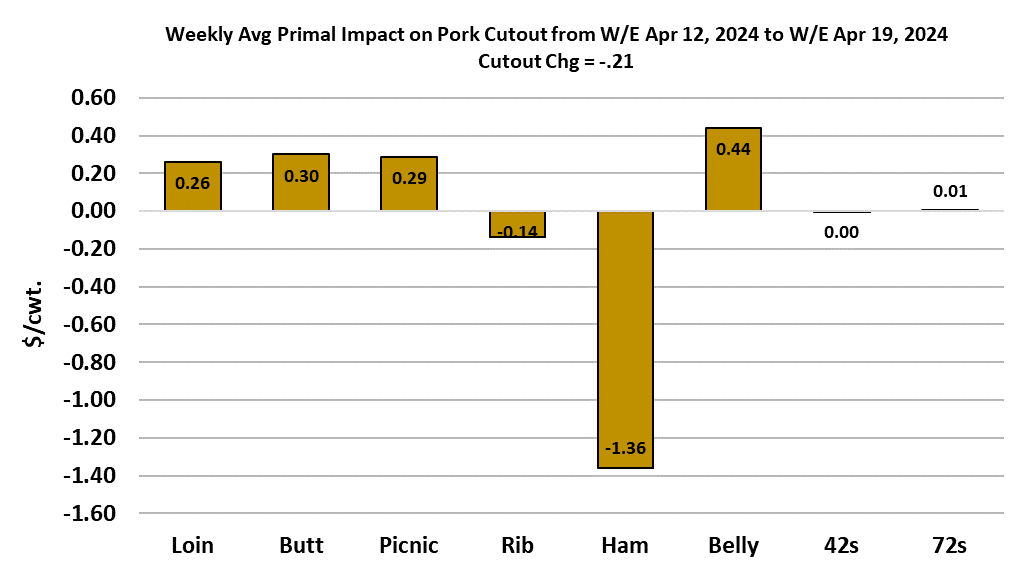

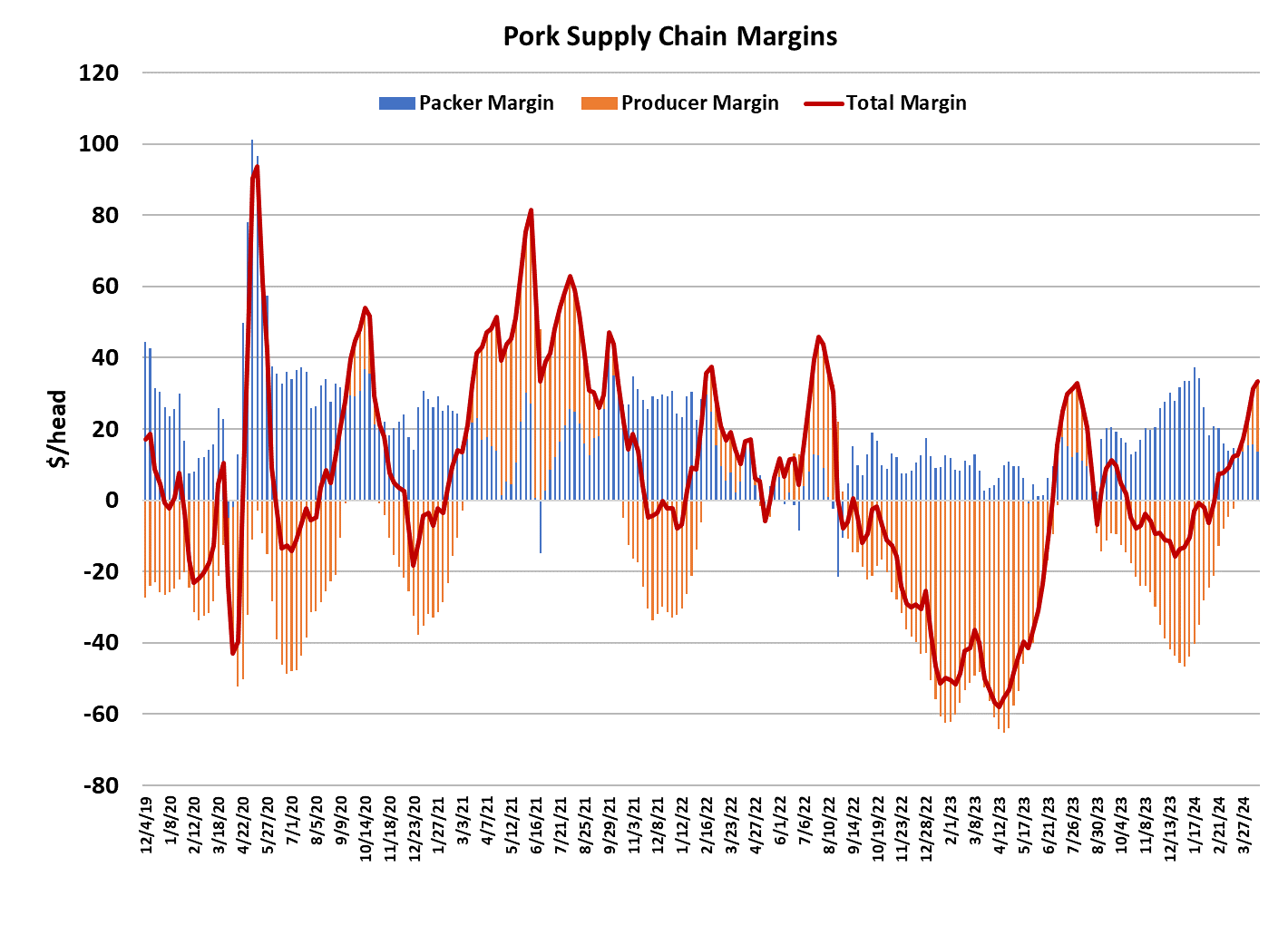

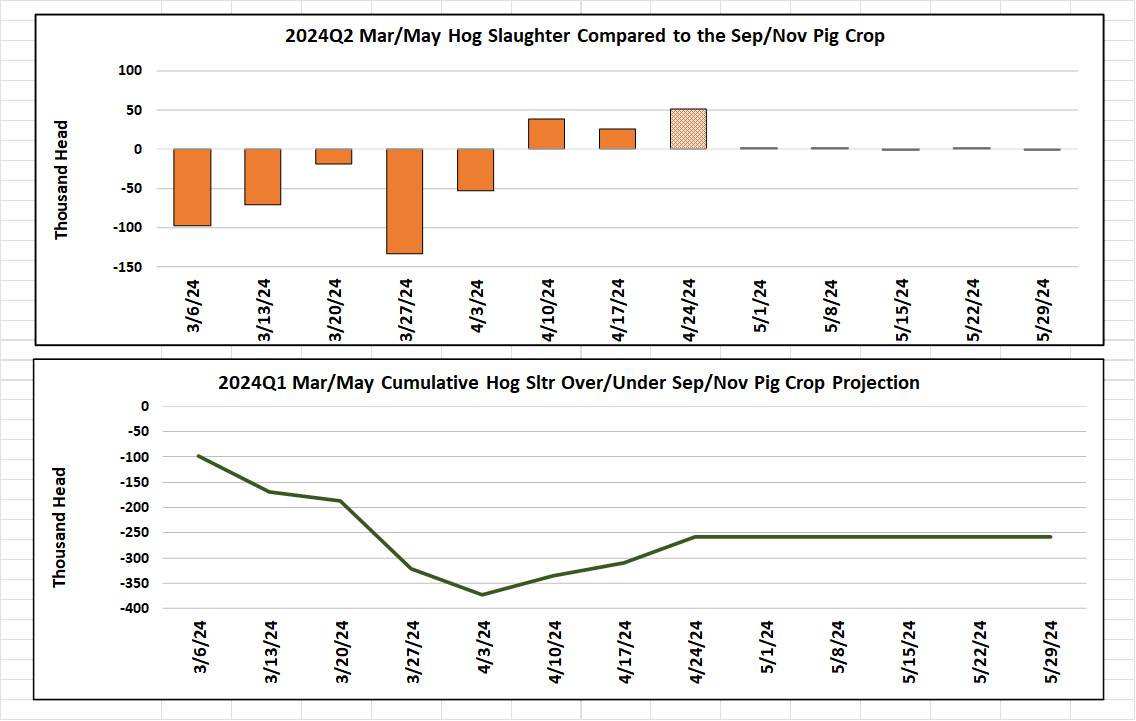

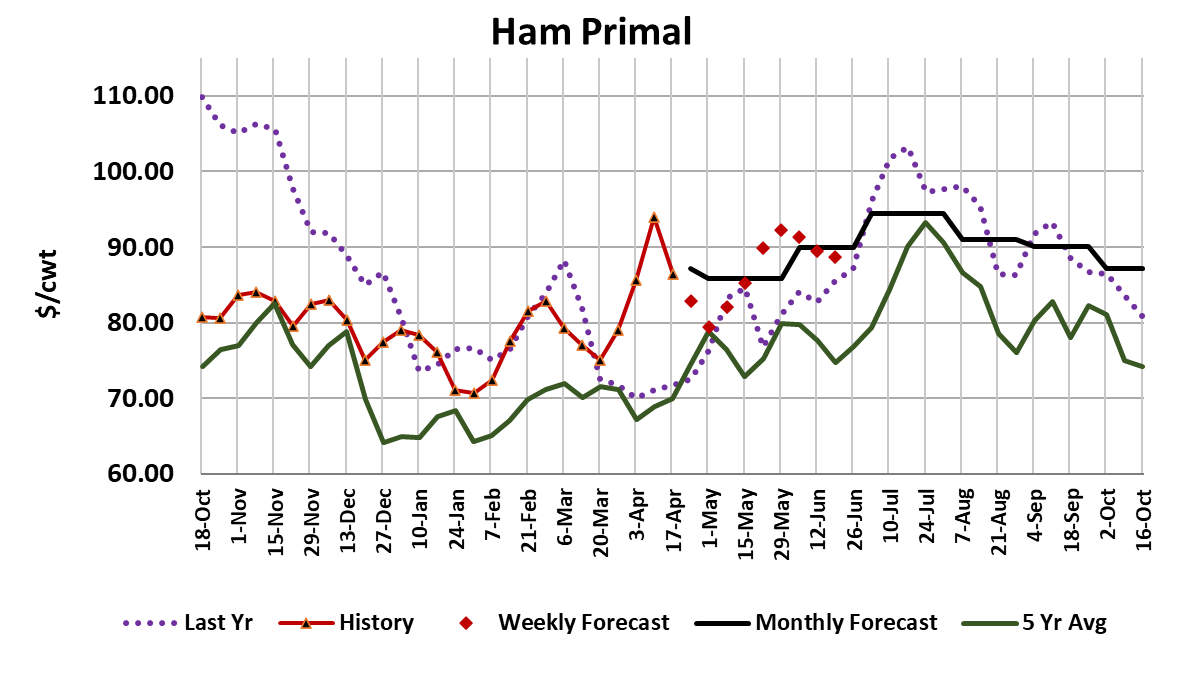

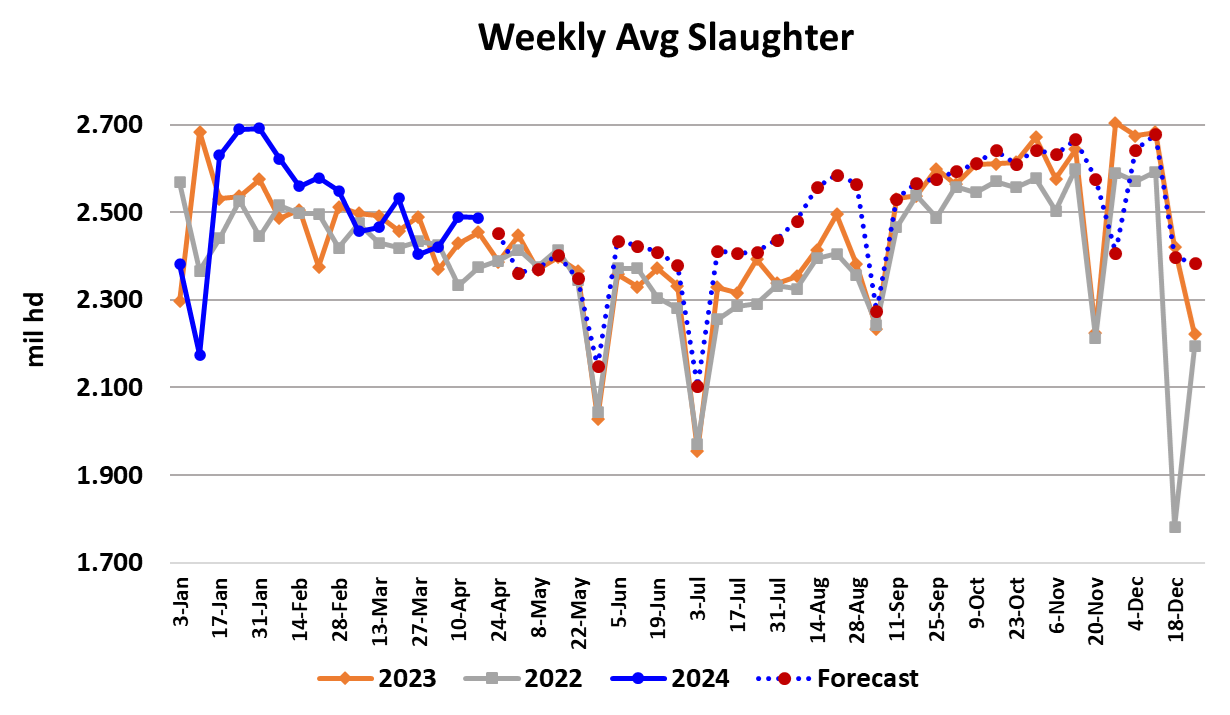

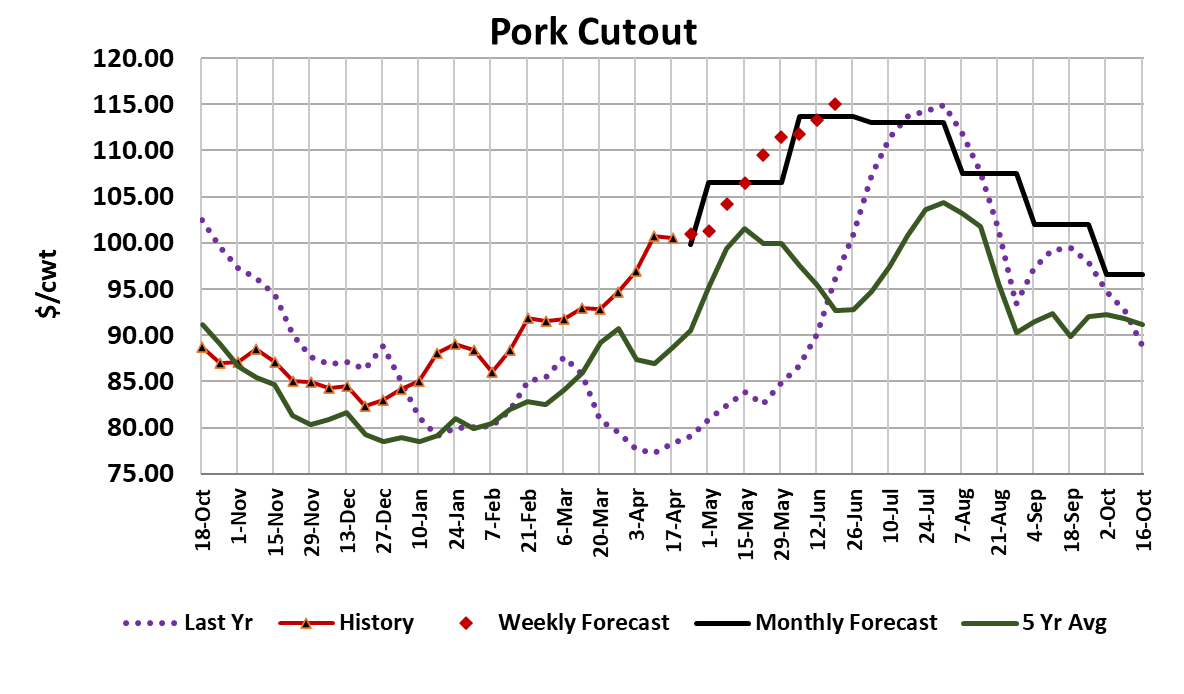

After bursting higher last week, prices in the hog and pork complex took a breather this week. The cutout dropped $0.20/cwt. on its way to averaging $100.55 and the WCB negotiated market was down $0.77/cwt. to average $89.15. However, for some strange reason, the front end of the lean hog futures curve posted gains in the $2-3 range and now look quite vulnerable unless some upward momentum in price levels can be re-established. The LHI is currently just over $91 and I think there is a good chance it can get to the mid $90s for the May expiration in three weeks, but it will need some help from the cutout to accomplish that goal. Last week, I pointed out that the rally in ham prices was due to come to an end and sure enough, the ham primal turned lower this week, shedding almost $9 on a weekly average basis. Hams and ribs were the only items to move lower this week, so the price weakness is not widespread throughout the carcass. In fact, the loins, butts and picnics all continue to march higher in orderly fashion. The belly primal was up $4 this week, but that was largely due to a low volume/high price print that happened on Monday. In reality, bellies are still treading water and waiting for their moment in the spotlight which should be coming in a few weeks. In the meantime however, the concern is whether or not the slow, steady gains in the retail primals can offset further softening in the ham primal. Close examination of the attached price chart for the ham primal indicate that once it starts to decline, it is usually a 2-3 week event and we have only had one week lower so far. That means there is likely further weakness in ham pricing that will hamper the cutout’s upward momentum. Bellies just don’t appear to be ready to pick up the slack, so we may be looking at only minimal gains in the cutout next week. The negotiated hog markets that looked so hot last week have cooled substantially and, while they should keep going higher, I suspect it will be a slow grind for the next couple of weeks rather than a sharp increase. The evidence is starting to mount that hogs on the ground are a little more plentiful than previously thought. This week’s kill came in at 2.487 million head, just a tad below the 2.49 million posted the week before. I’m calling next week closer to 2.45 million, but if that is wrong, it is probably too low. This was the second week in a row where the kill outpaced the prior pig crop and next week is likely to make it three in a row. It is starting to look like USDA might have gotten the pig crop correct, but that it was back-end loaded, thus we saw lighter-than-expected kills early in the March/May quarter and now we may be experiencing heavier-than-expected kills in the second half of the quarter. That could be a bit of a headwind for both negotiated hog prices and the cutout. Packer margins are still very healthy at about $14/head, so there is plenty of incentive for them to keep slaughter elevated if the supply of hogs allows. The best gains in hog and pork prices are likely to come once the seasonal downtrend in hog numbers and carcass weights takes hold. Both of those things are probably a couple of weeks down the road, so near-term price gains could be modest. One other thing that doesn’t bode well for very strong pricing environment this summer is the fact that the Dec/Feb pig crop, which will fuel the Jun/Aug kill, was reported up almost 2% YOY, so we are likely to see stronger YOY pork production this summer unless unusually hot weather sets in and decimates carcass weights. Of course, strong exports could be the counterbalance to that, helping to siphon off a good bit of that extra production. Domestic demand for pork appears to be quite good right now and the combined margin is still rising and now challenging the highs made last summer. The hog margin component of that is much better than it was last year, mostly due to declining corn prices moving the cost of production lower this year. I estimate that producer margins are currently very near $20/head, which is about $7/head stronger than what packers are getting. It has been a long time since we’ve seen producer margins outpace packer margins. Of course the risk is that producers might drop their herd reduction efforts due to this newfound profitability. Further guidance on that will come in the June and September issues of the Hogs & Pigs survey. One other risk that comes to mind is that the current upcycle in pork demand is getting a little long in the tooth, having started back at the beginning of the year. I’d like to think that the first half of that demand improvement was just recovery from the awful demand conditions of 2023 and so a longer upcycle is justified. However, it’s possible that demand could stumble for a few weeks somewhere along the line. The futures market looks fairly priced relative to the fundamental forecast for May, June and July and a little over-priced for the Aug and Oct contracts. However, it seems to be a little ahead of itself at the moment and a modest pullback could be in order. Traders are acting like cash prices are rocketing higher, but that isn’t the case just yet. Next week, look for further erosion in ham prices and perhaps only small gains in the cutout and negotiated markets.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}