Pork Wrap April 16

The pork cutout was about a dollar higher on an average basis this

week, but the negotiated cash hog markets were almost $2 higher.

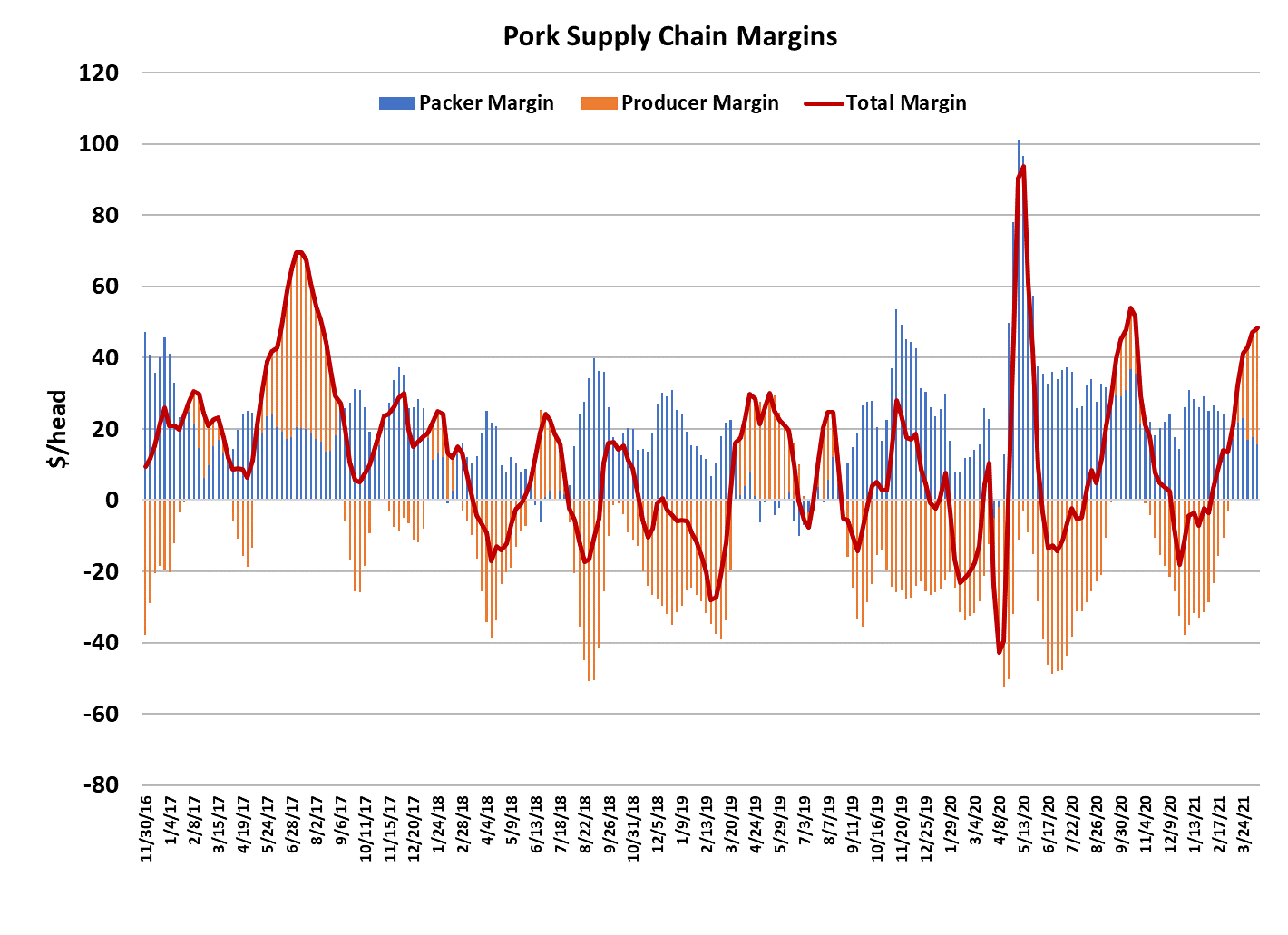

That compressed packer margins down to a little under $16/head.

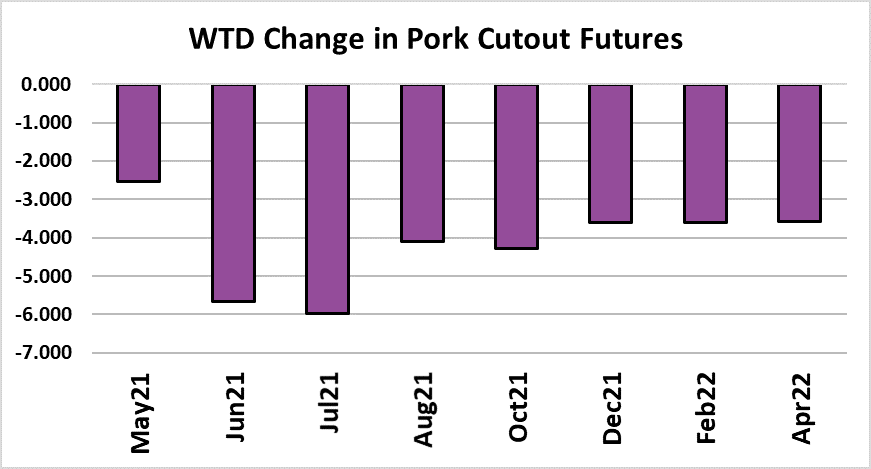

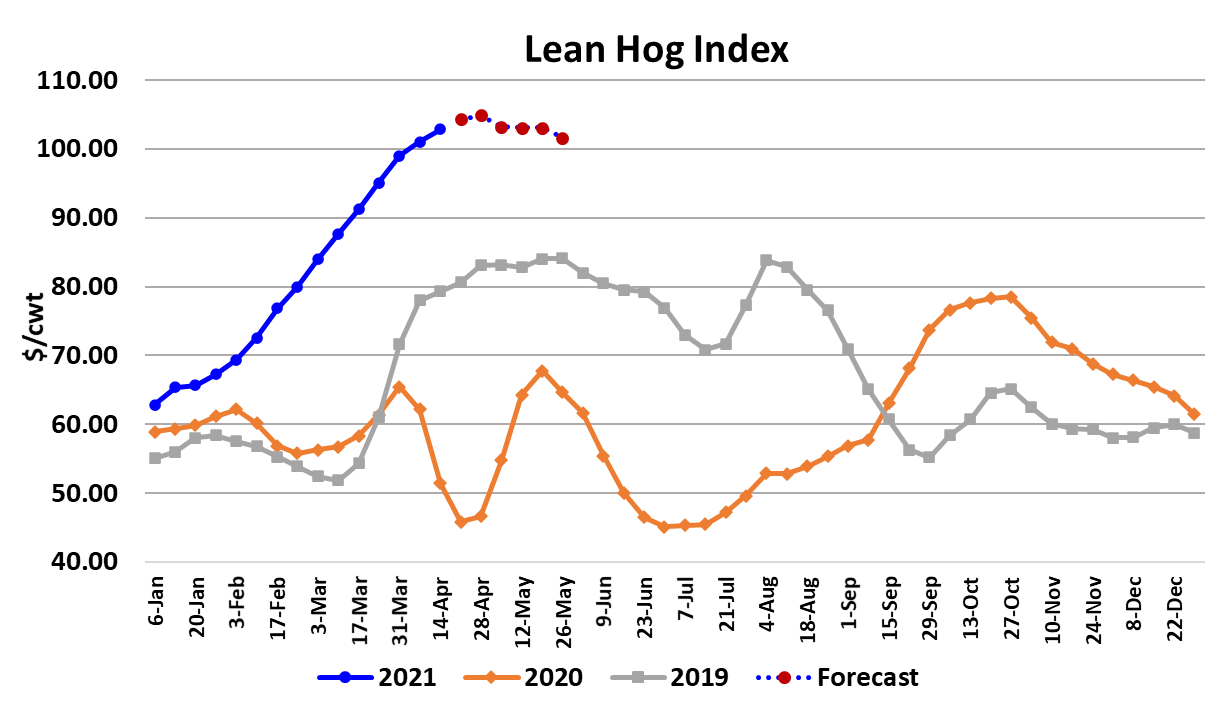

The lean hog futures were volatile this week and the most active

Jun contract lost almost $7 on the week. Apr went off the board on

Thursday and will cash settle at $103.24. The same “loss of faith in

the future” that plagued the cattle market this week also influenced

the hogs. At these high levels, futures tend to be very jumpy.

Traders don’t think in terms of sideways markets, they either figure

it is going up or going down and if the cash market stops going up,

then it must be about to go down. The problem with that thinking is

that the cash market hasn’t stopped going up yet. Traders are

trying to pick a top and that is always a risky proposition. Perhaps

the biggest contributor to the change in psychology this week was

some softness in the belly market. Traders know all too well how

fast a belly market can decline and how fast it will drag the cutout

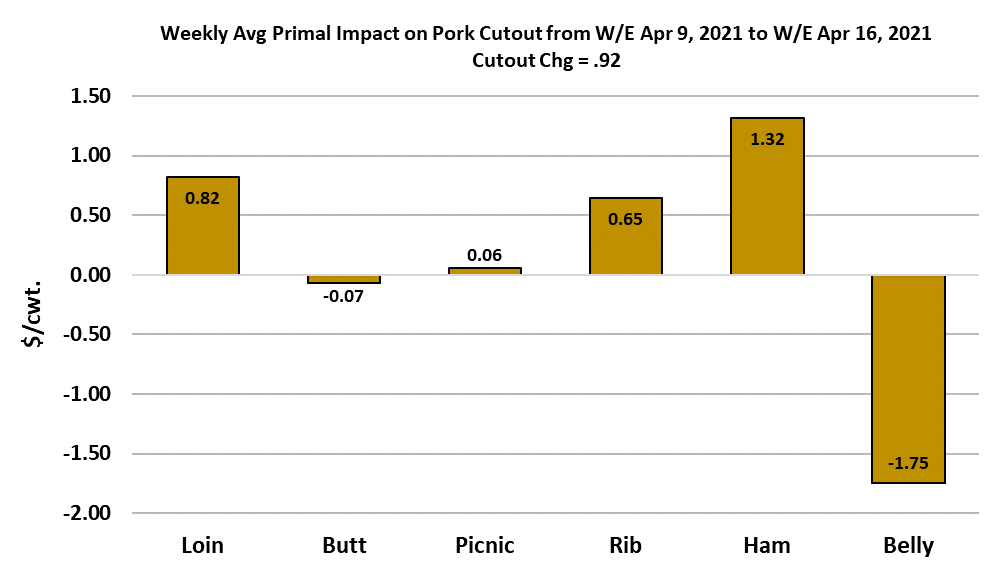

down. However, the chart to the right indicates that the belly was really

the only primal with pricing problems this week, and even those

weren’t too severe. Traders would be better served to take their

cues from the relentless advance in the negotiated hog markets.

Packers wouldn’t be paying up for negotiated hogs day after day if

they thought the cutout was about to fall apart. Measured from

Friday to Friday, the WCB cash market was up almost $4.50 and is

now approaching $106. My model says that if the cutout and

negotiated markets to stay at Friday’s close, then the LHI will be

worth $106 by the end of next week. It will be interesting to see if

the bears are willing to continue selling with the LHI at that level.

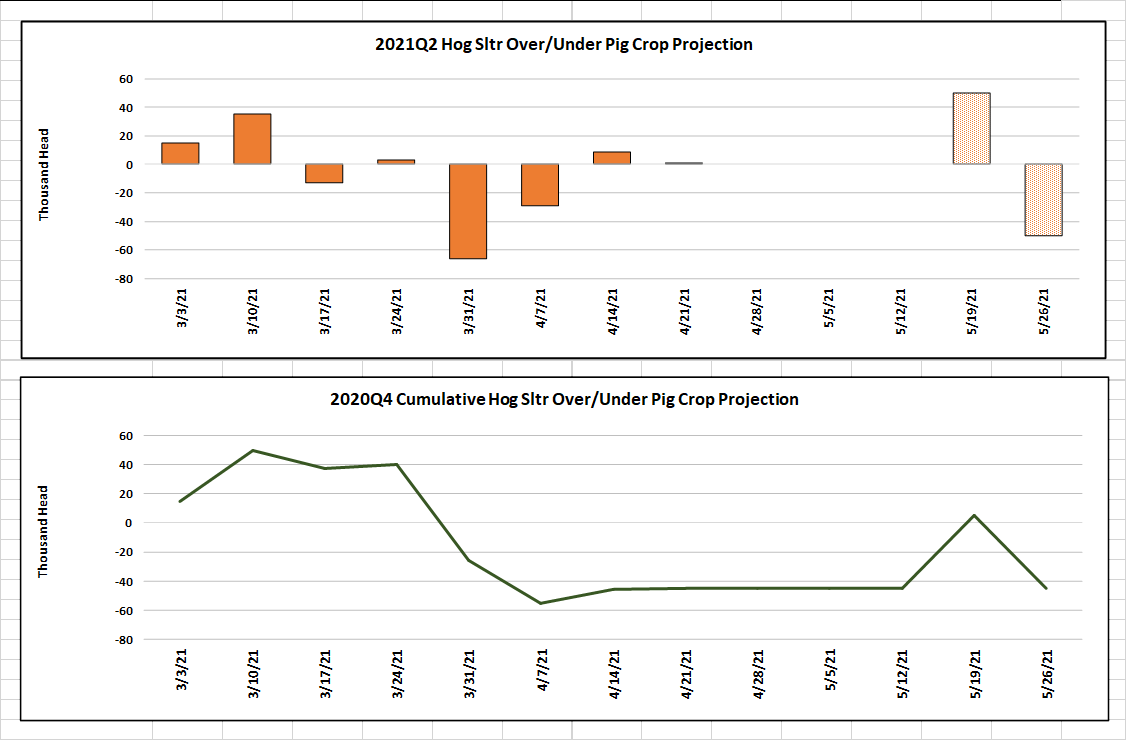

This week’s kill came in at 2.47 million head, which was once again

very close to what the Sep/Nov pig crop projected. Barrow and gilt

carcass weights remain stuck at 215, but it isn’t unusual for carcass

weights to hold in a sideways pattern at this time of year before

turning lower into summer. So, the supply side of the market

continues to look well behaved, although the continued rise in the

negotiated markets makes me think that perhaps some tightness in

the producer-owned hog supply is starting to arise. Retailers are

probably not very pleased with these high wholesale prices, but

they don’t have many good alternatives. Beef is super-expensive

right now and while chicken is a little less pricey, it is still high and

not a first choice among consumers. This makes me wonder where

any future weakness in the cutout might originate.

Clearly, the bellies are a candidate, but we are coming into

prime bacon season. Cold storage stocks of bellies are very

low. Recall that bacon producers had to switch bacon

packaging away from foodservice bulk-type toward retail

consumer packs last spring when COVID broke. Now, with

foodservice on the rebound, they will need to reverse that

change and it could leave one channel or the other short of

product for a while.

Hams have shown surprising resilience and processors will be

busy preparing for the upcoming sandwich season. I’ve got

hams forecasted to ease a little in the next few weeks, but they

are likely to remain well above historical averages for this time

of year. We are starting to see a little weakness in the lean

trim and I can’t help but wonder if that is because hams are

starting to go into the grinder. Ribs are getting hit with a

double whammy of strong demand from foodservice reopening

and consumers in the retail market looking to fire up their

smokers this spring. To me, the butts seem like the logical

place for price softness to set it, but it hasn’t happened yet.

The combined margin was higher again this week, but only by

a little. It looks like it might be ready to make a top, but it has

head-faked similarly a couple of times during the recent

uptrend so I’m not ready to call a top in the demand cycle.

The net new export sales numbers were small on this week’s

report, but that shouldn’t be surprising given the high pork

prices. I’m actually surprised that exports have held up as well

as they have throughout this run up in pricing. The Philippines

has greatly increased its purchases of US pork as that country

grapples with serious ASF spread. China has been taking a lot

of US pork too, but that share isn’t growing, it is in more of a

sideways pattern of late. So, we are left with a market that

continues to experience very strong demand and a hog supply

that is slowly declining in seasonal fashion. The supply side

looks pretty positive over the next couple of months, so if one

wants to bet on lower hog and pork prices, they will need to

count on demand stumbling. I’m not really looking for much

demand weakness from now until Memorial Day, but have built

in some softening as we move into June. Even so, hog and

pork prices are likely to stay well above historical norms well

into summer.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}