Pork Wrap April 15

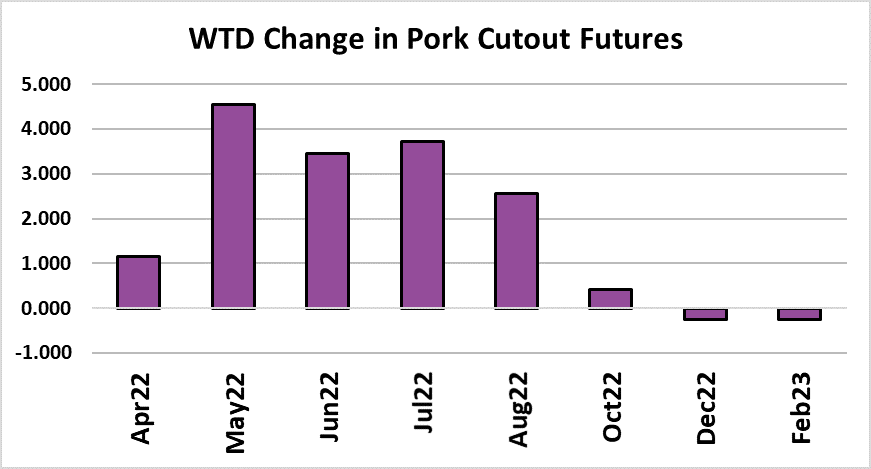

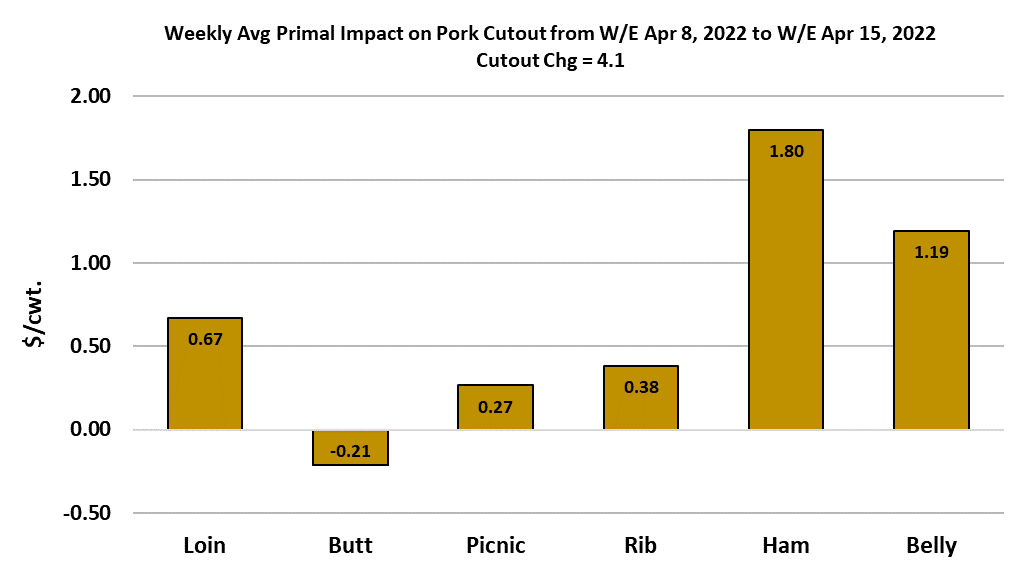

The pork market moved higher this week, with the cutout gaining

$4.10 to average $108.22. Most of that gain can be attributable to

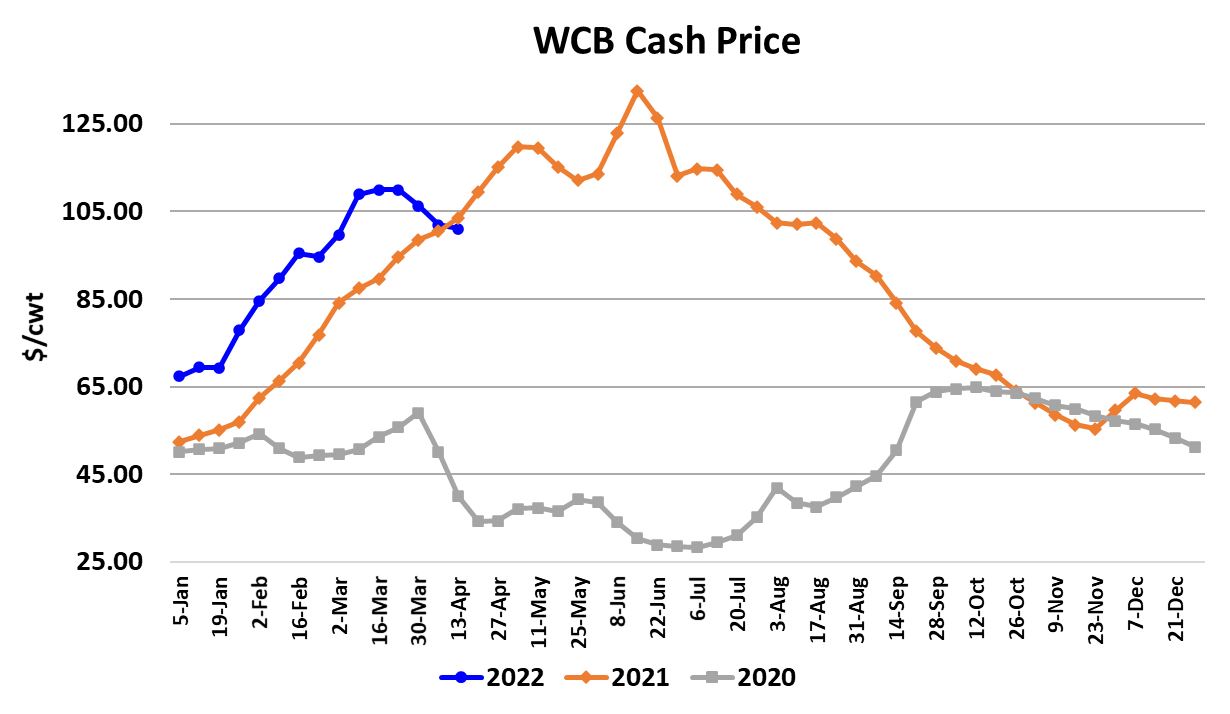

the hams and bellies. Cash hogs, on the other hand, eased lower

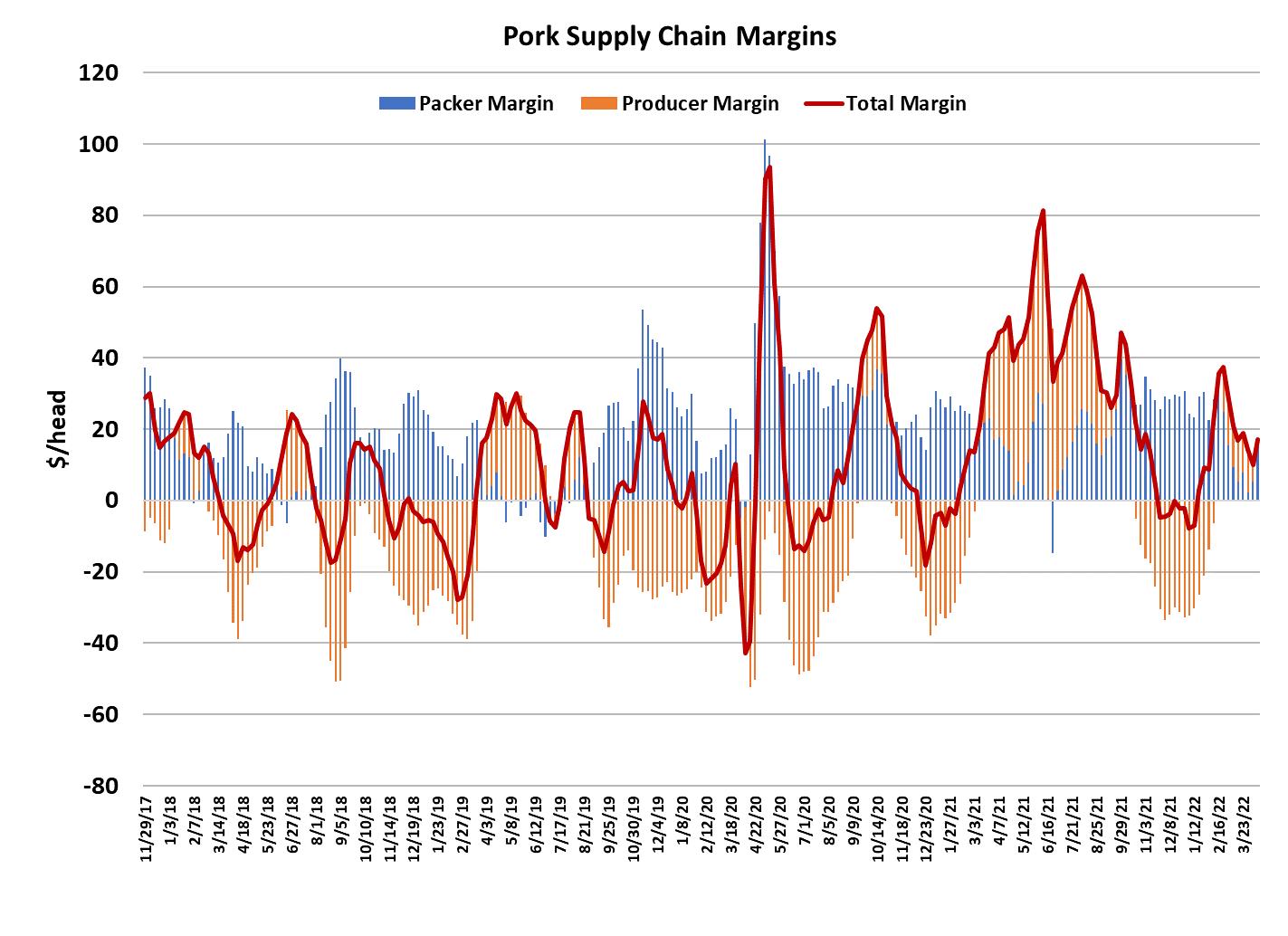

with the NDD negotiated market losing $1.87 on a weekly average

basis. That brought some much needed help to packer margins,

which moved from $5/head last week to over $16/head this week.

However, I’m not yet ready to subscribe to the idea that the cutout is

going to continue up from here. It may get help early next week

from the short kill this week, but the bellies have been acting fickle

and could go lower in the short run. Hams have been supported by

a larger-than-normal proportion of product being sold boneless and if

we see the sales mix move back toward more bone-in product in the

next few weeks, then there is price risk to the ham primal as well.

Of course, the flip side of that is that kills are going to be getting

progressively smaller each week from now until early July. Packers

pulled the daily kill down significantly for Good Friday and are only

planning on killing 8,000 head tomorrow. Basically, there is no

Saturday kill this week. That should tighten up product availability

early next week, but my sense is that buyers are already well

positioned for the shrinking spring kills. They have been boosting

cold storage stocks moderately in recent months because they know

that the hog supply is smaller this summer than it was last year.

There is also a really good chance that the demand pull this spring

won’t be as strong as it was last year. Don’t get me wrong, I’m

certainly looking for some price appreciation as we head into

summer, but I am not nearly as optimistic as the futures are at this

point. I also don’t think that the gains are going to come in a straight

line.

There could be some soft spots along the way that cause traders to

question the high valuations they are placing on the summer

contracts. The Apr contract expired today at just a hair under $100

and the May contract closed the week just shy of $113. It is pretty

rare for the LHI to gain more than $10 over the course of a month

and with all of the headwinds facing consumers this year, I’m betting

that May will struggle to earn its premium. If May struggles, so will

June. The fact that the trajectory of the negotiated hog market is

downward right now is a huge headwind for the LHI. It seems that

disease problems that were often cited earlier this year have started

to fade and that has put some leverage back into the packer’s

hands. Of course, everything is ultimately in the consumer’s hands

because pricing all up and down the supply chain is contingent upon

the strength of consumer demand. In that regard, pork is in a better

position than beef due to its lower price point during these times

where consumers are becoming increasingly price conscious.

Chicken prices are really elevated also as that industry struggles

with avian influenza outbreaks and what appears to be very strong

demand. So it is possible that pork might be in the sweet spot for

consumers right now-cheaper than beef and almost cheaper than

chicken. That makes me think that pork demand is not on the verge

of falling apart, but it also is not going to match the super-strong

levels that we saw last year at this time. This week, sow prices

printed higher than butcher hog prices. That is a pretty rare

occurrence and may signal that consumer demand is strongest for

the lower-end products in the pork complex. Sow meat also

contains a lot more fat and fat seems to be a premium product

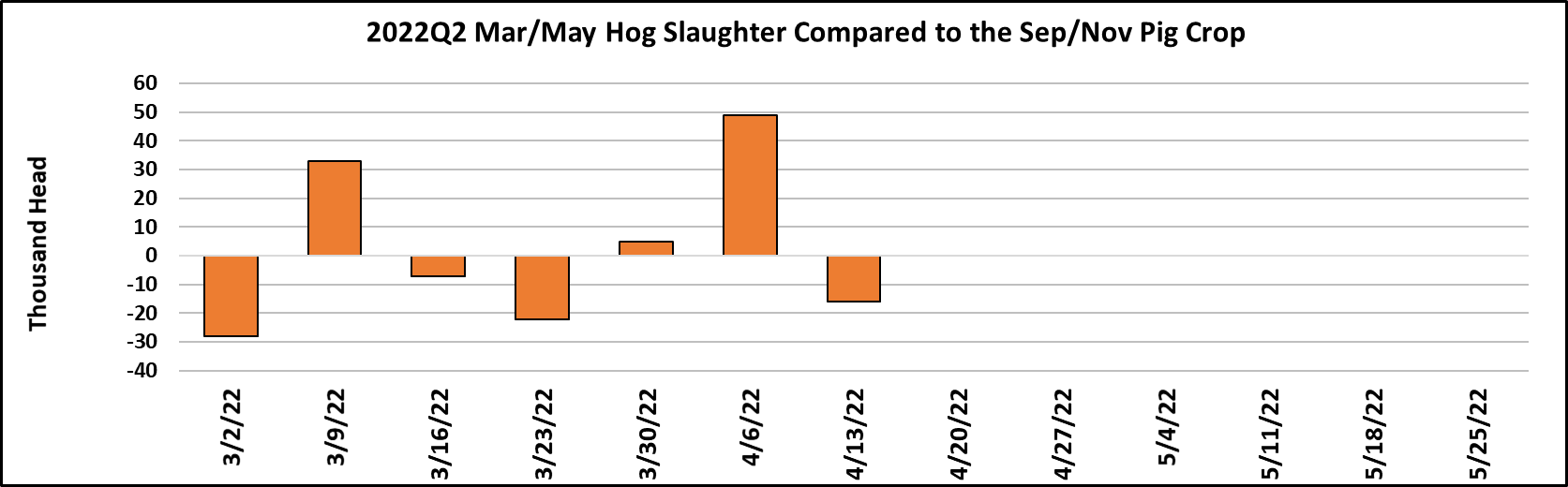

these days. This week’s kill totaled 2.35 million head, which was a

little shy of what the pig crop called for, but cumulatively, slaughter

so far in the March/May quarter has been almost dead on the pig

crop projection.

Next week’s slaughter should be a little larger than this week, but

probably not by much. By mid-to-late May, the weekly kill should

drop under 2.3 million head per week and it should bottom close to

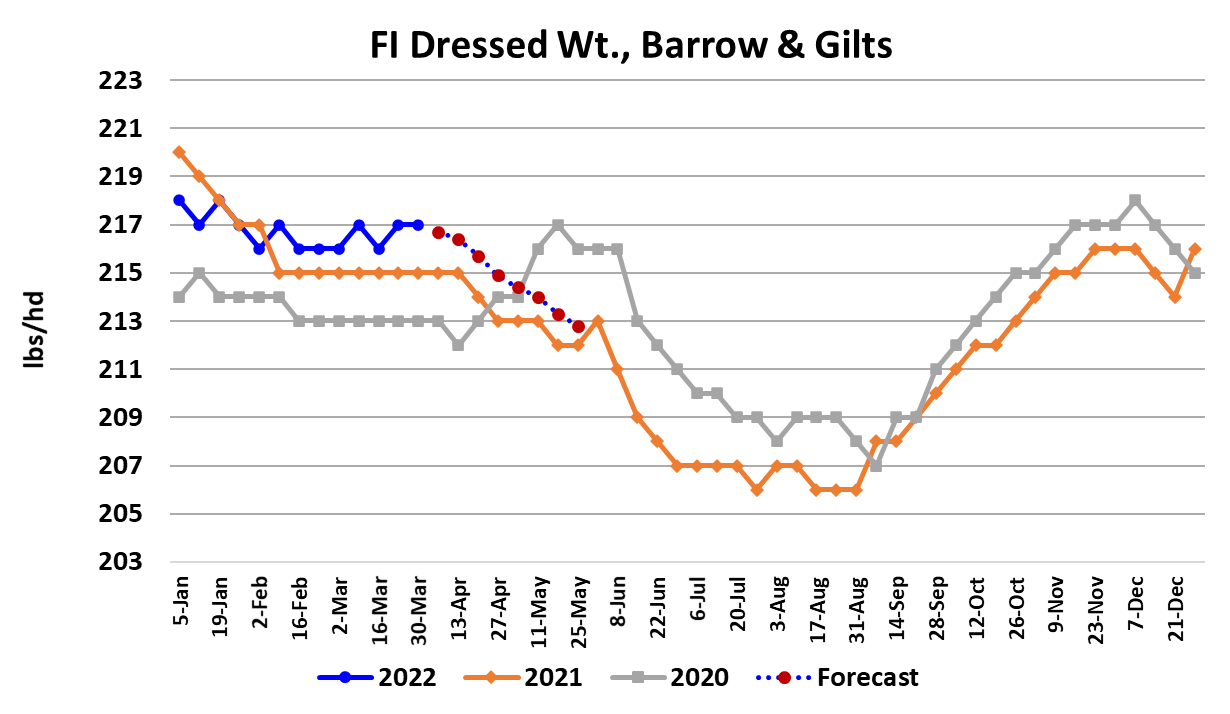

2.25 million head per week in late June or early July. Hog weights

remain plateaued for now at two pounds over last year, but some

YOY increase is expected and there doesn’t seem to be anything

concerning about carcass weights right now. So far, super-high

corn pricing hasn’t led producers to push hogs out the door any

quicker than normal. Weekly exports have been mostly sideways

recently, but way below last year at this time. China seems to have

lost interest in US pork as prices in China are still exceptionally low.

Pork prices in the EU are rocketing higher, most likely due to

buyers wanting to have more product around them as the Russia-Ukraine conflict intensifies.

Even so, it is not likely that much US pork will head to Europe.

Instead, US pork might replace EU pork in some importing

countries if relative prices justify it. That could help US exports

some, but I don’t think the effect will be large and certainly won’t be

enough to offset lethargic movement to China. The combined

margin chart seems to be telling us that pork demand has entered

another upcycle and while that might be true, I want to see the

combined margin gain for another week at least before I declare

this downcycle to be finished. If pork demand is now in an uptrend,

then that would be consistent with beef demand and the first time in

a while where demand for both is working higher at the same time.

Next week, we want to see if the cutout can hold on to this week’s

gains. That means the bellies and hams need another strong

showing. They may both deliver on that, but my gut tells me that at

least one of the two will struggle next week.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}