Pork Wrap April 14

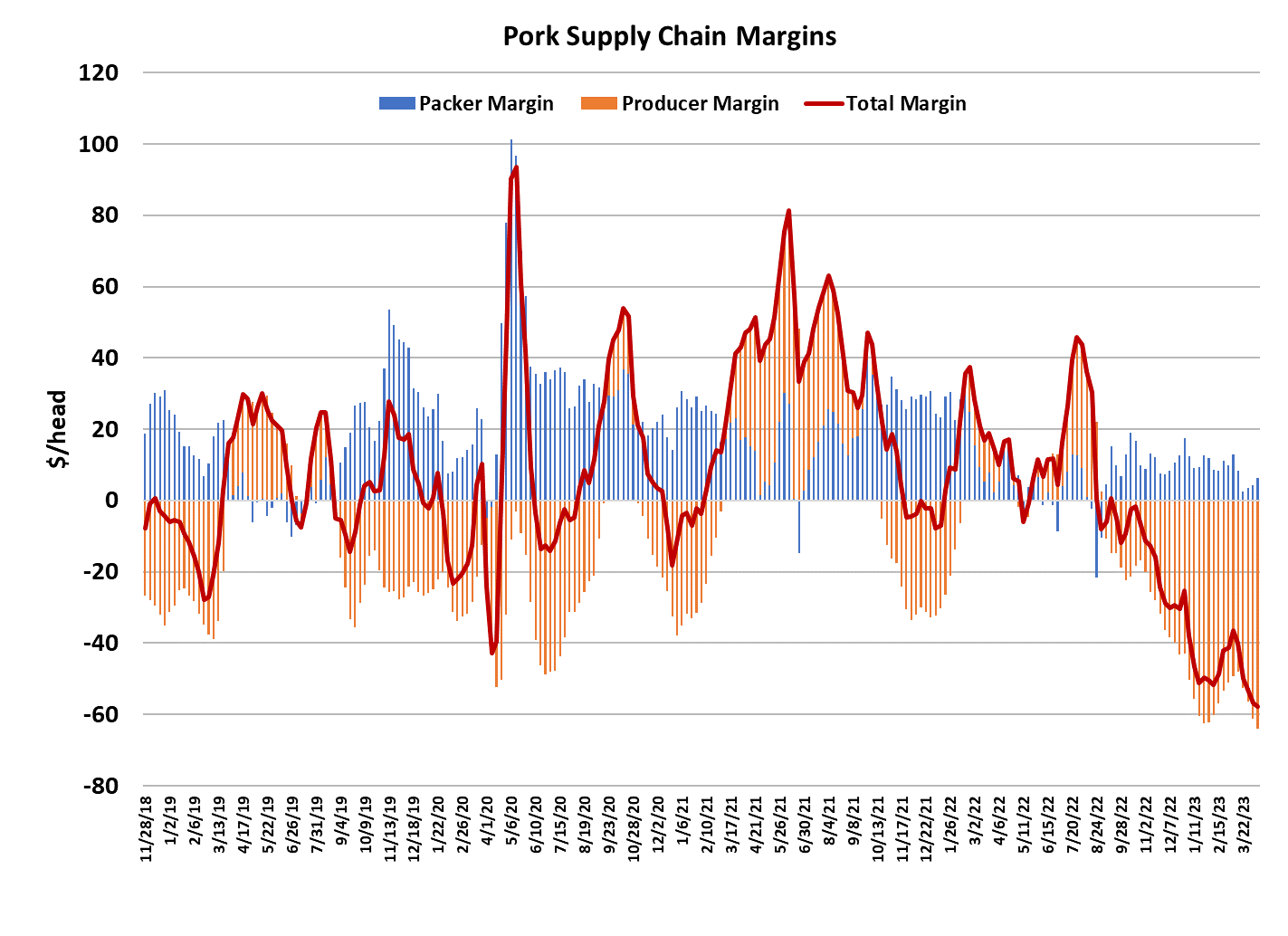

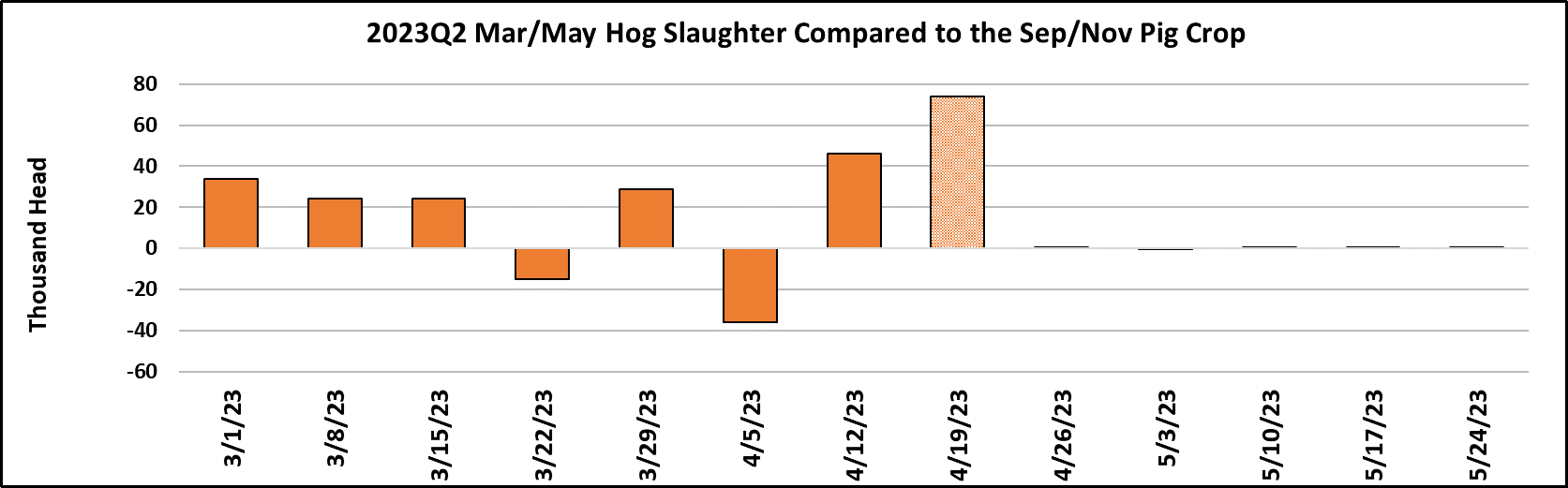

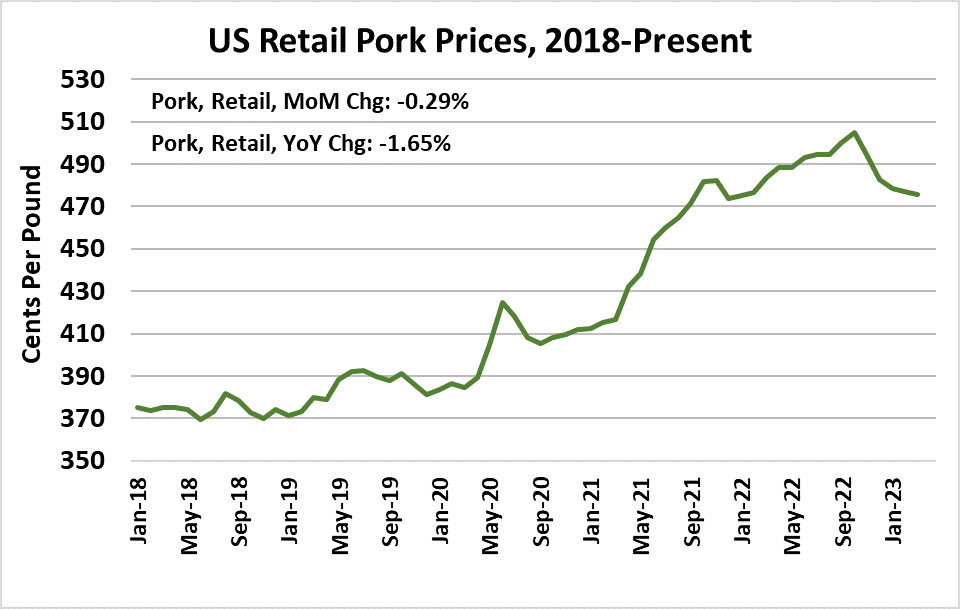

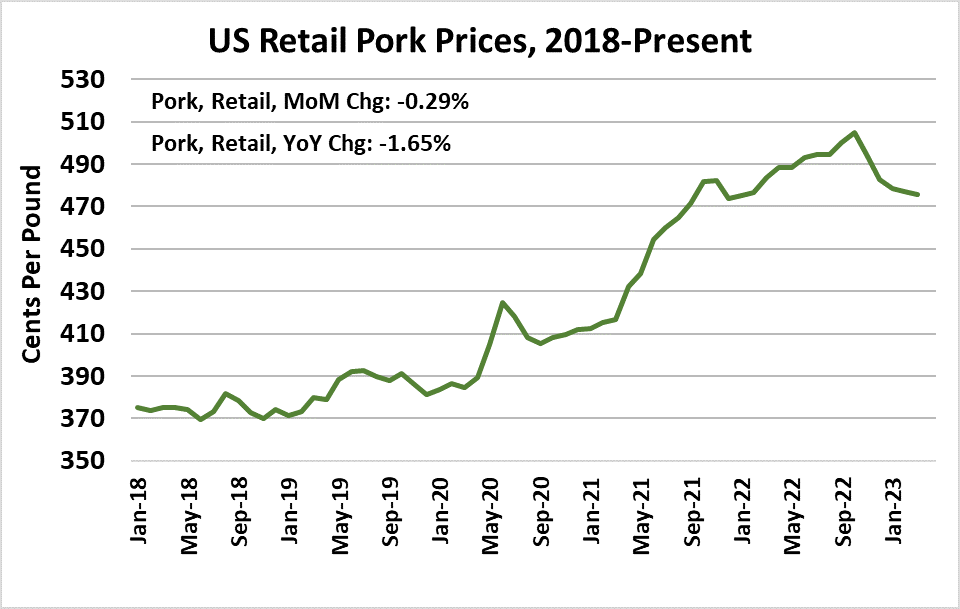

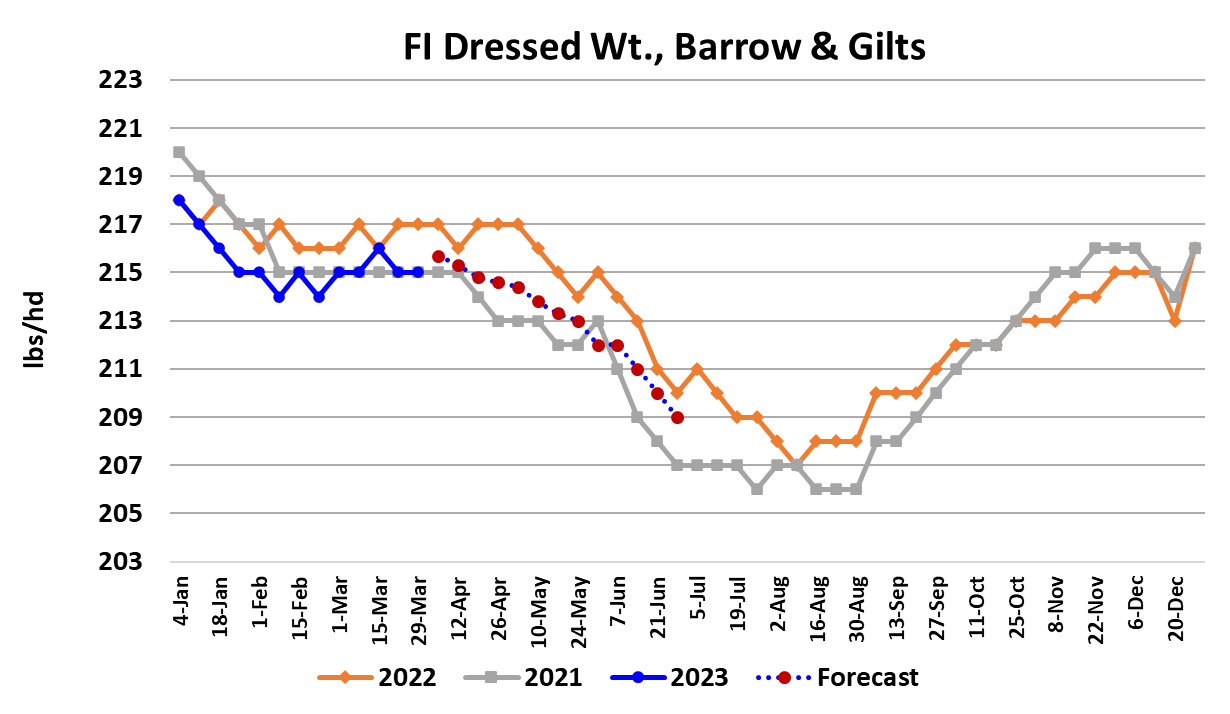

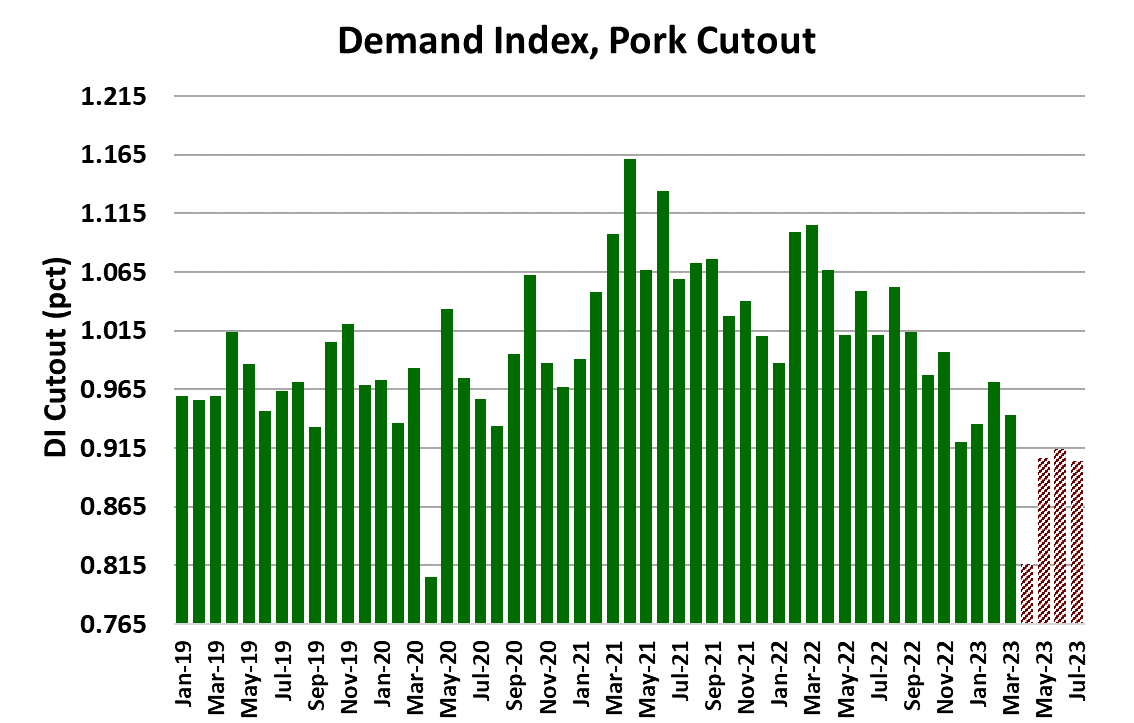

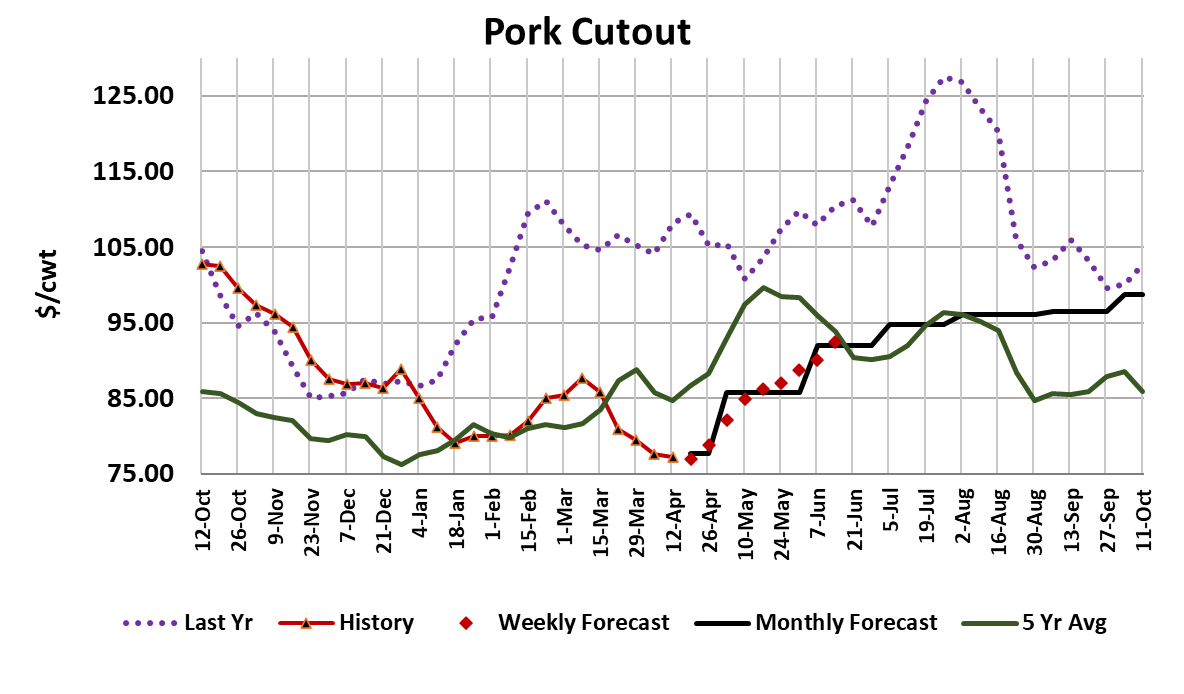

This week, while all of the fireworks were going off in the cattle and beef complex, it was just more of the same in the hog and pork complex. Hog and pork prices continued to their painfully slow grind lower. The NDD negotiated hog market was down $1.56/cwt. on a weekly average basis and the pork cutout lost $0.39/cwt. this week. There is an increasing sense in the industry that surely the spring turn higher in the market is just around the corner, but so far that hasn’t materialized. Domestic demand continues to soften. The combined margin fell to yet another all-time low this week. Once again, bellies were the biggest drag on the cutout, while hams provided some modest support. It seems unlikely that the cutout will make a strong upward correction without some fairly decent help from the bellies. Large cold storage stocks are probably limiting spot demand from bacon slicers and the high price of eggs in recent months has probably damaged bacon demand since those two items are strong compliments. Egg prices are now coming down at a good clip, but are still well above normal levels. Further, consumers who might would have normally had a bacon and egg breakfast may have changed their habit to something else while egg prices were in the stratosphere. So it may take longer than one might imagine for belly demand to return to normal and that is a bad sign for the hog and pork complex this summer. It seems like week after week, I have to take my price forecasts lower for almost everything in the pork complex because spot prices are under-performing. The Apr futures will expire on Monday somewhere close to $71.60 and that will be about $4 lower than where the February contract expired. Clearly, this year looks nothing like that pandemic years for the pork industry. My theory is that pork is heavily favored by lower-income consumers and those folks are being squeezed now that their pandemic savings have been used and inflation forces them to be very judicious with every dollar. Upper-income consumers are not feeling nearly the same financial pinch, but those folks prefer, and can afford, beef, so we have seen beef demand greatly outperform pork demand this spring. I’m not really sure if anything will change that situation over the next few months, so my bias is that pork demand will probably remain underwhelming for some time. Sure, there should be some seasonal improvement in demand, but its not likely to be strong enough to take the cutout back over $100/cwt. like we have seen in recent summers. Adding to the industry’s problems are hog supplies that continue to run larger than expected. So far in the March/May quarter, the industry has over-killed the Sep/Nov pig crop by about 150k and that is after USDA drastically slashed the Sep/Nov pig crop in the latest Hogs & Pigs report. This week’s slaughter was tempered by a very light kill on the Monday following Easter, but it still registered 2.44 million head because packers killed 173k on Saturday. Next week’s kill is shaping up to be back near 2.5 million head. We know from the Hogs & Pigs report that available hog supplies this summer should be about 1% larger than last year and could be even bigger than that if USDA’s habit of under-estimating the pig crop persists. Barrow and gilt weights have been holding in a sideways pattern but should start to trend lower soon. The DTDS weights don’t give any indication that hogs are backing up in the pipeline. Producers are probably eager to ship hogs out of the barns given that they are now losing a little over $64/head on every animal produced. There has been a lot of talk about larger corn production this summer pushing corn prices down toward $5/bushel at harvest, but I don’t think that producers can wait that long for relief on their biggest input cost, so I’ve been forecasting bigger reductions in the breeding herd from this point forward. That is why the fall and winter contracts are showing such large underpricing at present. I am probably looking for more herd liquidation than what futures traders have in mind. Time will tell on that one. There was a huge pork shipment to China reported in this week’s export data, but it was probably mostly offal and even then something looks fishy about the size of that shipment. I expect a lot of that will be retraced next week. The May and June futures seem really high compared to where the spot hog market is, especially when we consider that every price in the hog and pork complex has been moving at a glacial pace so far this year. It is hard to imagine the LHI rallying $10 in four weeks to reach the $81 price that the May contract is currently carrying. There isn’t really any guarantee that the LHI and cutout have stopped going down yet. They might continue to ease for another couple of weeks and that would be disastrous for May at $81. Seasonally, it makes sense that prices should start to rise because demand should get better heading into grilling season and hog supplies should get smaller as we move toward summer, but the way this market has behaved so far in 2023 even those normally dependable events may be called into question. The forecast for next week has the cutout easing a little lower yet again. More of the same.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}