Pork Wrap April 12

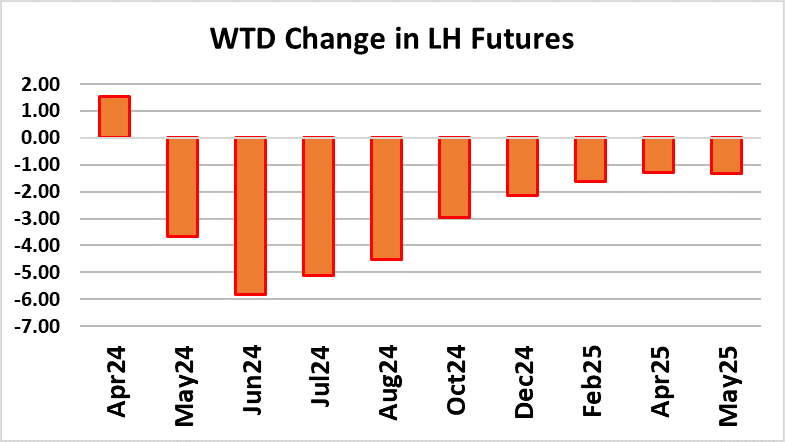

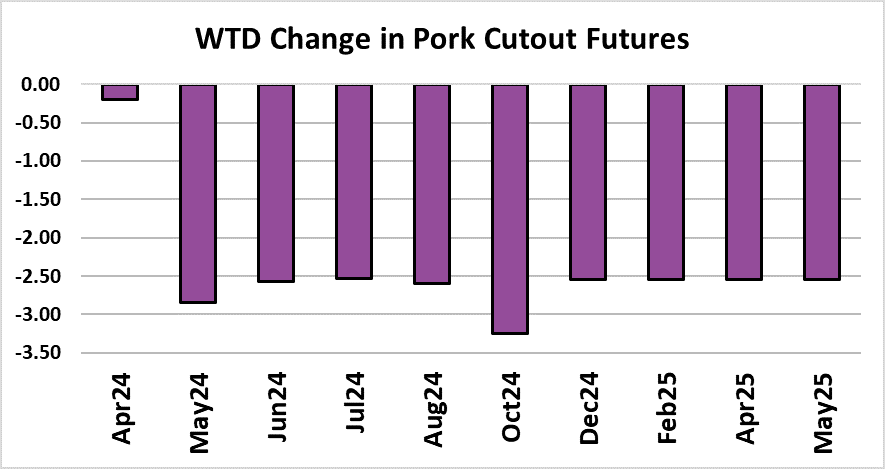

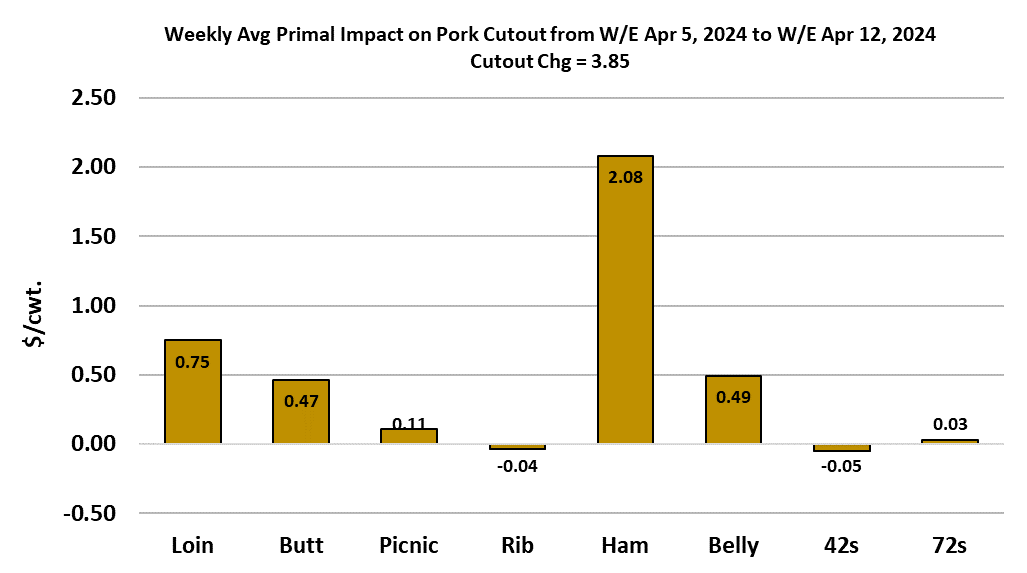

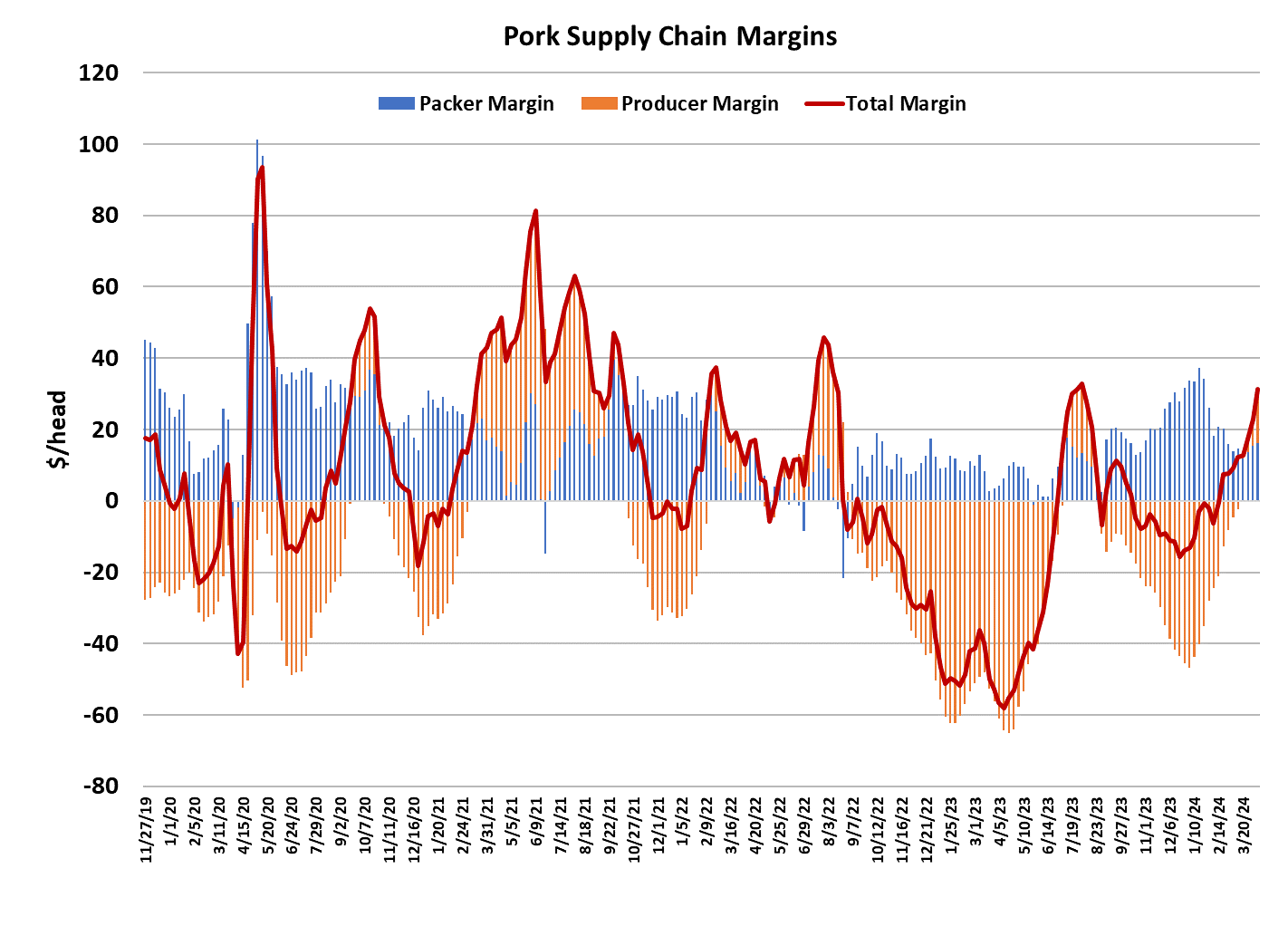

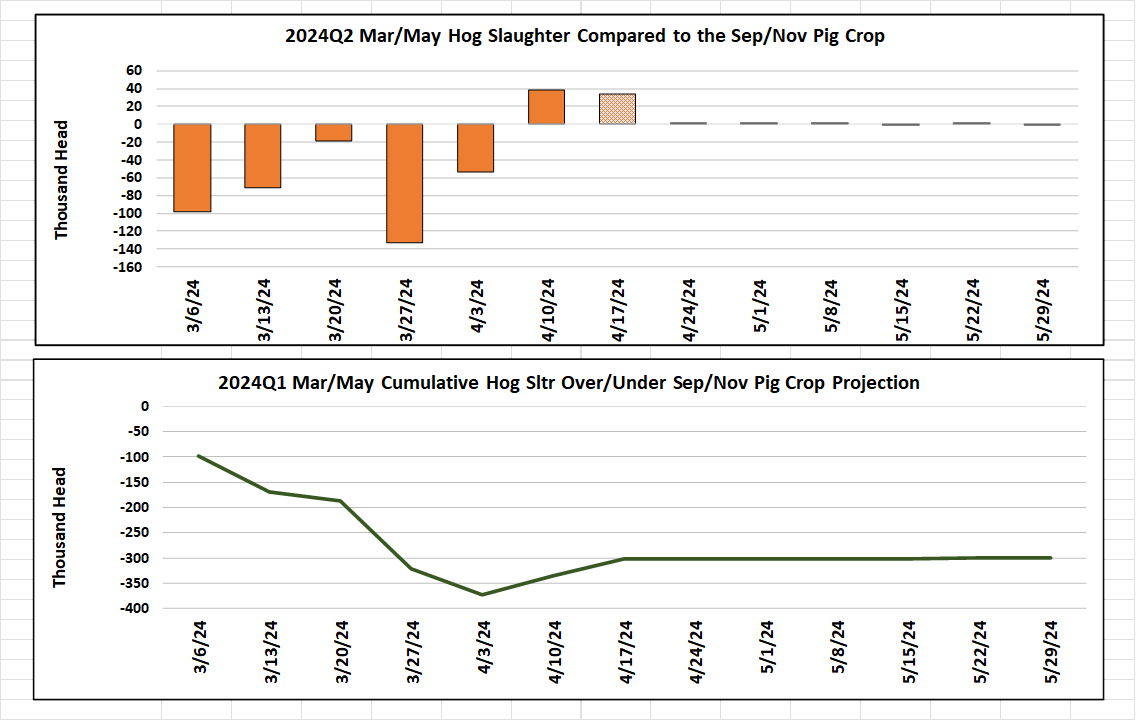

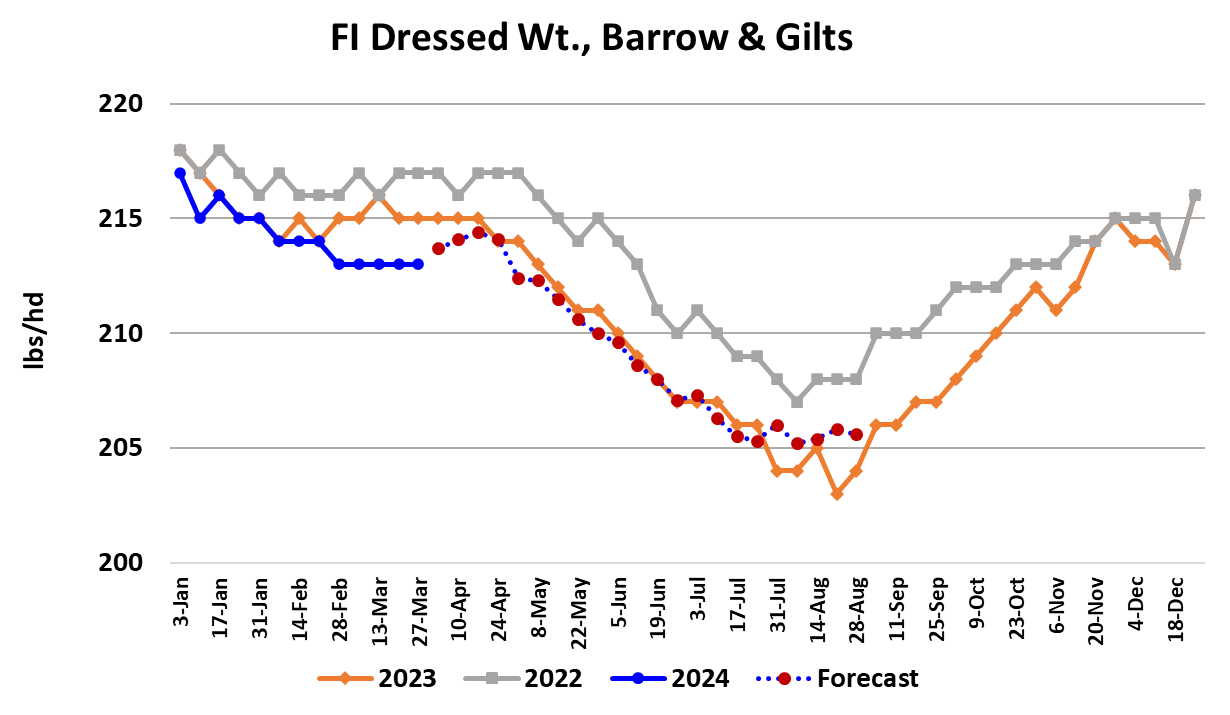

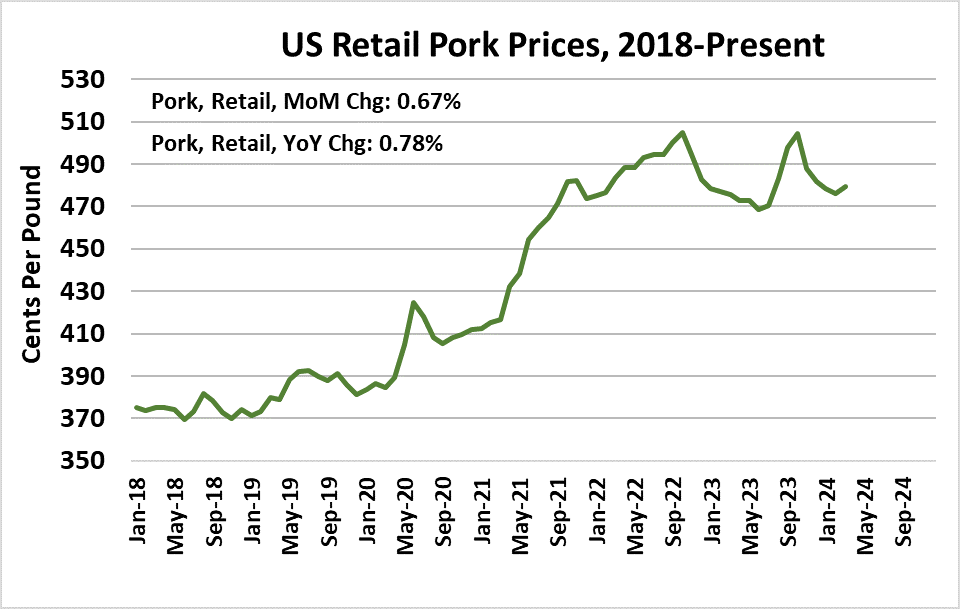

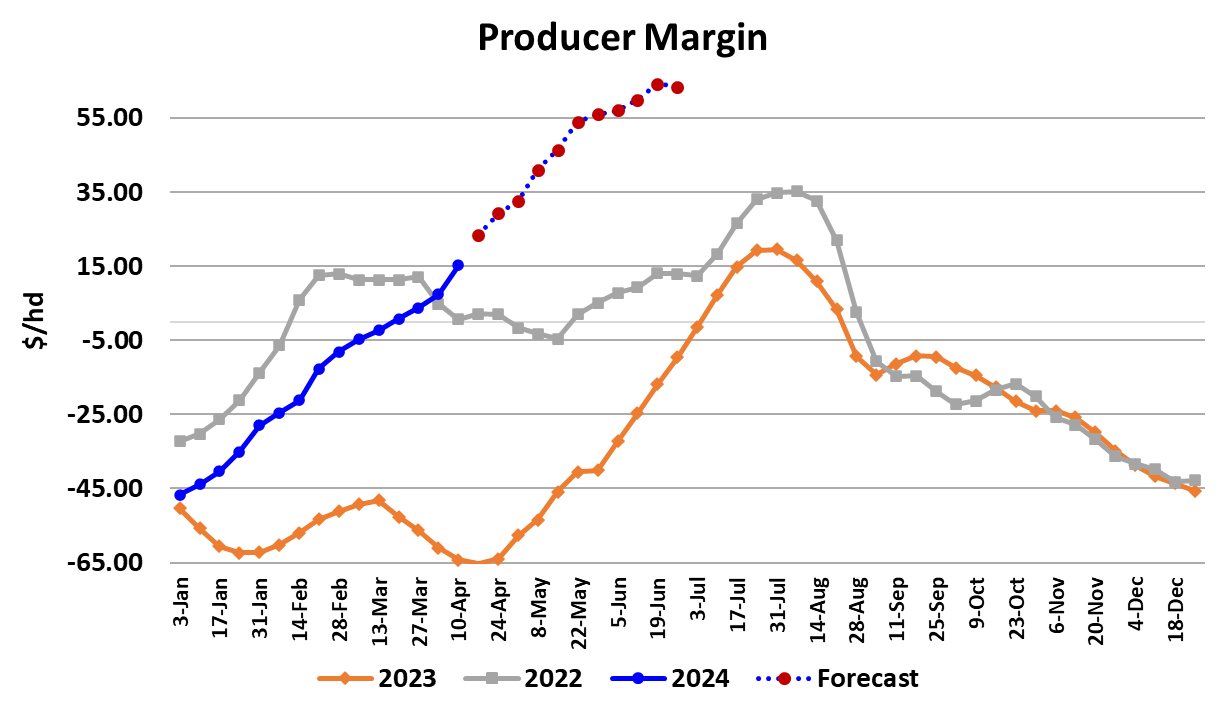

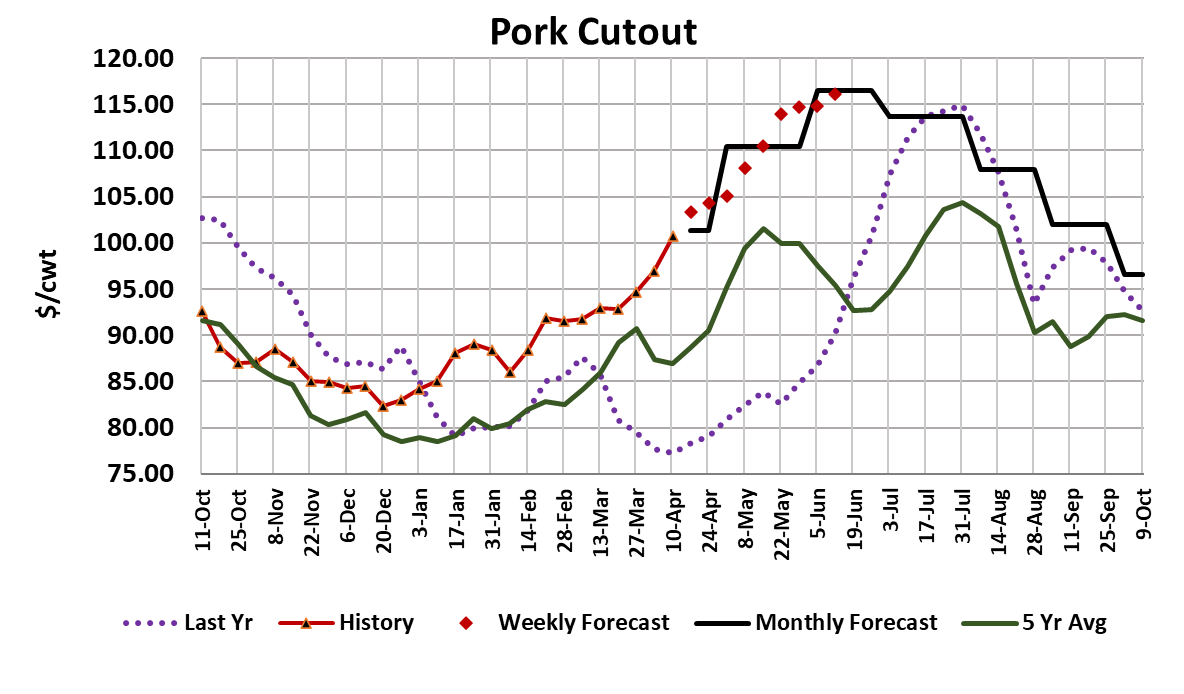

The hog and pork complex got pumped up this week, just in time for the Apr futures expiration. The cutout gained $3.85/cwt. on a weekly average basis in moving to $100.76 and the WCB negotiated spot market added $4.54/cwt. on its way to averaging $89.93. As a result, the LHI surged higher, up $3.41 on a weekly average basis, and will likely be very near $91 when the Apr’s settlement value is calculated on Monday. It appears as though a disconnect is starting to develop between spot hog prices in the WCB and the ECB region. On Friday afternoon, USDA reported the WCB price almost $3 over the ECB price. We have seen this happen before, and it most frequently happens in the summer when available hog numbers are the smallest. Perhaps the markets are signaling that hog numbers are starting to tighten seasonally, particularly in the WCB region. This week’s kill came in at 2.49 million head, which was up almost 70k from the week before. This was the first week so far in the March/May quarter where slaughter exceeded what the Sep/Nov pig crop implied. I’m looking for next week’s kill to be at a similar level, but after that the forecast has kills trending lower in a seasonal pattern that should persist until early July. Packers have plenty of incentive to keep the kill elevated, as their margin is currently around $16.50/head. Of course, with hog supplies set to decline seasonally and hog prices rising, packers will need to keep the cutout moving higher if they want to protect their margin. That is a tall task and I suspect that cutout values will not keep pace with hog prices in the next couple of months, so a significant reduction in packer margins is likely. Barrow and gilt carcass weights are still holding in a sideways pattern at 213 pounds and are running two pounds below last year. The weather forecast indicates that higher temperatures are in store for the Midwest over the next week or so, but that probably won’t have a measurable impact on performance. In fact, we may actually see FI hog weight bump a little higher for a few weeks before they begin their seasonal decent in early May. The de-trended and de-seasonalized carcass weights continue to run at low levels, suggesting that hog producers are doing a good job of staying current on marketings. Overall, the supply side picture looks modestly bullish at this point and will probably look more bullish a month from now. The demand side of the market appears very healthy at the moment. The combined margin continues to track higher and we are in a situation where both the packing and production sectors are profitable. This week’s big gain in the cutout was driven by the hams, but the loins, butts and bellies also made a contribution. The ham primal has soared from $75/cwt. to $95/cwt. over the past three weeks. Careful inspection of the attached chart reveals that upswings in ham pricing tend to last only a few weeks before prices move back down again. That makes hams look vulnerable at these lofty levels and I’m sure that was one of the things rolling around in the minds of futures traders this week when they elected to crash the Jun futures almost $6 lower this week. The forecast does respect this pattern and has the hams turning lower soon, but I think the softening phase will be brief and shallow before hams take another run higher in May. I don’t think that this strong move in ham prices is solely the result of domestic demand. The export market is probably lending a big hand here as well. Spot volumes have been running light relative to the kill for the past couple of weeks and that suggests that a higher percentage of product is moving through non-spot channels, such as the export market. Even though I’m looking for the upward run in ham prices to come to an end soon, I don’t think it will be enough to turn the cutout lower because I’m counting on the bellies and retail primals to push upward. The action in futures was a bit puzzling this week. The Jun contract brushed up close to $110 during Wednesday’s session and by Friday afternoon it was close to $102. That seemed like a rather extreme reaction when there was very little in the fundamentals that would suggest such a sharp correction was necessary. True, the summer contracts had been on a long upward run and were overbought in a technical sense, so that might have justified a modest pullback, but not $8. Perhaps the most interesting result of the crash in hog futures is that it left the May contract in the high $93 area and the LHI is expected to print near $91 on Monday. Can the LHI gain $3 in a month? Heck, it gained over $3 this week. Given warmer weather and the expectation for seasonally declining hog supplies, the bears seem to be playing with fire on the May contract. The fundamental forecast has the cutout at $108 for May expiration and the LHI just a tad over $100. The bear argument hinges largely on the fact that prices in the hog and pork complex have been on an upward trajectory for a long time now and so a correction is likely. The combined margin is approaching the top it made last summer, which is pretty impressive given that it is only mid-April. It has been in an uptrend since early January, so perhaps this upcycle is getting a little long in the tooth. Time will tell. USDA released retail pork prices for March this week and the data indicated a 0.7% increase from February and a 0.8% YOY increase. While the cutout has been largely rising since January, retail prices in March were actually lower than they were at the end of 2023. Retailers’ slowness in passing on price increases has probably played a role in keeping consumer pulls strong in 2024. Next week, watch for further gains in cash hog prices and probably another dollar or two higher in the cutout. Some recovery in the futures also seems likely.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}