Pork Wrap April 1

Price direction in the hog and pork complex isn’t very easy to discern

right now. Last week it looked as though the combined margin might

be making a bottom and we were on the cusp of a new upcycle in

demand. This week however, the market didn’t follow through and

that raises the potential that it was just stalled for a bit and the

downtrend will remain in place. The price changes weren’t big this

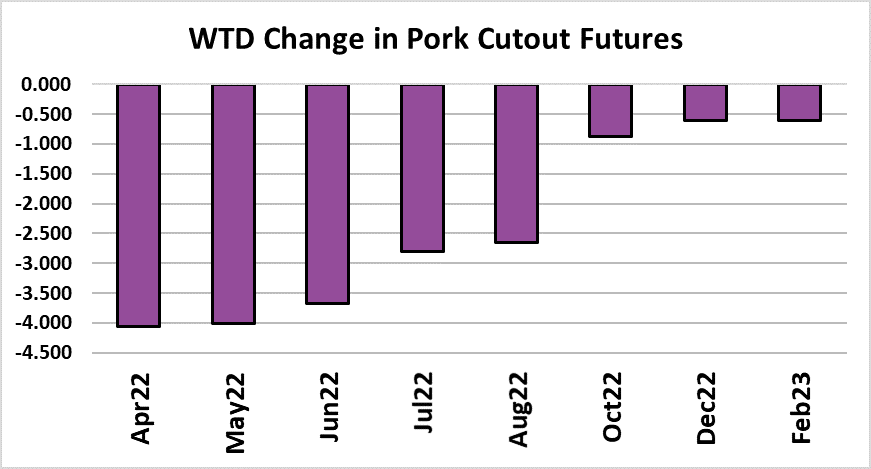

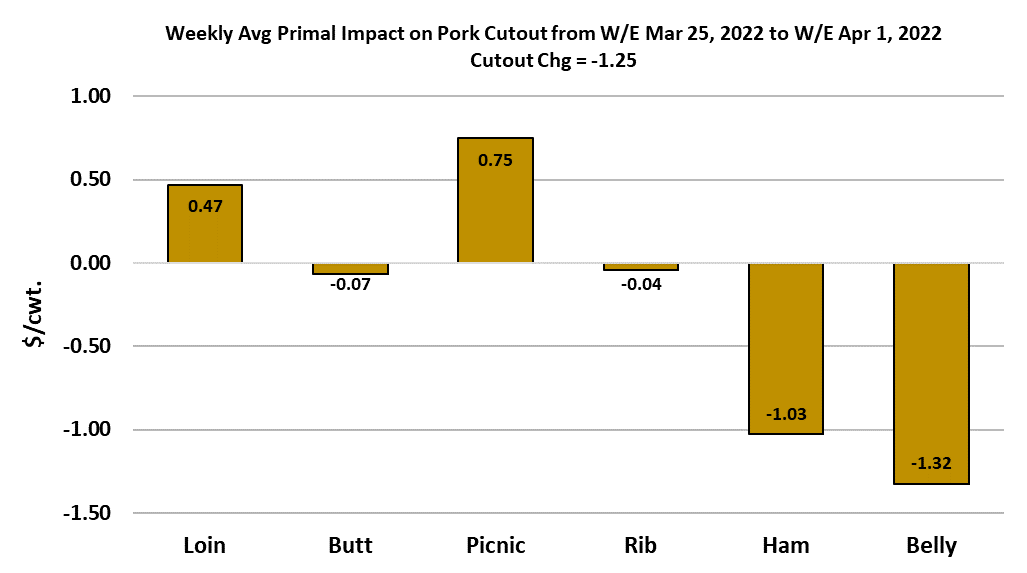

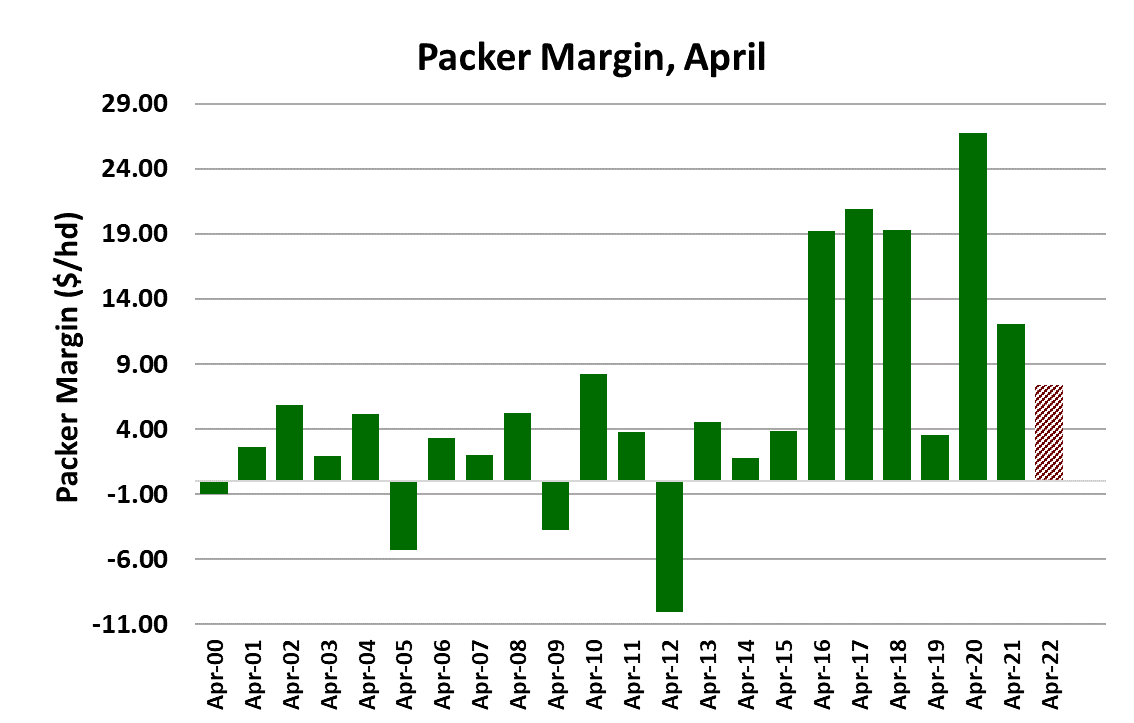

week, but they were mostly negative. The cutout dropped $1.25 on a

weekly average basis and the WCB negotiated market was $3.70

lower. The lower negotiated market takes some of the pressure off

of packers to boost the cutout in order to protect their margin, but their

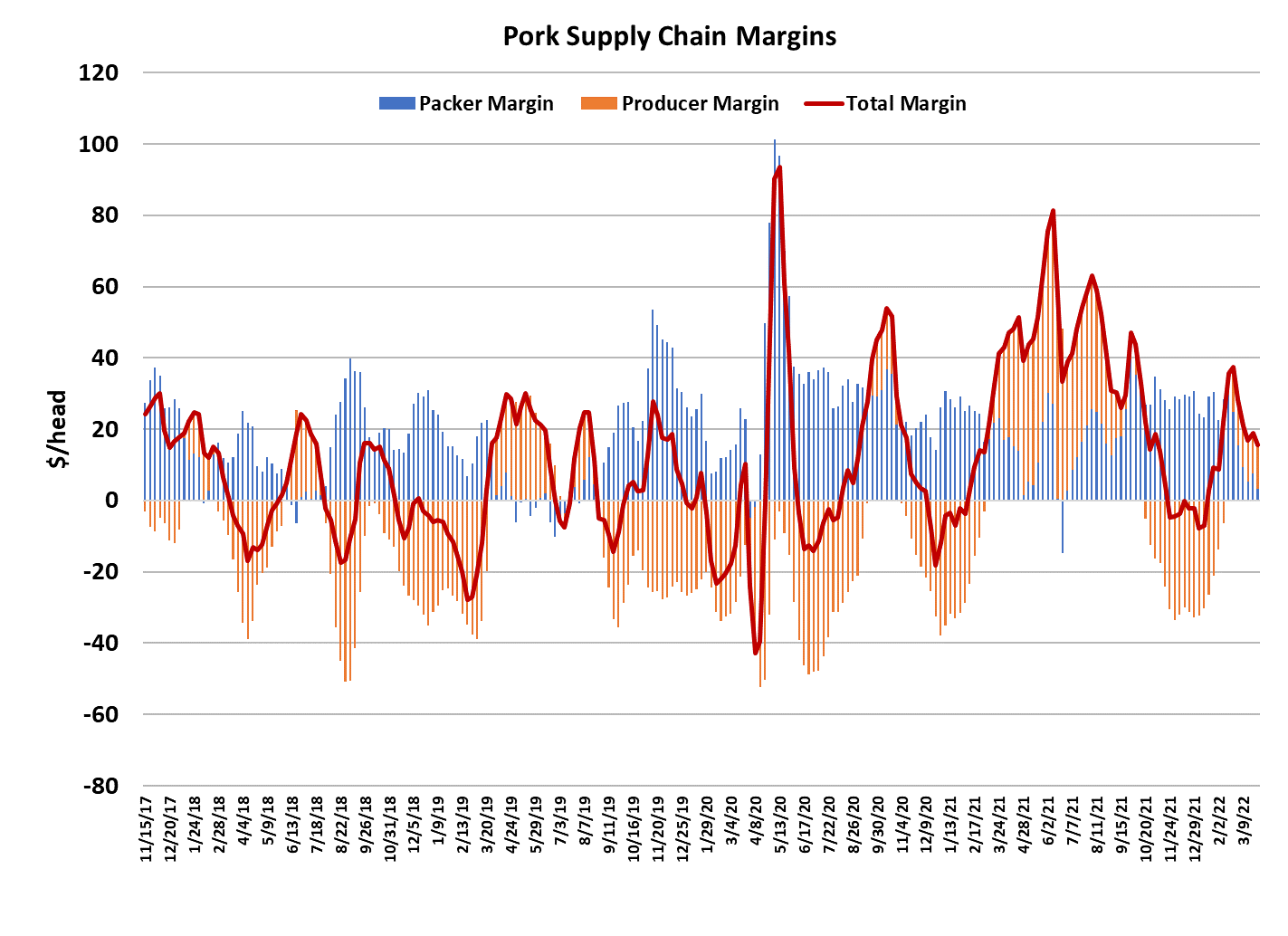

margin still isn’t very healthy. I calculate this week’s margin at only

$1.83/head. Last year at this time packers were making $17/head. I

couldn’t help but notice that during the PEDv crisis back in 2014, it

was late March/early April when the WCB negotiated market made its

top and turned lower.

Perhaps that marks the point in the calendar when the supply

tightness driven by disease starts to ease. This week’s Hogs and

Pigs report did point to some moderate disease issues in the herd as

both the number of sows farrowing and pigs saved per litter were well

below expectations. Maybe we are now moving past the peak in

those problems. It is worth noting that back in 2014 the cutout

followed the negotiated hogs lower from early April to Memorial Day.

Could we be looking at a mini-version of what happened back in

2014? Possibly. The cutout did start to look much softer towards the

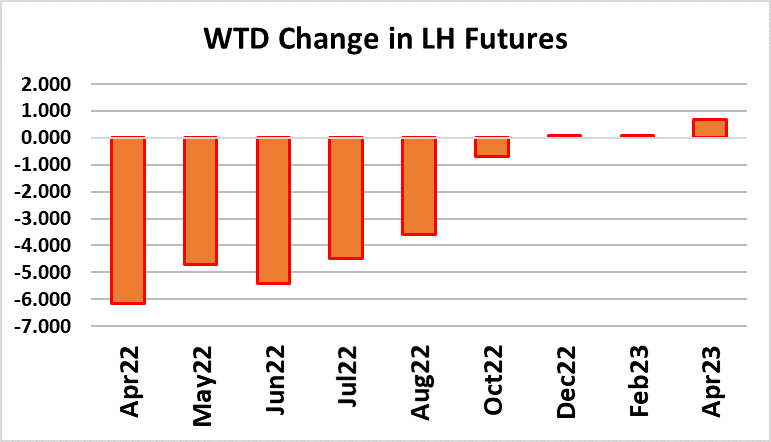

end of the week and futures traders took notice, causing the Apr

contract to lose over $6/cwt. It is the bellies that are creating the most

concern right now. It is starting to look like the belly primal headfaked us with two stronger weeks in the midst of a downtrend that

started in late February.

On Monday, the belly primal printed $204 and by Friday afternoon, it

was down to $173. You can see why traders are concerned. To

make matters worse, the ham primal now seems to be softening up.

Here also, it looks like the hams gave a two-week head-fake that

made it look like they would be strengthening back in mid-March, but

now the data seem to support a continuation of the downtrend.

Outside of the bellies and hams, the rest of the carcass performed

relatively well this week, so all is not lost. As of now, the fundamental

forecast doesn’t have the cutout dropping below $100 in the nearterm, but I must admit that the odds of that seem to be growing by the

day and next week’s forecast revision might tell a different story. If

overall pork demand is going to continue to soften for a few more

weeks, then it will be up to seasonally smaller pork production to

provide support. This week’s kill registered 2.44 million head, about

33,000 more than last week.

That was still pretty close to what the pig crop projected, but my

concern lies with next week’s kill where there are already indications

that packers will slaughter more animals on Saturday and thus the

weekly total could expand out to 2.48 million head. That is going in

the wrong direction for this time of year—kills should be getting

progressively smaller, not larger. If my forecast of a 2.48 million

head kill for next week is correct, that would be about 100k more

than the pig crop indicated. Easter is two weeks down the road and

we should see a modest reduction in slaughter that week. Perhaps

next week’s bigger planned Saturday is designed to compensate for

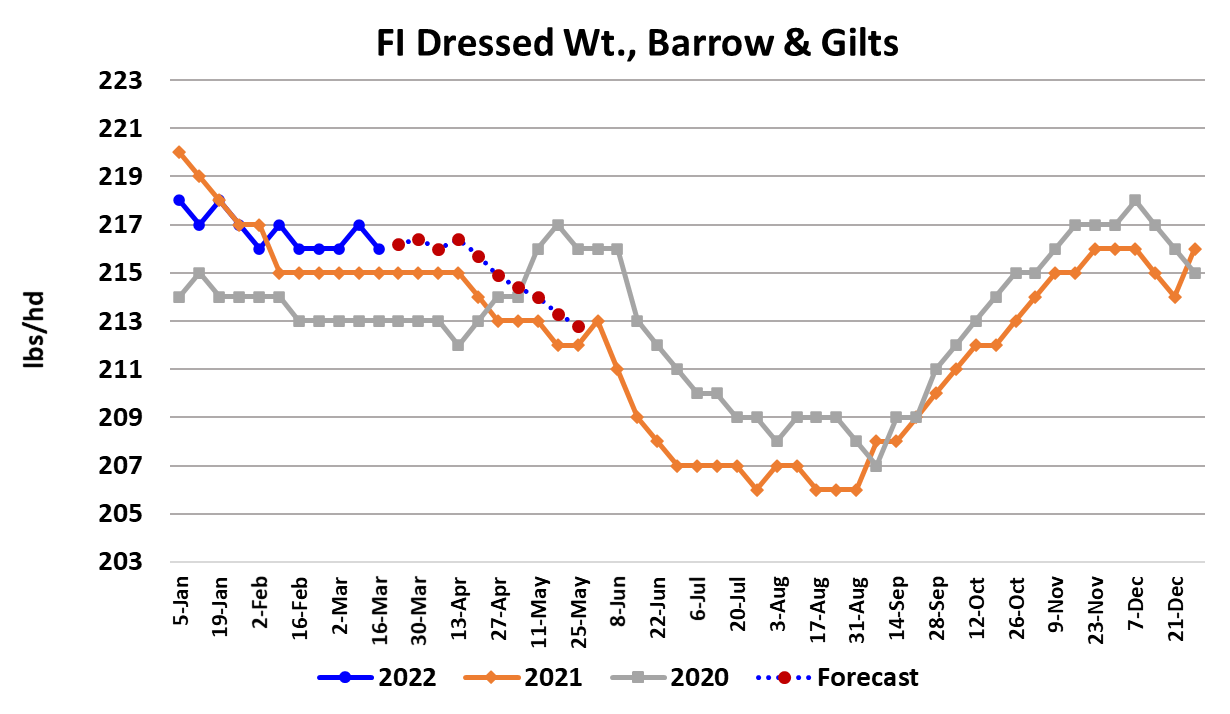

a smaller slaughter during Easter week. Barrow and gilt weights

were reported down one pound this week and are only slightly

above last year at present. Thus, the weight data doesn’t seem

to indicate any problems with the production pipeline.

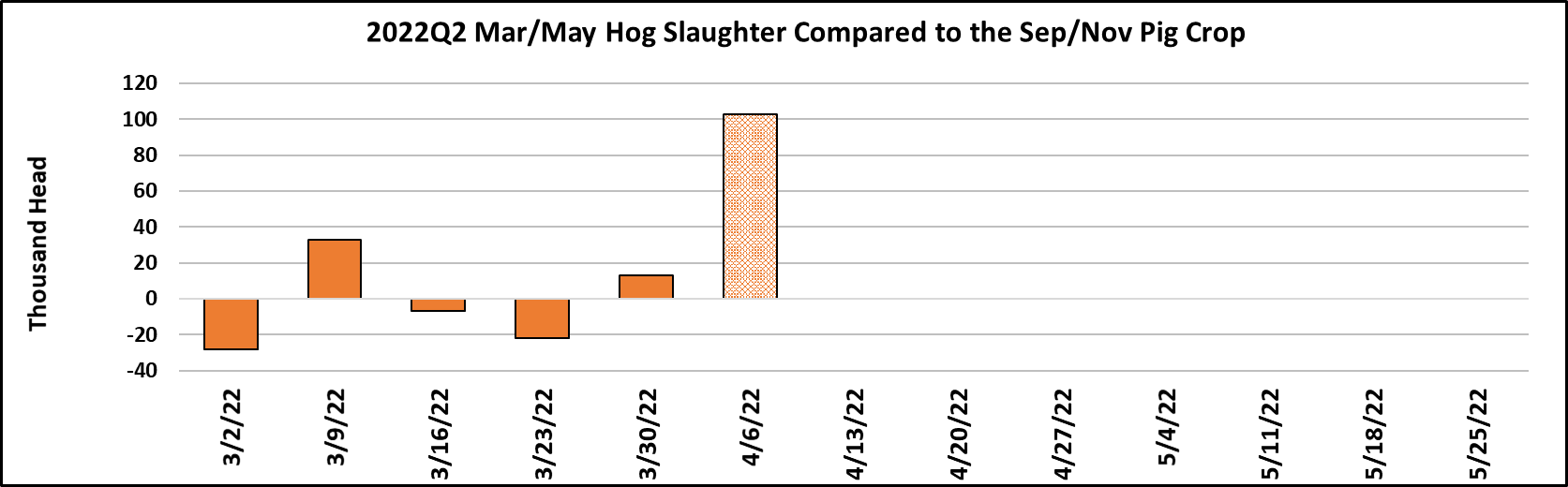

USDA released the result of their quarterly Hogs and Pigs survey

this week and it showed more contraction in the herd than

expected. The breeding herd was estimated to be down almost 2%

YOY when the average trade guess was for a steady breeding herd.

That suggests smaller pig crops in the future and is likely what

supported the back end of the futures curve this week while the

front months were moving lower. The Dec/Feb pig crop was 1%

less than last year and those are the hogs that will be slaughtered

from June to August, so we can expect roughly 1% smaller

hog slaughter this summer compared to last. That is significant,

but not game-changing, and it doesn’t in any way imply that pork

prices will be higher this summer than last year. The supply picture

is only half of the price equation. Demand will have a lot to say

about price levels also and my guess is that demand will fall well

short of the phenomenal demand we saw last summer. In

addition, the export picture is looking a lot softer than it was last

year.

As a result, the fundamental forecast has per capita availability for

the Jun/Aug quarter down only slightly YOY. To be sure, once I

input the numbers from USDA’s survey, it raised price forecasts for

the balance of 2022, but that only erased a small fraction of the

over-pricing that I’m seeing in the deferred futures. My

assumption has always been that the deeper we get into the

year, the softer demand will become. Futures traders are unlikely

to factor in significant demand weakness until they see it

happen. Perhaps we are just on the cusp of that now. Next week,

watch the bellies and hams because that is likely to be what either

drags the cutout down or boosts it higher. Also watch

the negotiated markets for further weakness that would signal the

top in that market has been made.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}