Pork Wrap April 09

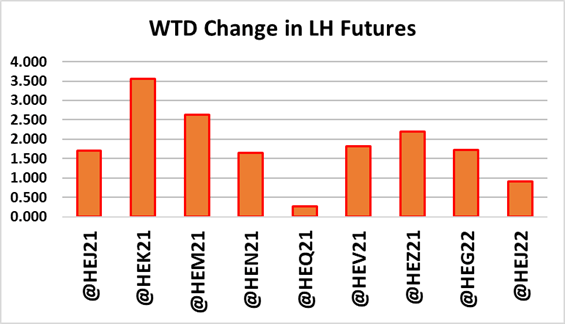

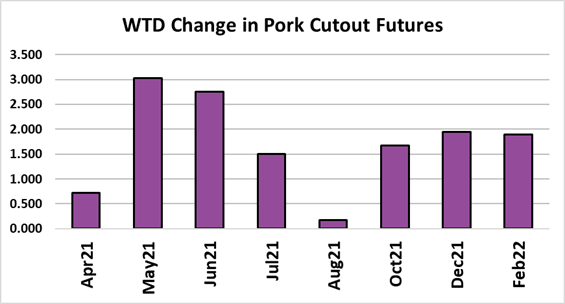

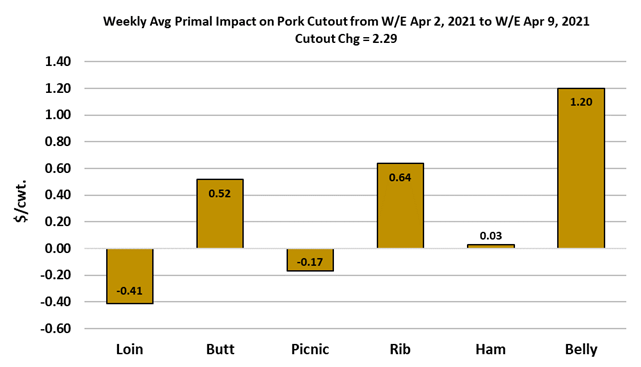

This week the pork cutout added a little over $2 on a weekly average

basis and the WCB negotiated market added a little under $2. So, the

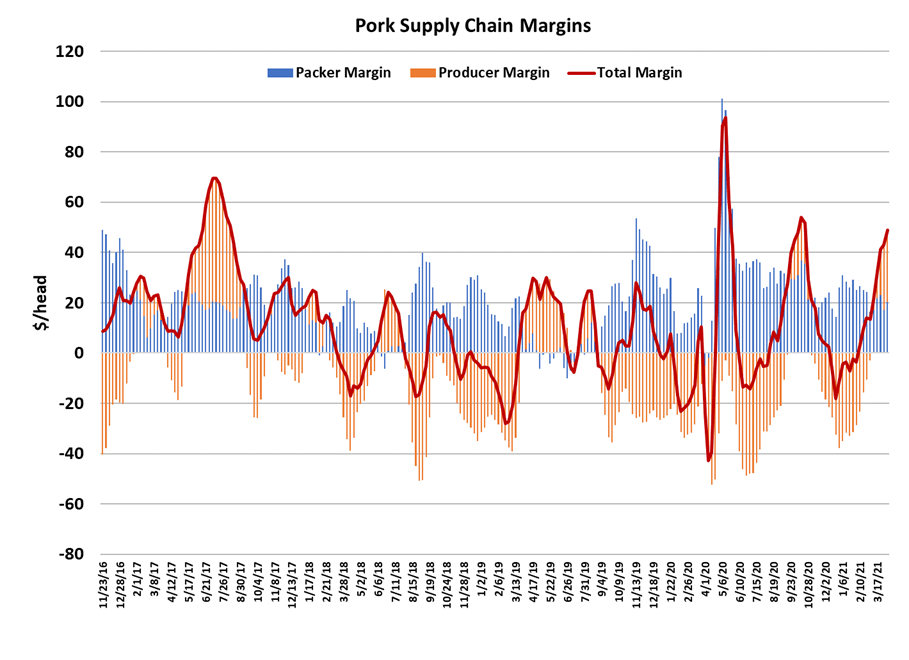

markets are still working higher—no change there. Packer margins

increased a tad to $18.20/hd. All of the same supply/demand dynamics

that have been in play for the last few weeks—tightening supply, strong

demand—remained in place this week. This swine kill came in at 2.49

million head, with packers using a big Saturday kill to offset a very soft

kill on the Monday following Easter. That kill was a little larger than

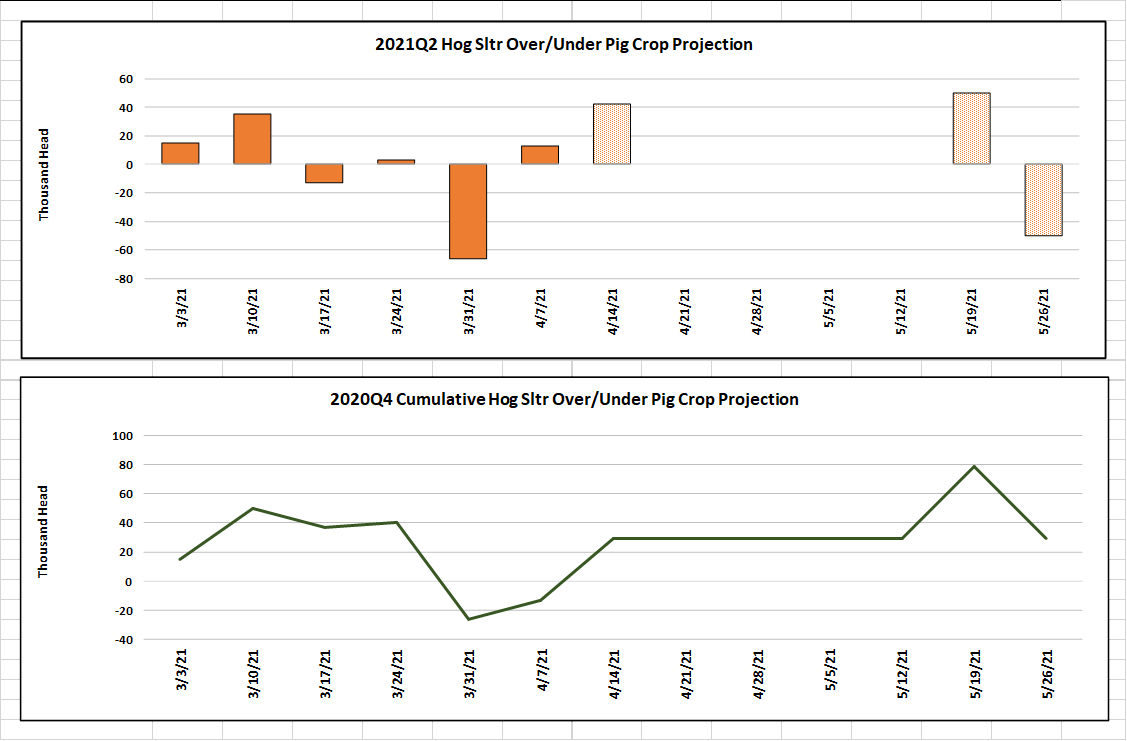

what the pig crop suggested (chart to right), but not by a lot. As of right

now, the cumulative over/under kill for this quarter is very close to zero,

so there is no reason to think that the USDA survey got the pig crop

wrong. Barrow and gilt carcass weights remained flat at 215 (+2

pounds YOY) in this week’s data, so no surprises there. The supply

side of this market is behaving as expected.

It is the demand side that is causing all of the fireworks. Further, it is

domestic demand that is driving prices higher, not surging international

demand. This week USDA released trade data that showed pork

exports in February were down 10.1% YOY. That was expected, since

the weekly data has been running consistently below year ago since the

beginning of 2021. So, if the price strength isn’t being driven by a

supply restriction and it isn’t being driven by strong export demand, then

there is only one possible culprit left: domestic demand. The combined

margin chart to the right shows a pretty strong move higher this week after looking like it might be trying to peak last week. Recently, I’ve said that this market reminds me a lot of the Atkins Diet fad back in the early

2000s and the longer this demand strength goes on the more it

resembles that market situation. If it is true that some shift in the

public’s dietary patterns has occurred and that shift causes them to

demand more animal protein, then this demand strength could last for a

long time. In that situation, what I think we would see on the combined

margin chart is a long, relatively sideways pattern start to develop. You

can see from the chart to the right that the combined margin has rarely

plateaued. It is almost always going either up or down. It is worth

keeping an eye out for that.

One thing that makes me think that this is something different from the

many demand cycles we have seen in the past is that it seem to be

affecting all of the animal proteins at the same time. A big part of what

drives normal demand cycles in retailers switching from a relatively

pricey protein to a more attractively priced one. So, it is not very

common to have all of the protein demands in an strong upcycle at the

same time. When they do all show strength at the same time, it makes

me think there is something beyond the normal retailer-driven cycle

going on.

Another thing that would impact the demand of all proteins in

relatively the same way at the same time, is growth in consumer

disposable income. Three rounds of stimulus checks have been

sent to US consumers in the past year and so it is also possible

that this demand surge is being driven by stimulus money.

However, pork demand started strengthening way before the most

recent (and largest) stimulus checks were issued. I have to think

that the stimulus payments are helping this demand cycle along,

even if they are not the primary cause of it. The other things that

get mentioned but I don’t really think are doing much to boost

demand are:

1) Increased vaccination rates causing an increase in consumer

confidence and thus spending and,

2) Increased foodservice demand as the economy reopens.

The latter seems to be the one that gets the most attention and I

will grant that there could have been a modest demand pressure

from foodservice operations rebuilding inventories in anticipation

of reopening, but that rebuilding of inventories is a one-time event

and once that is done then meat sales at foodservice takes away

from sales at retail and any demand strength created shouldn’t

persist. Further, the demand index data indicates that red meat

demand improved during the pandemic compared to where it was

prior. If that was due to the shift in consumption from the

foodservice channel to the retail channel, then movement back in

the other direction should be negative for meat demand.

At this point I’m leaning strongly toward either a dietary shift or

stimulus money, or both, driving this demand shift. Understanding

the cause of a demand shift is important because it will help us to

better gauge how long it will last. The futures market thinks it will

last for quite a long time given the way it has priced the summer

and fall contracts. My fundamental forecast is not as generous,

but I’m assuming that this demand cycle will turn lower in a

reasonable time frame like all the others before it. If something

structural has changed (like dietary patterns) then the fundamental

forecasts will likely prove too low. Next week, watch the daily

demand scatters since those will give the first indication if demand

were to soften, but remember that it takes several consecutive

down days to confirm the trend has turned.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}