Beef Wrap October 1

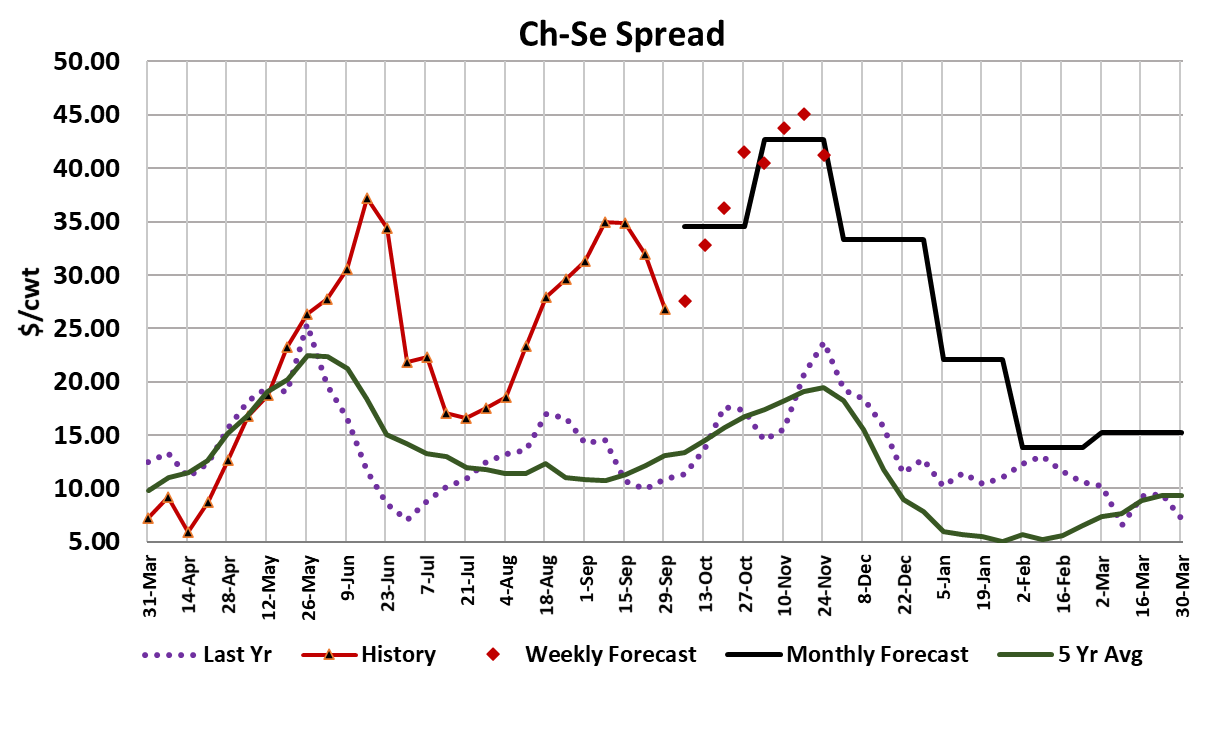

Cash cattle averaged a dollar lower this week at $122.65, but other

than that, it was more of the same in the cattle and beef complex

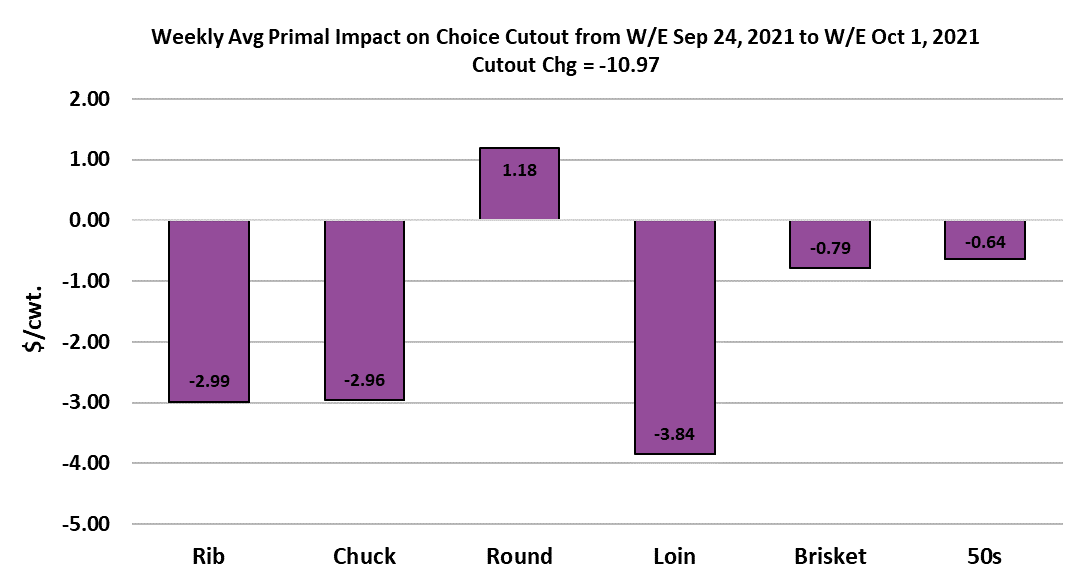

this week. The cutouts continued lower, with the Choice down

almost $11 on a weekly average basis and the select down a little

less than $6. That compressed the Choice-Select spread down to

$27 from $32 the week before. The rapid decline in rib prices is

primarily driving the spread lower. I don’t expect it to get a whole

lot narrower from here and am forecasting it to expand back out to

over $40/cwt near the end of October. The chart below indicates

that all of the primals except the round were contributors to this

week’s drop in the cutout.

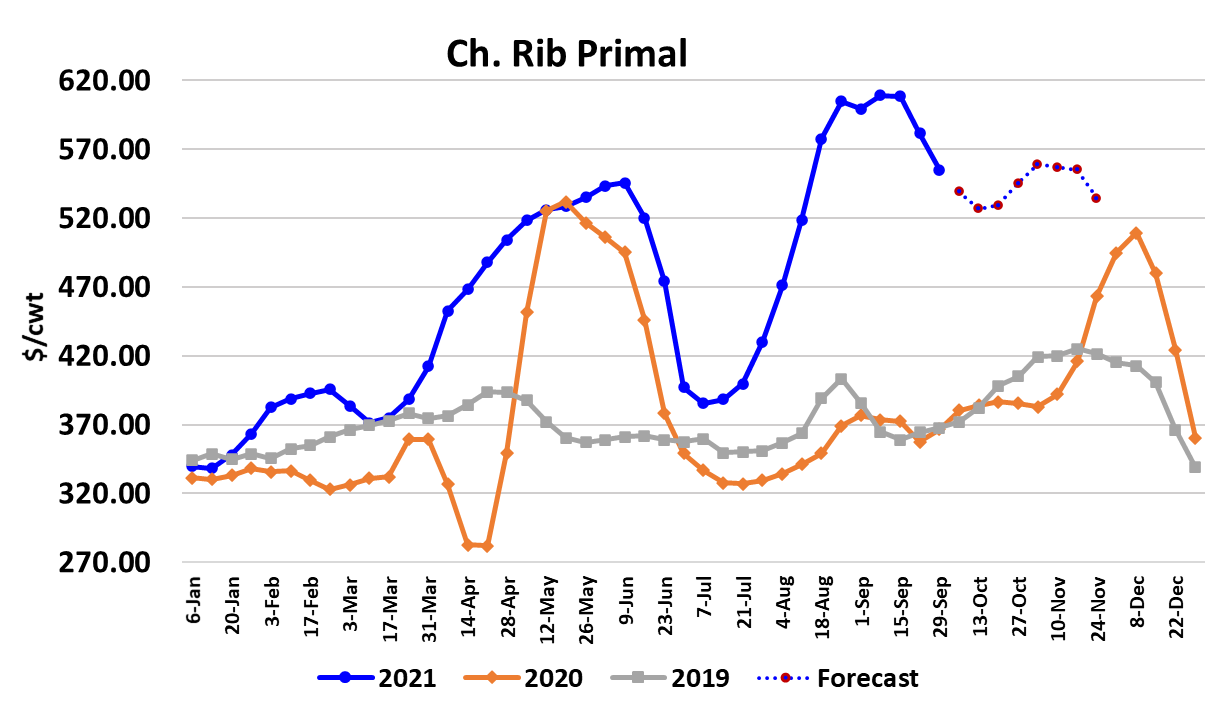

While it felt like the ribs were the major contributor, they actually

had a similar impact on the cutout as lower chuck prices did. It has

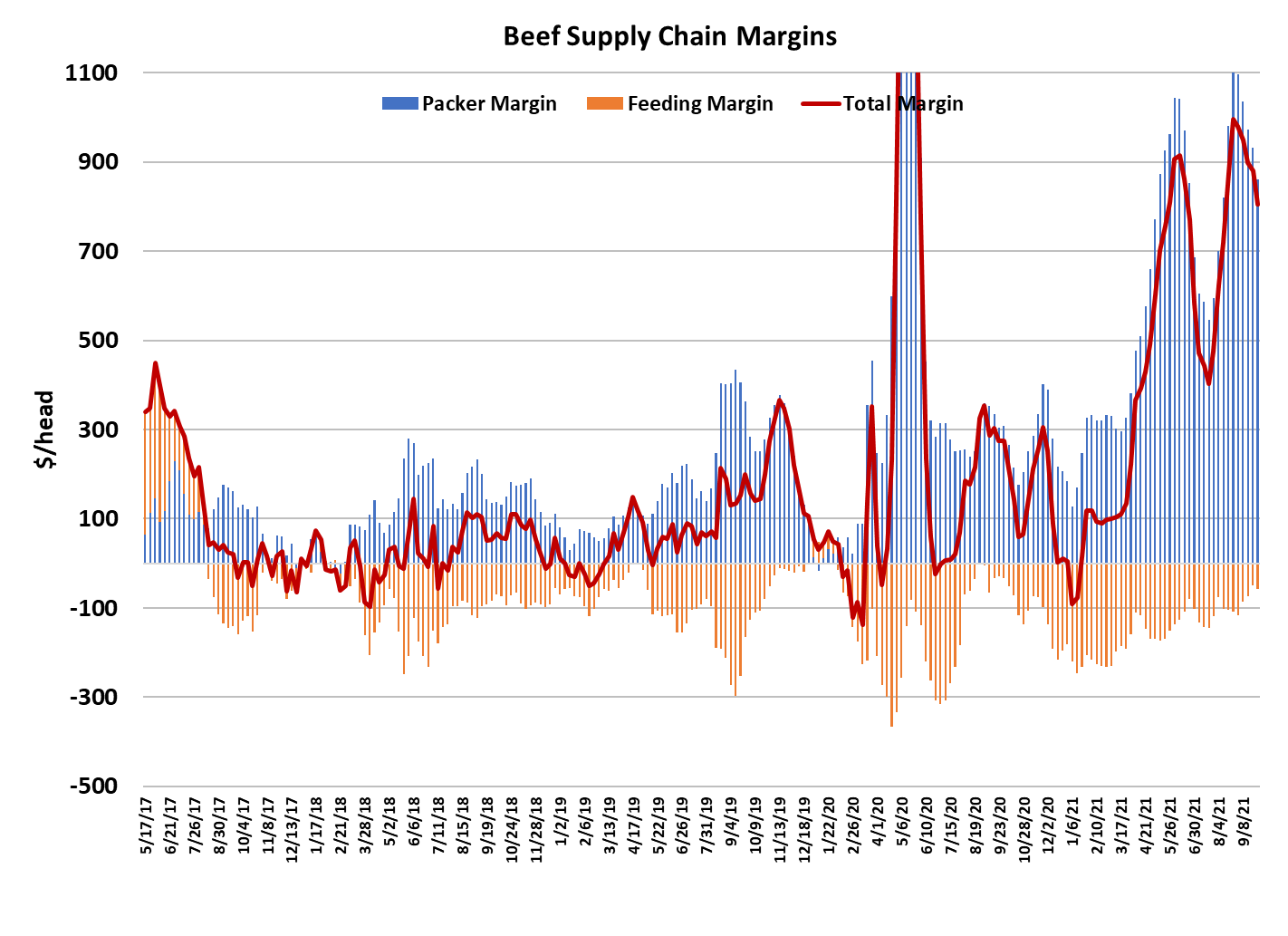

been clear from the daily demand scatters that beef demand is

softening and the combined margin chart points in that direction

also. We know that almost all of the price softness must be

attributable to weaker demand because beef production hasn’t

changed all that much, now estimated at around 537 million

pounds per week. The fed kill was disappointing this week,

registering only 492k as some cooler cleanings were going on and

the Saturday kill wasn’t boosted to make up for that. The flow

model tells me that in October the fed kill needs to run about 505k

per week in order to not backup any additional cattle. We have

probably already backed up about 20-30k from September. All that

means is the cattle supply will remain ample this fall, while the beef

supply will be constrained by packer’s ability to get them all dead in

this tight labor environment.

So far, carcass weights seem to be behaving normally as they rise

toward a peak in early November. This market isn’t very

complicated at the moment. It is clear that the cattle supply

modestly exceeds the packers ability to kill them and that has kept

cattle prices in check. The beef market is resetting after moving to

super-strong levels late in the summer. And everyone is just

watching the beef come down and waiting for it to find a bottom.

Once beef prices catch however, things could get interesting.

Buyers may rush in at that point and thus create a V-shaped

correction because they remember how fast prices rose this

summer. I’ve revised my thinking a bit on the ribs going into the

holidays. Now I look for them to decline for 2-3 more weeks and

then see a modest increase into late November, but I’m not

expecting the top this fall to exceed what we saw in late August.

That change in the forecast pattern for ribs has also altered the

pattern for the cutout, so that it doesn’t decline quite as rapidly as

I had forecast before. I’ve got the end meats posting some

modest gains over the next couple of weeks, but then trending

lower right into December. Beef 50s fell hard this week, losing

$25 Friday-to-Friday and finishing up today at $103. 90s are also

slowly working lower as seasonally larger cow kills are providing

some supply side pressure. That will eventually make the grinds

look more attractive to retailers, but I’m not sure the consumer is

all that fired up about grinds at this time of year.

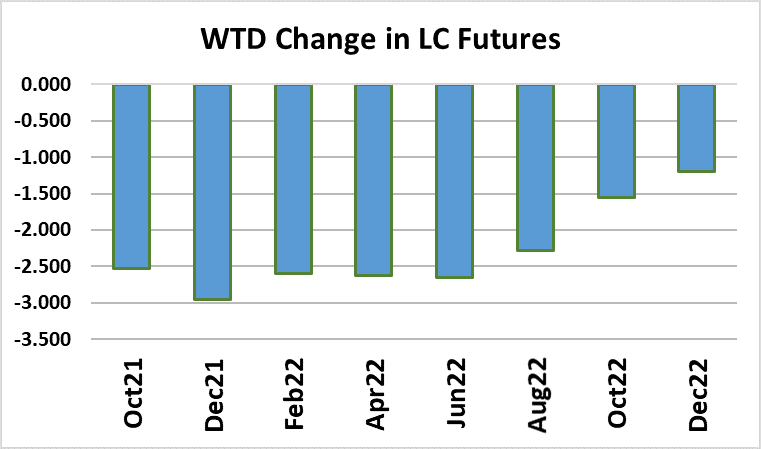

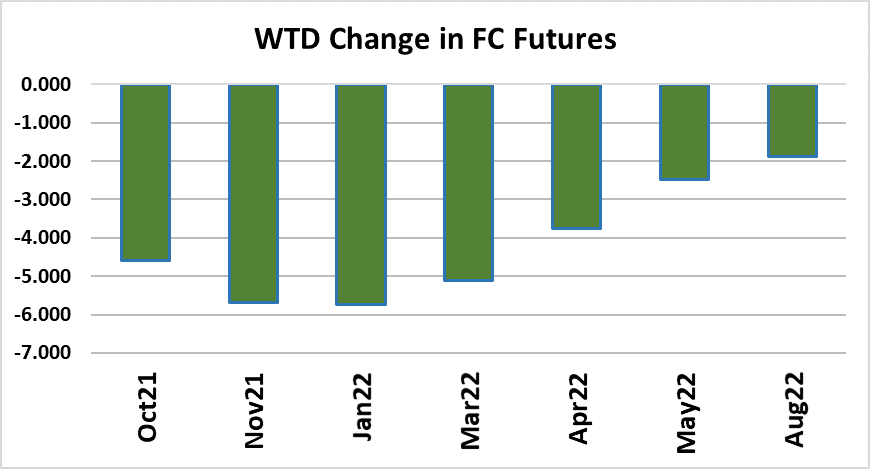

Futures traders showed they are running out of patience this

week, pushing the cattle curve down by $2-3. It is becoming

painfully clear that as long as the labor bottleneck is affecting

plants, the price of cash cattle isn’t going up. So with each

passing week, the premiums on deferred futures look less and

less attainable. The October contract will enter its delivery period

on Monday, but is trading over $3 under the spot market so there

isn’t much risk of deliveries occurring. It looks to me like the Oct

contract is demonstrating more pessimism than is warranted and

it will likely put some money back on as it moves through October.

A rising October however, does not guarantee that the rest of the

curve will move higher with it. Export demand for beef continues

to look very good in the weekly numbers that we watch.

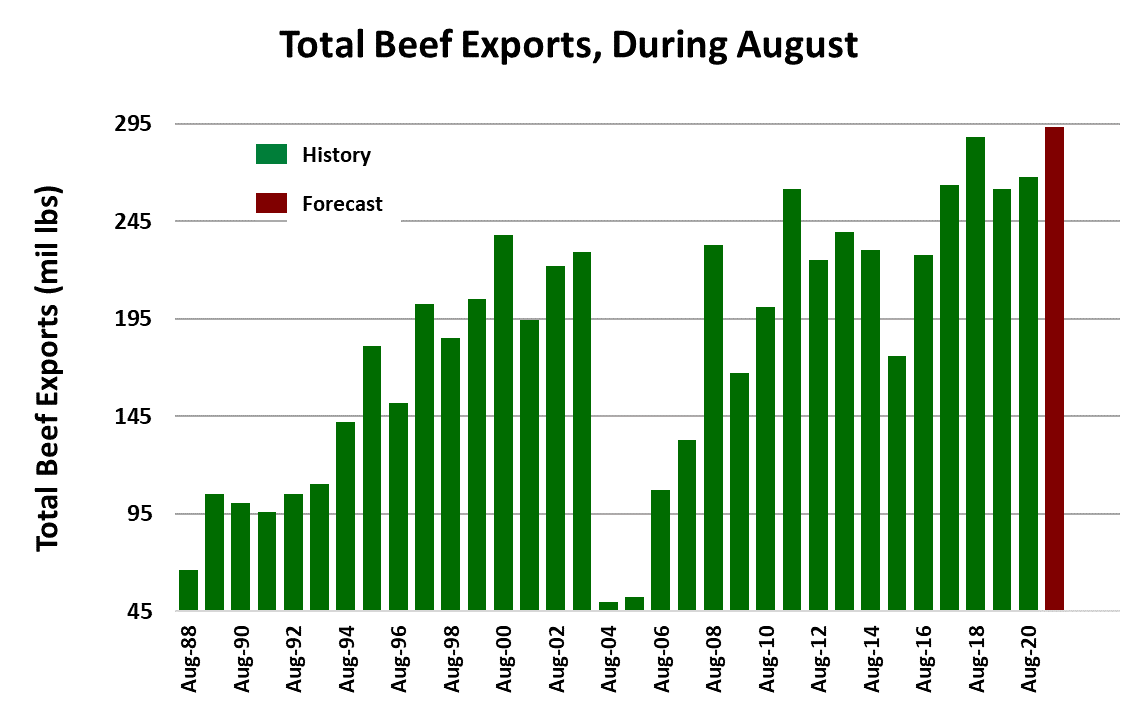

The official monthly export data from ERS for the month of August

will be released Wednesday. I’m expecting it to show about a 9%

YOY increase. China continues to be a big customer for US beef

and I don’t look for that to change anytime soon. Next week it will

be more of the same, with everyone sitting on the edge of their

chair waiting for the cutouts to find a bottom. I don’t expect that

will happen next week, but it could materialize by mid-month if the

ribs get low enough to attract those that still have unmet needs for

the holidays.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}