Beef Wrap March 22

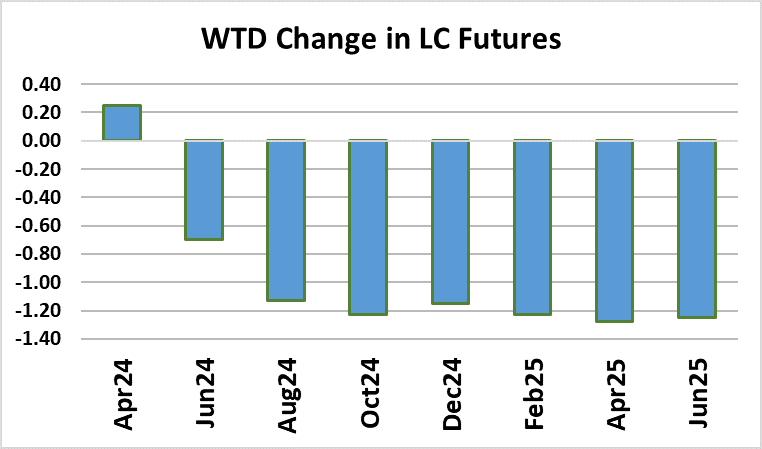

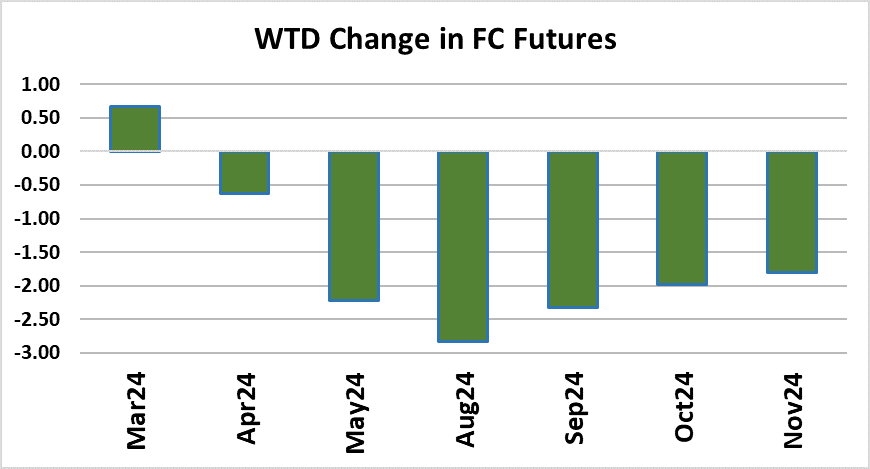

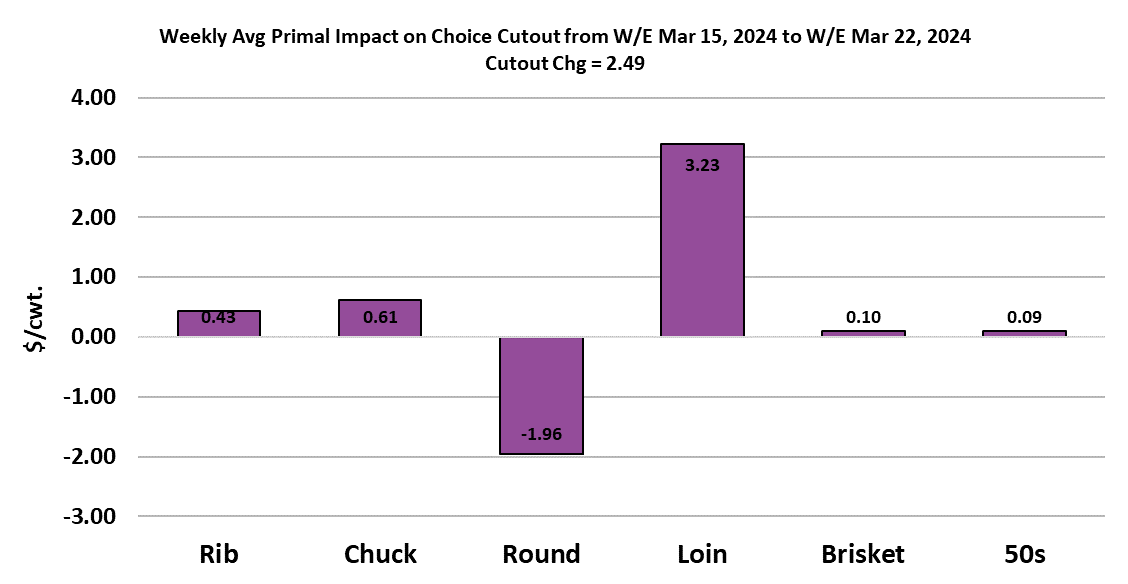

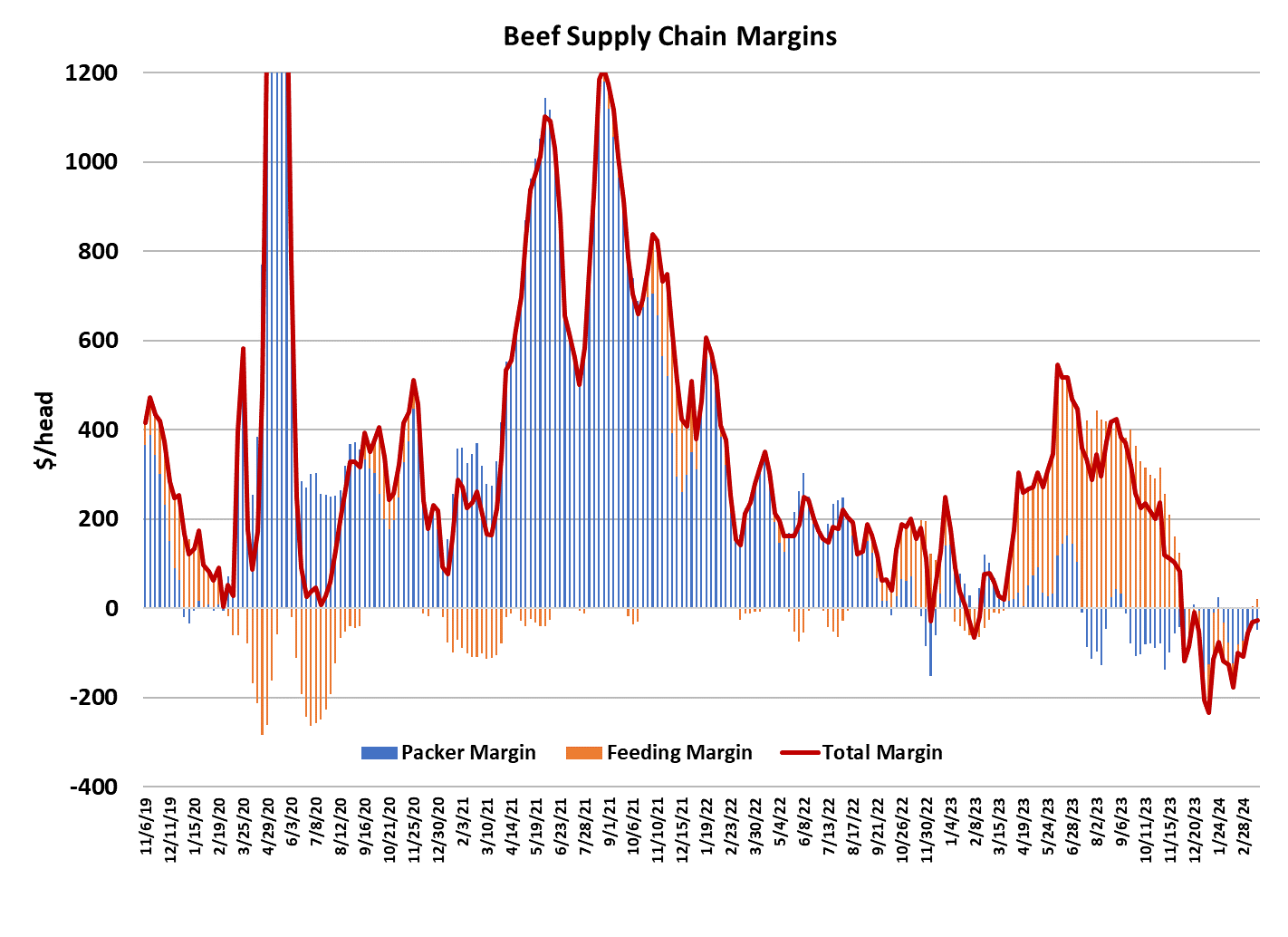

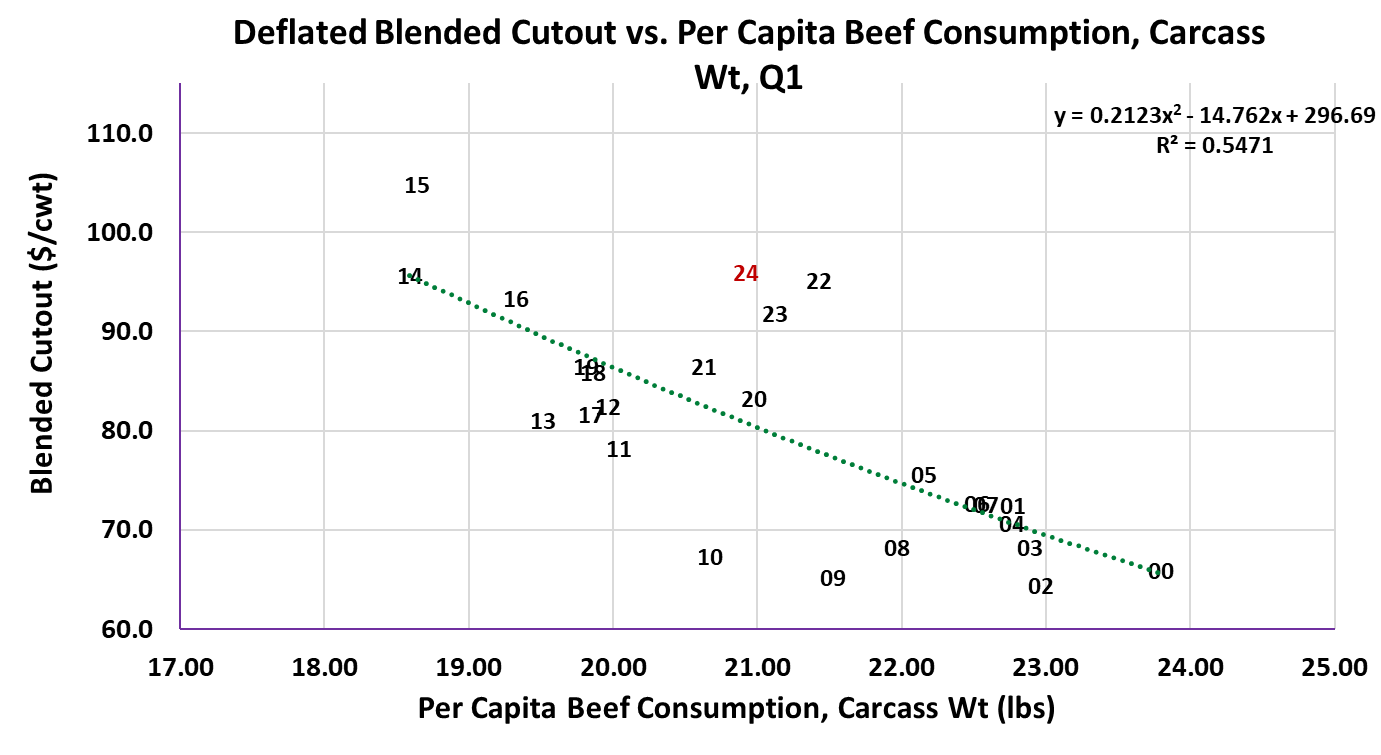

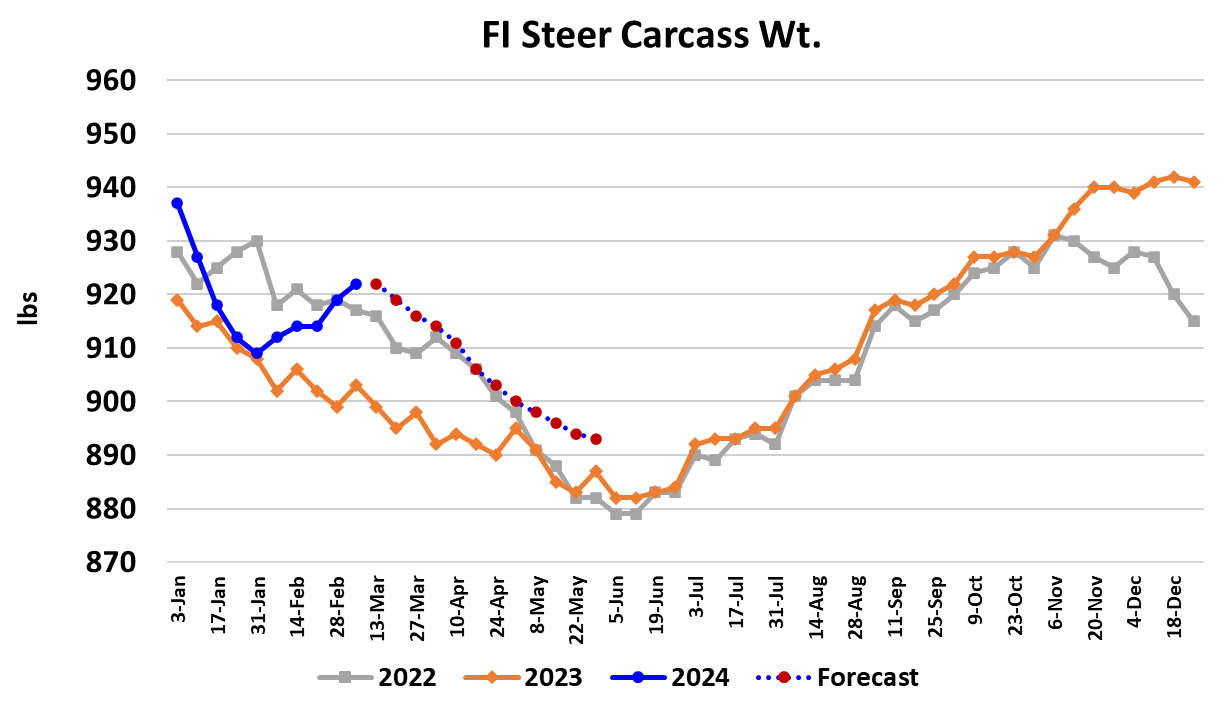

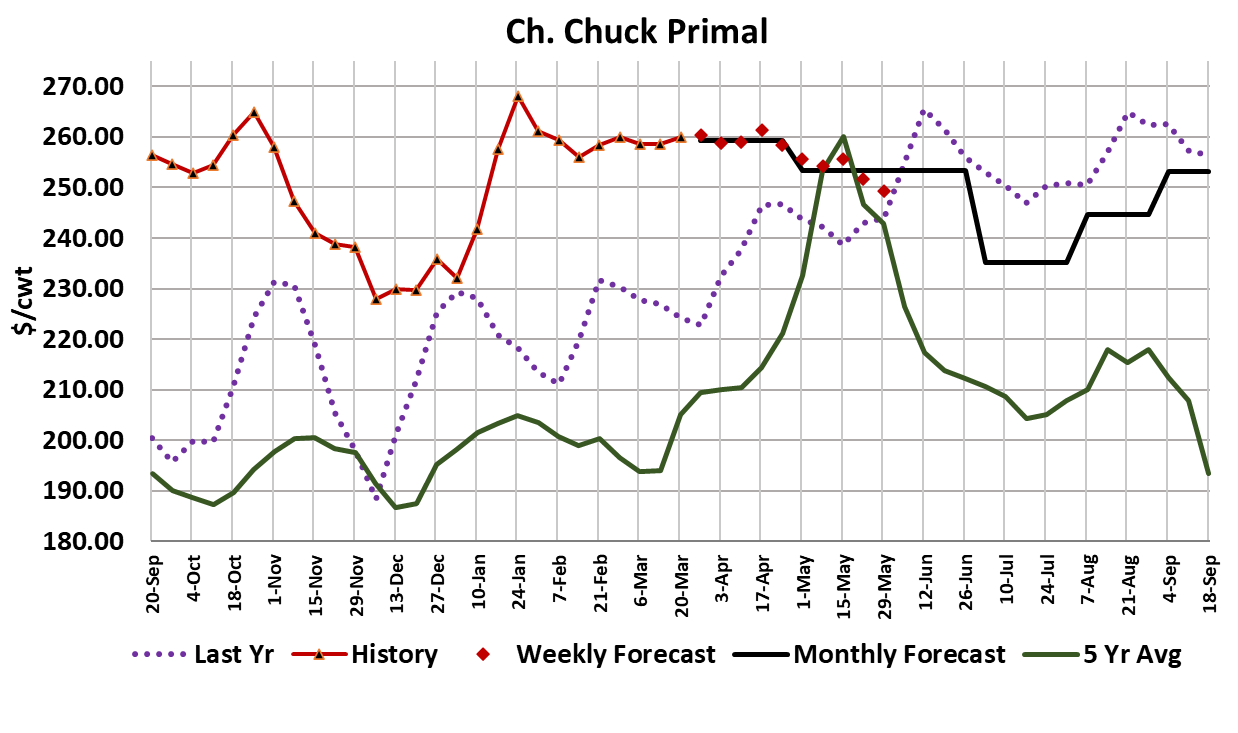

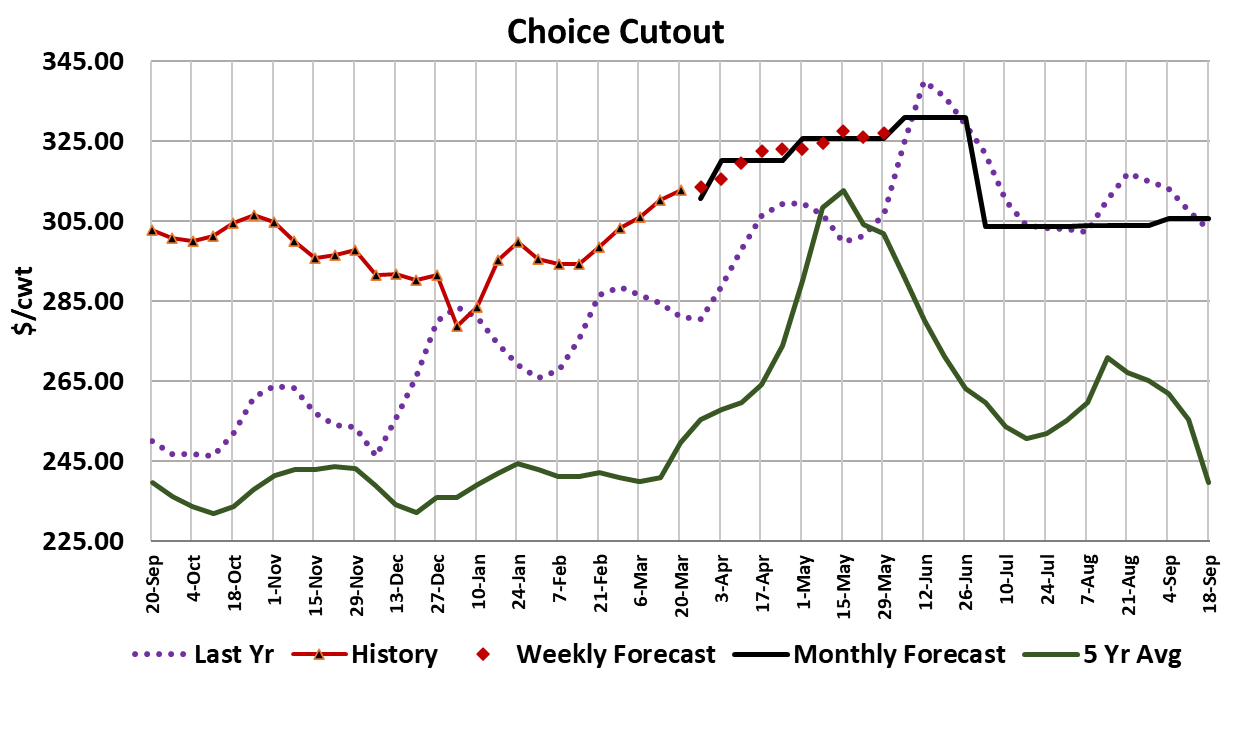

Beef packers managed to keep beef prices moving higher this week, with the Choice cutout adding $2.49/cwt. on a weekly average basis and the Select cutout gaining $2.10/cwt. However, by the end of the week the cutouts were showing some signs of fatigue. Cattle feeders managed to wrangle another $2+ gain in the cash cattle market this week. When all of the data is complied on Monday, I’d expect the 5-area live price to be close to $189.60, which would be the highest weekly price ever paid for fed cattle. Cattle prices in the North are now holding a $2-3 premium over the South and that is a normal seasonal that is expected to persist through the spring. Last year in April through August, the northern premium was exceedingly large, averaging close to $7/cwt. That was an outlier, but we could certainly see a $4-5 premium emerge this year. Of course, the question on everyone’s mind is whether or not this week’s gains mark the spring top in cash cattle prices. If it does, it would be a little early since we typically don’t see the cash market top until sometime in the mid-April to mid-May timeframe. Last year, the market made a top in the second week of April, pulled back for a few weeks, then surged to an annual high in early June. The early data suggests that packers bought nearly 100,000 head of cattle this week in the negotiated market and that would be the largest weekly trade volume since the first week of October. The conventional wisdom suggests that when packers boost their live inventory like that, they won’t need to be as aggressive in the cash market the following week. However, it also means that a lot of cattle were cleared out of feedyards and so it lessens their need to move cattle in the following week. The situation is further complicated by the fact that next week is Easter week and thus weekly slaughter is likely to be somewhat depressed by light kills on Good Friday and the following Saturday. This week’s fed kill tallied 476k, the same as the week before, but larger than the 460-465k kills that we saw in late February. Packer margins declined to -$48/head as the increase in the cutouts didn’t quite cover the cost of the more-expensive cattle they bought the week before. I’m not ready to forecast the cash cattle market lower at this point, but think the gains will slow down in the next couple of weeks. Once we get past Easter week, the cutouts should get a boost from renewed interest on the part of retailers looking to feature beef in the early weeks of the grilling season. If the weather in early April turns out to be chillier than normal, it could put a damper on beef movement, but so far this spring temperatures in the lower 48 states have been well above normal and there is no reason to think that won’t continue. This week the loin primal was the biggest contributor to the cutout’s gain and I’d expect that to be true again next week. This is the time of year when loin prices start to ramp higher, with rib prices joining the party a little later. Both ribs and loins are priced above last year currently and I’d expect that to remain the case right through the summer. End meat prices are showing larger YOY gains than the middle meats so far in 2024. Both the chuck and round primals are likely to post 15% YOY price increases for Q1 and briskets should be up over 20% YOY in Q1. That makes sense given how strong the lean trim market has been. 90s appear poised to post a 17% YOY increase for Q1. As long as the 90s remain elevated, it will be difficult to push end cut prices lower. Trimmed shoulder clods are currently reported near $330 in the negotiated market and, when ground, that is a pretty good substitute for beef 90s which averaged $333 this week. Pastures in the cattle producing states are in much better shape this spring compared to last, so it is reasonable to expect more cows to stay on the farm this spring, rather than go to slaughter, and that will limit the raw material for producing 90s, driving prices even higher as we move toward Memorial Day. Thus I think its likely that the end cuts stay well supported over the next few months. Couple that with the well-known seasonal price advance in middle meats during grilling season and we have a recipe for further appreciation in the cutouts. Right now, the fundamental forecast has the Choice cutout approaching $330/cwt. by Memorial Day. If I’m wrong about that, I’m probably too low. What kind of cattle price would that support? Well at a $330 Choice cutout, packers could pay close to $195 for cattle and not lose money. Of course, Apr/May is normally the time of year when packers realize some of their best profits so cattle might not get to that level. Cattle supplies typically expand in spring based on past placement patterns, so that tends to hold the cattle market in check, or even push it lower, while improving beef demand lifts the cutouts to the packer’s benefit. Last year, packer margins averaged around $42/head in Apr/May, but this year as we head into that time period, they are starting with margins that could be $50 or more in the red so it may be difficult for them to match last year’s profitability. This week, the FI data showed a 3-pound increase in steer weights, but a 3-pound decrease in heifer weights. It looks like this counter-seasonal surge in carcass weights may now have finally run its course and weights should resume the normal seasonal downtrend soon as they work toward a bottom in late May or early June. Weights are likely to remain well above last year for the foreseeable future as the industry tries to counter declining animal numbers by making each one a little larger. There is a blizzard forecast to hit the Northern Plains on Sunday and Monday and that has the potential to muddy up the feedyards in that area, thus curtailing weight gains for a while. I still don’t get the sense that cattle feeders are feeling much urgency to market cattle and until that happens, I’m reluctant to forecast the cash cattle market lower. They may get helped along in that direction by today’s Cattle on Feed report, which showed February placements up 9.7% YOY—a number that was about 3% stronger than the consensus forecast. Total on-feed inventories as of March 1 are now 1.3% larger than last year and cash cattle prices are 14% higher than last year. How can that be? Well, for one thing, beef demand in Q1 has been stronger than last year by a couple of percentage points. Another consideration is the weight distribution of cattle currently in feedyards. Perhaps this year there are fewer cattle currently market-ready and more that not quite ready yet. Keep in mind that for cattle feeders market-ready now means an animal that weighs 50 pounds more than it did last year. Packers are unlikely to push back against heavier carcasses at this point in the cattle cycle when animal numbers are so low. They need the extra tonnage too. Next week, watch for some wild action in the futures on Monday as traders adjust to the COF data that was released today and keep an eye on those lean trimming prices because they are likely to play a big role in how high cutouts go this spring.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}