Beef Wrap June 28

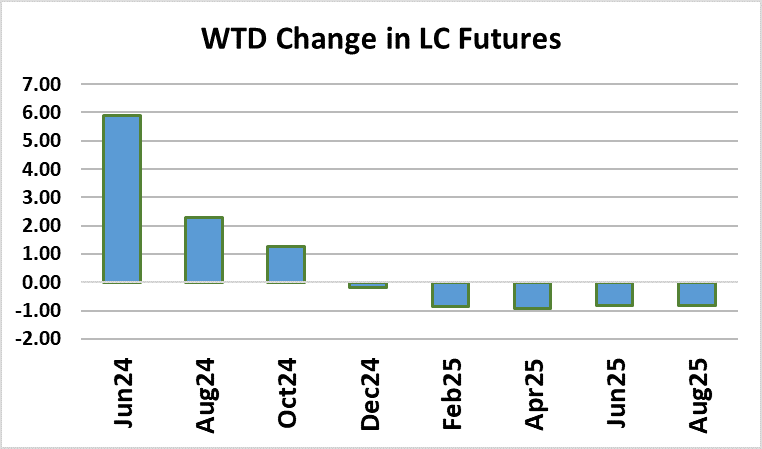

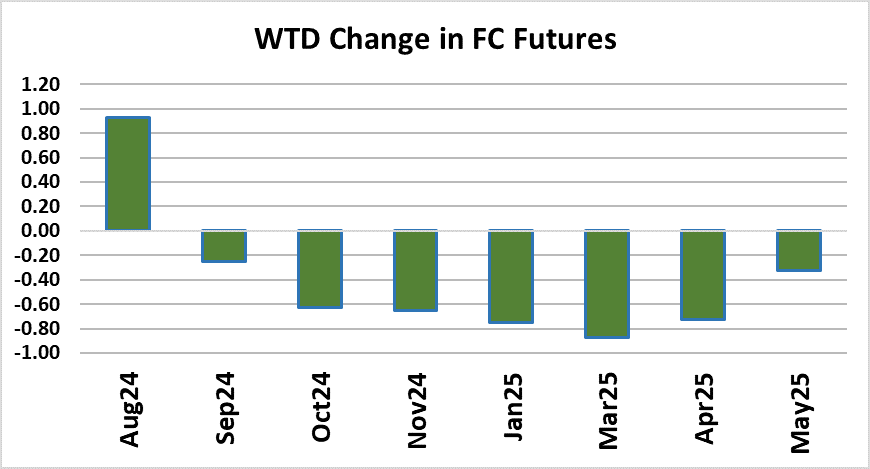

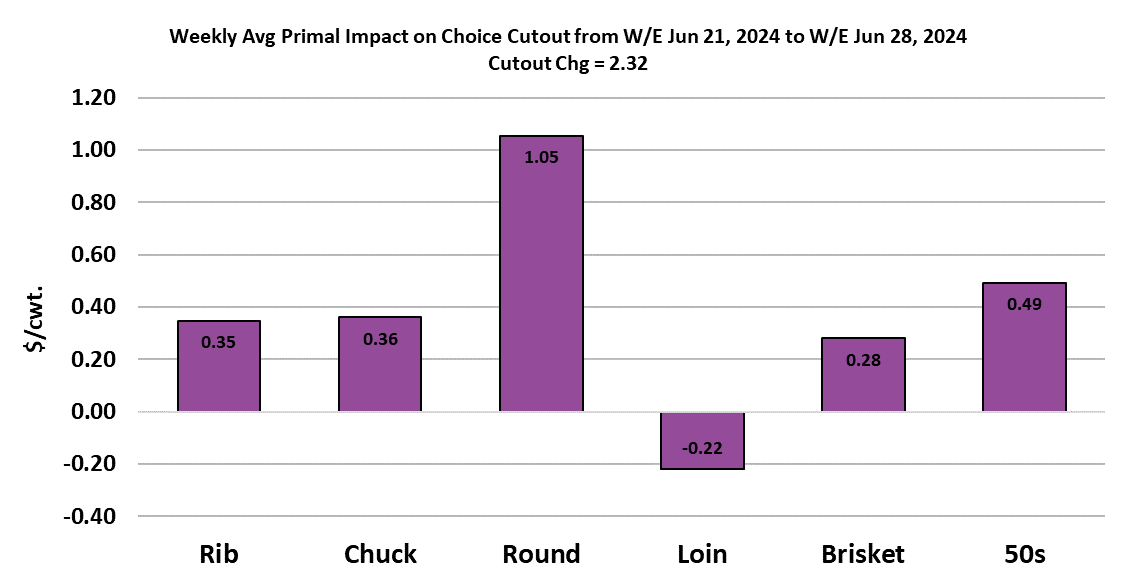

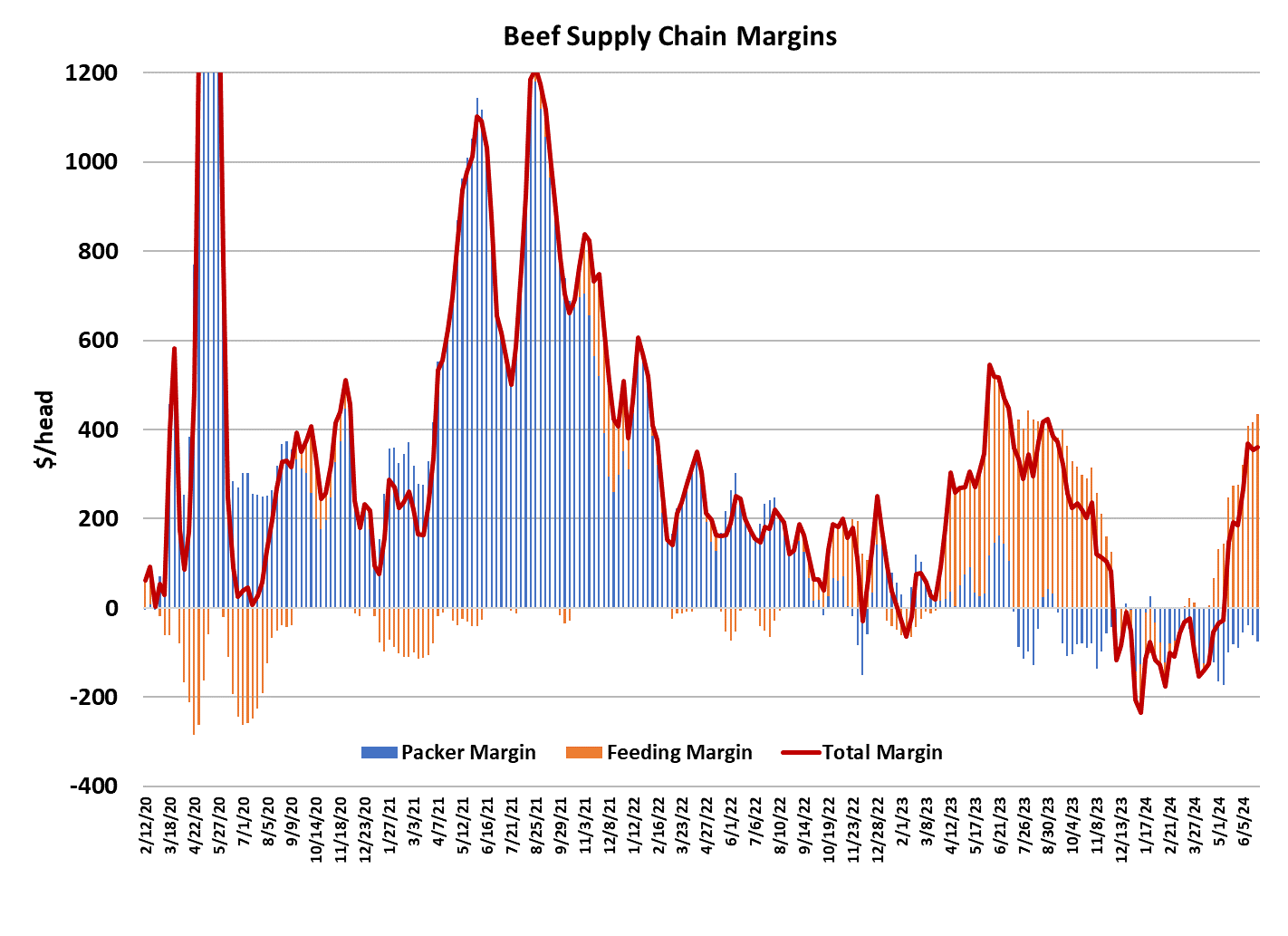

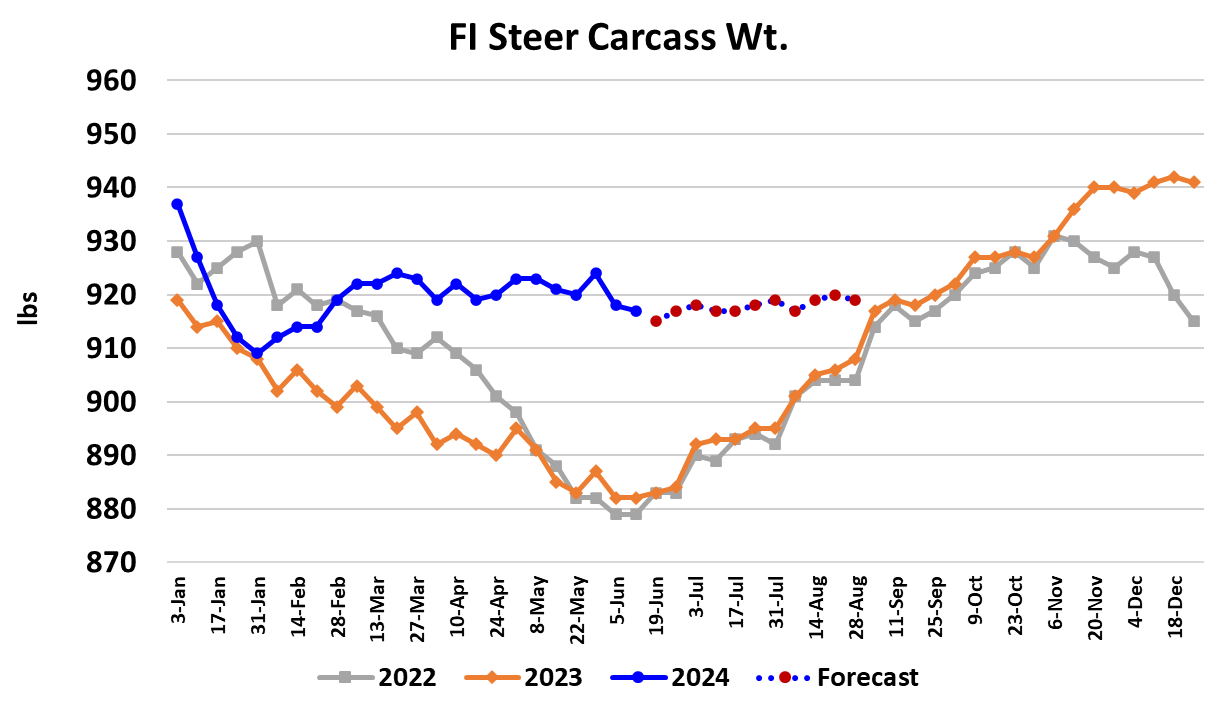

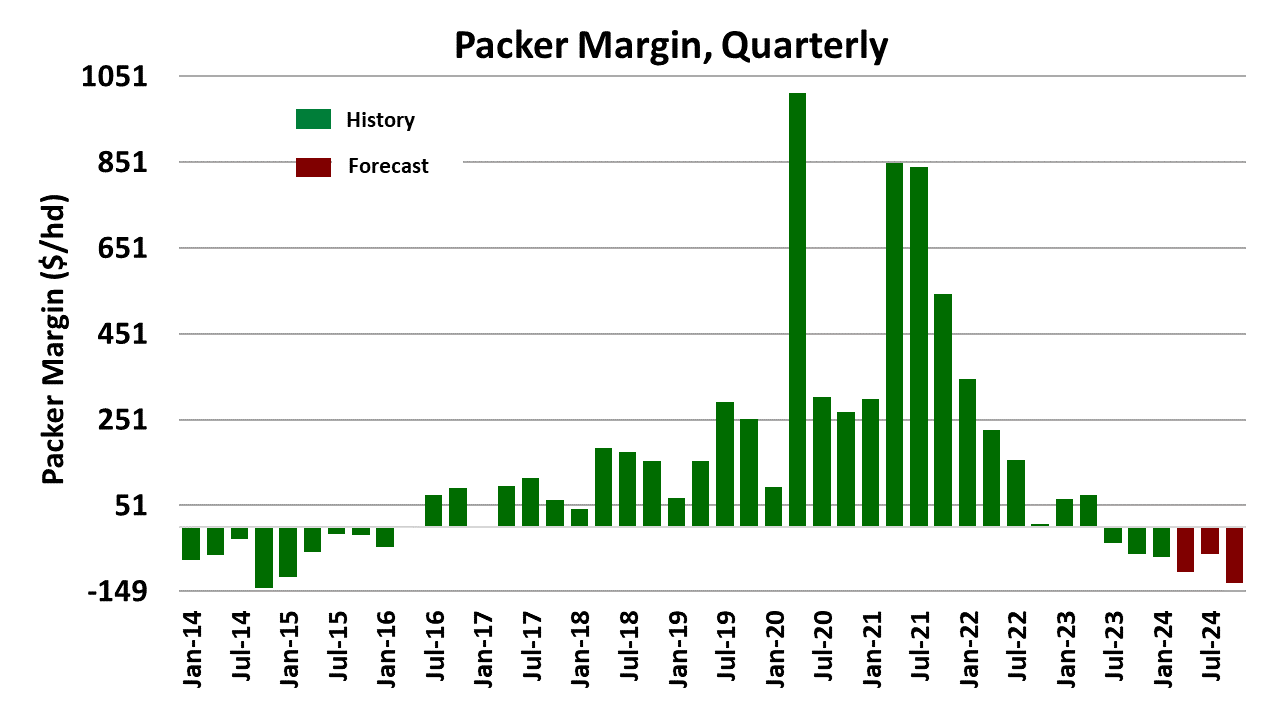

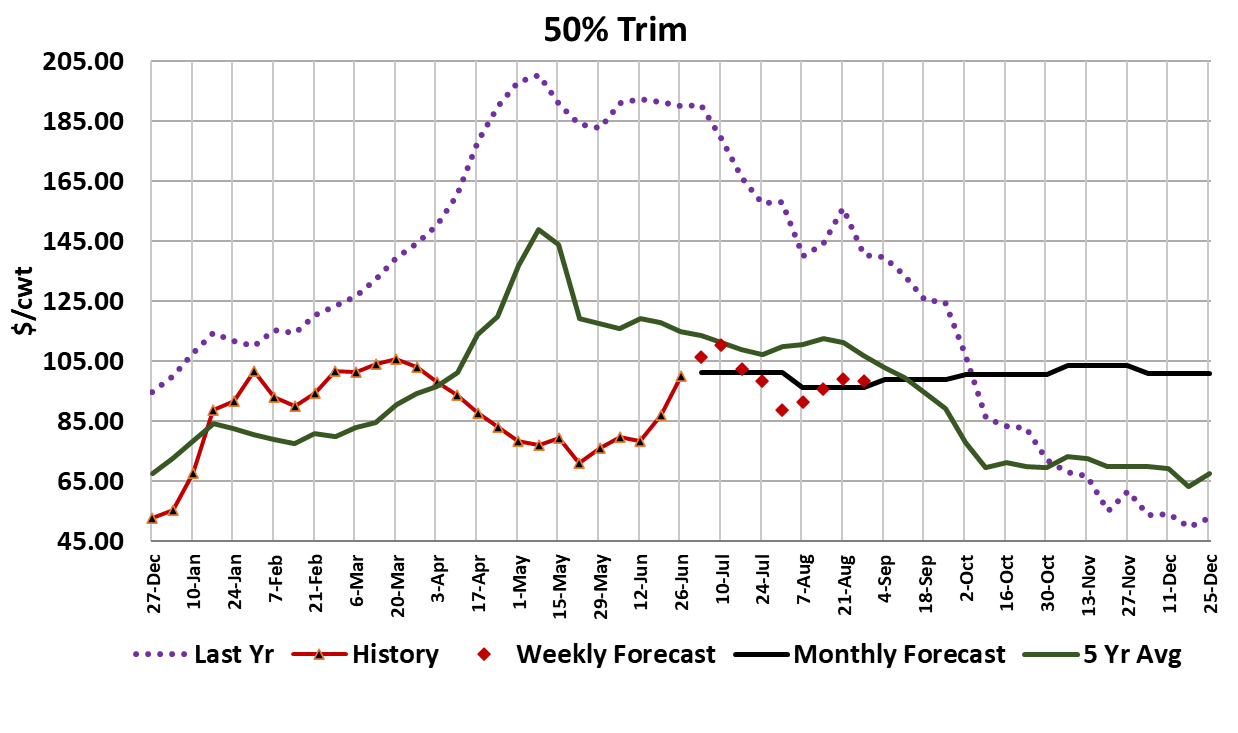

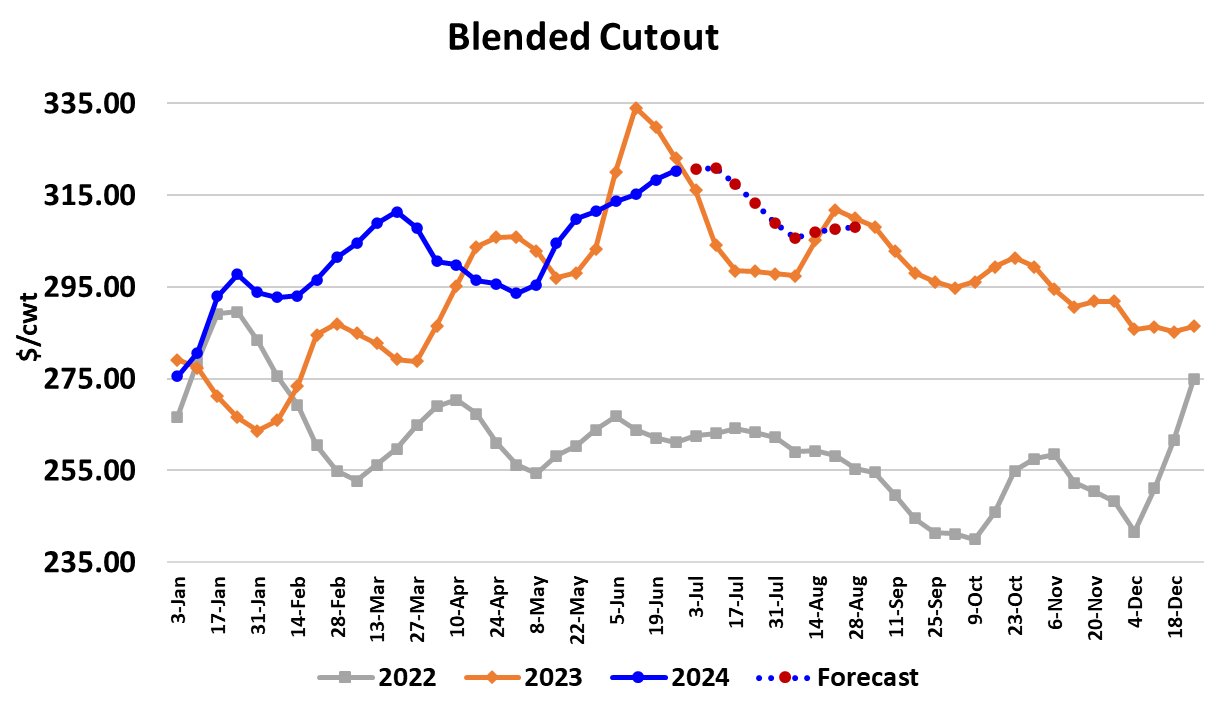

Wholesale beef prices continued to claw higher this week, with the Choice cutout adding $2.32 to average $323.71 for the week and the Select cutout gaining $0.02 to average $303.98. Volumes transacted in the negotiated market were down considerably from the week before, so gain in prices may be more a function of smaller availability than any new surge in demand. Cash cattle traded steady in the South at $190 and prices were mostly $198 in the northern live market, which was up $1 from the week before. This rally feels like it is in the process of topping and thus prices may soon start to track lower. However, the cutout is still getting a lot of support from the end meats, which are being ground and used as a substitute for very expensive lean trim. This week the 90s were close to $8/cwt. higher on a weekly average basis. As long as 90s prices continue to advance, it may be difficult to move the cutouts lower by a significant amount. Seasonal patterns tell us that we should be close to the annual top in the lean trim market, but it sure isn’t acting like it is ready to give up ground. Another warning sign is coming from the price of fat trim, which averaged just over $100 this week, which is about $22 higher than where it was just 2 weeks ago. Cattle should be carrying a lot of finish given heavy carcass weights, so this doesn’t strike me as a supply-side phenomenon. Instead, I suspect that what we are seeing is much better demand for ground beef as the calendar transitions from the early summer holidays, which typically favor middle meats, to the dog days of summer when consumers tend to get more cost conscious and retailers cater to this by putting more ground beef in the ads. However, we haven’t yet seen a big pullback in middle meat pricing. Prices in the loin complex have been easing a bit lately, but the rib primal was actually higher on the week. The seasonals would tell us that both rib and loin prices should be rolling over soon, so that is something to keep an eye out for. The fundamental forecast has the blended cutout holding near current levels for a couple more weeks before it starts to track lower. That is largely due to expected strength in the end cuts negating some softening in middle meat prices. In general however, overall beef demand still looks relatively strong. On the supply side, this week’s fed kill registered 495k, down 10k from the week before. Packer margins are still underwater to the tune of about $75/head, so they may opt to keep kills a bit constrained during July to help support the cutout. Next Thursday is Independence Day and thus the weekly kill will be down due to the holiday. I’m looking for next week’s fed kill to come in close to 425k. That will tighten up beef availability the following week and is one of the reasons why I’m not forecasting an immediate move lower in the cutouts. FI carcass weights for steers were reported down 1 pound this week and we can see from the attached chart that steer weights have been mostly sideways around 920 lbs. since late February. The forecast has that pattern continuing right through August and then weights are likely to start tracking higher once again. Steer and heifer beef production looks like it may only be up 1% YOY this week, but that follows a 4% YOY increase during the first three weeks of June. Buyers may find availability a bit tighter over the next couple of weeks, particularly if packer margins don’t improve. The number of cattle reaching market weight should increase in the northern feeding region over the next few weeks, thus helping to keep a cap on cattle prices and likely causing the price premium the North holds over the South to erode. Without leadership from the higher-quality northern market, I’m skeptical that the national average price can continue to advance. I’d look for a slow easing in the cash cattle market over the next few weeks, but not a big drop. It is starting to look like June feedyard placements may be higher year-on-year and if that is the case, then the industry my find itself with 2% more cattle on feed as of July 1 compared to last year. That supply is somewhat back-end loaded, so it is more likely to pressure the market in the fall and early winter than in the near term. The futures curve steepened considerably during the last half of June, and we now have the Aug25 futures trading almost $3 below the Aug24 contract. That seems wildly inconsistent at this point in the cattle cycle where numbers are still shrinking and heifer retention hasn’t yet started in earnest. Perhaps now that the Jun contract is off of the board, that relationship will begin to correct. Next week, look for both the cattle and beef markets to be mostly steady with this week’s level as the markets slowly work to carve out a top.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}