Beef Wrap June 11

This week’s weighted average price for cash cattle was almost

exactly $120, pretty much the same level it has been at for the past

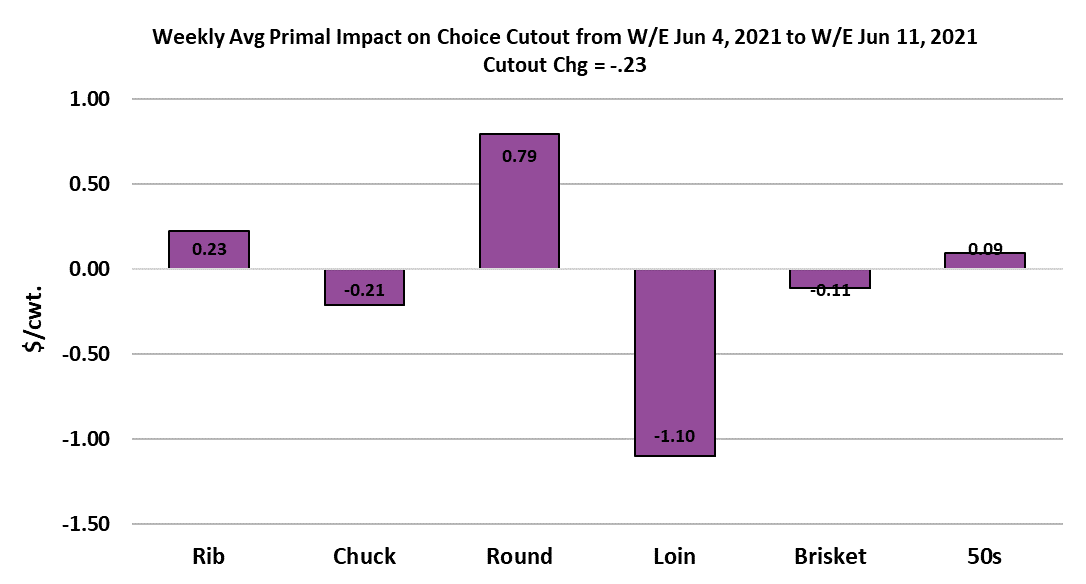

five weeks. The cutouts stalled, with the Choice losing $0.23 and

the Select down $3.04. Many market observers are holding their

breath waiting for the cutouts to plummet from these extreme

levels. I’m not one of them. Yes, the cutouts may have a modest

amount of downside risk over the next few weeks as the calendar

moves closer to the dog days of summer, but I really don’t think that

beef demand is going to deteriorate so rapidly that the market loses

value in big chunks.

The primary reason that domestic demand falters in most situations

is because retail buyers find a different protein that offers more

profit potential. In the current environment however, retailers won’t

find much value in either pork or chicken, since those prices are

very elevated also. Plus, I get the feeling that beef movement at

retail is still very brisk and it is hard to steer away from something

that is driving customers into the store. Therefore, if beef prices

pull back in coming weeks, I think it will be because packers are

stringing together larger kills and thus the supply side is pressuring

prices. This week’s fed kill registered 530k, which is near the upper

bound of what we think the labor situation in plants will allow.

There should be plenty of cattle available to fuel kills around 530k

for the balance of June and most of July. For the two months prior

to Memorial Day, fed kills averaged 513k per week, so if the

industry can manage to put a string of 530k kills together, it will

definitely improve availability and thus probably pressure prices

somewhat.

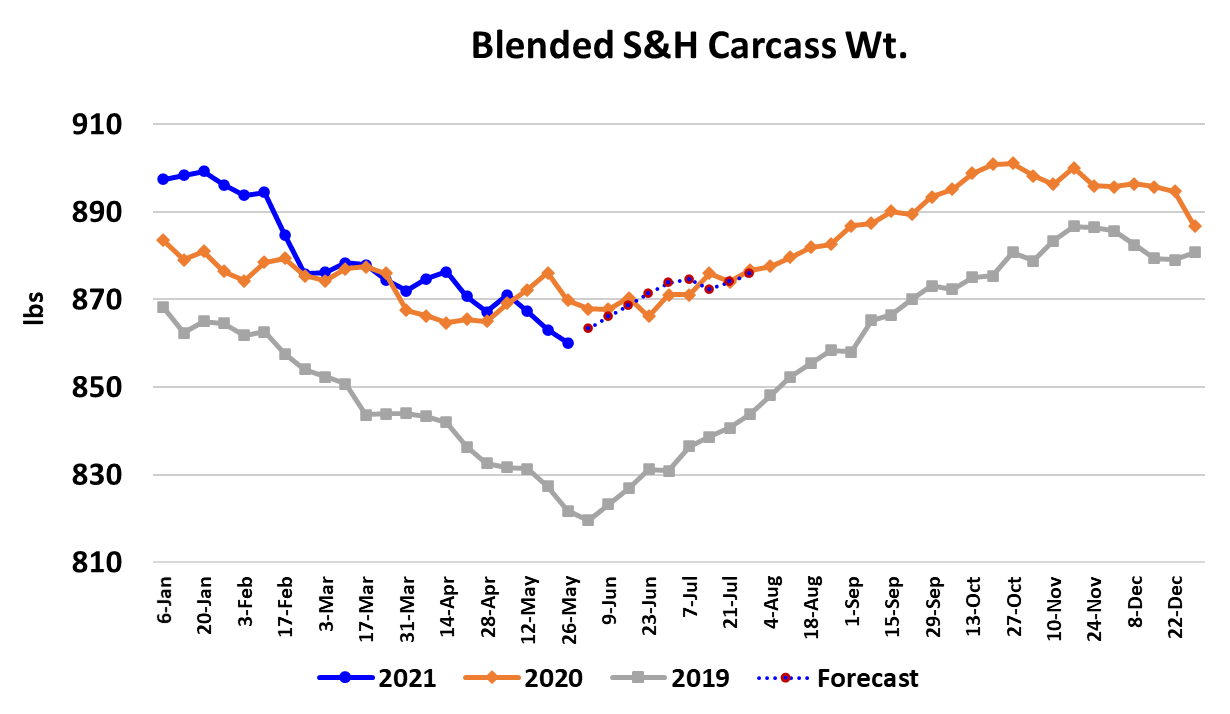

Carcass weights appear to have finally reached their seasonal low

and will likely work higher for the next 4-5 months. That will also

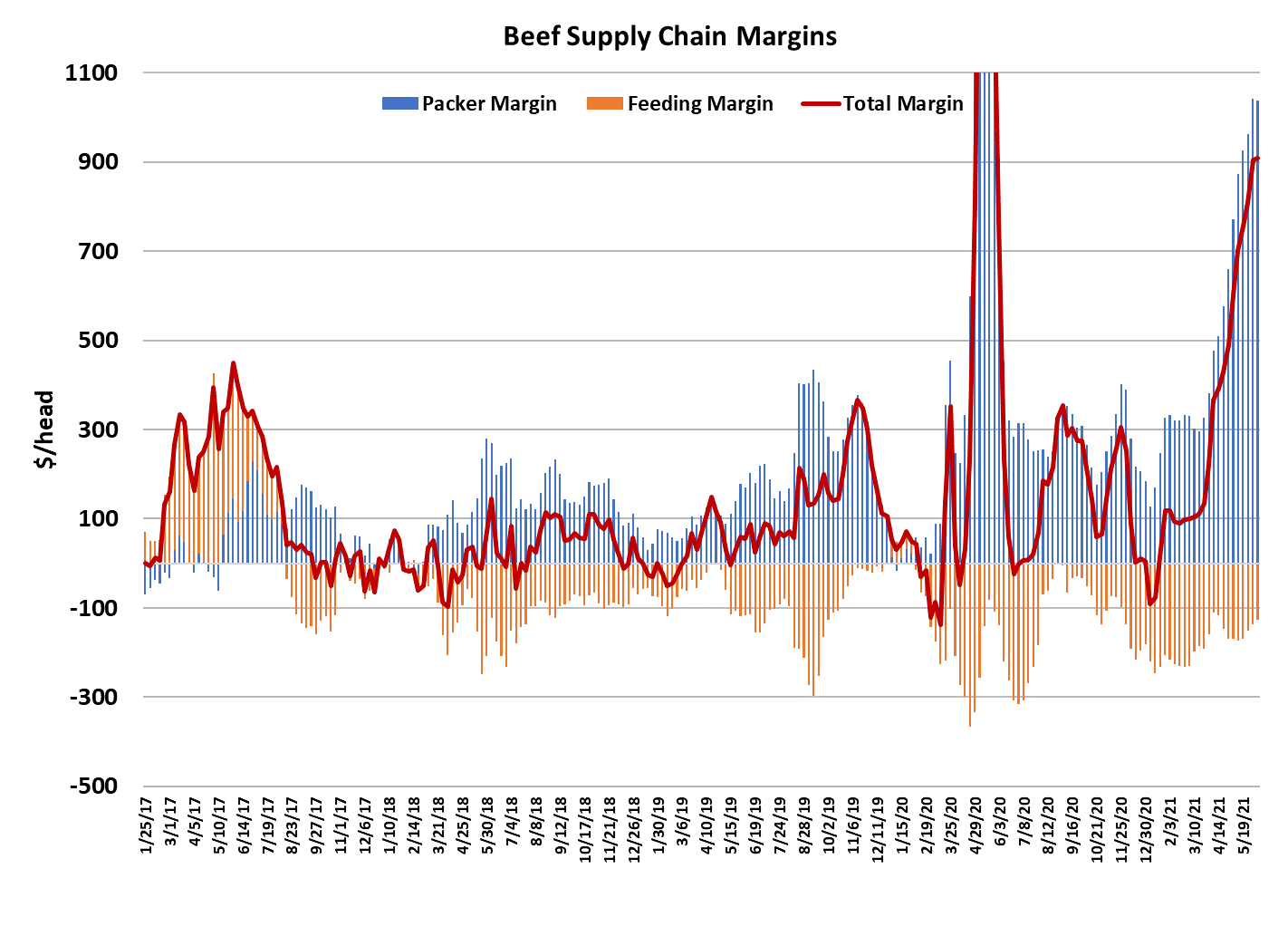

add to beef availability this summer. The combined margin moved

higher again this week, but the rate of increase slowed

considerably. It could be preparing to make a top, but I’d want to

see a couple more weeks of data to verify that. This week, it was

mostly the loin primal that was pressuring the cutout and that

probably reflects the completion of last minute buying for Father’s

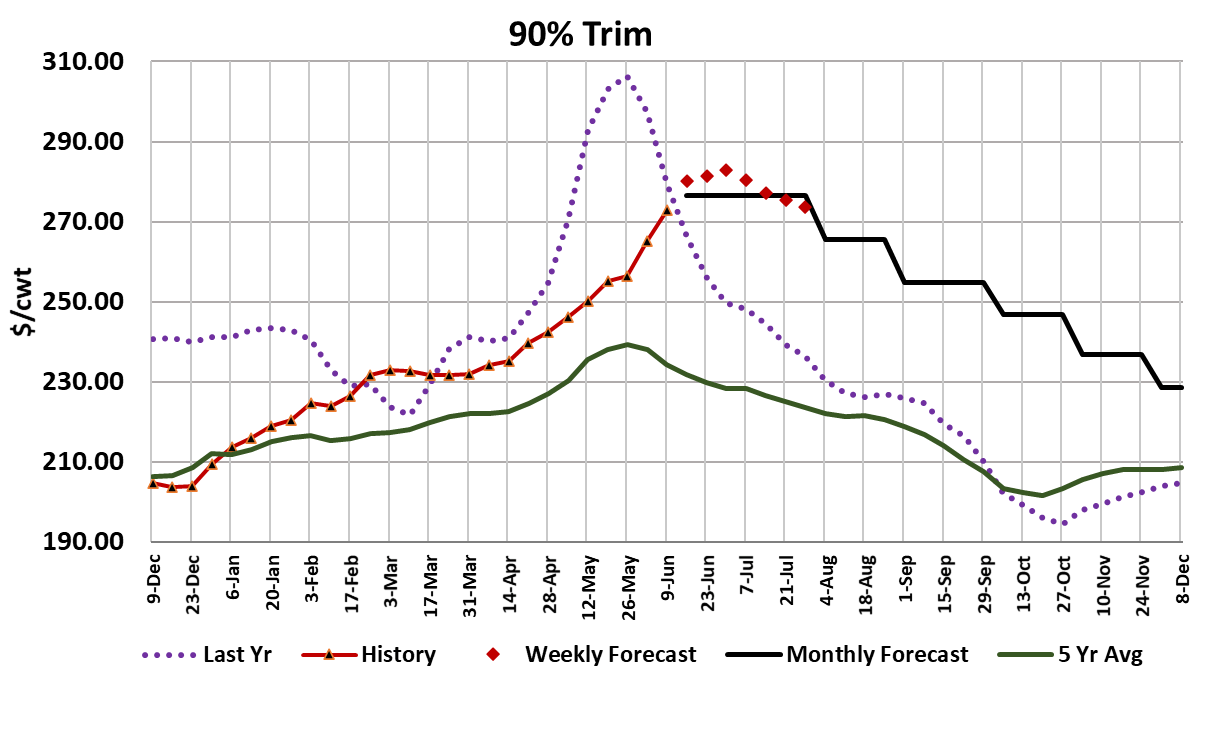

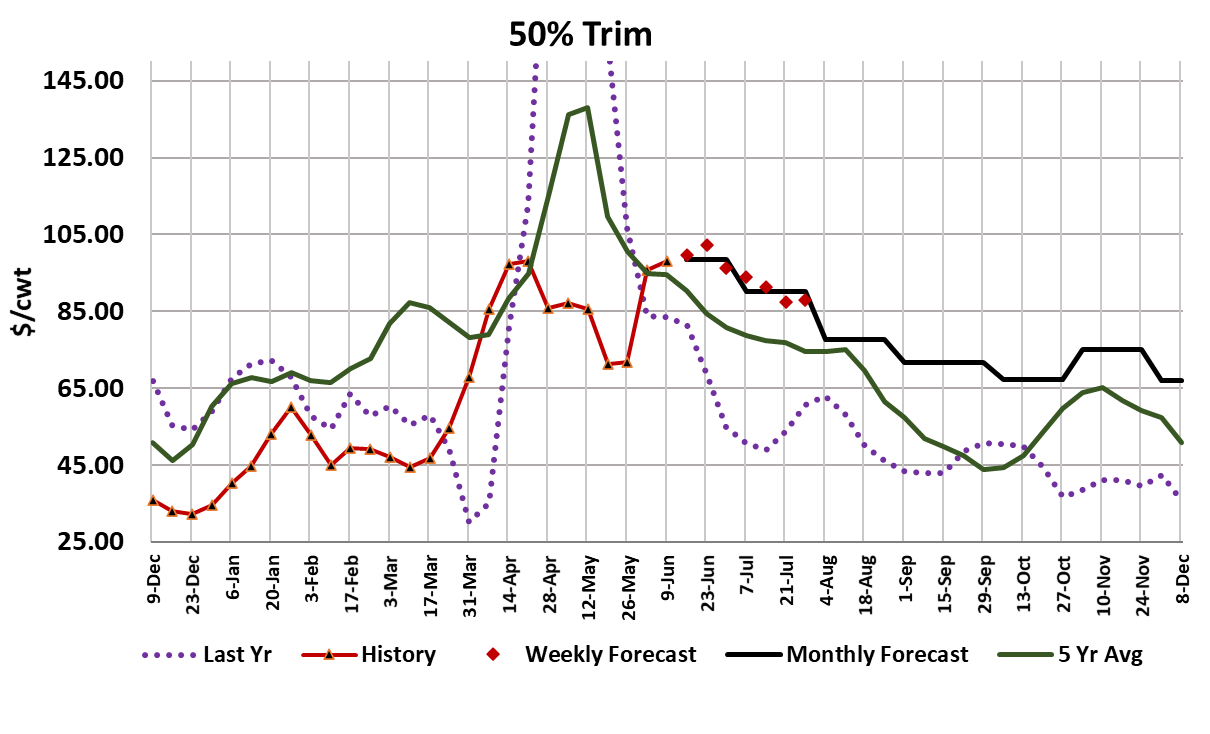

Day. The trim markets have firmed up considerably and this week

the 50s printed over $100 once and averaged $98 on the week.

Lean trim is also screaming higher (chart below). The 90s are

approaching $275.

It will be awful hard for the end cuts to lose much value while the

90s are escalating. That leaves the middle meats as having the

biggest potential for a downward correction in the next few weeks.

But even if the cutouts were to drop $20-30 in the next few weeks,

it probably doesn’t negatively impact cattle prices because packer

margins are so wide that they can easily absorb that type of

decline in the cutouts. I estimate packer margins this week held

steady at $1040/head. If the Choice cutout fell to $300 and cattle

prices held at $120, packer margins would still be around $700/

head. That is not a margin situation that would require

management on the cattle side.

We know that packers are struggling to find the labor needed to

run their plants full out. To fix that problem they are going to have

to raise wages and so the cost of processing cattle is going to go

up, maybe by a lot. That means beef prices have to go up also.

So, I think that going forward we are going to see beef pricing well

above what we were used to in the pre-COVID days. In addition

to beef prices going up, cattle prices normally move down when

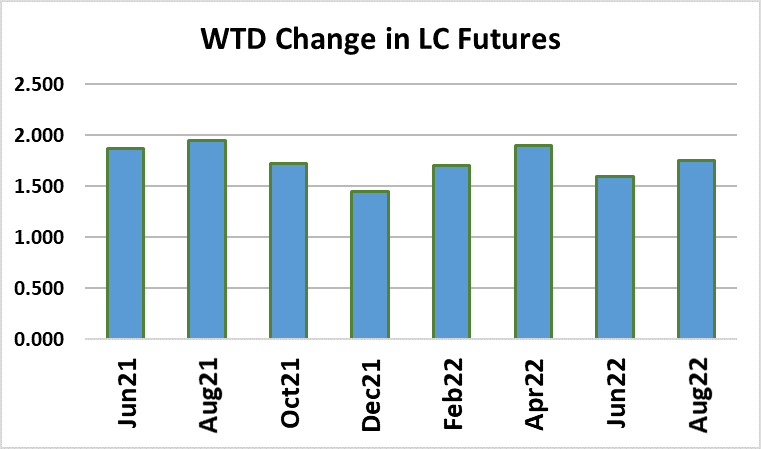

packer costs increase. The futures market doesn’t seem to be

anticipating that just yet. All of the 2022 contracts are trading over

$130, probably because traders expect food inflation to lift beef

(and thus cattle) prices next year. If cattle prices rise next year, it

will be because the herd is shrinking to the point where it forces

packers to compete for cattle. It won’t just be because packers

are giving part of their margin to cattle feeders. Packers will be

giving more of their margin to their workers.

Right now, there is very little incentive for packers to compete for

cattle. That situation won’t last forever, but it could last many more

months. Next week, all eyes will be on the cutouts for signs that

the top has finally been made. I wouldn’t be totally shocked if they

move higher again.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}