Beef Wrap July 2

Cash cattle prices averaged about $1.50 lower this week to $123.80,

but there are some pretty strong regional differences in pricing. Cattle

in the Southern Plains are bringing $122 or less while cattle in the

North are bringing from $125 to $127. There are two factors at work

here. The first is just a general cattle availability situation, where the

number of market-ready animals is larger in the South. The second is

driven by how well the cattle grade.

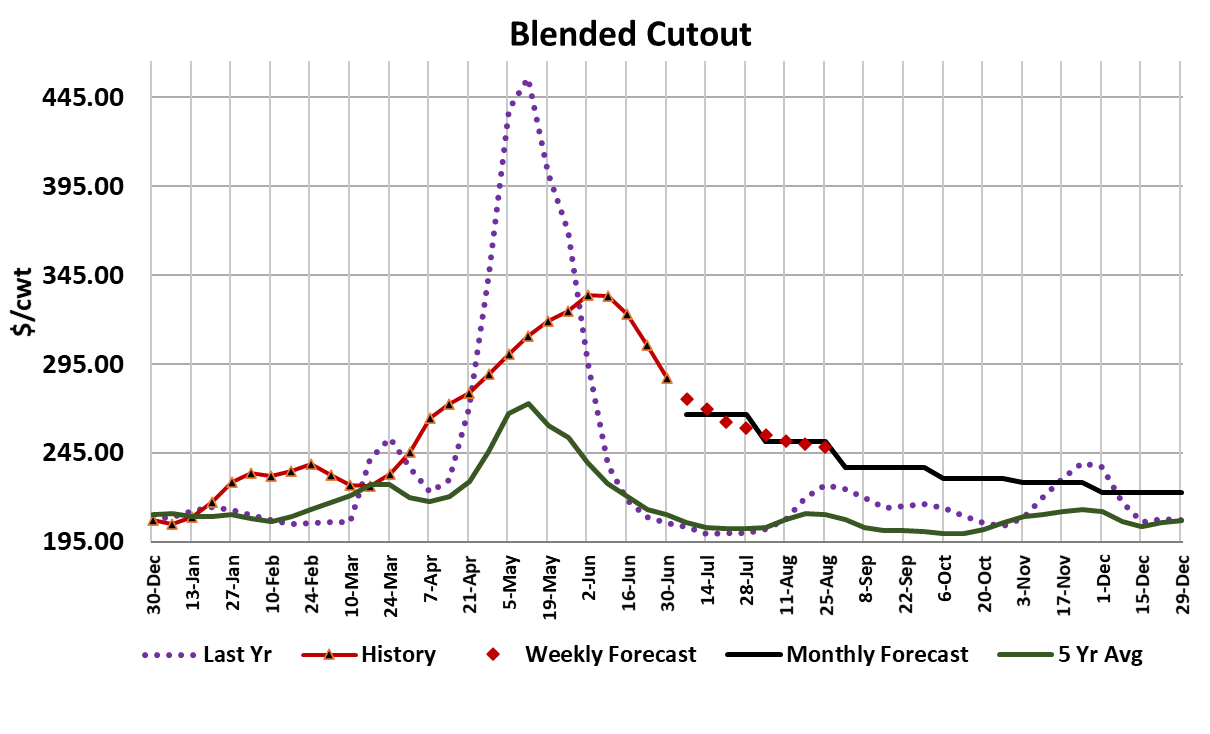

The wide Choice-Select spread ($21 Friday afternoon) is prompting

packers to pay a strong premium for cattle that grade better and those

cattle tend to reside in the North. Nonetheless, it is impressive that the

cattle didn’t give up more ground given that the Choice cutout lost over

$21 on a weekly average basis and the Select was down almost $9. I

have to admit that the beef market is coming down faster than I

envisioned it would and I’ve adjusted my price forecasts lower in

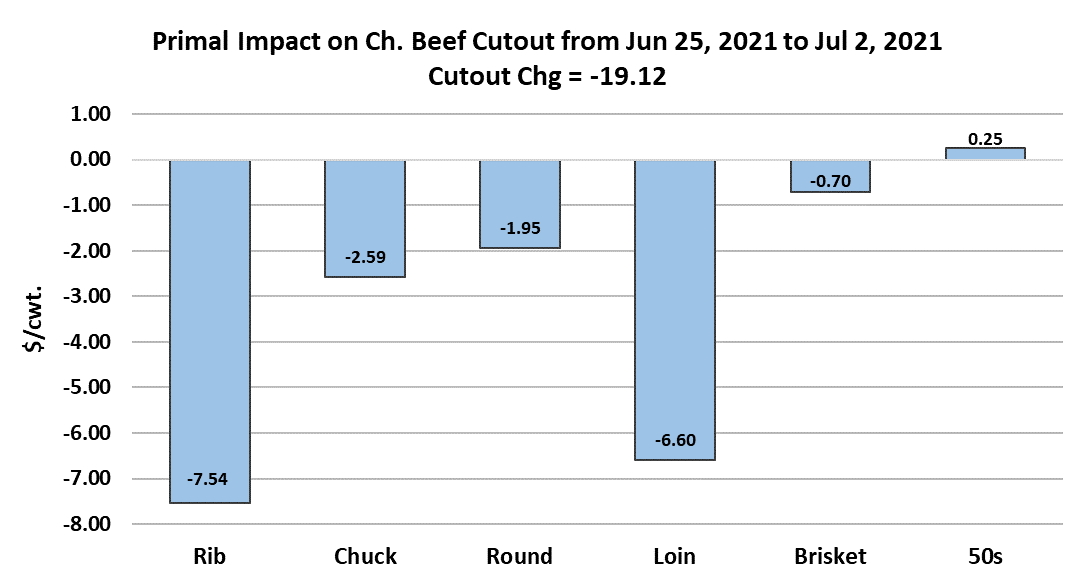

response. The chart below indicates that it is still the middle meats that

are primarily responsible for the collapse in the cutouts recently. End

meats were down some this week, but are at much higher levels that

one would expect for this time of year. Importantly, the 50s market is

actually strengthening. Same goes for the 90s market.

I think we are seeing pretty strong demand for grinds now that we are

beyond Father’s Day and in the case of the 50s, supply is being limited

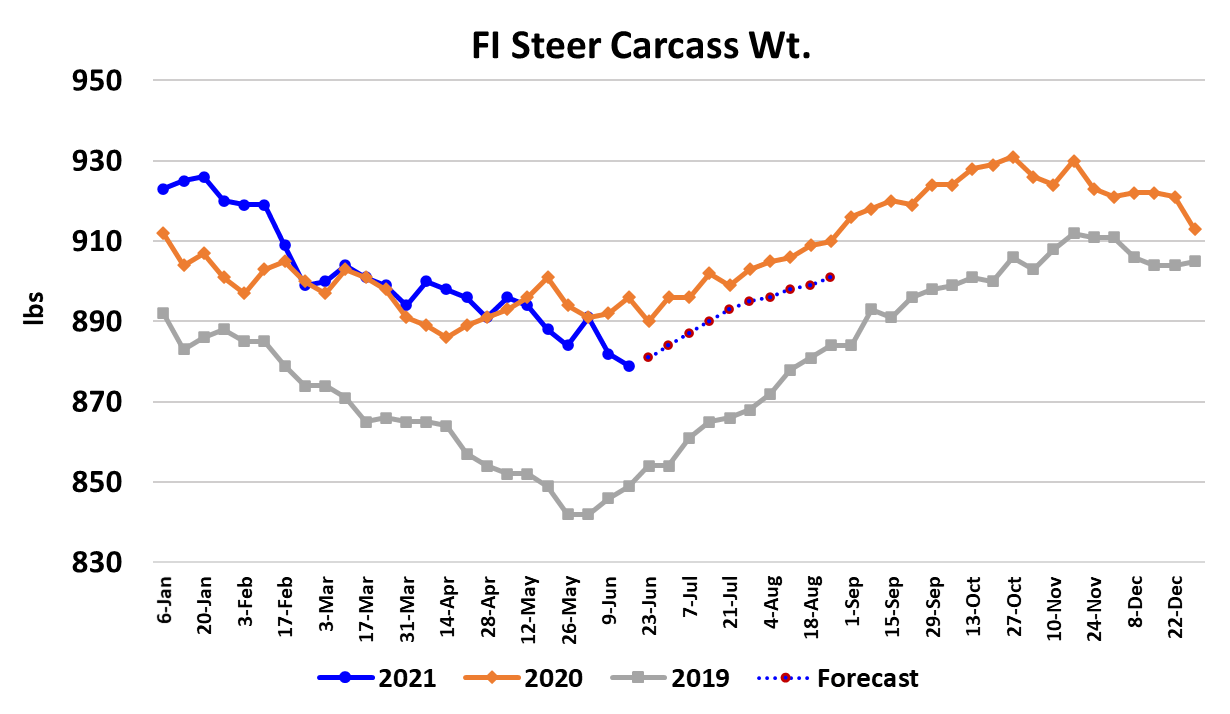

by declining carcass weights. I thought that the bottom had been made

for carcass weights, but was proven wrong this week when steer

weights were reported three pounds lower to 879 lbs. It is really

unusual to see weights still declining this late in the summer. Normally

they bottom by mid-May. The DTDS weights are looking far better than

they did just a few weeks ago, with the steer DTDS now at -10. That

suggests that feedyards have improved their currentness dramatically

in the past few weeks. That may also be helping producers in the

North to press for higher cash prices.

As far as kills go, packers have done an admirable job of keeping

weekly fed slaughter up around 525k, in the weeks following the JBS

cyberattack. This week’s fed kill came in at 492k as packers did a

rather light Saturday since it is Independence Day weekend. Next

week should be even smaller, perhaps around 440k, since there will be

no kill on Monday. It will be interesting to see if these holiday-reduced

kills can slow down the slide in the cutouts. Once the holiday is behind

us, I’d expect packers to go back to kills around 525-530k for a few

weeks, but as August approaches, the flow model tells me that there

will be fewer cattle available and thus we could see the fed kill drop

back toward 515k or perhaps even 510k at times.

August usually brings on some institutional buying interest as

schools and colleges prepare to open for the fall semester. With

so many schools being shuttered last year, it’s a pretty good bet

that many have zero meat inventory and thus may have to come

back into the market a little more aggressively than normal. So we

may find out sometime in early August where the bottom is in the

beef market. The demand side of the market feels like inner tube

that is hissing with an air leak.

Apparently now that consumers can do things besides stay at

home, they have reduced their demand for beef and other animal

proteins. This is in-line with what I’ve been saying all along that

when the pandemic ends, meat demand should decline. It is

worth noting that foodservice is “back” in a big way, yet that is not

supporting the cutouts at all. That is because demand at retail is

declining more than demand is increasing in the foodservice

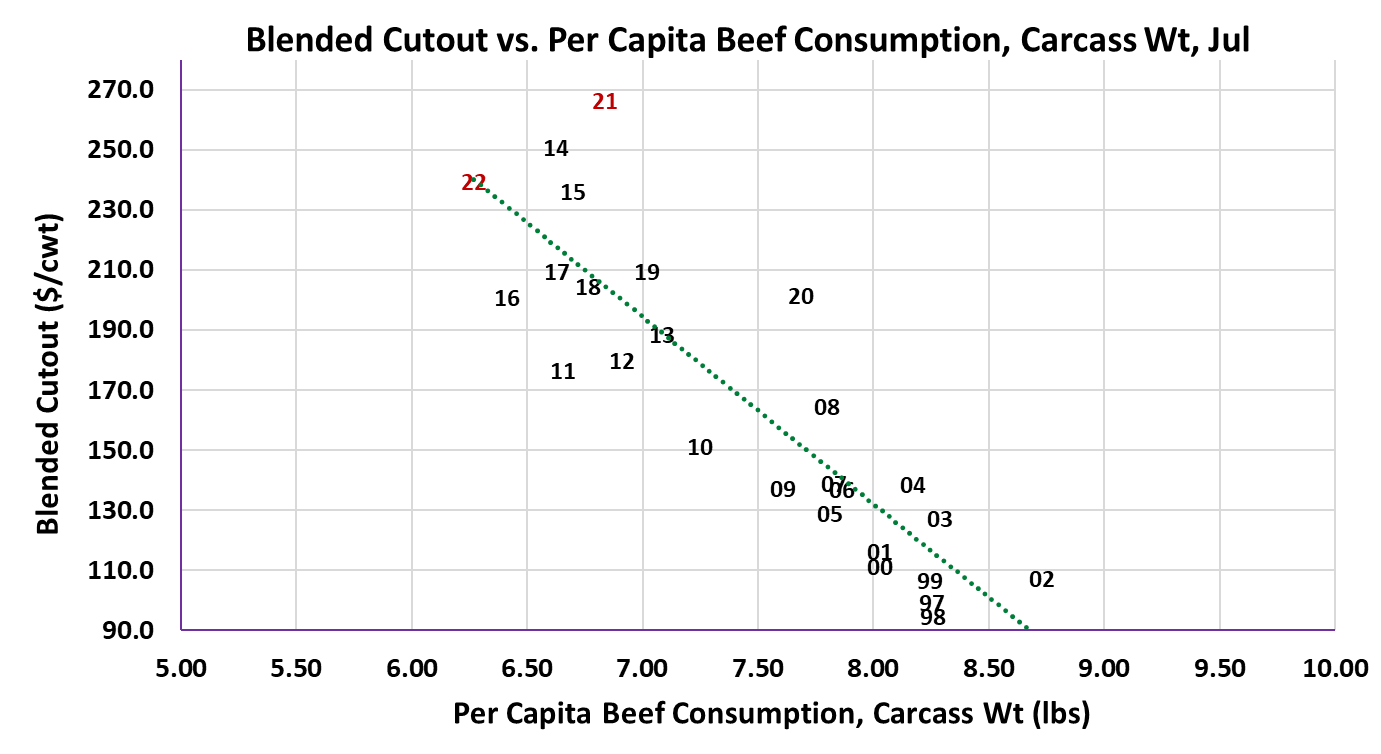

sector. I’ve included the scatter diagram for July and you can see

that I’m still forecasting the 2021 data point to be well above the

regression line, but it is not nearly as high over the line as it was

back in May and June. My guess the ’21 data point will move

closer to the regression line in the next few months as the air

continues to come out of the demand side of the market.

Export demand for US beef appears to be quite strong and that is

one of the factors that should help support beef prices above

historical norms even when all of the pandemic boost in domestic

demand has dissipated. China seems to like US beef more than

US pork recently and as long as they are gobbling up large

quantities of US beef, there will be a strong tone to the export

market. Next week, watch for the declines in the beef market to

slow as smaller production starts to be realized. Also watch

carcass weights since they may surprise everyone and continue

lower.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}