Beef Wrap January 9

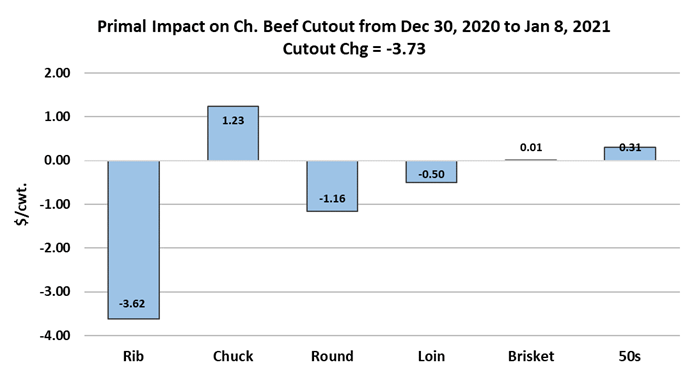

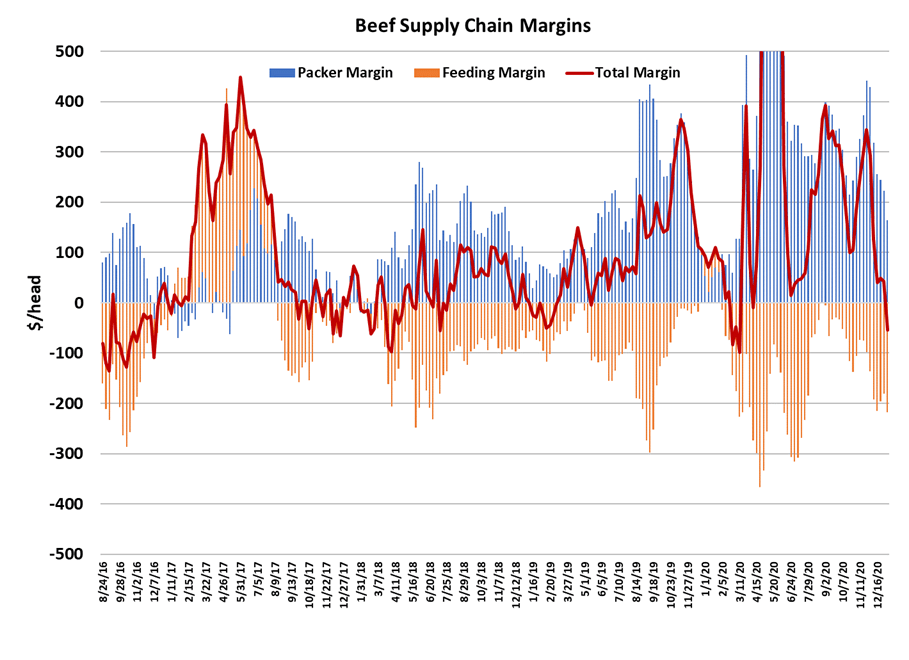

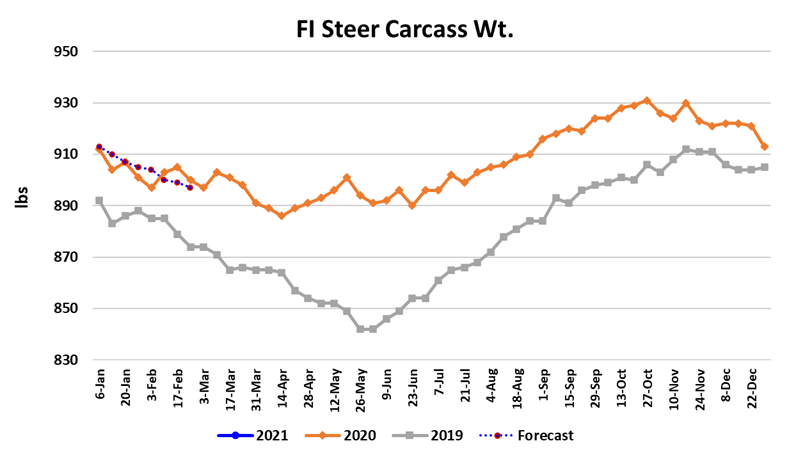

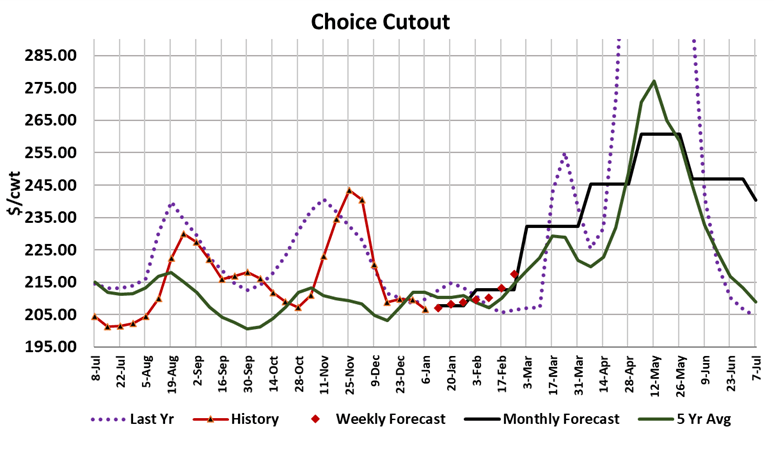

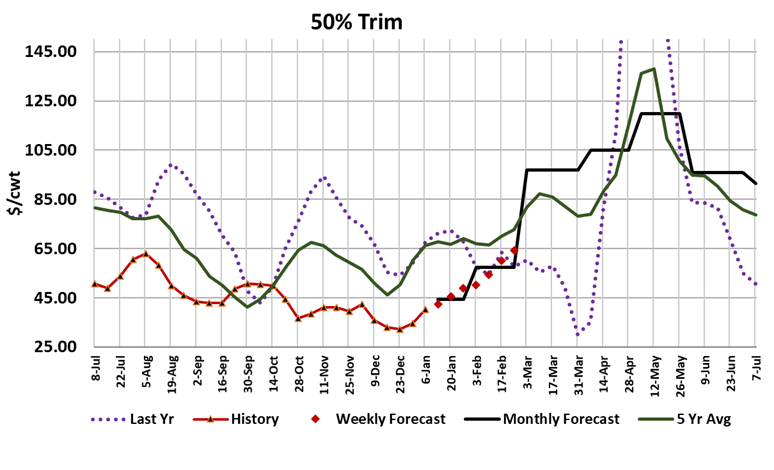

Cash cattle traded in a range of $110-112 this week. The weighted average, at $111.50, was virtually unchanged from the prior week. The cutouts wobbled a bit, with the Choice averaging about $3 below last week and the Select about flat with last week on a weekly average basis. It feels like the beef market is trying to find its footing here. Declines in the ribs this week weighed on the cutout, but typically early January means a bottom in the rib market and beyond that interest from steakcutters looking for a bargain will provide support. Interestingly, the chucks were higher on the week while rounds moved lower. Both should see some moderate buying interest in the next few weeks. The 50s moved back over the $40 mark this week for the first time in almost a month. 50s should have more upside potential due to recent moderating of carcass weights. As we go forward over the next few weeks, I think the tug-o-war between supply and demand is going to be pretty well balanced. On the supply side, this weekfs steer and heifer slaughter came in at 511k, which was 4k lighter than the last full-week kill in December. Previous placement patterns suggest that there should be enough steers and heifers to support a 525k weekly kill, but packers probably want to see some further demand improvement before they push the kill up that high. I wouldnft be surprised to see at least a couple weekly fed kills in January at or above 520k level. February will bring smaller kills, down around 495-505k. Carcass weights took a surprise dip this week, with steer weights losing 8 pounds in the data for Christmas week. Suddenly, steer weights are only 8 pounds heavier than last year. Ifm not quite sure what caused that sudden drop, especially given that it was a very short kill week and weights tend to rise when the kill is short. Maybe the last of the backlogged cattle got cleaned up right on schedule at the end of December. Whatever caused the correction in weights, it will certainly be welcomed by cattle feeders. Going forward, cattle feeders may start to feel the pinch from higher corn prices and that could dampen carcass weights further as producers shift rations towards a little more hay and a little less corn. The flip side of that is that the structure of the futures board is dangling premiums on the Feb and Apr contracts and that could encourage slower marketings and thus higher carcass weights. I think that cattle feeders will be a little more resistant to slowing down cattle after what they just came through in the second half of 2020. Packer margins fell to about $165/head this week, the result of packers killing more expensive cattle in an stagnant beef price environment. Their margins are likely to stay below $200/head during January and February. In years past, packer margins normally went negative at this time of year, but something has changed in the last few years and negative packer margins rarely happen anymore. So, there is still financial incentive for packers to keep the kill high, but they are wise enough to know that if they over-do it at this time of year they could seriously dent the cutouts and thus hurt themselves more in the process. Domestic demand was strong in December, but Ifm looking for it to be somewhat weaker in January. The combined margin chart below shows that a little head-fake developed in late December when it looked like the combined margin might be turning higher, but alas, it continued lower. A turn higher shouldnft be too far away however. We got the ERS export data for November today and it showed a 13.2% YOY increase. That is the second month in a row of increasing exports and it wouldnft surprise me if December is higher also. So, international demand looks good while domestic demand is softening somewhat, but expected to turn higher shortly. I think that helps the cutouts gradually work higher, but the bigger gains should come in February when kills ease back some more. Cash cattle can move higher too, because the weight data makes it look like cattle feeders should have some leverage improvement and packer margins typically come under pressure at this time of year. Watch for some price improvement in the end meats next week and also the carcass weight data to see if it is going to take back any of this week’s decline.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}