Beef Wrap January 30

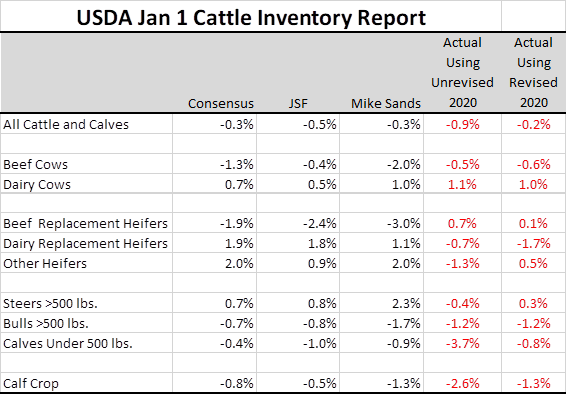

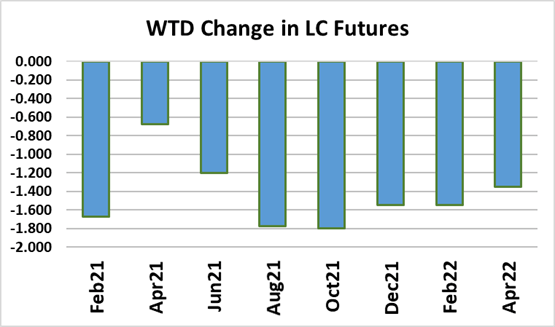

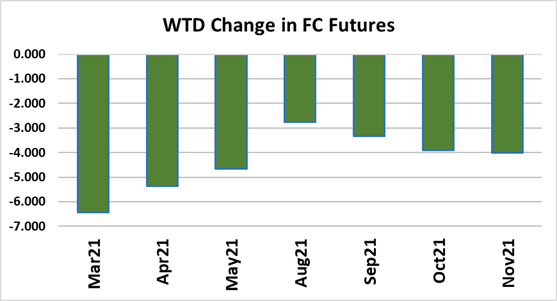

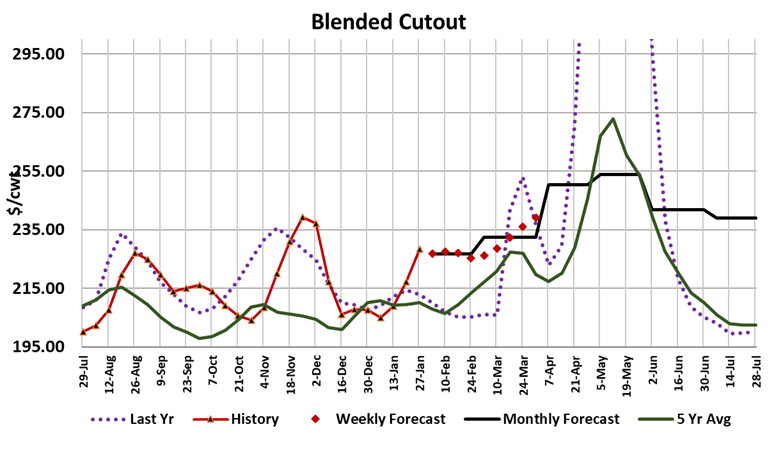

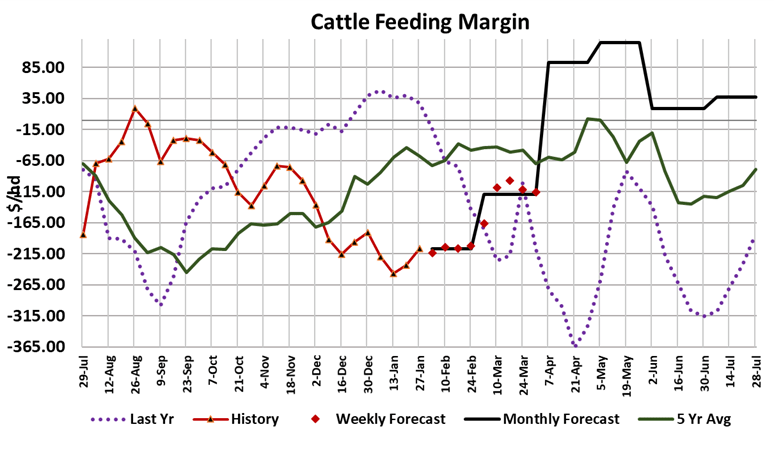

Cash cattle traded higher this week, with $113 registering as the top price. The weekly average is likely to be around $112.25, which would be $3 above last week. Packers were able to comfortably pay higher money for cattle because the cutouts have been roaring higher. The Choice added $11.13 Friday-to-Friday and the Select was up $9.36. Their margin swelled out to $392/hd, but that will narrow up next week as those more expensive cattle show up for slaughter. Still, when the cutouts are rocketing upward that provides a lot of margin for everyone in the supply chain and this week packers shared a little of that prosperity with producers. The combined margin chart below shows how strongly this margin gain has been. How much further do they have to go? Well, I think it is reasonable to expect the combined margin to reach $300 and that can probably be attained within 10-14 days, so I wouldn¡¯t look for this rally to carry much beyond then. The magnitude of the daily price increases is also likely to be smaller as the combined margin moves higher. Thus, I¡¯d say its reasonable that cattle feeders could coax higher money out of the packers for at least another 2 weeks, which would get us to the middle of February. By then the cutouts could be turning lower and that will make the packer more resistant to paying up. However, with each passing week the cattle feeder¡¯s leverage position should be improving and so I wouldn¡¯t really expect that cattle prices will collapse even if the cutouts eventually do. This week¡¯s fed kill came in at 512k, up 3k from the week before. Kills are falling short of what the flow model projected for January by about 155,000 head. That is the second month in a row that we have under-killed the model, but weights seem to be coming down slowly and so maybe the previous placements were over estimated. This bears watching however, because if USDA¡¯s placement survey was correct then its possible that some cattle are starting to back up. The DTDS weights will be the best indicator of this. Right now my forecast has the DTDS weights coming down rapidly, but if they don¡¯t then I would get more bearish about the near-term price prospects for cattle. Obviously, the demand side of the beef market is very strong at present. It looks like the January demand index for the blended cutout will come in around 1.10, which is about 5% above the long-run average. However, with all the excitement surrounding the cutout¡¯s rapid rise in recent days, it is important to keep in mind that the blended cutout in January is likely to be nearly equal to the average it posted in December and only about $4 higher than it was last January. Beef exports looked good in this week¡¯s data and, while higher spot pricing might discourage some export sales, there is a good chance that even higher Apr and Jun futures prices will encourage foreign buyers to act now rather than to wait to make US beef purchases. For now, I¡¯m expected beef exports to hold up well. USDA released its Jan 1 Cattle Inventory report today and it showed that the total number of cattle in the US declined by only 0.2%, but that is a bit misleading because they revised the 2020 inventory number down substantially. In fact, USDA lowered a lot of the 2020 numbers and that always creates a dilemma when trying to compare the actuals to what analysts projected beforehand. As a result, I included 2 columns in the table below¡ªone using the unrevised 2020 numbers (which is what the analysts would have had in hand when they made their forecasts) and one using the revised 2020 numbers. The size of the beef cow herd is one of the more important statistics coming out of this report since that is the engine that will fuel future growth prospects. Here, the survey indicated considerably more beef cows that what analysts were looking for. The calf crop is also an important number and it was reported to be smaller than what analysts were looking for. The implied calving percentage for last year¡¯s calf crop was really low, at 86.4%. That is the second year in a row that the survey has indicated a very low implied calving rate. That calving rate is a measure of productivity of the breeding herd and to see it down so much for two years in a row is a bit concerning. The futures market was having a great week right up until mid-session today when a wave of selling hit and took the market sharply lower. The Apr and Jun contracts fared better than the rest of the curve this week. If the market pulls back further next week, I would see that as a buying opportunity for beef users who have uncovered needs this spring. Next week, watch the cutouts for further gains, but expect those gains to slow somewhat. We also need to see a material decline in carcass weights and the DTDS to make me feel comfortable that cattle are not beginning to back up.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}