Beef Wrap January 27

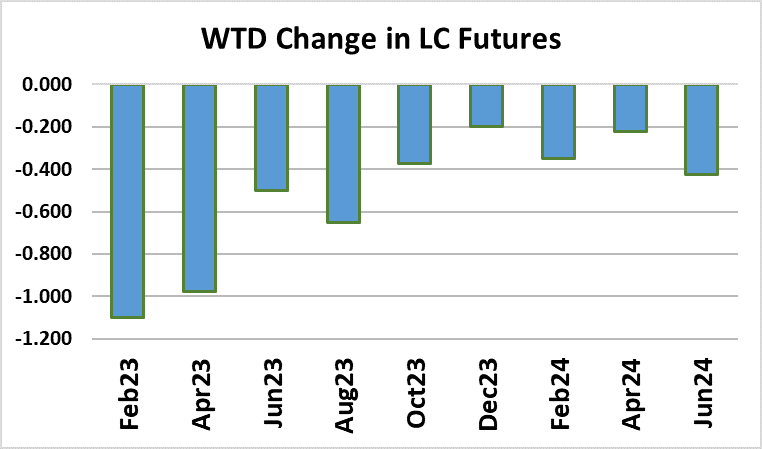

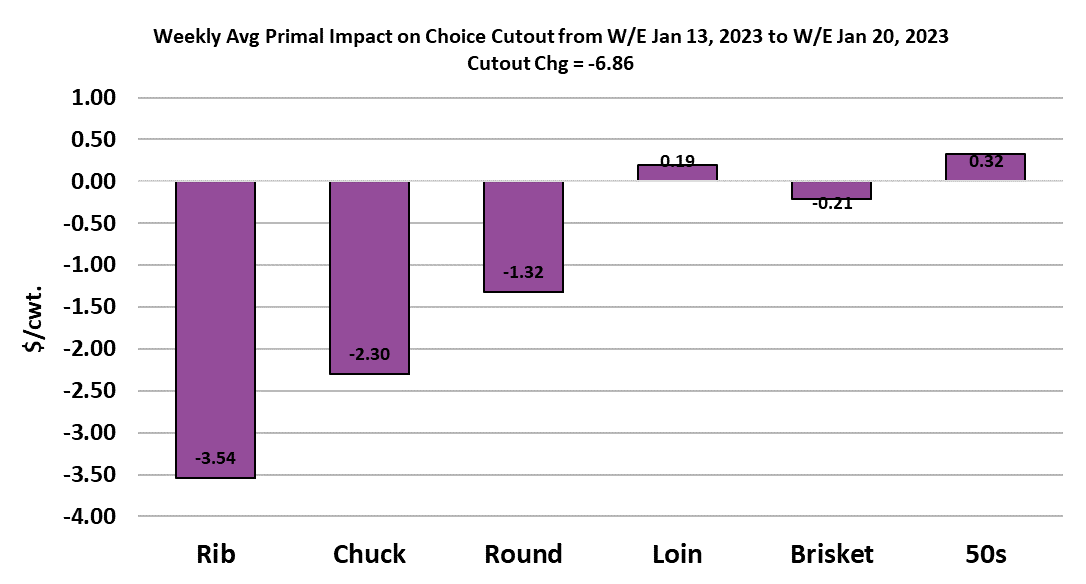

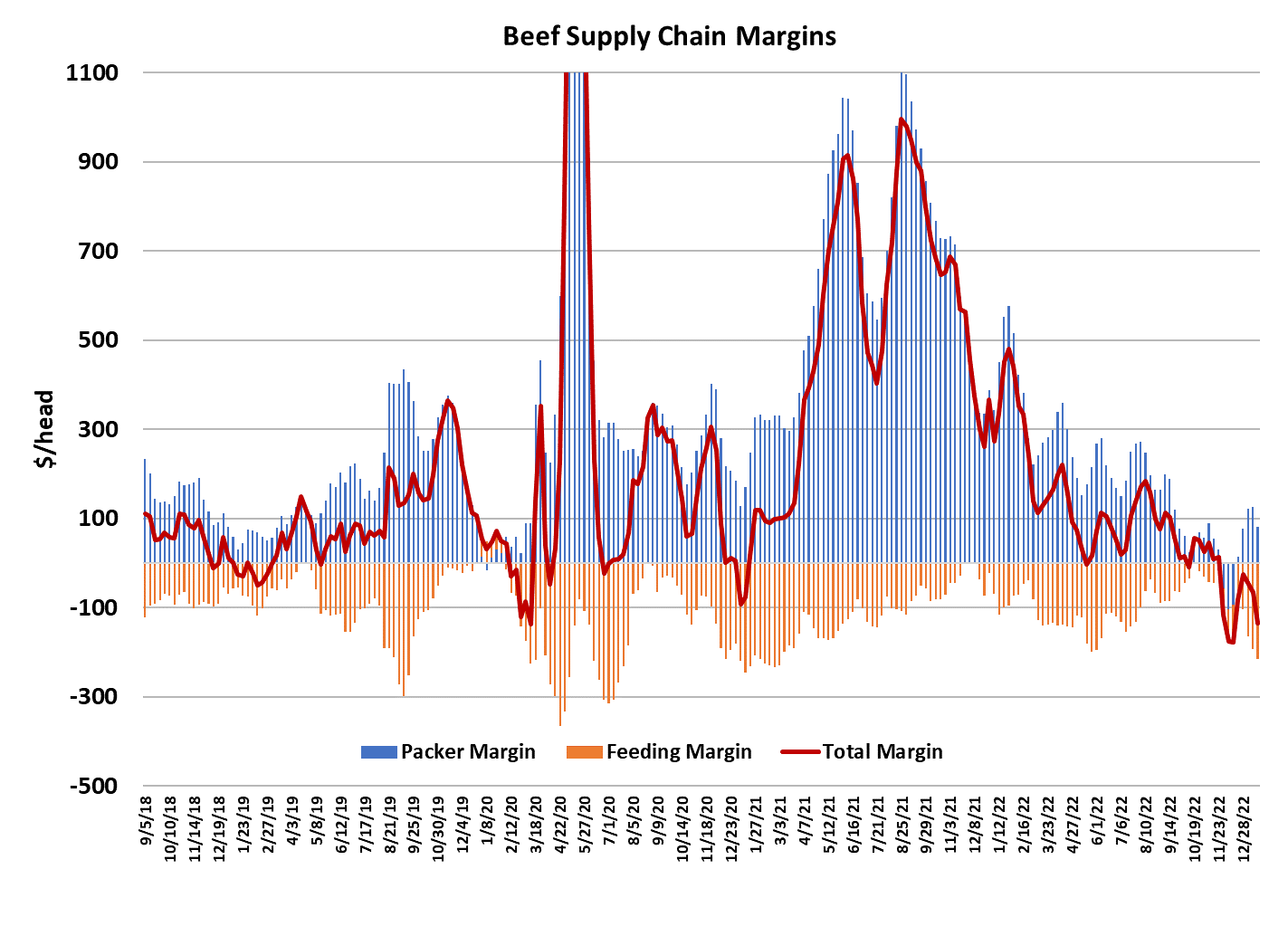

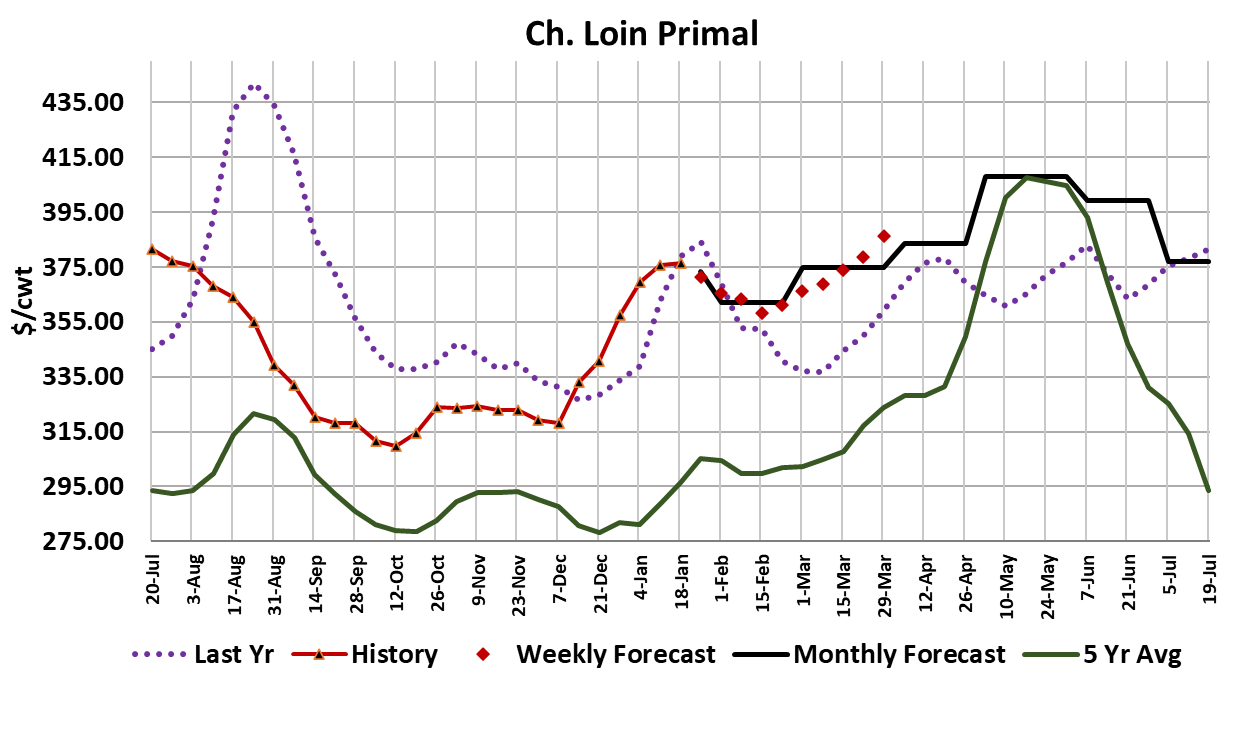

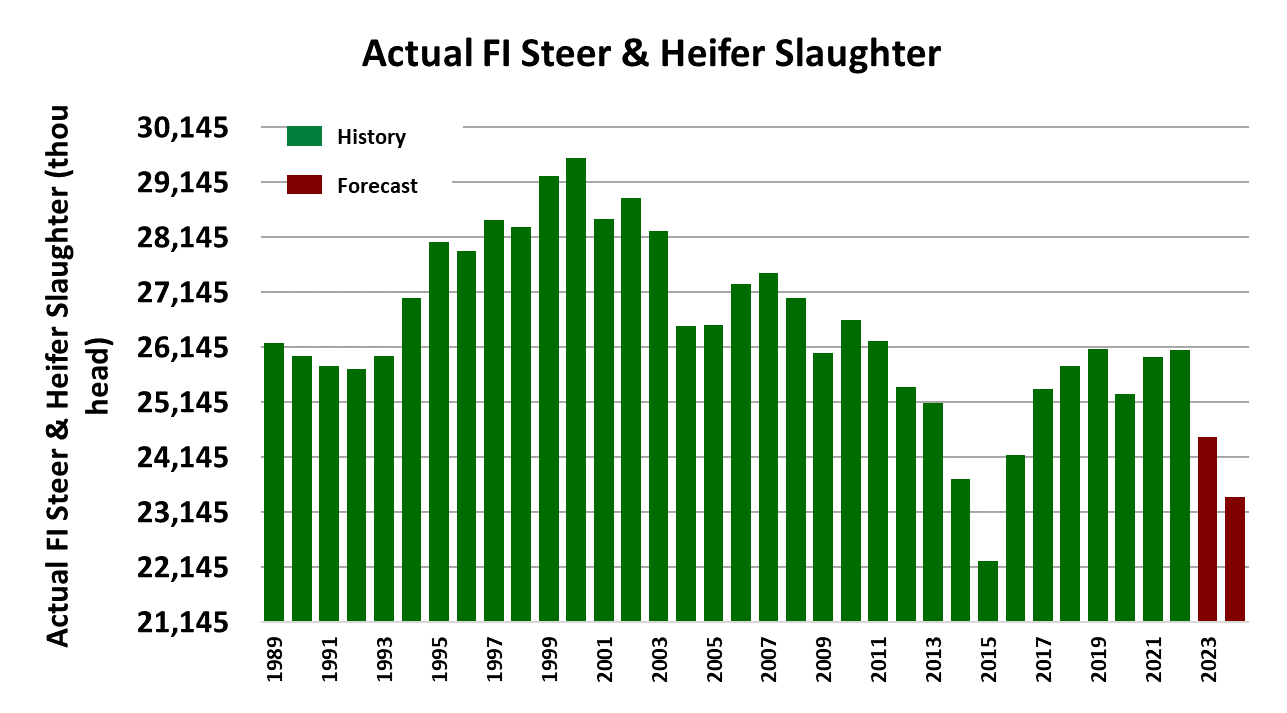

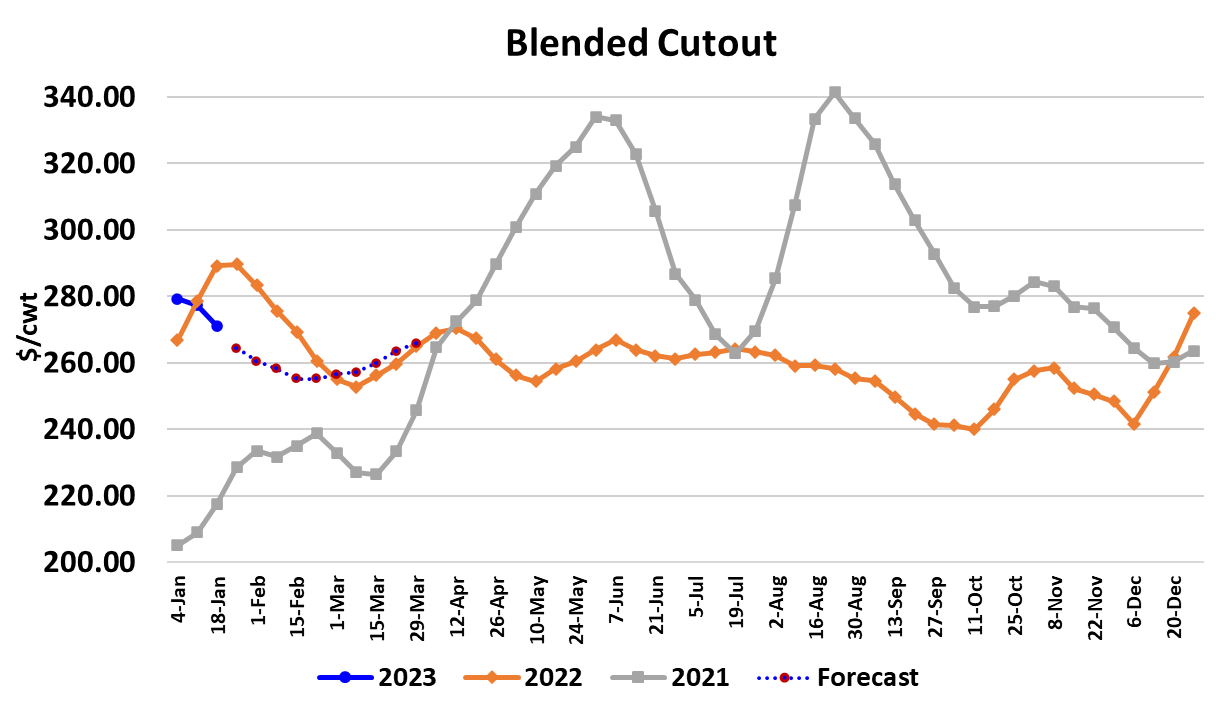

Cattle feeders ended up taking lower money in the cash market again this week, as average live prices were down about $1.50/cwt. from the week before and averaged a little over $155/cwt. The beef market also slipped lower too, with the Choice cutout losing $6.86/cwt. and the Select dropping $2.57/cwt. Packer margins compressed down to $80/head from $125 the week before. Going forward, I expect that packer margins will continue to shrink as the beef loses value faster than cash cattle prices. By the time we get into February, packer margins could easily be back underwater. Of course, that will depend on how willing packers are to cut the kill in coming weeks. Past placement patterns suggest that the number of market-ready cattle will decline over the next six weeks, so if packers try to keep kills at today’s level they are likely to bid the cattle market back up and thus quickly run margins into the red. Packers did show pretty good discipline this week as the fed kill totaled only 494k, but that was constrained by some weather in the Plains states that probably kept packers from killing as many as they would have liked. Unlike what occurred in December, packers didn’t boost the Saturday kill to make up for lost weekday production. That is a positive sign that they are getting the message that strong kills equals poor profitability. I estimate that they only killed 20k steers and heifers on Saturday this week and I wouldn’t be surprised if next Saturday is even smaller. Once February arrives, we might see Saturday kills at 10k or less. This week’s cow kill clocked in at 153k, which is consistent with where the non-fed kills were before the holidays. I’d look for that to drop off a little in the weeks ahead because tax considerations often cause producers to send more cows to town in January. Steer carcass weights bounced back strongly this week, up 4 pounds, but heifer carcass weights were down 7 pounds. Thus, the blended steer and heifer carcass weight was down one pound. I’m guessing that heifer carcass weights are a little overdone and will show an increase next week, but in general carcass weights should continue to ease seasonally lower. There was a pretty significant band of snow that plagued Nebraska and Iowa this week and feedyards there are starting to get muddy. If we get a couple more storms like that in succession, then carcass weights and the grade in that area of the country could start to come down faster than normal. This week we got the official slaughter totals for December thus we can see that FI steer and heifer slaughter in 2022 was 26.1 million head, which was a half-percent higher than 2021. In fact, S&H slaughter over the past five years has been remarkably steady, with very little variation from the average of 25.9 million head. Viewed that way, it doesn’t look like much of a cattle cycle. More like a cattle flat line. However, the piper is likely to come calling here in 2023 and I’m projecting S&H slaughter to be only 24.5 million head, down 6.1% YOY. That is what has traders so excited and has kept the deferred futures in contango for most of the past year. But as always, I will caution that price is generated from the intersection of supply and demand and just because supply will be down doesn’t guarantee sky-high pricing. The pandemic years produced some exceedingly strong beef demand and I doubt that consumers will be able, or even willing, to keep that up over the next couple of years. Speaking of demand, this week we finally saw rib demand start to collapse and the rib primal price dropped a little over $30/cwt. on a weekly average basis. The attached chart indicates that the chucks and rounds were also softer on the week. The loins have been a pillar of support for the cutout and are way above typical pricing at this time of year. However, the loin primal was exceedingly strong last year at this time and it finally broke lower in the last week of January. So, perhaps the loin cuts are living on borrowed time too. The combined margin worked lower again this week and is starting to look pretty ugly once again. It is not as ugly as the combined margin chart for pork, but both are heading in the same direction. The difference is that beef saw a little bump over the holidays where pork did not. Both chicken and pork are very cheap at wholesale compared to beef, so that has the potential to shift some retail demand in the next couple of months and cause beef demand to under-perform. The next big event in beef demand will be the spring grilling season, but there are a lot of winter weeks left to go through before we get there. The forecast has the blended cutout working lower to perhaps a bottom around $255/cwt. in mid-to-late February. That would be about $15 below today’s level. USDA provided the results of their most recent Cattle on Feed report today and most of the numbers were well aligned with the analysts’ pre-report estimates. December placements were reported down 8% from last year’s very strong number. Those placements were somewhat bigger than what I had dialed in prior to the report, so adopting them increased my production forecasts and lowered price forecasts a bit over the next six months. This week’s futures trade was a bit subdued, as nearby Feb lost a little over a dollar and the remaining contracts losing less. The bullish supply story in the cattle complex makes it difficult to pressure the futures significantly lower right now, but I suspect that as the bearish demand story becomes more obvious the futures will find it easier to retreat. Next week, watch for further erosion in the end meats to help drag the cutout lower and keep an eye on the weather in the Northern Plains since more sloppy weather could hinder performance and thus further limit production.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}