Beef Wrap February 6

no pdf

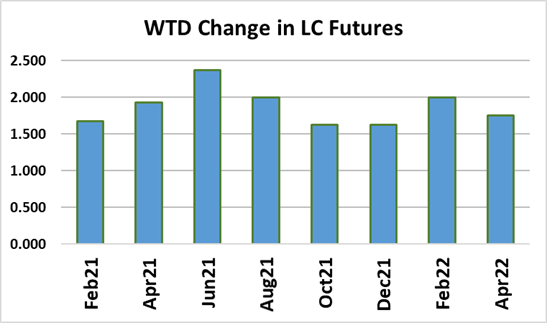

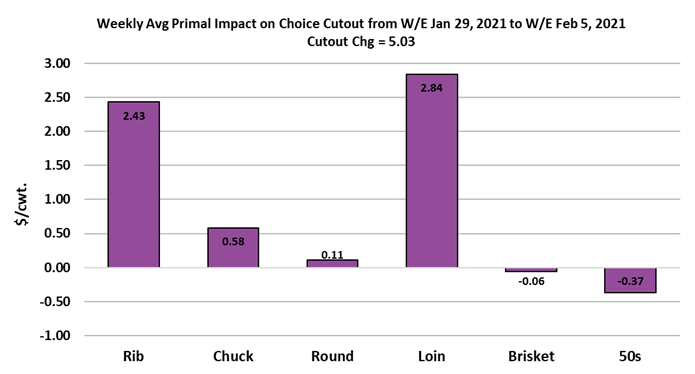

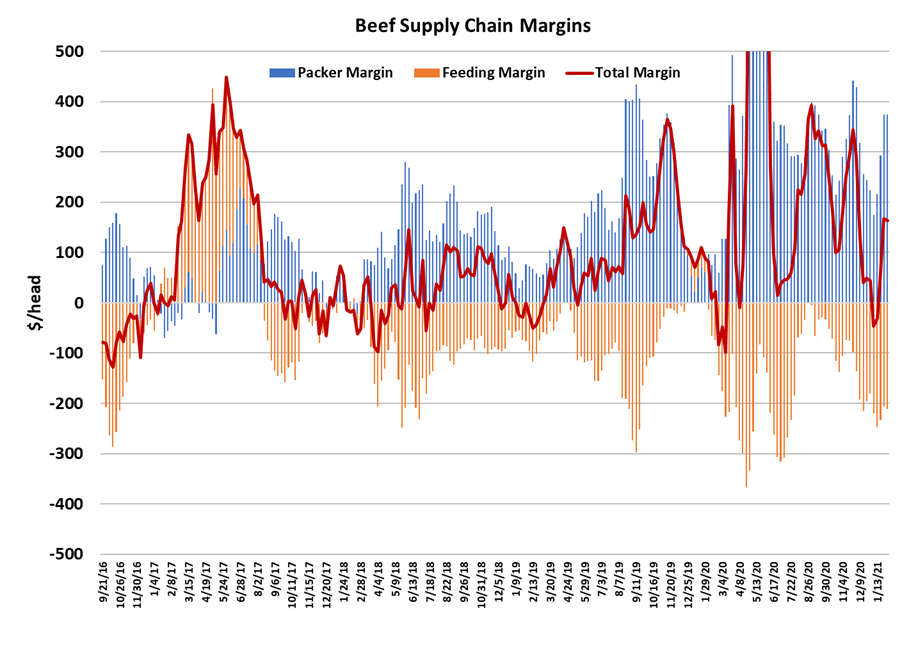

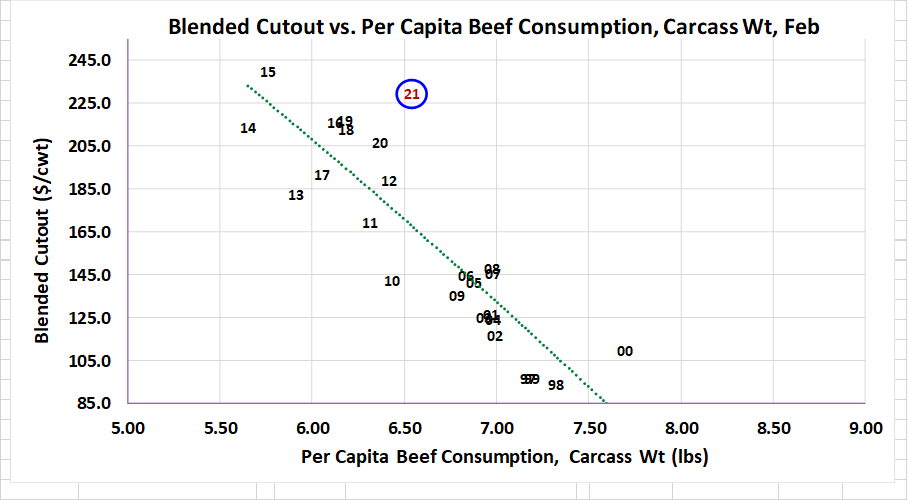

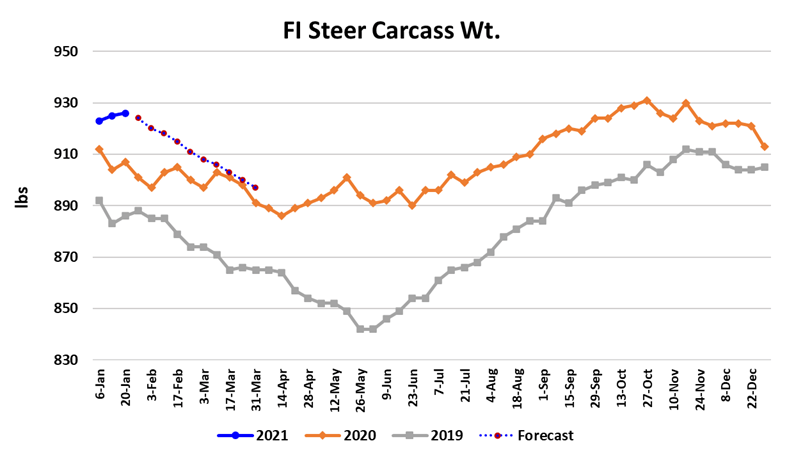

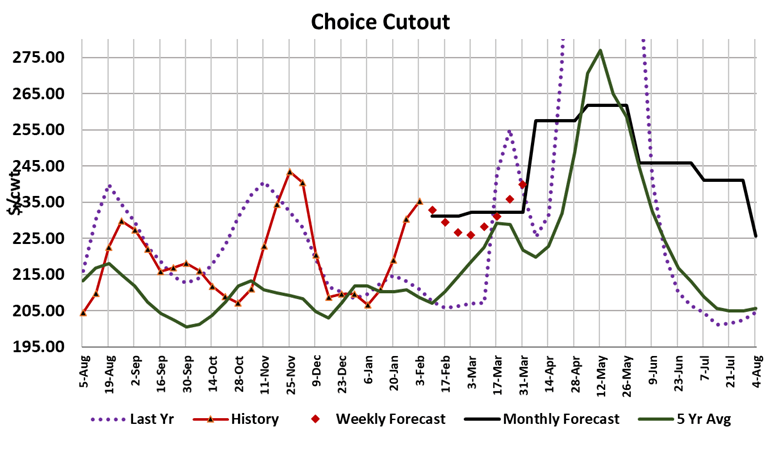

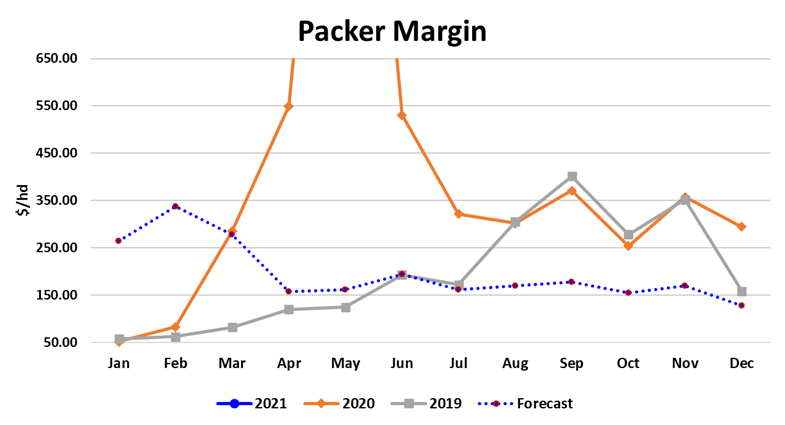

It was another positive week for the cattle and beef complex as cash cattle, cutouts and futures were all higher. Cash cattle traded mostly between $113-114 this week and my guess is that there were more $114s than $113s, but we will only know that on Monday. The Choice cutout gained right at $5 on a weekly average basis and the Select cutout was up about $4. Packer margins were pretty much unchanged this week as the increase in the cutouts offset last weekfs cattle price increase. Margins are close to $370/head. At this point, it is all eyes on the cutouts. They seem to be acting like they are making a top, but that is not a given at this point. Demand is very strong and the combined margin chart below went flat this week. Is it about to turn lower? Possibly, but if it does it will mark a very small rally off its December lows. My fundamental forecast has the Choice cutout pulling back about $9 over the next three weeks toward the $225 area before it starts to rise again in March. I donft think that a retreating cutout necessarily means a retracement of cash cattle prices, but it could. It is normal for packer margins to compress in February and one way for that to happen would be for the cutout to decline while cash cattle stayed steady or bumped higher. That is the scenario that I have dialed in for February. However, it does make me a bit nervous that cattle weights are still so heavy and that might limit producer leverage in the weeks ahead. Another factor to consider is the premium that Feb and Apr futures are carrying to the current cash market. That works in favor of my scenario because it could give cattle feeders the strength to resist lower bids from packers simply by hedging with the futures and then carrying some cattle forward. Of course, there is always the possibility that the cutouts are not done going up yet, in which case rising cash cattle prices are an easy result. One thing for sure is that beef demand has been really good during December and January and the million-dollar question is whether or not that will continue to hold in February. Ifm betting that it will and Ifve got the February demand index for the blended cutout dialed up to 1.14. Last year it was 1.09 and that was an all-time record. Maybe Ifm too optimistic on February demand, but I can still get to a 1.14 demand index and have the cutout fall $9 from this weekfs level. I will admit that the 2021 data point on the February scatter below does stand out. Ifm betting that pandemic-driven demand through retail channels will remain strong in February and thus we won’t see pricing nearly as soft as in Februarys past. This weekfs fed kill came in at 515k, up 4k from the week before and likely the biggest kill until late March or early April. Packers will do a lot of plant maintenance in February. Right now, Cargillfs Dodge City, KS plant is down through Wednesday. There will be others. February is the ideal time for them to get their maintenance projects done. That means that we can look for fed kills to fall back into the 490-500k range for the next few weeks, and maybe all the way through March. The flow model is projecting March fed kills of only 500k, so if kills exceed that during March it could be a sign that some cattle backed up during Jan/Feb. Carcass weights look troublesome. Steer weights topped out a 931 pounds in the last week of October and this weekfs data showed them at 926 pounds. Thatfs only a 5 pound decline over a 13-week period. The normal seasonal would call for a much bigger drop than that. But we must keep in mind that there were still some backlogged cattle around during Nov and Dec and the weather in cattle country was great in late fall and early winter, so that might explain the unusually slow decline in carcass weights. Now however, Mother Nature seems to be stepping up her game and throwing a lot of bitter cold and snow at the Plains States over the next week or so. That could help correct the weight situation, but we wonft know that until 3 weeks down the road when the FI carcass weight data is released. I would feel a whole lot better about my spring price forecasts if carcass weight would start to come down more rapidly. The DTDS is scary high at this point. Sometimes good demand can cover a lot of sins on the supply side and maybe that is what will happen this time with carcass weights. I am encouraged by the export picture. The Commerce Dept data for December was released today and it showed beef exports up 12%. The weekly export data has looked pretty good recently also. So, I feel positive about all of the fundamental factors in this market except for carcass weights.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}