Beef Wrap December 19

No pdf

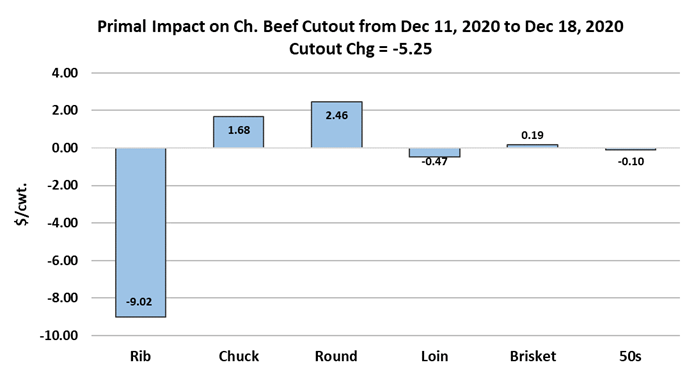

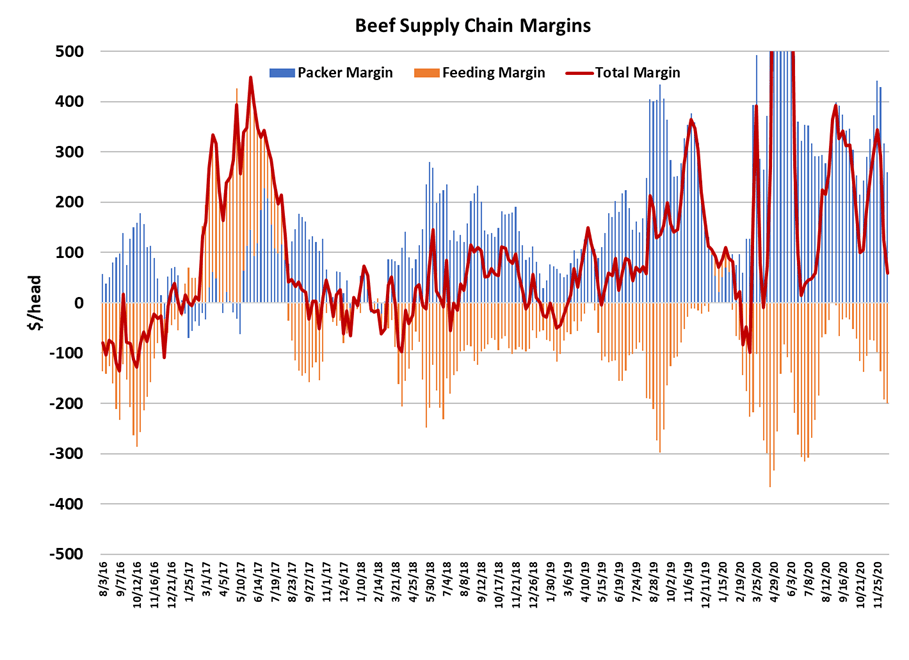

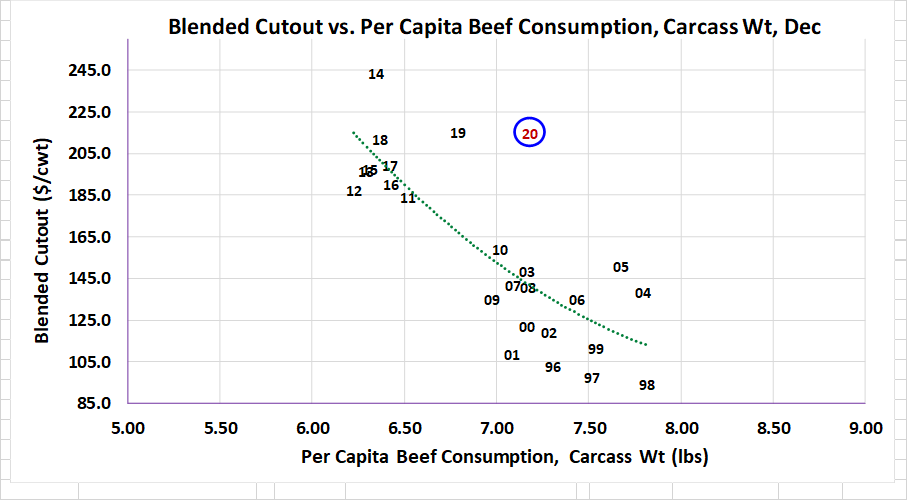

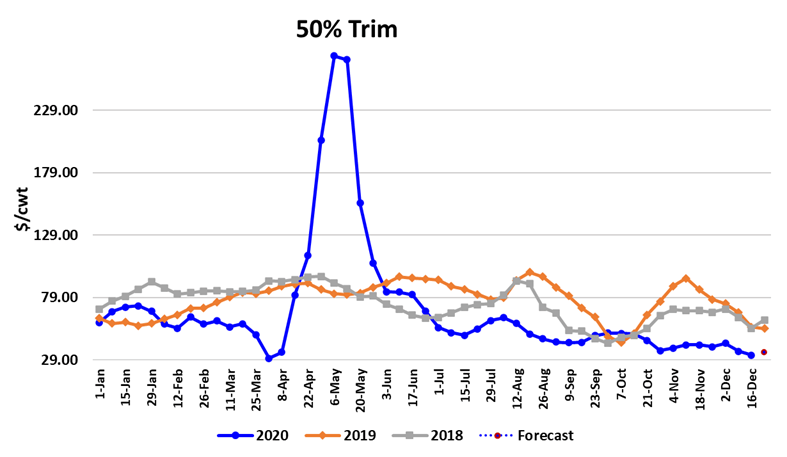

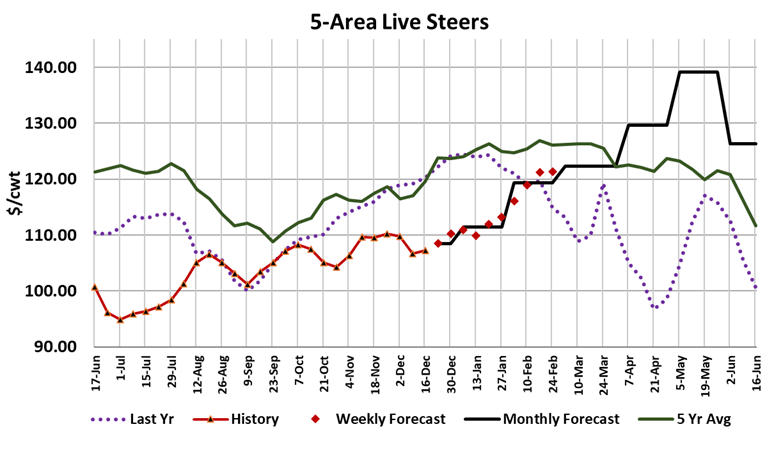

Cash cattle traded in a pretty wide range this week with some $105 being reported and, at the other end of the spectrum, some $108 trades reported in the south late in the week. Some cattle feeders were willing to sell their cattle to the board this week at $108-109 by tendering delivery certificates. When those got re-tendered, a packer stepped in and demanded those certificates with $1 attached. That means some packer was eager to pay $107-108 for cattle. I take that as a bullish sign. The Dec contract traded above $110 today and that might draw more deliveries. Perhaps traders are anticipating packers giving the feeders a little ¡°Christmas gift¡± in the form of higher prices in the last two weeks of the year. The cutouts continued lower this week, but at a much slower rate than in the past couple of weeks. End meats attracted some buying interest and that helped to slow the cutout¡¯s decent. The Choice lost $5.25 while the Select was down $1.44. The rib primal continues to tumble lower now that the holiday buying is behind us. I still think that we have a little further down to go in the cutouts, but not a lot. The 50s look awful, quoted today in the low $30s and that is never a good sign. However, as we move into January, value meats become the focus and ground beef is normally a strong retail feature early in the new year, so perhaps the 50s will get a lift from the demand side once the holidays are behind us. The 90s are also relatively cheap, now trading close to $200, so retailers ought to be able to put together some really hot pricing on ground beef in January. Beef demand has been in a seasonal downtrend and the combined margin chart below indicates this is still ongoing. However, it looks to be very near a turning point, so by the time the calendar turns to January we could be experiencing a rebound in beef demand. Overall demand remains very strong as illustrated by the December scatter diagram below. The 2020 data point is riding very high¡ªstronger than even last year—and there is some risk that it may work higher before the month is done because I’m forecasting further price weakness over the holidays and if that doesn’t happen then the 2020 data point will rise on that scatter. As I discussed in this week¡¯s special RMO, the covid pandemic has been a net positive for beef demand and it looks like Dec, Jan and probably Feb are going to be “strong covid” months. Thus, I don¡¯t really expect much risk to beef demand for at least a couple more months. The fed kill this week clocked in at 519k, 5k smaller than last week, but there were some minor plant disruptions that were evident in the daily slaughter data. I¡¯ve got next week¡¯s fed kill pegged at 365k, and then 415k in New Year¡¯s week. After that, fed kills should rise to around 530k per week in January before pulling back to the low 500s during February. Steer carcass weights were reported one pound higher this week and are running about 1.8% over last year. I suspect that excellent weather in the cattle feeding states is slowing the rate of descent in carcass weights and the two short kill weeks ahead won’t help in that regard. This week¡¯s deterioration in the cutouts pushed packer margins lower, now at $260/head. Margins should continue to work lower during January toward an annual low sometime in February. Overall fed beef production this week was about even with last year and that makes one wonder, if production is the same and demand is better than last year, why are fed cattle prices $12 below last year? That comes down to cattle feeder leverage and carcass weights and the DTDS are telling us that they just don’t have the kind of leverage they had last year at this time. That too will rectify, but it may not be until the end of January or early February. Some winter weather would certainly help temper carcass weights and thus push the leverage meter a little more in the cattle feeder’s direction, but right now the forecast isn’t offering much hope for that. I¡¯d look for feeder leverage to improve in Jan/Feb as weights come down further. Demand should stay strong and the cutouts should average close to last year during Jan/Feb. Cash cattle averaged $115.50 last Jan/Feb and it looks like they are on their way there again, although it is reasonable to expect the lowest prices in early Jan and the highest in late Feb. Today¡¯s Cattle on Feed report pegged November placements down 8.9%, which was only 1% larger than what I had plugged in, so the survey numbers didn¡¯t change my forecast much. It still looks to me like the Apr-Jun period has the potential to be price explosive as supply will tighten dramatically at a time of year when demand should be surging seasonally. The next two weeks will not provide us with much in the way of good fundamental data. USDA won¡¯t issue reports on the 24th and 25th and trade is likely to be light in both the cash cattle market and the beef markets. Watch the cutouts for signs of a bottom.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}