Beef Wrap August 31

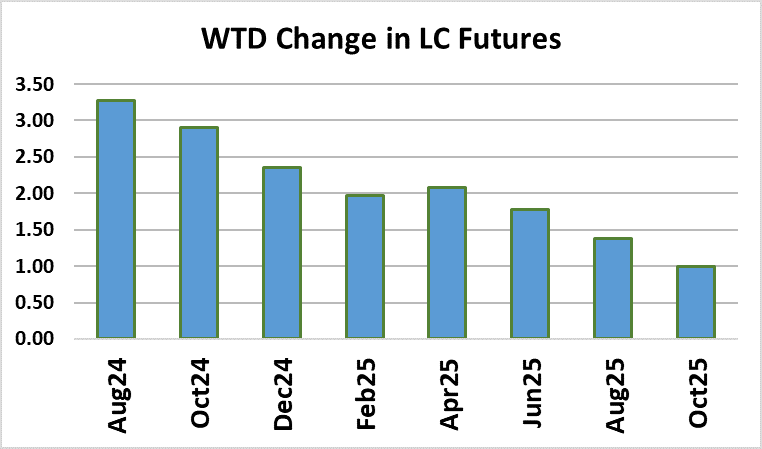

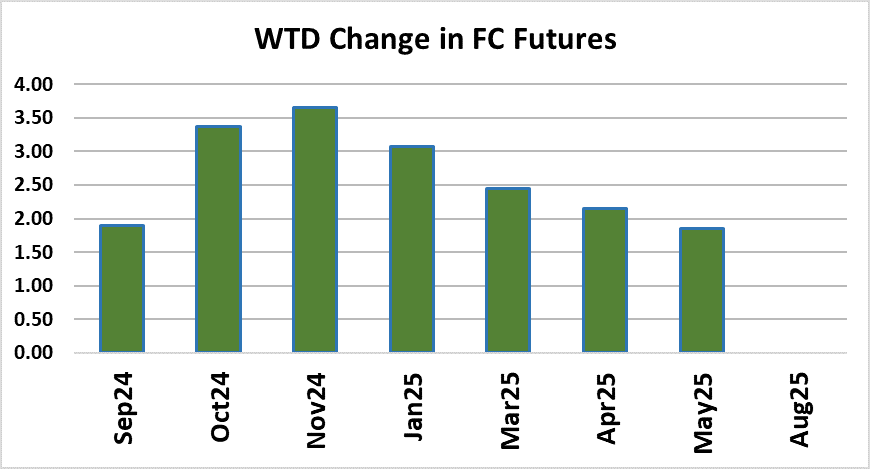

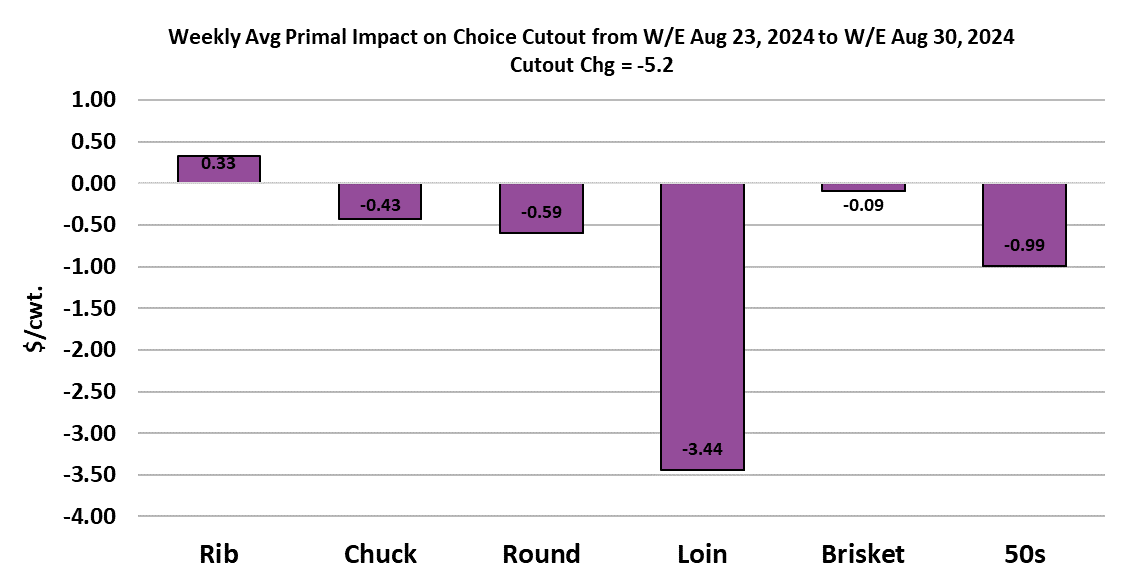

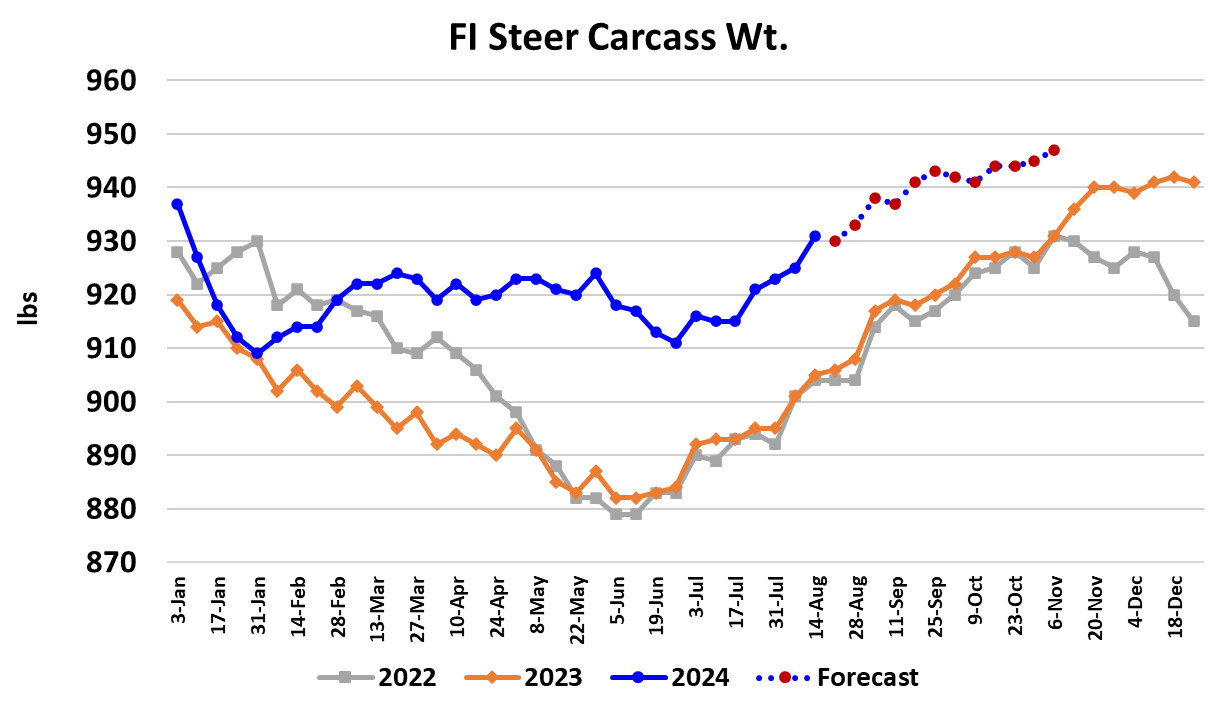

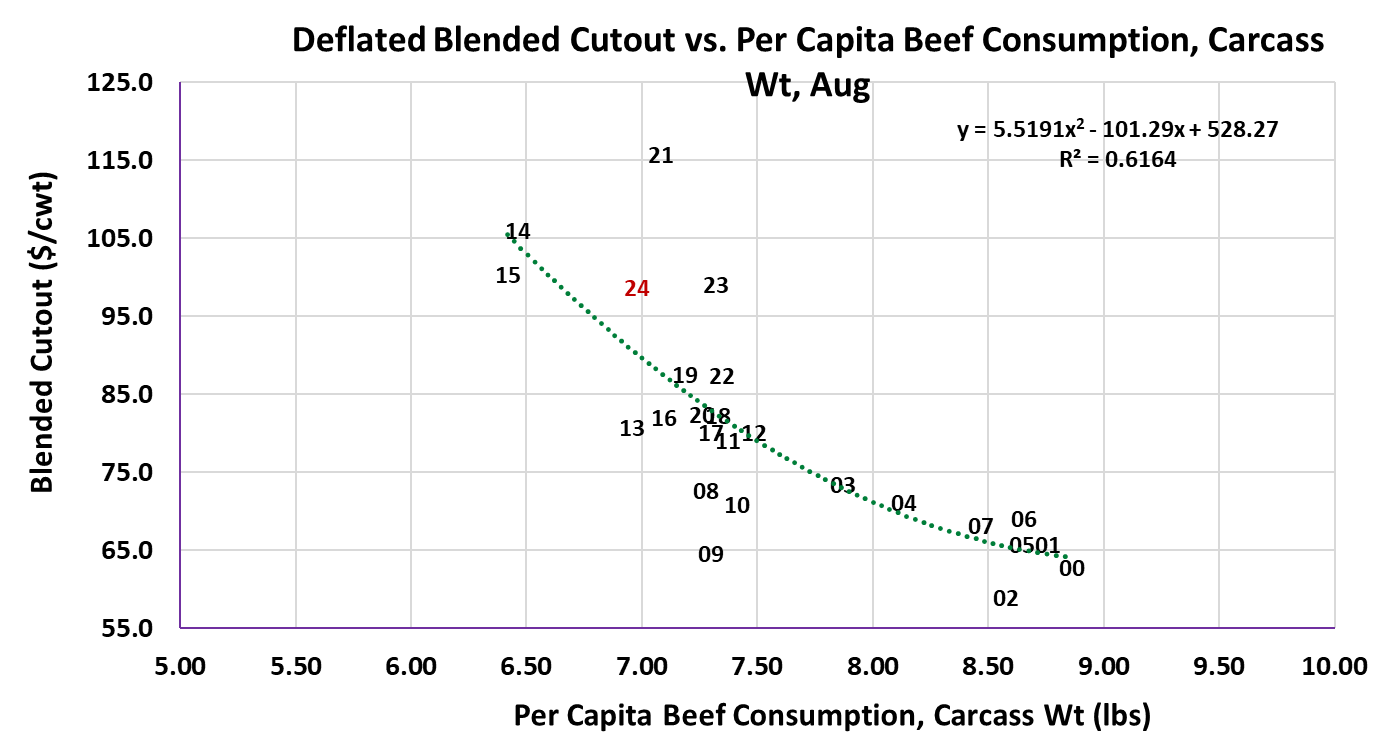

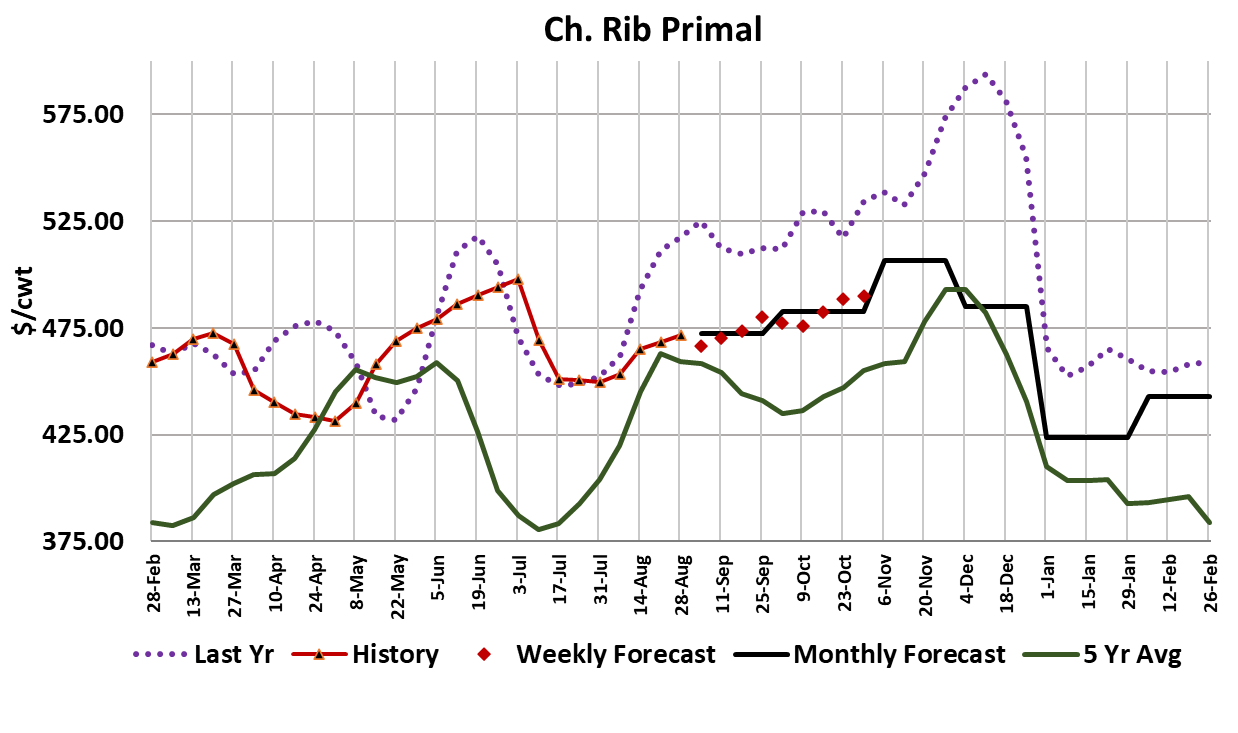

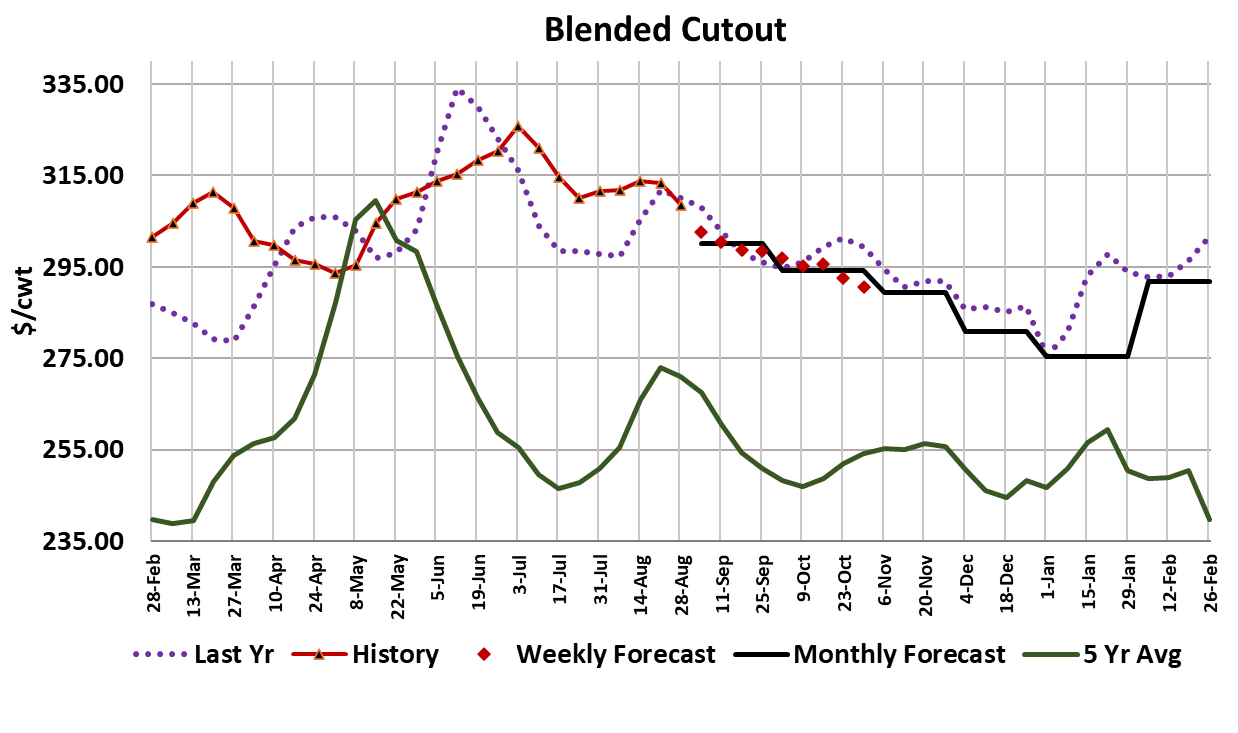

The beef cutouts continued lower this week, with the Choice dropping $5.20/cwt. to average $310.63 and the Select losing $3.31 on its way to $298.02. This week’s decline was largely driven by a big drop in the loin primal and a sharp down move in the price of 50s. Choice striploins were responsible for the loin’s share of the loin decline as Labor Day buying dried up. The 50s, which averaged close to $163 last week, printed closer to $139 this week—a nearly 15% decline in one week. Some of that can likely be explained by light processor demand in anticipation of reduced hours next week, but carcass weights are getting heavier by the day now and that is also playing a role. Demand for trims generally softens moving into September because the summer travel season is complete. The one part of the complex that isn’t showing much weakness is the lean trim, where the 90s were up marginally from last week while the chuck and round primals were down only slightly. We should see the 90s start to ease in September as well, but I wouldn’t look for a big price decline. That means that the chucks and rounds also probably remain relatively firm and that should provide a pillar of support that keeps the cutouts from dipping too low in September. The cash cattle market traded lower again this week with trade in the South steady to slightly lower around $182-183 while trade in the North was down about a dollar to $184. When all of the data are tabulated on Tuesday, I expect the 5-area price to be in the vicinity of $183.80, which would be about $1.75 lower than last week’s average. The 5-area price, which is the closest thing to a national average price that we have, has gone from $195 to $184 in five weeks. The Aug24 live cattle futures expired today at $185.85, which is about a $3 premium to this week’s price in the South. That looks a little rich, but there were no contracts open at expiration, so there will be no deliveries next week. Now Oct24 moves into the spot position and it added almost $3 this week to finish at $178.60. That suggests that traders still expect a few more dollars of downside movement in cash cattle prices over the next few weeks. I can’t argue with that, but available cattle numbers should be tightening up as we approach October and that could cause the cash to turn higher as Oct moves into delivery near the beginning of the month. The fundamental forecast has fair value for Oct expiration around $182-183, and if I’m wrong about that, I may be too low. This week’s kill was estimated to be 494k for steers and heifers and 117k for cows and bulls. That was a little larger than expected, so perhaps packers were trying to build some inventory ahead of next week’s short kill. The fed kill next week is likely to be below 440k. The FI steer weights jumped 6 pounds this week and that leaves them now 26 pounds heavier than last year. Steer and heifer beef production during September is expected to run about 3.5% stronger than last year, mostly as a result of heavier carcass weights. The attached scatter diagram projects domestic beef demand during August to be stronger than normal, but not as strong as in August of last year. I’m getting the sense that domestic beef demand is slowly eroding, so that is something to keep a close eye on over the next couple of months. It will be interesting to see how the middle meats perform in Q4 this year, since that will have a big bearing on our demand readings. Right now, the rib primal is about $50 lower than it was last year at this time and while that gap may close some in the fall, I suspect that ribs will have a hard time matching last year in Q4, simply because of heavier carcass weights. The smaller ribeyes that foodservice prefers may be more difficult to source this year, but there could be an abundance of the heavier variety that typically moves in retail channels. Export movement still looks lukewarm in the weekly data and I don’t think that we can count on big buying from China this fall, so that probably means that exports don’t really impress in the second half of the year. The weather forecast for the holiday weekend looks like a mixed bag, with good weather out west, but lots of rain near the population centers on the East Coast. That suggests that clearance at retail may only be so-so and that would limit fill-in business after the holiday. Next week, look for the cutouts to drop a few more dollars and the cash cattle market to trade steady to a little softer.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}