Beef Wrap August 2

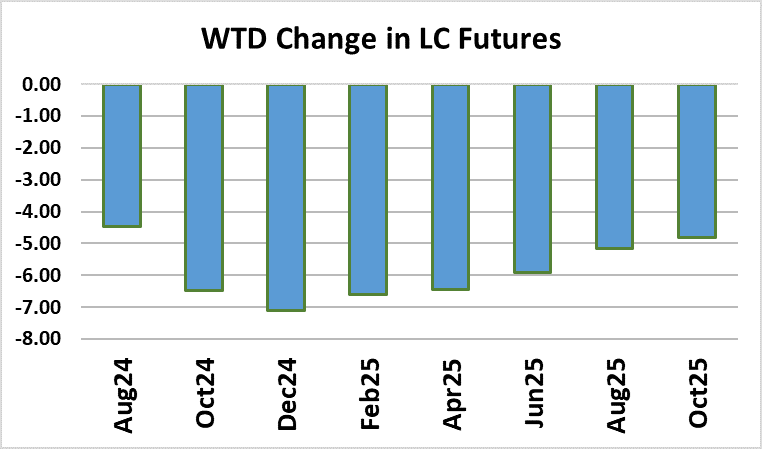

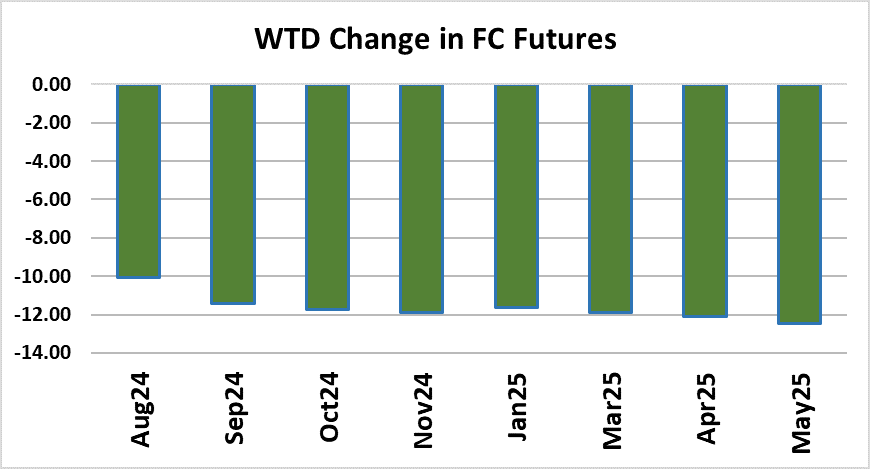

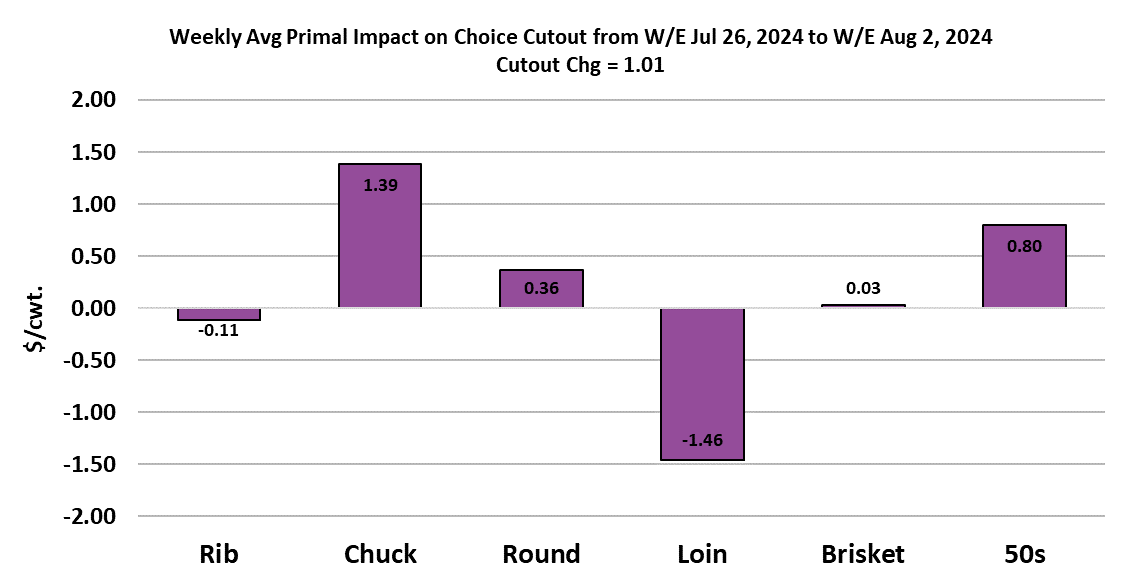

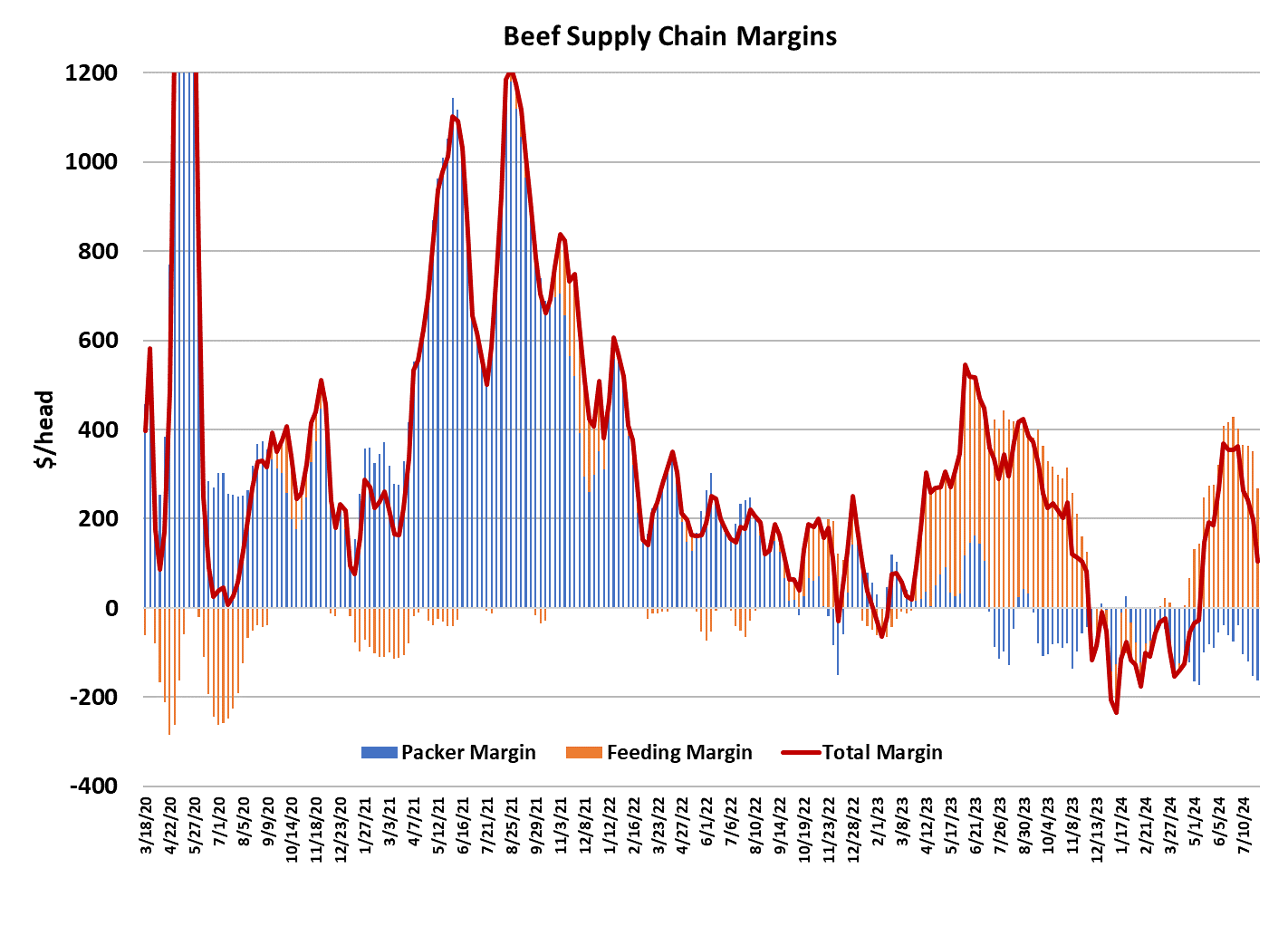

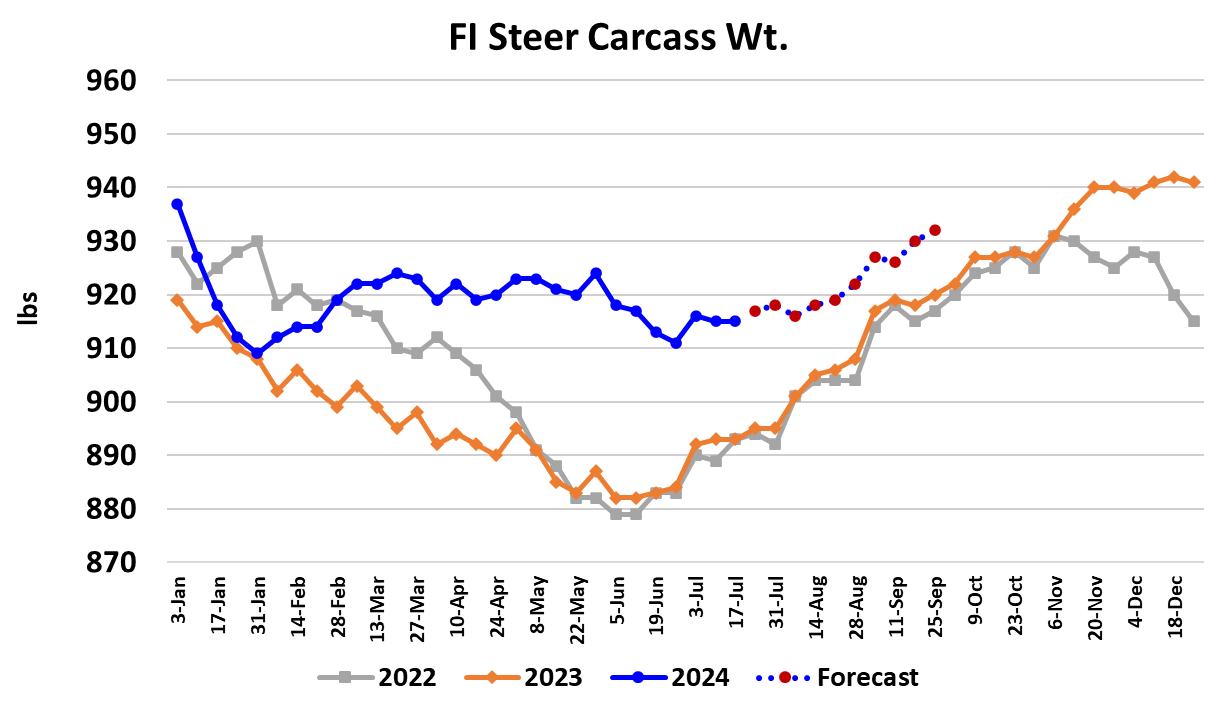

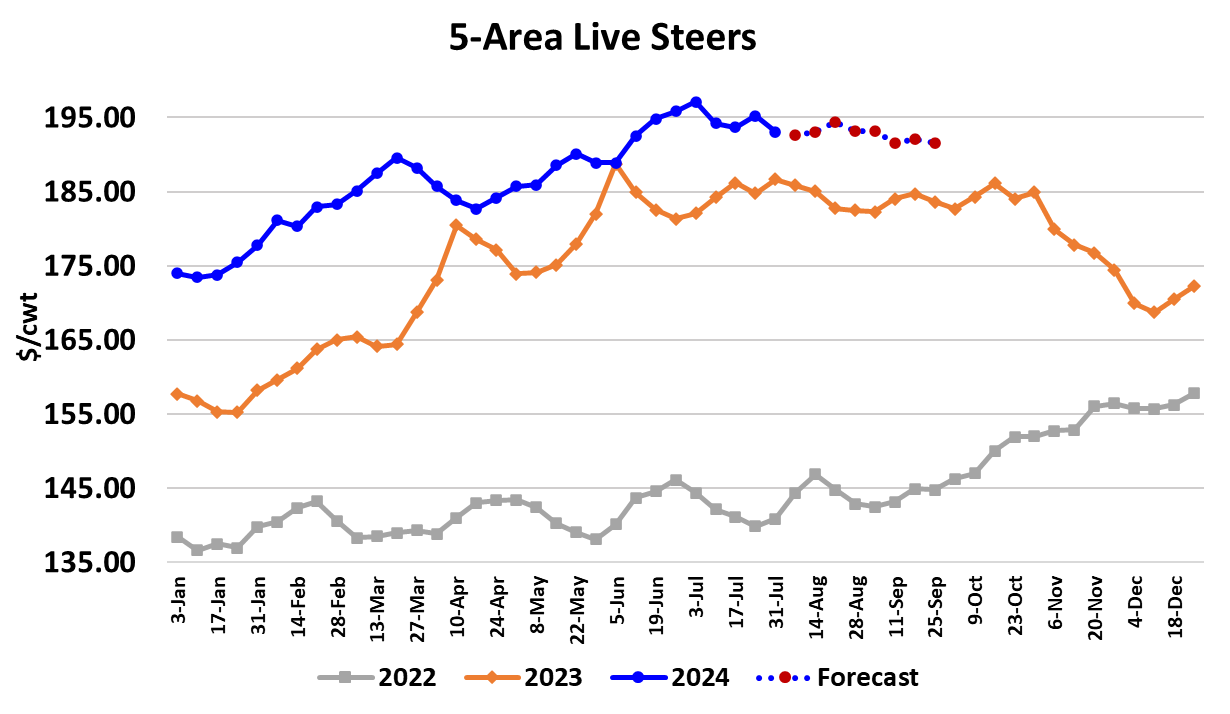

It was a bit of a “good news/bad news” week in the US cattle and beef complex. The good news was that packers were finally able to end the slide in the cutouts, as the Choice added $1.01 on a weekly average basis and the Select was up $3.23. The bad news was that the futures crashed hard on Thursday and Friday, knocking from $4-7 off of the live cattle contract and $10-12 off of the feeder cattle contracts. That sell-off seemed to be precipitated more by outside events than any negative shift in cattle market fundamentals, so there is a good chance that at least some of those declines will be recaptured next week. The outside event was primarily a meltdown in the stock market, that was likely the result of an overbought condition in combination with macro data on Friday that pointed toward a faster deterioration in the labor market than was anticipated. Traders seem to be reading that as an indication that a recession is coming and assuming that will put a dent in beef demand. The Federal Reserve is coming to the rescue with interest rate cuts, but those likely won’t be announced until it meets again in the middle of September. As a result, traders are now worried that the cuts will be “too little, too late” to avoid a downturn in the economy. The reaction in the cattle futures market seems way overdone and perhaps unwarranted because a close look at the historical data suggests that beef demand only suffers in a big way during the most extreme economic downturns, like the Great Recession that was spawned in 2008. Economists have struggled to find a statistical link between garden variety recessions and beef demand and this situation is much more like the garden variety than like 2008. In fact, there is no hard evidence of a macro downturn at present, so even the assumption that a recession is on the way might be a big stretch. One thing that I’ve learned in watching the cattle market over the years is that sell-offs that are not caused by a significant, measurable shift in cattle or beef fundamentals don’t usually stick—the market tends to bounce right back within a few days. Those that are driven by fundamentals are much more likely to stick, or even accelerate downward. One telling sign that occurred during this week’s sell off is that there wasn’t an immediate rush by cattle feeders to get cattle sold. When things turn ugly in the futures and cattle feeders immediately start accepting lower money in the cash market, that is a sign that the cattle feeders’ hand was weak before the event. This time, cattle feeders were relatively calm and really hadn’t moved very many cattle as of press time on Friday afternoon. That suggests that they think their hand is relatively strong. There were a few cattle traded in the South at $188, which was down $2 from the previous week and some in the North moved at $196, also down $2, so I’m going to presume that is where the bulk of the trade will end up and we should end up with a 5-area weighted average close to $193 for the week. This week, the middle meats exerted some modest downward pressure on the cutout while the end cuts provided positive pressure. The 50s were the tie-breaker, averaging almost $160 for the week and $17 higher than the week before. There is little doubt that overall beef demand has been softening over the past few weeks and the combined margin confirms this. Packers were only able to stabilize the cutout by reducing the fed kill. However, demand should start to improve modestly as we move deeper into August, unless beef buyers who are watching what has happened in the futures step back in anticipation lower prices to come. When that happens, and it certainly could happen in the current environment, we usually end up with the beef buying community getting very short bought and that creates the risk of a sharp move higher at some point down the road. This week’s fed kill came in close to 485k, just about even with the week before. That is smaller than what the flow model suggests should be ready in August, but not by much. Packers will need to continue to keep kills constrained for several more weeks in order for it to back up enough cattle to make a material dent in cattle prices, absent outside events. FI steer weights were reported steady with the week before at 915 pounds and that comes at a time when weights are normally increasing. The gap to last year is now +22 pounds for steer weights and will likely shrink further in coming weeks. This week’s beef production from fed animals was 2.6% higher than last year, but non-fed beef production was down over 14%. As a result, total FI beef production looks like it was flat to slightly lower than last year. It is the lean end of the complex that is getting shorted at present and that is where we should expect to see the most resistance to lower pricing in coming weeks. Packer margins are still dismal, registering -$165/head this week. Those margins should improve a little next week if the packers manage to get the showlist bought cheaper this week, but they will still be deep in the red. Unfortunately for packers, red ink is likely to be the norm for the next couple of years. Next week, look for a little more slippage in the cutouts and perhaps another $1 or so down in the cash cattle market. Some recovery in the futures is also likely.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}