Beef Wrap August 13

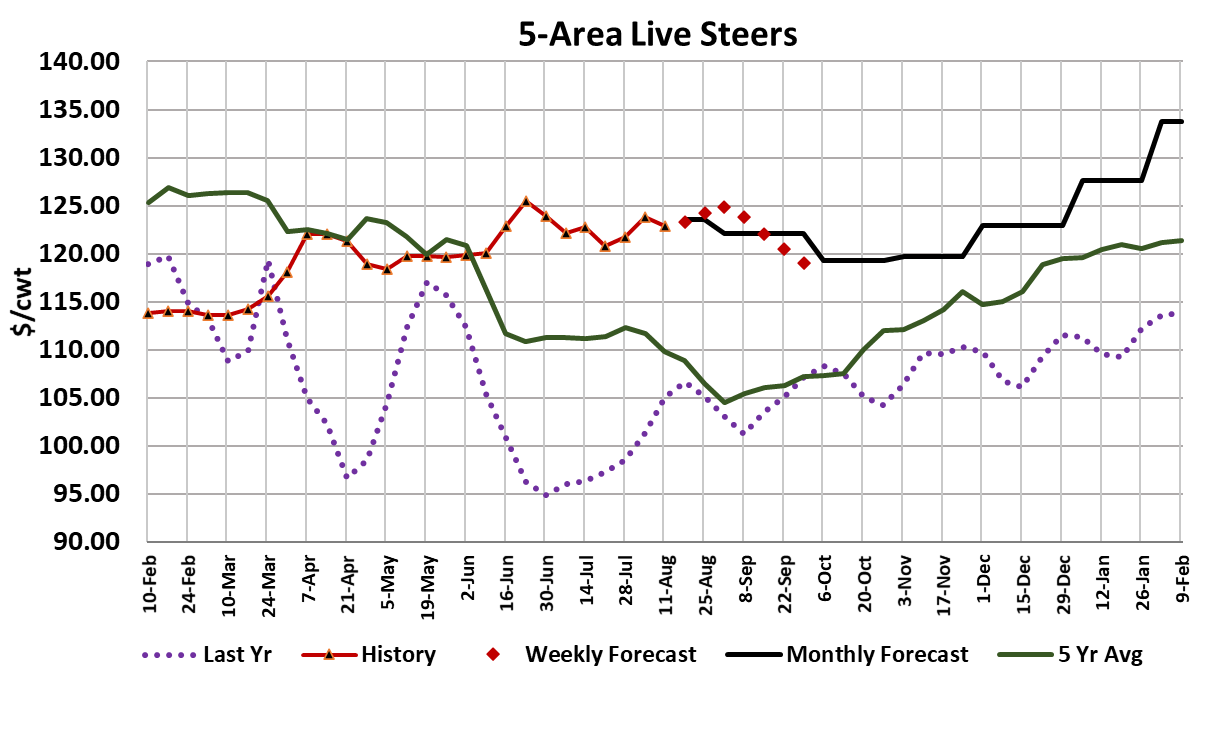

Cash cattle averaged about a dollar lower in the live markets this

week at $122.84. The dressed markets, which are primarily in the

north, were about $2 higher. Beef markets continued to soar with

the Choice adding almost $23 on a weekly average basis and the

Select adding a little over $18. At this rate, it won’t be long before

the beef market eclipses the high that was set back in early June.

What in the world is going on with this beef market? It is hard to say

for sure, but I would bet that it has something to do with the

resurgence of COVID infections in the US. That is the only thing that

has really changed since the beef market bottomed earlier this

summer.

We already know that stay-at-home behavior is positive for beef

demand and with infections rising, more people are probably back in

stay-at-home mode. We also had the Child Tax Credit stimulus,

which was paid out for the second time today. Those monthly

checks that range from $250-300 per child are going right into the

bank accounts of some of the poorest Americans. They naturally

want to upgrade their diet. Finally, there may be a certain amount of

quiet stockpiling going on by consumers. People who thought the

pandemic was coming to an end earlier this summer may have

worked down their freezer stocks of meat and now that the

pandemic is back on full-bore, they are restocking. Further, people

also stockpile when they sense that inflation is rising. Buy it now, or

pay more for it later. Inflation measures have certainly been strong

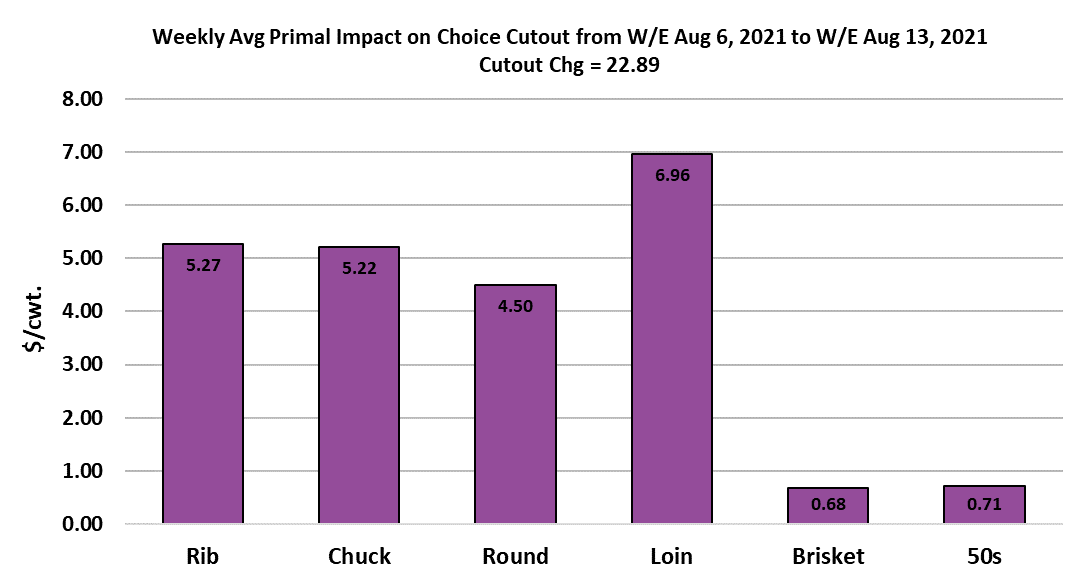

recently. The chart below indicates that all of the primals except

briskets and 50s were major drivers of this week’s cutout gains.

And, briskets and 50s are not really cheap either. Whenever I see

broad-based move like that in the cutout, it suggest that the demand

curve for all beef has moved outward. Stockpiling would do that.

Stimulus money would also do that.

I’ve notice that in my local retail circular there is much less meat on

feature and the price levels are not all that attractive. USDA

released their retail beef price data for July this week and it showed

retail prices were about 6.5 cents per pound higher than the record

set in June. My guess is that August retail prices will be even higher

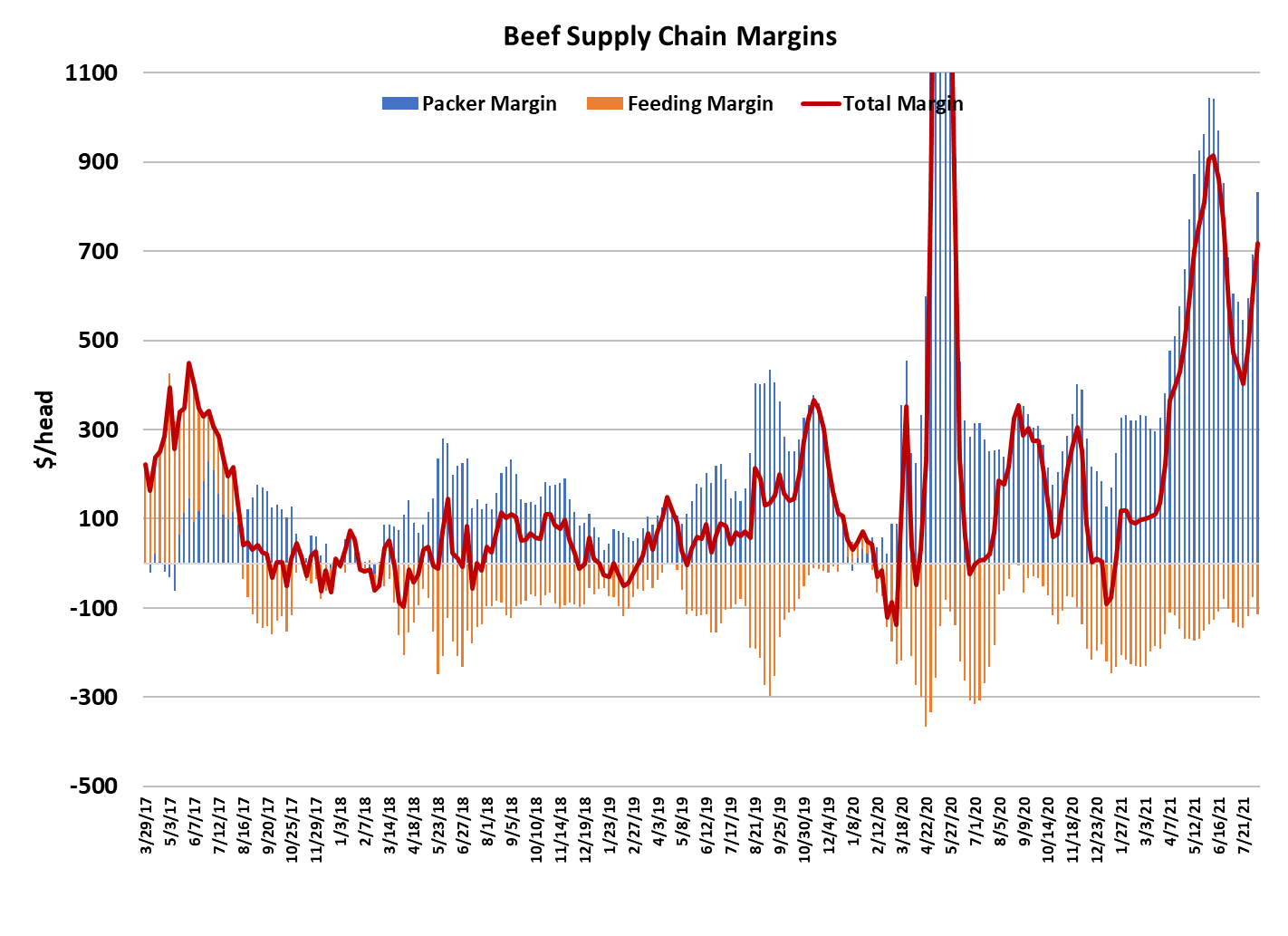

than July’s. It feels a lot like an inflationary spiral is in place. The

combined margin chart shows that the second wave of super strong

demand is in place and could easily outperform the previous top with

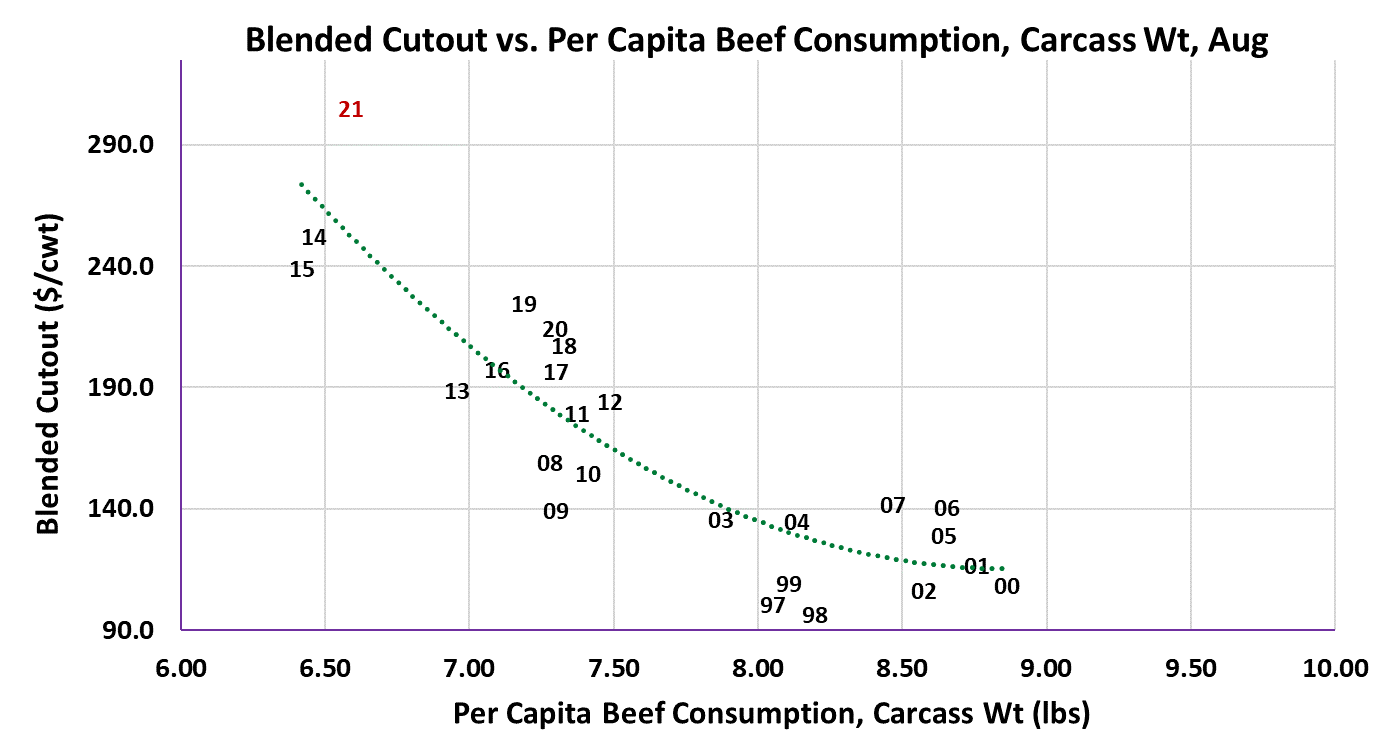

a few weeks. I’ve also included the price-quantity scatter diagram

for August below. The thing to note here (besides how high the

2021 data point is from the line) is how small per-capita domestic

availability is.

It is on the order of what we saw back in 2014 and 2015. That is

being caused by small fed kills as labor problems keep packers

from processing normal levels of cattle. So, there is a supply side

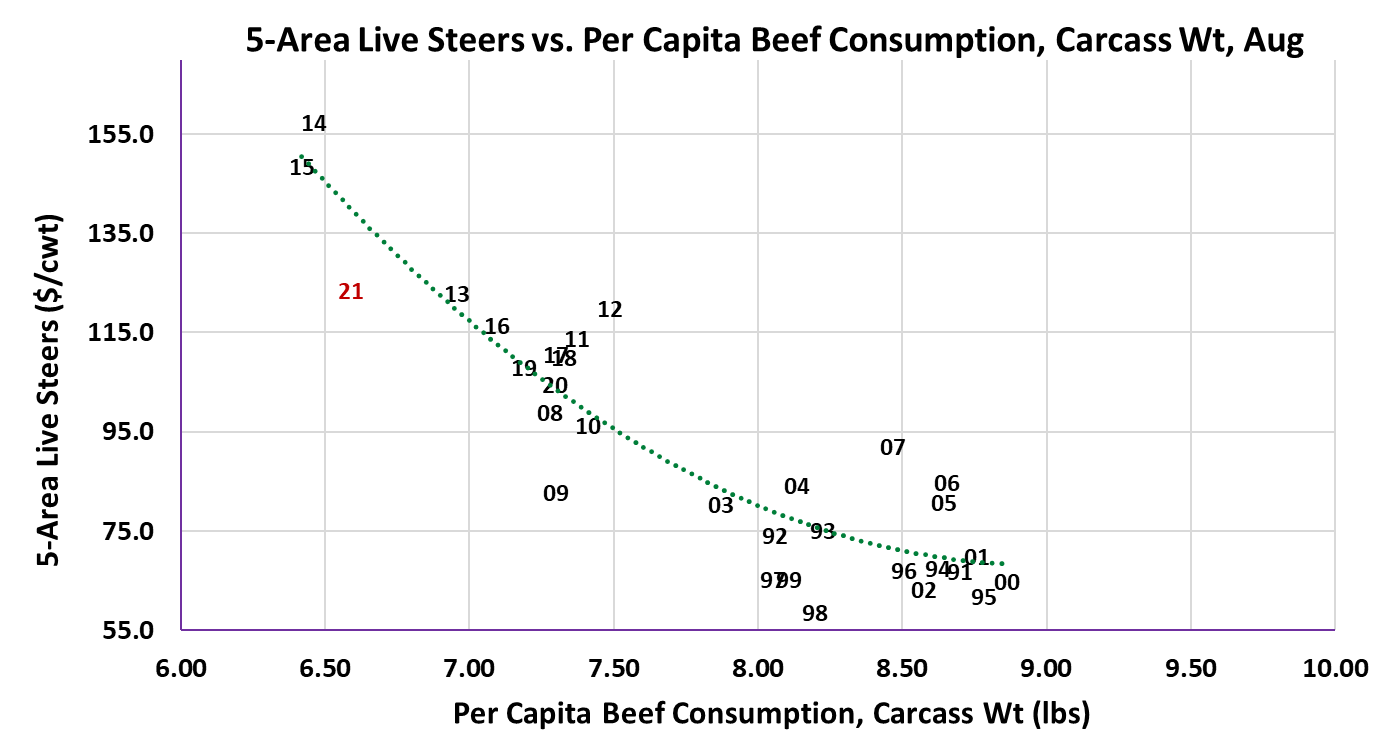

component to this rally as well. Now look at the second scatter

diagram below which plots the cash cattle price against the same

per-capita consumption variable. Back in 2014-15 when beef

supplies got really tight, cash cattle prices were up around $155

because there were no bottlenecks in the system and packers had

to compete vigorously for cattle.

The difference between then and now is that back then there was a

real shortage of cattle and plenty of processing capacity. In 2021,

we have plenty of cattle and a shortage of processing capacity. As

long as that persists, I think we can expect cash cattle to trade in

the $120-125 range, regardless of what the beef market does. I

calculate packer margins this week at $858/head and poised to go

well over $900/head next week. Tyson’s stock surged almost 15%

this week when they reported on and extremely profitable quarter.

Anyone who was paying attention to the meat markets should have

seen that coming. The next quarter will likely also be profit

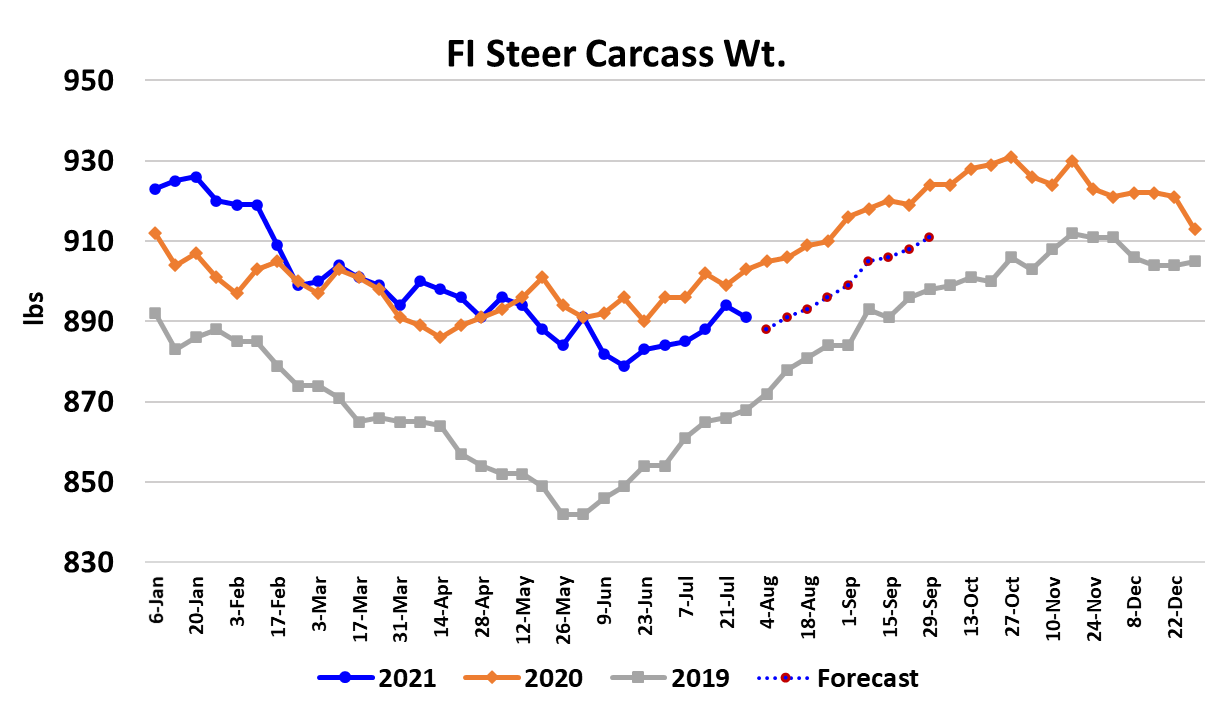

blockbuster for meat companies. This week’s fed kill only

registered 505k, which is below what the flow model suggests

should be available during August. That said, the weight indicators

do not suggest that cattle are backing up in feedyards to any

significant degree. Steer carcass weights actually declined 3

pounds this week when the normal seasonal would have them

increasing. The DTDS weights also suggest that cattle are not

overly heavy at the moment. The futures were largely unchanged

on the week, except for nearby Aug, which lost almost $2 Friday-toFriday. The Aug contract has had to contend with a slew of

deliveries as cattle feeders in the South attempt to score a better

price for their animals than what the packers are offering in that

region.

Ultimately, I’m looking for cash cattle prices to decline this fall, but

in order for that to happen, beef prices will need to cool off a lot.

For now, traders will be best served to delineate the trading range,

sell when prices near the top of the range and buy when they near

the lower end. Next week, watch those cutouts. Will they gain

more next week than they did this week? I’m not forecasting that

by any means, but it really wouldn’t surprise me if this strength in

the beef market continues unabated.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}