Pork Wrap May 21

Pork packers have done a superb job of reclaiming their margin after it

almost went to zero three weeks ago. They figured out that all they

needed to do was to cut the Saturday kill down to almost nothing and

suddenly their margin began to improve. This week it stands at $11/

head, which is outstanding for this point in the year. The kill reduction

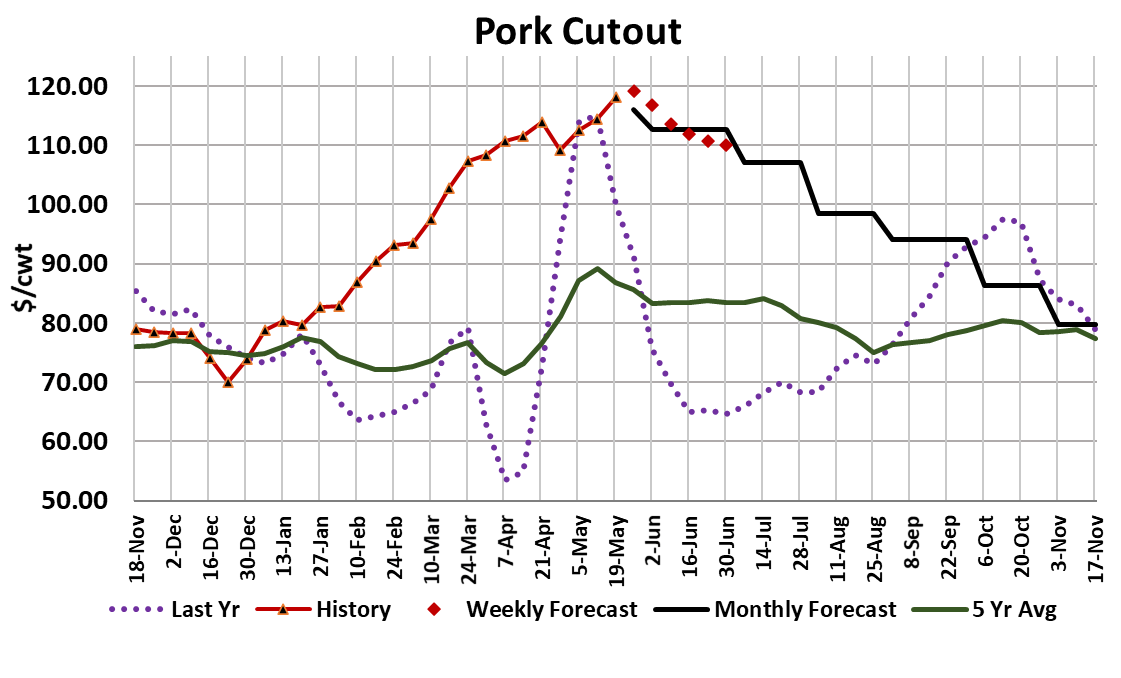

has helped the cutout move higher (up $3.67 on a weekly average basis)

and the cash hog market move lower (WCB down $4.33 on a weekly

average basis). Both the cutout and the negotiated cash hog market

figure into the LHI calculation and I estimate that the LHI is currently

about 2/3rd negotiated hogs and 1/3rd cutout. That means the LHI is

going to have a hard time advancing further as long as the negotiated

market is on the defensive.

The cutout made a big jump today and that ignited a futures rally that

saw the Jun contract exceed $114.50, more than $3 over today’s LHI.

Now it is possible that that the negotiated market could turn higher, but

the way it has moved steadily lower tells me that we have already passed

the tightest hog numbers. Further, if the cutout stalls or turns lower,

there will be very little hope of turning the negotiated hog market higher

because packers will be back in margin management mode. I guess a

good question at this point is, “What are the odds of the cutout stalling or

turning lower?” Given that the cutout has only declined one week since

December, the odds don’t look very good, but all of the last-minute

Memorial Day business is complete now, so there could a little let-up in

demand next week.

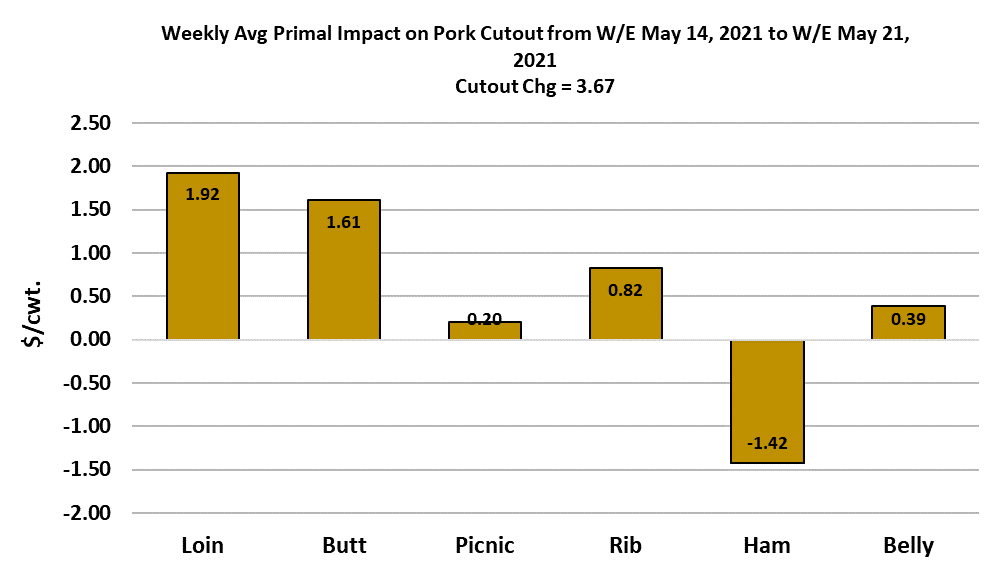

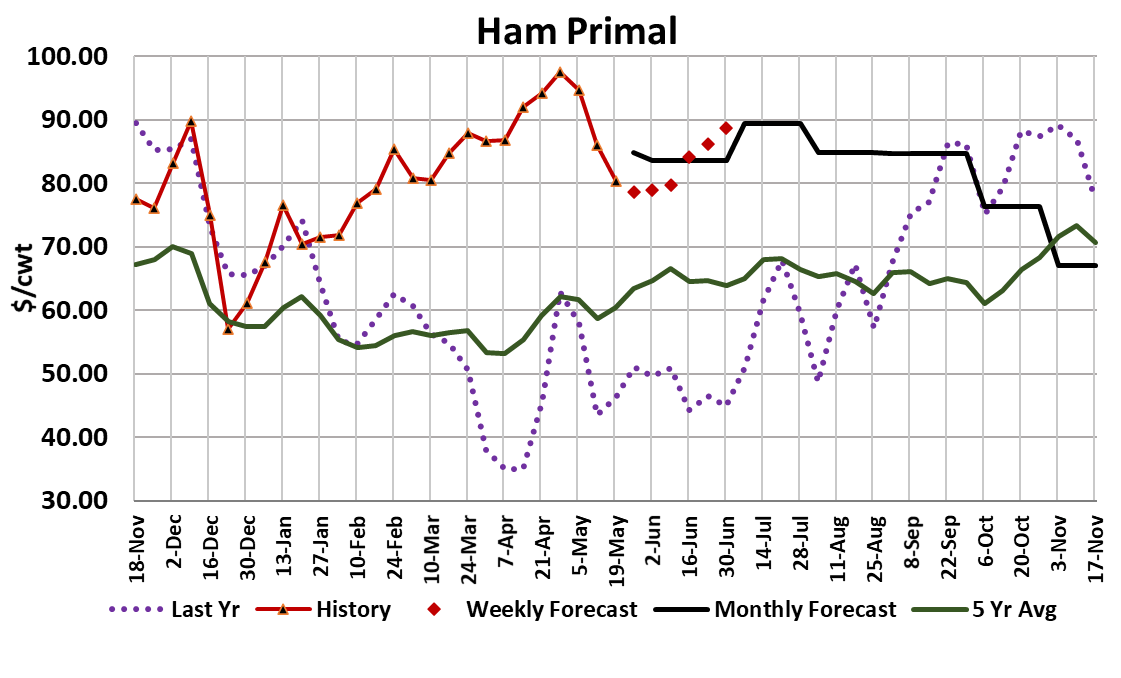

All of the primals were higher this week except hams, and those made a

fairly strong recovery on Friday. The logical place for price weakness to

develop would be in the retail cuts—loins, butts, ribs as demand at retail

scales back post-Memorial Day. But there is really no guarantee that

demand at retail fades after the holiday. This is a very unusual demand

situation that we are in and it feels more like demand is permanently

moving to a new, higher level than simply cycling up and down every

couple of months. Retailers are not balking at paying a $120 cutout

because their customers are not balking at paying whatever price they

slap on pork in the meatcase. Still, from an analyst’s perspective, it is a

lot easier to forecast a declining cutout from these super-high levels than

it is to forecast it continuing higher.

I’m looking for a modest decline in the cutout during June, but have it

holding above $109 until the end of the month. The combined margin

gave a hard head fake about three weeks back and is now continuing

higher. It has double-topped like that before and when it did, it signaled

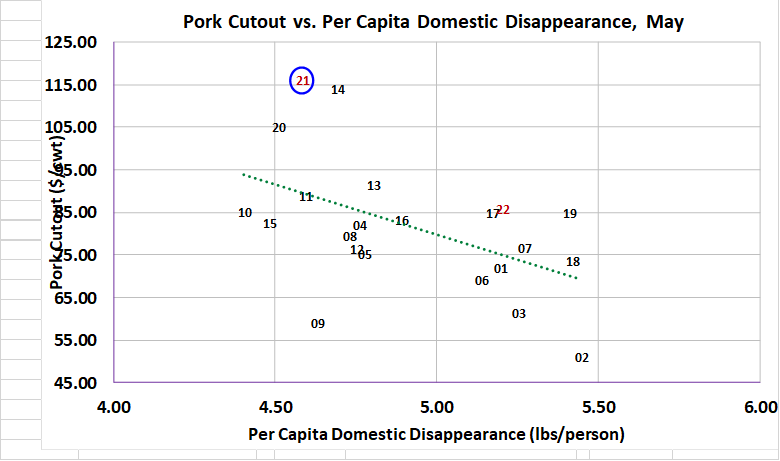

some softening shortly thereafter. I’ve included the price-quantity scatter

diagram below for the month of May and you can see how incredibly

strong demand has been this year.

Pork demand is also being supported by really high beef and

chicken prices. It seems to me that when one of that trio starts to

soften substantially, the other two will follow. Since pork is the one

that got this demand party started back in the winter, it is a good

candidate to turn lower first. Today’s big increase aside, I’m not

sure I’m ready to look for the hams to appreciate much in the nearterm and the bellies are not acting like they will make a big move

higher either. Together, those two primals represent about 41% of

the carcass, so it may be hard to get much more cutout

appreciation without help from those processing items.

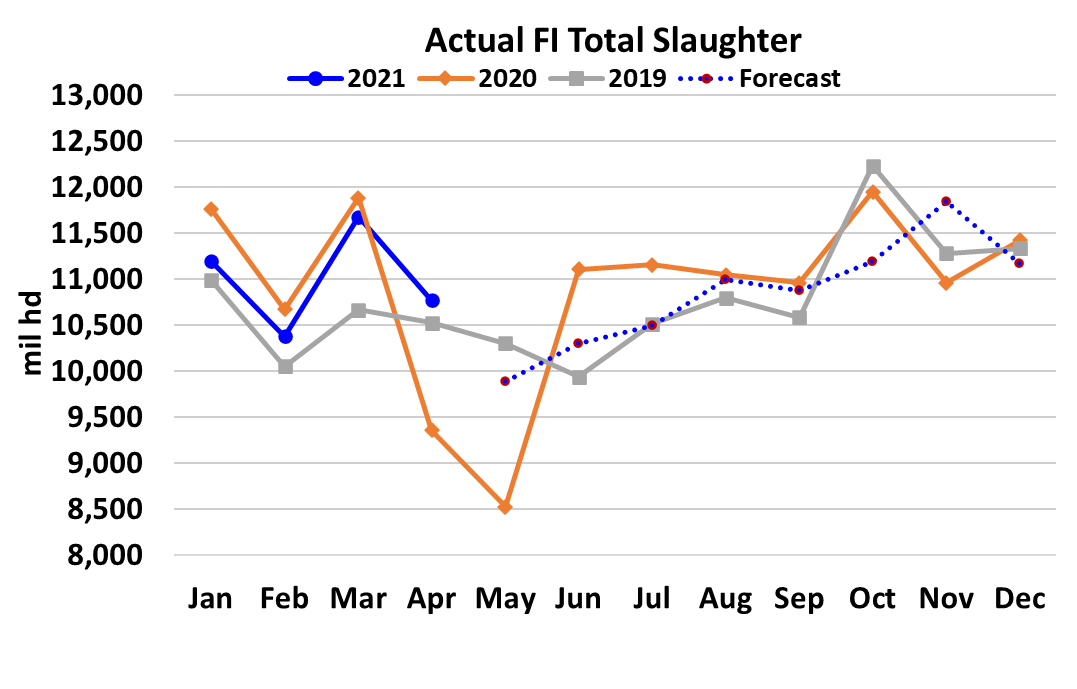

This week’s slaughter came in at 2.39 million head, about flat with

the week before. It’s hard to compare against last year, but

slaughter for this week in 2019 was actually a little smaller than

what was posted this week. Weights are almost identical to where

there were at this point back in 2019. So, there is not much that is

abnormal about the supply picture at this point. Kills usually reach

their annual lows around the end of June, so we have about five

more weeks where slaughter levels should be declining. Based on

the prior pig crop, I’m forecasting the slaughter low point to be

about 2.33 million head. That is only 60k lower than this week’s

slaughter. So the end of shrinking hog supplies is within sight.

The labor problems that are plaguing the beef industry are also

present in the pork industry, but they are having less of an impact

in pork due to where we are in the seasonal supply cycle. That will

change in the fall when hog numbers swell to the annual peak and

it will be interesting to see if pork packer margins blow out to

incredibly high levels, the way beef margins have, when the supply

of animals swells late in the year. My guess is that they will.

Hog producers had better hope that pork packers get their labor

issues sorted out before Q4 gets here. The recent pullback in the

corn market has given hog producers a little relief, but the futures

are still projecting breakevens this fall in the mid-$80s. That is

about where the Dec contract finished this week. Next week,

watch for some softening in the retail primals and possibly the

cutout. It could be a down week if the cutout loses ground next

week. Stratospheric markets like the one we are in now need to be

constantly fed bullish news in order to keep climbing.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}