Pork Wrap May 7

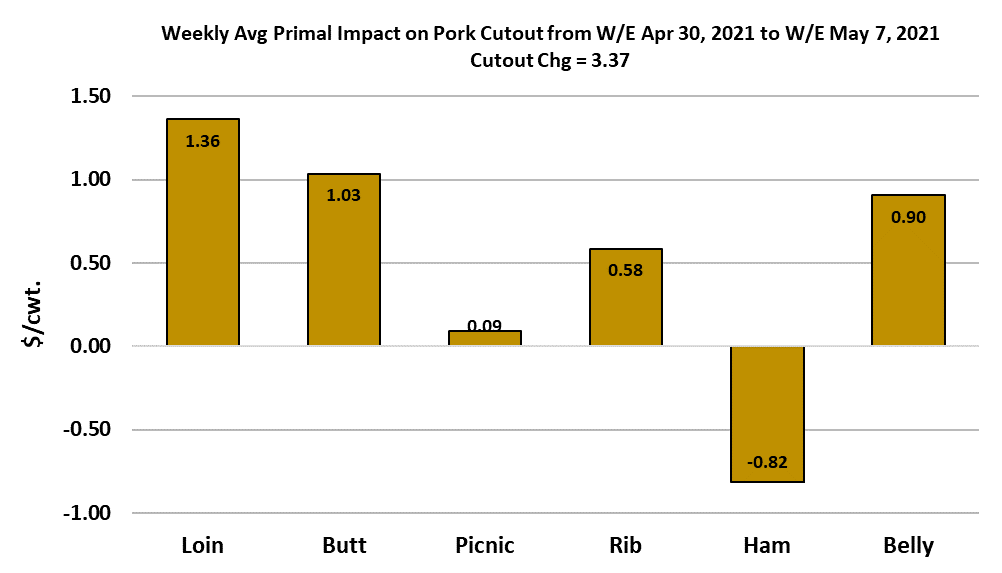

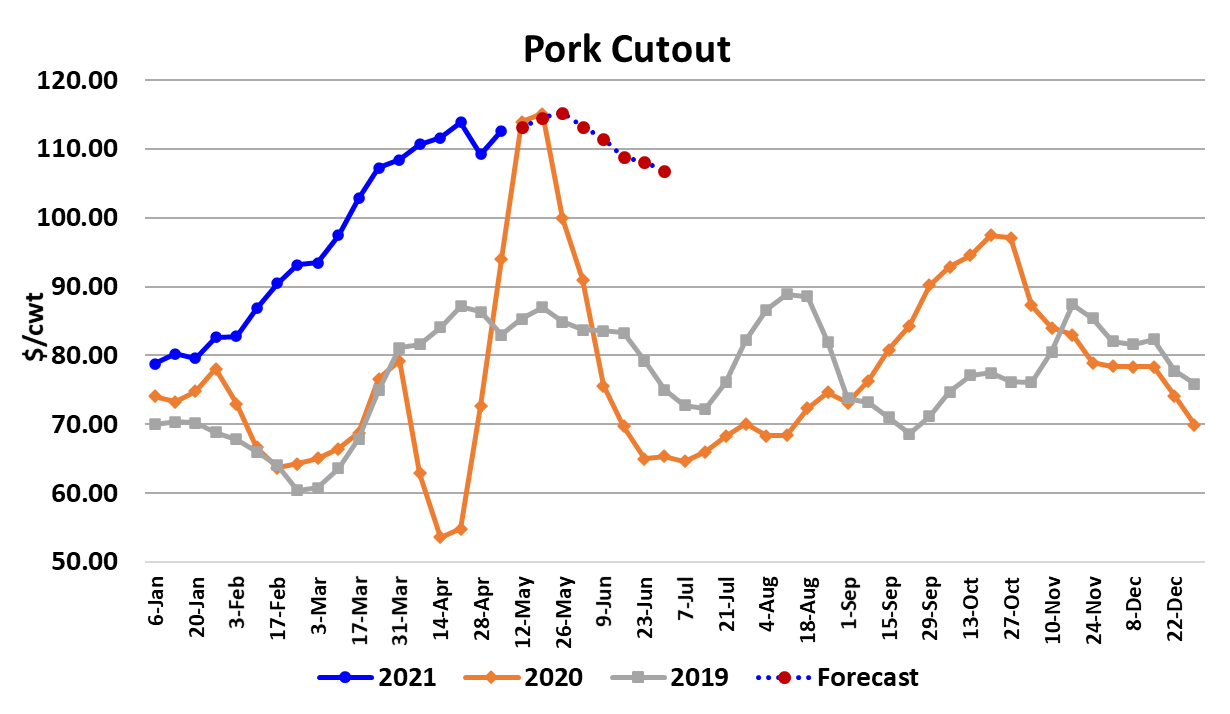

The cutout turned back higher this week, adding $3.36 on a weekly

average basis. Cash hogs also moved higher, with the WCB

negotiated market up $4.68. The turnaround in the cutout was helped

along by some modest improvement in belly prices, which had been a

source of softness over the last couple of weeks. The belly primal

added about $5 on the week. The rest of the carcass continues to look

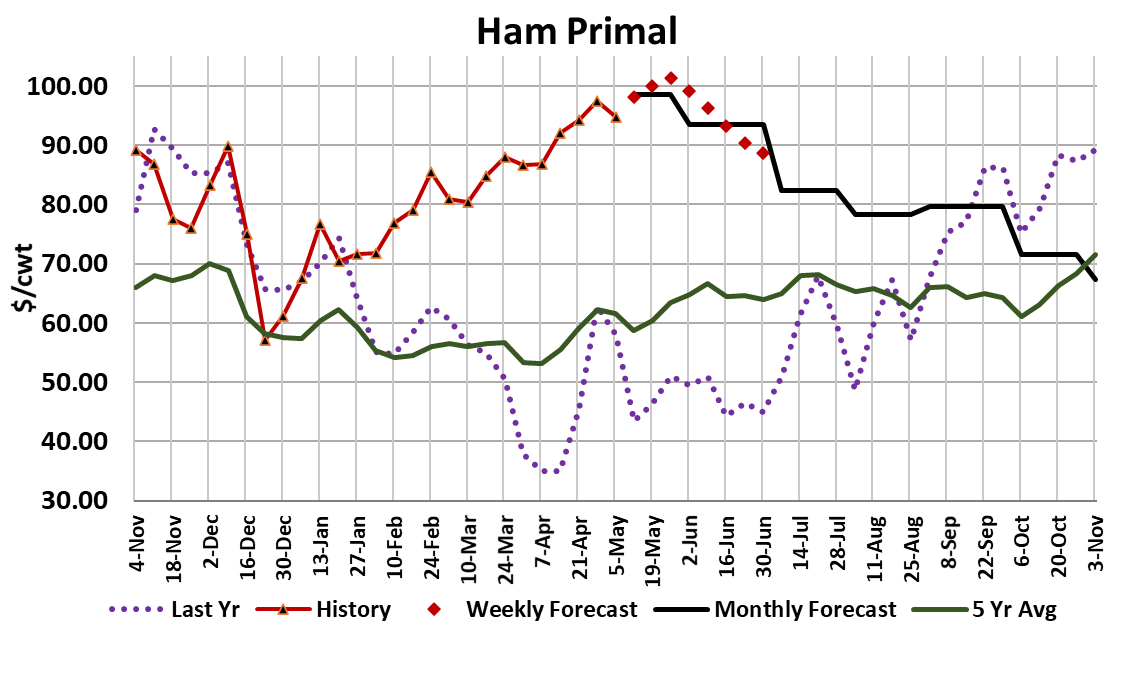

strong, with the exception of the hams.

The ham primal was down about $3 on the week, but I don’t want to

conclude that the hams are going to enter into a long-run downtrend. I

think it is probably just a bit of a breather for the hams, much like the

bellies just took and soon processors will be back to bidding them up.

I’ve got the ham primal forecasted to peak at just over $100 ahead of

Memorial Day and after that they should start to work lower. Packer

margins improved this week to about $6/head, but that is inflated

somewhat by the fact that the full impact of the higher negotiated hog

market hasn’t yet been registered into the LHI. Once that happens, I’d

look for margins to be closer to $4/head. This rapid compression in

margins has definitely caught packer’s attention and this week they

responded by slashing the Saturday kill down to a mere 15,000 head.

That moved the weekly total down to 2.41 million head. I’m sure they

are hoping that will boost the cutout next week and I suspect they are

right on that. Cutting the kill right in the midst of prime grilling season

demand is going to force some pork buyers to pay more than they

would like. Another side effect of cutting back on the kill is that it might

cool down the red-hot cash hog market. It dipped a little on Friday, but

my guess is that it would take several weeks of constrained kills to

have a material impact on cash hogs. Hog weights finally printed lower

this week, with barrow and gilt weights down one pound to 214. As of

today, the weather forecast holds cooler-than-normal temperatures

throughout the midsection of the country for the next week or so and

that should be supportive to hog weights in the near term.

However, hot weather is inevitable as we head into summer and that

will start to push weights lower and become a drag on overall pork

production for the next 2-3 months. With the arrival of June, the

industry will begin killing the Dec/Feb pig crop, which was estimated to

be down 3% from last year. So, both hog numbers and hog weights

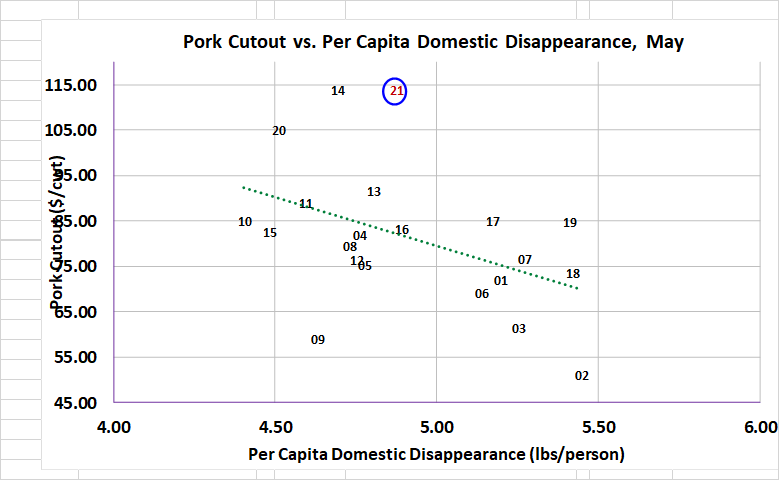

are moving in the direction of tighter pork production. Demand remains

phenomenal. Just look at the scatter diagram below for the month of

May. The 2021 data point is actually further off of the regression line

than the point for 2014 when the industry was dealing with sharply

reduced production due to PEDv. With supply shrinking and demand

super strong, I was forced to raise price forecasts yet again this week.

I’ve now got the cutout continuing to work higher until just after

Memorial Day, when I would expect some of the seasonal

demand pressure to let up and thus prices could start to erode

some. I don’t think the market is going to go into a large-scale

freefall however. There are just too many buyers out there that

are in hand-to-mouth mode right now and those will be greatly

tempted to step into the market on even a modest price decline.

In fact, after this week’s forecast revisions, I now have the cutout

holding above $100 until mid July. I also dialed up the demand

forecasts through the remainder of the year, because it has

become abundantly clear that this strong demand environment is

going to last much longer than originally envisioned.

The combined margin, which I use to quantify demand cycles,

turned unexpectedly higher this week after posting a sharp

downturn last week. That also factored into the decision to push

demand higher over the next few months. However, even after

increasing the demand index forecasts for the second half of

2021, the deferred futures still look way too rich. I guess futures

traders are looking for way stronger demand than I am, or else

they expect a much brighter export picture in the second half of

the year because supplies for the balance of 2021 are fairly easy

to project at this point. Some of the enthusiasm for deferred hogs

may be arising from a commodity price inflation play.

Prices of all commodities, except cattle, are now quite elevated.

Corn seems to be leading the way, with the nearby May contract

settling at $7.72/bushel today. With feed prices so high, hog

producers will need to see hog pricing this fall much stronger than

normal in order to avoid financial disaster. The hog futures

market is offering them that opportunity right now and they can

hedge very strong pricing right through Q1 of next year. The

official export data for March was released this week and it

showed a 3.9% gain over last year’s strong number. That was

bigger than what I had dialed in, but not large enough to explain

the strength in hog prices that we saw in March.

China is still buying a lot of US pork, but it is their appetite for US

beef that is capturing all of the attention lately. Next week, watch

the ham primal for some firming up after this week’s setback and

keep an eye on the daily kills for indications that packers feel like

they need to do more than just cut out the Saturday kill in order to

improve their margin.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}