Beef Wrap November 7

No PDF

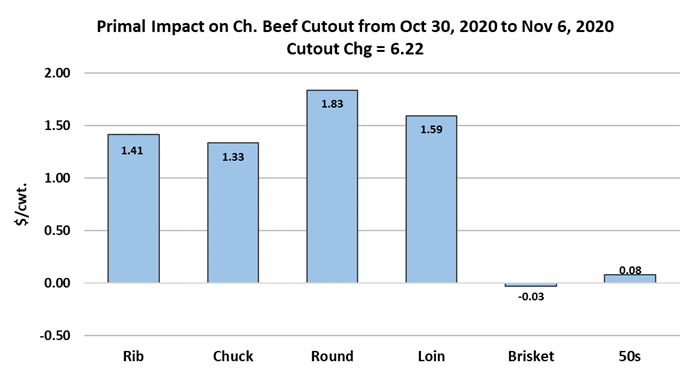

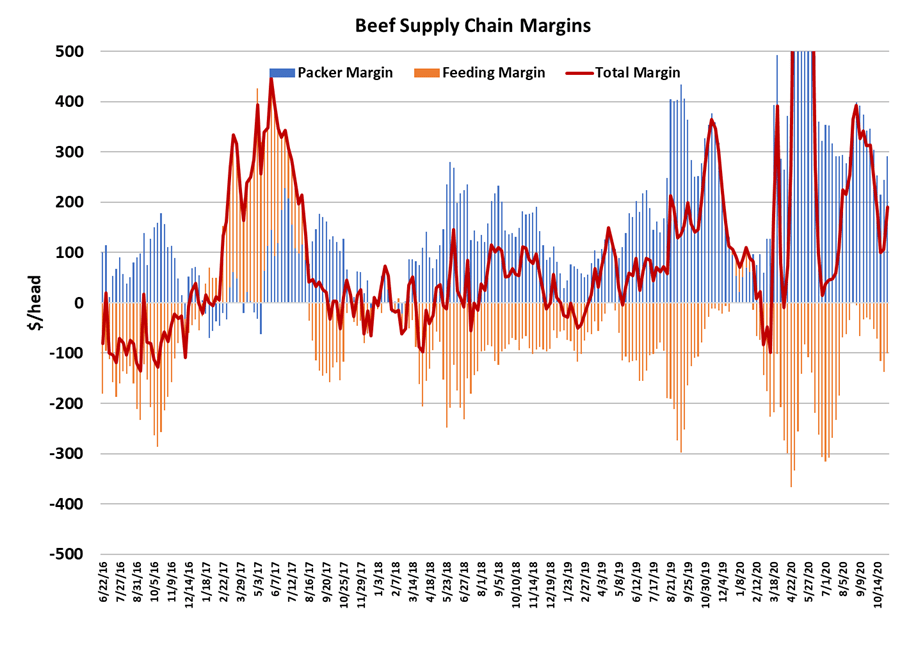

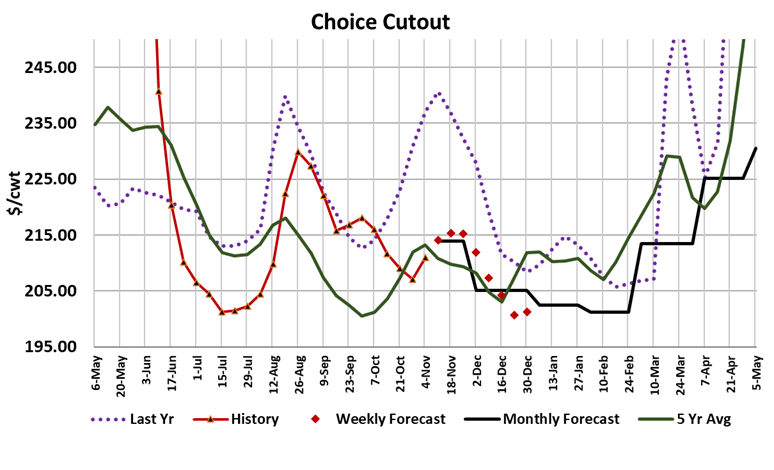

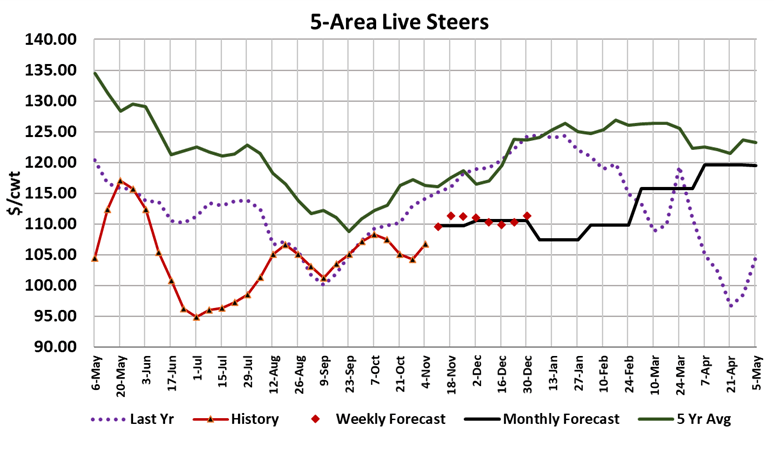

The cash cattle market advanced again this week to $107, up $1 from last week. Interestingly, cash trade in the North was also $107 which brings that region back on par with the South now. Perhaps the supply situation in the North is not as burdensome as it has been. The boxes performed well this week also, with the Choice gaining $6.22 Friday-to- FridayandtheSelectup$7.25. Thelong-awaitedholidayrallyinthe middle meats seems to be underway now, with the Choice Rib primal finishing today over $400, up about $12 from the week before. Gains in the end meats have come mostly from the rounds, but the chucks look like they are beginning to see improved interest. Briskets are soft and not helping the cutout at all. Trim remains very soft, with the 50s mired in the mid $30s for most of the week. There was a little uptick in the 90s, but these remain relatively weak in a historical context. The improvement in the cutouts allowed packer margins to expand back out tocloseto$300/hd. Thatgivespackersmoreroomtopayupforcattle next week and I wouldn’t rule out a $2 advance to $109 given that packers have a big forward book that they need to deliver on. Fed cattle kills remain subdued, as expected, due to light placements during the spring. The fed kill this week was estimated at 508k, up 8k from last week.

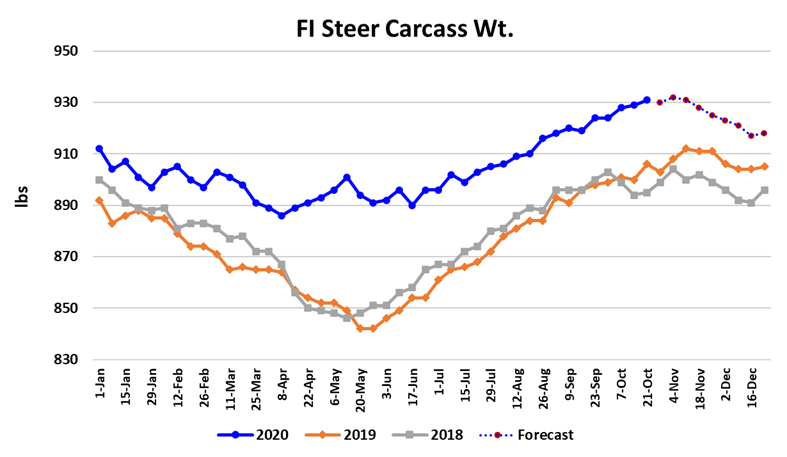

Thisholeinplacementsisbeingfilledinwithbackloggedcattle and will help cattle feeders get more current in the next few weeks. Carcass weights are still very heavy, with steers clocking in 25 pounds heavier than last year (+2.8%), but the blended steer and heifer carcass weight is only 20 pounds heavier than last year (+2.3%). Weights should be very near a top and will soon start to trend lower towards a bottom in April. The weather seems to have calmed down a bit in cattle feeding country and the forecast for the next week or so looks mild and dry, so that might delay the top in carcass weights a bit. But all in all, the supply side of the cattle market looks pretty manageable at present. The demand side of the market continues to improve and this is illustrated in the combined margin chart below. Beef demand is clearly in an upcycle that will probably last into early December. As demand works higher, so should the cutouts and cash cattle prices. After going through the fundamental forecasts this week, I’ve got the Choice cutout topping somewhere around $215-216 during Thanksgiving week, but do admit that the risk to that forecast lies to the upside. Cash cattle should toparoundthesametimeinthe$111-112range. AswemoveintoQ1, the supply side is likely to turn more negative since placements during the Aug-Sep timeframe were up an average of 8.7% YOY and those are the cattle that will get slaughtered in Q1. It does look like cattle feeders pulled back on placements during October and that could start to provide some supply relief by the time the Apr contract expires.

Of course, bigger supply does not guarantee lower pricing in Q1 sincewehavetotakedemandintoaccount. JanuaryandFebruary are typically weak demand months and this time around we will havearecessionontopofthat. Congresscouldcomethroughwith some stimulus money, but that might not hit consumer’s pocketbooks until mid-February or later. The covid crisis is getting worse, not better, and if it stays that way into Q1, it will be a drag on alreadyweakdemand. Avaccinecouldbecomeavailablebythefirst of the year, but it will take many months to get enough of the populationvaccinatedtomakeadifference. Italsolookslikewewill haveanewpresidentialadministrationcomeJan20. New presidents usually hit the ground running with a long list of things to accomplish. However, the Democrats may not have complete control of Congress so obstruction by Republicans in the Senate could hamper new legislation and perhaps even the stimulus deal. So there are a lot of reasons to expect demand to be weak in Q1 and when you combine that with nearly 9% larger cattle supplies and weights that could still be heavier than last year, it paints a bleak pictureforbeefprices. I’vegotQ1demanddownabout3%fromlast year, but last year the demand index was as high as it has ever been during Q1. Part of that strength stems from the consumer stockpiling event that happened last March, so if you take that out, then maybe I’m only down 2% on Q1 demand from pre-pandemic levels. Maybe that’s not enough. I’m currently forecasting the Choice cutout to average around $201 for Jan/Feb, but again if I’m too optimistic on demand then maybe something in the mid $190s would be more appropriate. Of course, winter is not here yet and if the weather gets nasty then all bets are off and prices will likely come in well above my forecast. Weather markets normally only happen about 2 out of 10 years, so the odds favor a mild winter but global weather has been so unsettled in the past few years that it might make sense to expect more adverse weather events than we have seen historically. That goes for droughts as well as winter storms and a good chunk of Western US is currently in a severe drought. There is always a risk that drought will spread to the Corn Belt next spring and jack corn prices even higher than they are now. The mis-pricing chart indicates that most of the opportunity in the futures lies on the long side at the moment, but the market has been steadily working higher and steadily removing the under-pricing. Next week, watch for further gains in the middle meats to advance the cutouts and keep an eye on the Thursday weight data for signs that carcass weights are finally making a top.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}