Beef Wrap September 13

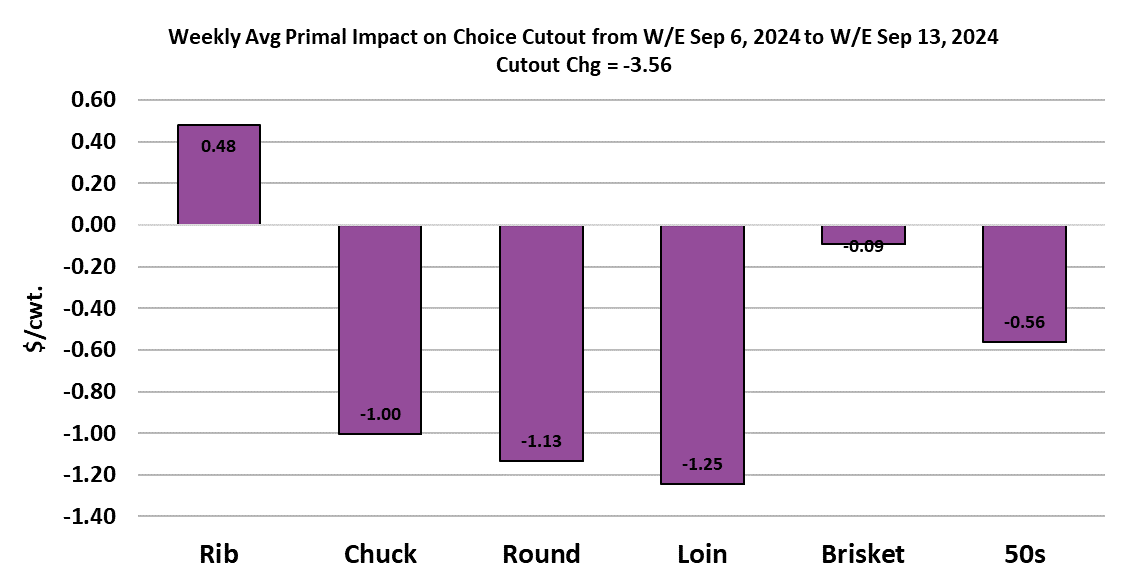

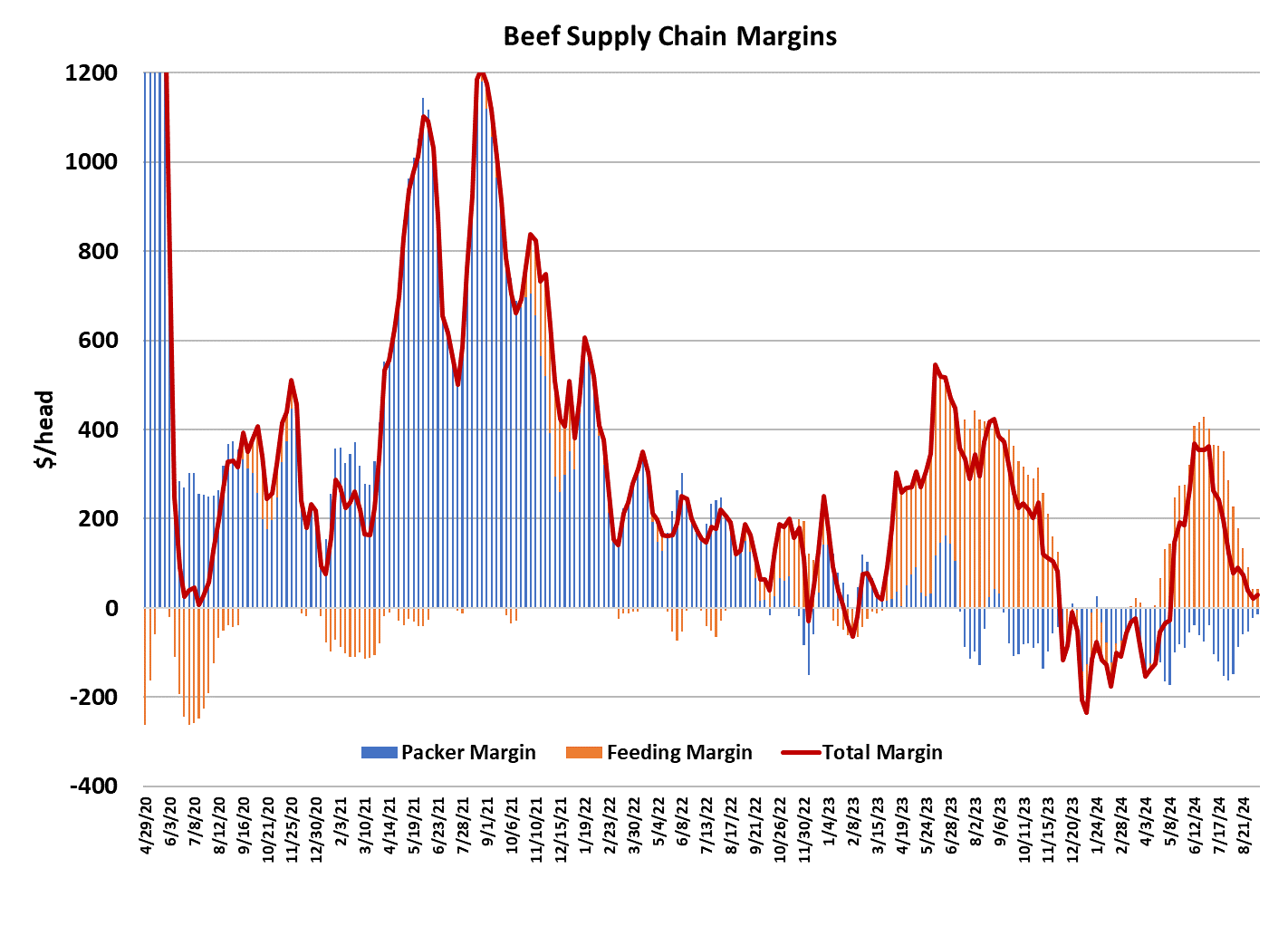

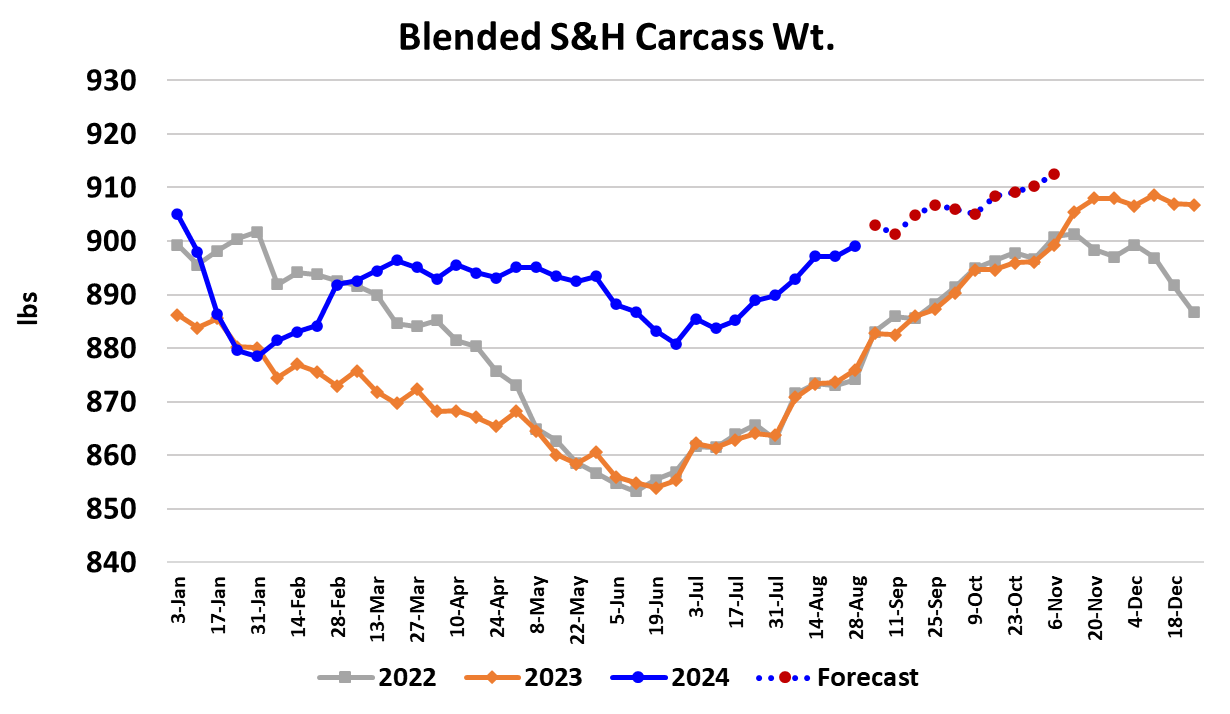

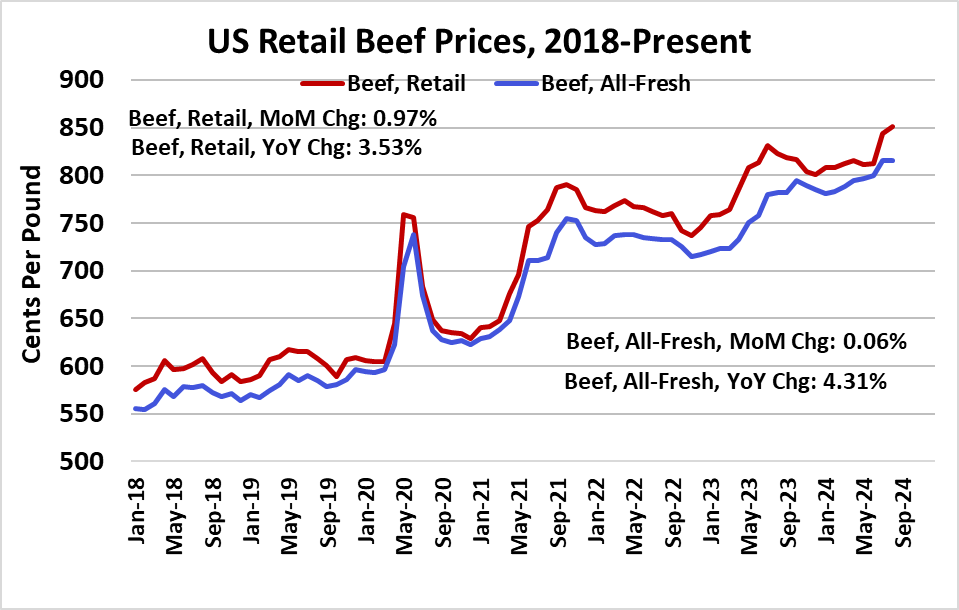

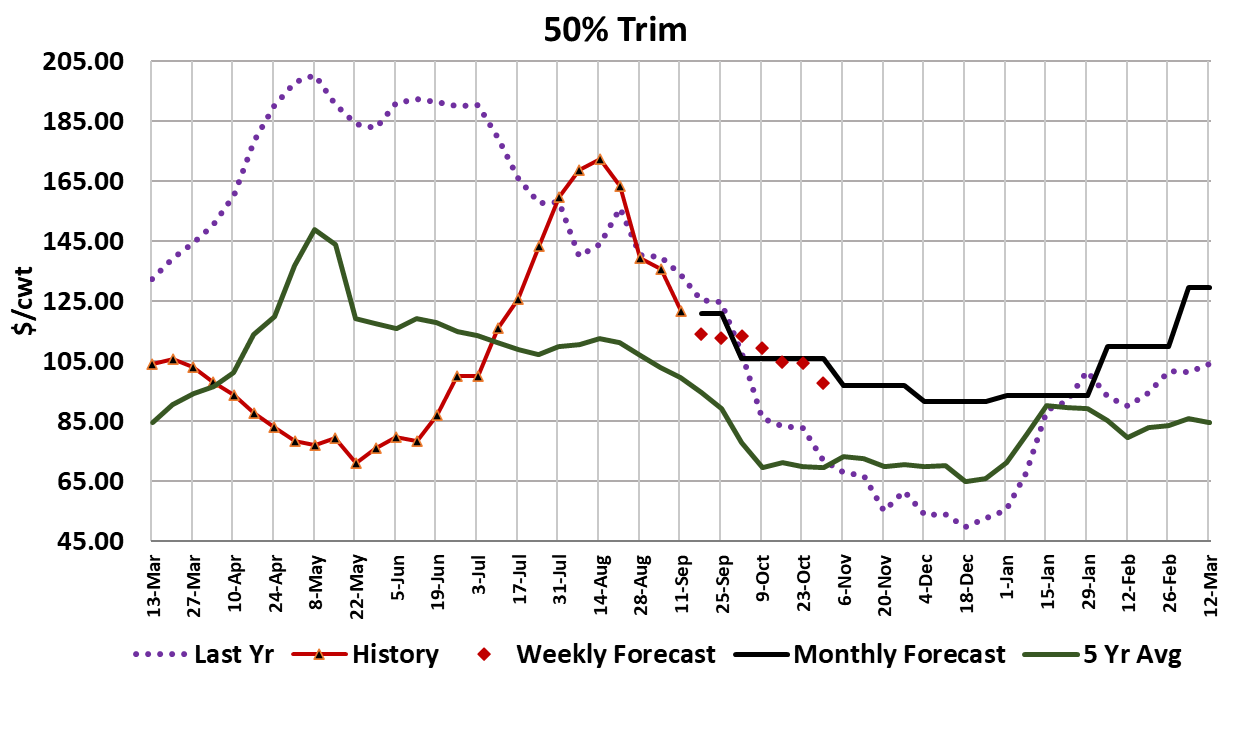

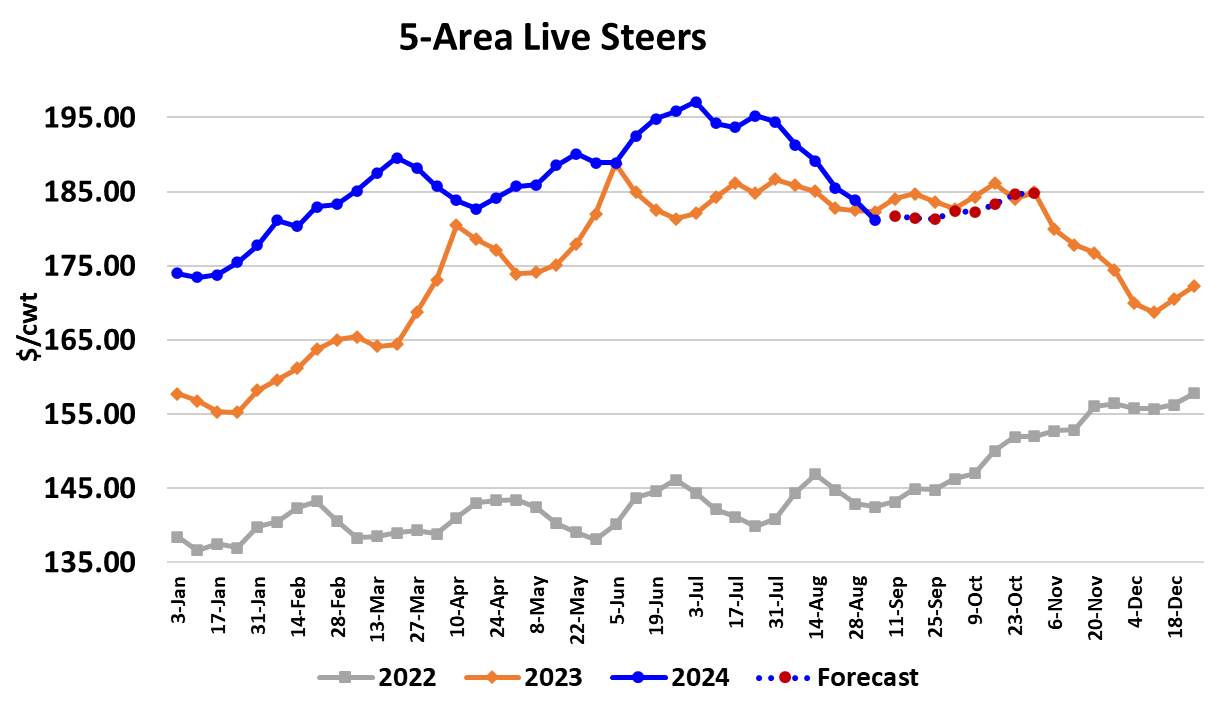

The cash cattle market finally stabilized this week with prices in the South steady at mostly $181 and prices in the North a little higher at $181-182. When the dust settles and all of the data is in, I’m looking for the 5-area average to be near $181.75, which would be up about $0.50 from the week before. The cutouts didn’t fare quite as well, with the Choice dropping $3.56 on a weekly average basis and the Select losing $2.16. The cutouts were pushed lower by some easing in end meat prices which corresponded with some softening in the price of 90s. It looks like finally the seasonal softening in lean beef prices is taking hold. That said, the 90s only lost about $2 this week on average, so the decline isn’t very steep. This is the time of year when non-fed (cow and bull) slaughter starts to increase seasonally as cow-calf operators begin to cull low-producing animals ahead of winter in order to save on hay and supplemental feed costs. USDA estimated this week’s non-fed slaughter at 121,000 head, which exceeded expectations and is the largest weekly non-fed kill since April. My expectations are for culling rates to be down this fall since producers likely had much better hay production this summer and may be thinking about expanding their herds by culling fewer animals than normal this fall. The forecast has non-fed slaughter topping out around 135,000 head per week near the end of November, which would be well below the 150,000 head top experienced last fall. That should keep supplies of domestic 90s fairly snug so users looking for big price concessions this fall could be disappointed. This week’s fed kill clocked in at 499k, the same as it was just prior to Labor Day week, so it appears that packers are picking back up right where they left off. At that rate, it is unlikely that any cattle are being backlogged and if packers continue to run fed kills near 500k during the balance of September it will likely make feedyards a little more current and thus help move the cash cattle market a little higher. What would make packers want to keep the kill elevated in the weeks to come? The simple answer is margins, which are estimated to be only about $10/head in the red this week. That is the best margin so far in 2024, but I don’t expect it will last very long. Beef prices are sliding seasonally lower and cash cattle look like they may be poised to advance, so margins could come back under pressure in the next few weeks. Cattle feeding margins are positive by about $40/head at the moment and it looks like that could improve over the near-term as breakevens are projected to move a little lower during October and cash cattle prices could move a little higher. Even though beef prices are moving lower at the moment, that is mostly a seasonal phenomenon and by early October we should see demand start to improve as buyers begin to source product in anticipation of the year-end holidays. This week, the rib was the only primal that saw higher pricing and that was a bit of a surprise since ribs normally set back a bit after Labor Day before they make their holiday run. It may be a sign that demand for middles is a little better than anticipated and if that continues into the holidays the cutout forecasts will likely need to be raised, although it might still be a very tall order for ribs to match last year’s fall highs. The 50s took another big step down this week, averaging close to $122, down about $14 on the week. Seasonally increasing carcass weights, along with softer demand for grinds at this time of year is likely responsible. The forecast has 50s dipping below the $100 mark near the end of October. The combined margin ticked a little higher this week and is just above the zero mark, so may be getting close to the end of this most recent downcycle in demand. The cutouts should continue to slowly ease over the next few weeks, but its unlikely that the Choice will dip much below $300 for any length of time. USDA provided retail beef prices for August this week and there was a fairly sharp increase in the traditional retail price series, while the “all-fresh” retail price, which captures features that the traditional series does not, was only up slightly. Nonetheless the average price of beef is now approaching $8.50/lb. and consumers still seem to be enamored with it. Consumer confidence was reported a little better this week and there are signs that inflation is starting to fade a bit from consumer’s minds. That can only help beef demand. In addition, next week the Fed is widely expected to begin cutting interest rates and the stock market is back near all-time highs in anticipation of that move. That should have consumers in a better mood as we head into fall. Next week, look for the cutouts to lose a little more ground and the cash cattle market to hold steady or perhaps advance a little bit.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}